Università degli studi di Paviaeconomia.unipv.it/pagp/pagine_personali/lbigogno/Lesson 13 IAS...

38

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 13 International Accounting Lelio Bigogno, Stefano Santucci 1

Transcript of Università degli studi di Paviaeconomia.unipv.it/pagp/pagine_personali/lbigogno/Lesson 13 IAS...

Università degli studi di PaviaFacoltà di Economia

a.a. 2013-2014

Lesson 13 International Accounting

Lelio Bigogno, Stefano Santucci

1

IAS/IFRS: IAS 37 Provisions,Contingent Liabilities andContingent Assets

2

History of IAS 37

� August 1997 Exposure Draft E59Provisions, Contingent Liabilities andContingent Assets

� September 1998 IAS 37 Provisions,Contingent Liabilities and ContingentAssets

� 1 July 1999 Effective date of IAS 37 (1998)� 30 June 2005 Exposure Draft of substantial

revisions to IAS 37

3

History of IAS 37RELATED INTERPRETATIONS

• IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities

• IFRIC 5 Rights to Interests Arising from Decommissioning, Restoration and Environmental Funds

• IFRIC 6 Liabilities Arising from Participating in a Specific Market – Waste Electrical and Electronic Equipment

• IFRIC 17 Distributions of Non-cash Assets to Owners

• Issues Relating to This Standard that IFRIC Did Not Add to Its Agenda

AMENDMENTS UNDER CONSIDERATION BY IASB

Liabilities

4

Objective

The objective of IAS 37 is to ensure thatappropriate recognition criteria andmeasurement bases are applied toprovisions, contingent liabilities andcontingent assets and that sufficientinformation is disclosed in the notes tothe financial statements to enable usersto understand their nature, timing andamount.

5

Objective

The key principle established by theStandard is that a provision should berecognised only when there is aliability i.e. a present obligationresulting from past events.

6

Objective

The Standard thus aims to ensure thatonly genuine obligations are dealt with inthe financial statements. Planned futureexpenditures, even where authorized bythe board of directors or equivalentgoverning body, is excluded fromrecognition.

7

Scope

IAS 37 excludes obligations andcontingencies arising from:

� financial instruments that are in the scopeof IAS 39

� non-onerous executory contracts� insurance company policy liabilities (but IAS

37 does apply to non-policy-relatedliabilities of an insurance company)

8

Scope

� items covered by other IAS. ◦ For example, IAS 11, Construction

Contracts, applies to obligations arisingunder such contracts; IAS 12, IncomeTaxes, applies to obligations for current ordeferred income taxes; IAS 17, Leases,applies to lease obligations; and IAS 19,Employee Benefits, applies to pensionand other employee benefit obligations.

9

Key Definitions

Provision: a liability of uncertain timing or amount.

Liability:� present obligation as a result of past

events� settlement is expected to result in an

outflow of resources (payment)

10

Key Definitions

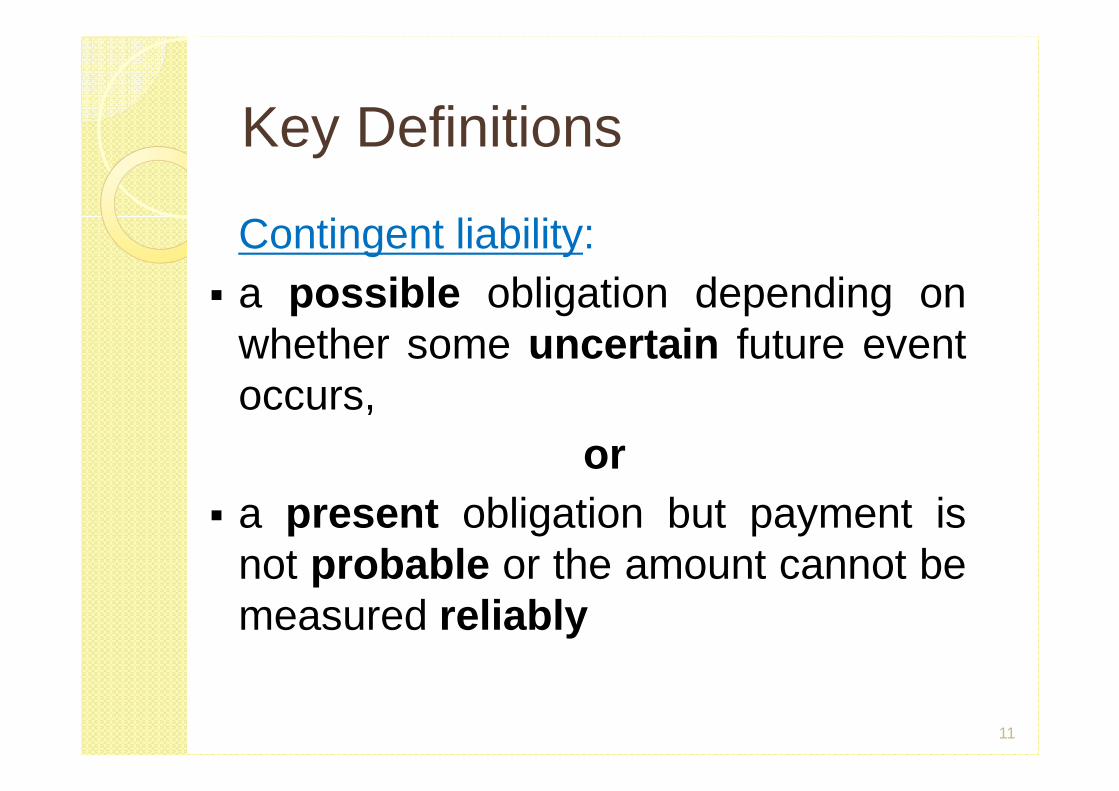

Contingent liability: � a possible obligation depending on

whether some uncertain future eventoccurs,

or� a present obligation but payment is

not probable or the amount cannot bemeasured reliably

11

Key Definitions

Contingent asset:� a possible asset that arises from past

events,and

� whose existence will be confirmedonly by the occurrence or non-occurrence of one or more uncertainfuture events not wholly under thecontrol of the entity.

12

Recognition of a Provision

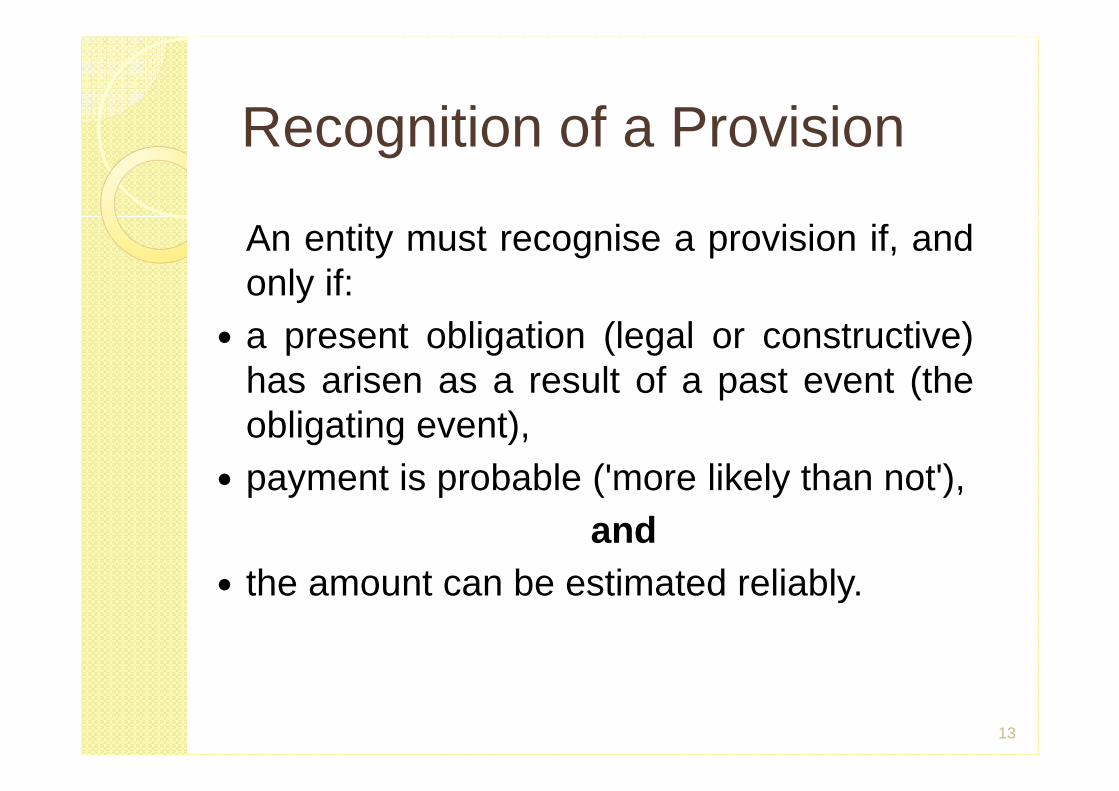

An entity must recognise a provision if, andonly if:

� a present obligation (legal or constructive)has arisen as a result of a past event (theobligating event),

� payment is probable ('more likely than not'),and

� the amount can be estimated reliably.

13

Recognition of a Provision

A constructive obligation arises if pastpractice creates a valid expectation onthe part of a third party, for example, aretail store that has a long-standingpolicy of allowing customers to returnmerchandise within, say, a 30-dayperiod.

14

Recognition of a Provision

An obligating event is an event thatcreates a legal or constructiveobligation and, therefore, results in anentity having no realistic alternativebut to settle the obligation.

15

Recognition of a Provision

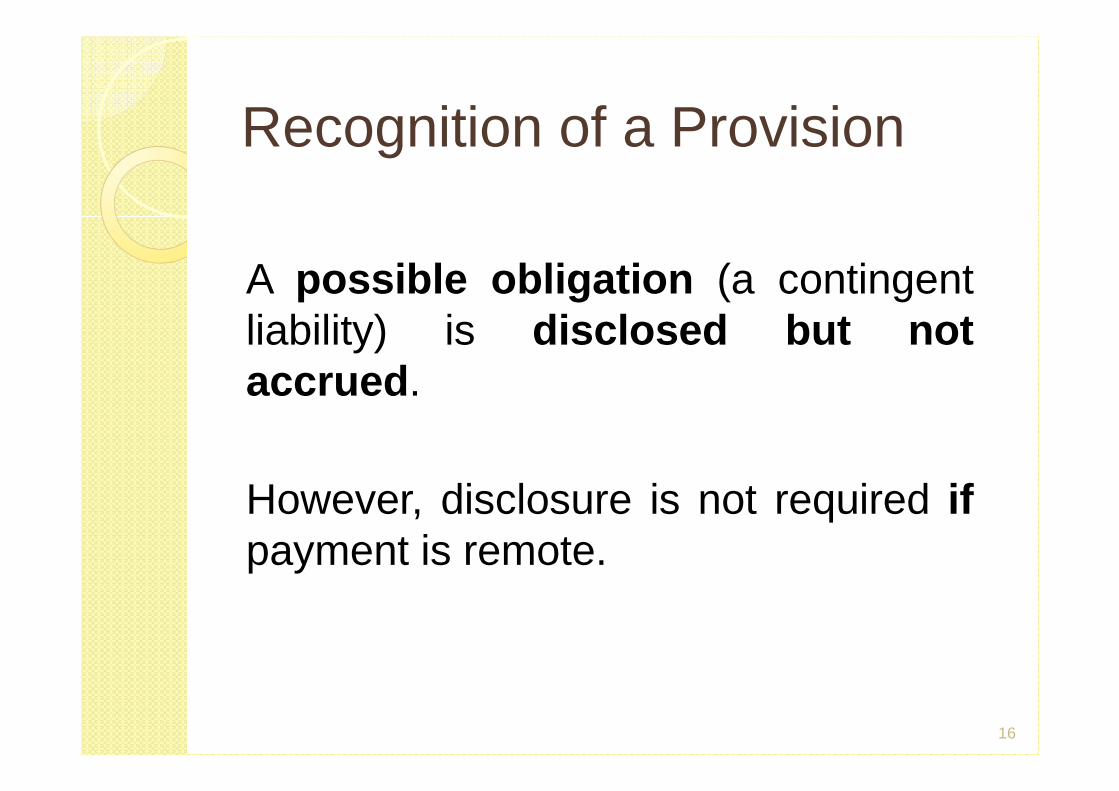

A possible obligation (a contingentliability) is disclosed but notaccrued.

However, disclosure is not required ifpayment is remote.

16

Recognition of a Provision

In rare cases, for example in a lawsuit,it may not be clear whether an entityhas a present obligation.In those cases, a past event isdeemed to give rise to a presentobligation if, taking account of allavailable evidence, it is more likelythan not that a present obligationexists at the balance sheet date.

17

Recognition of a Provision

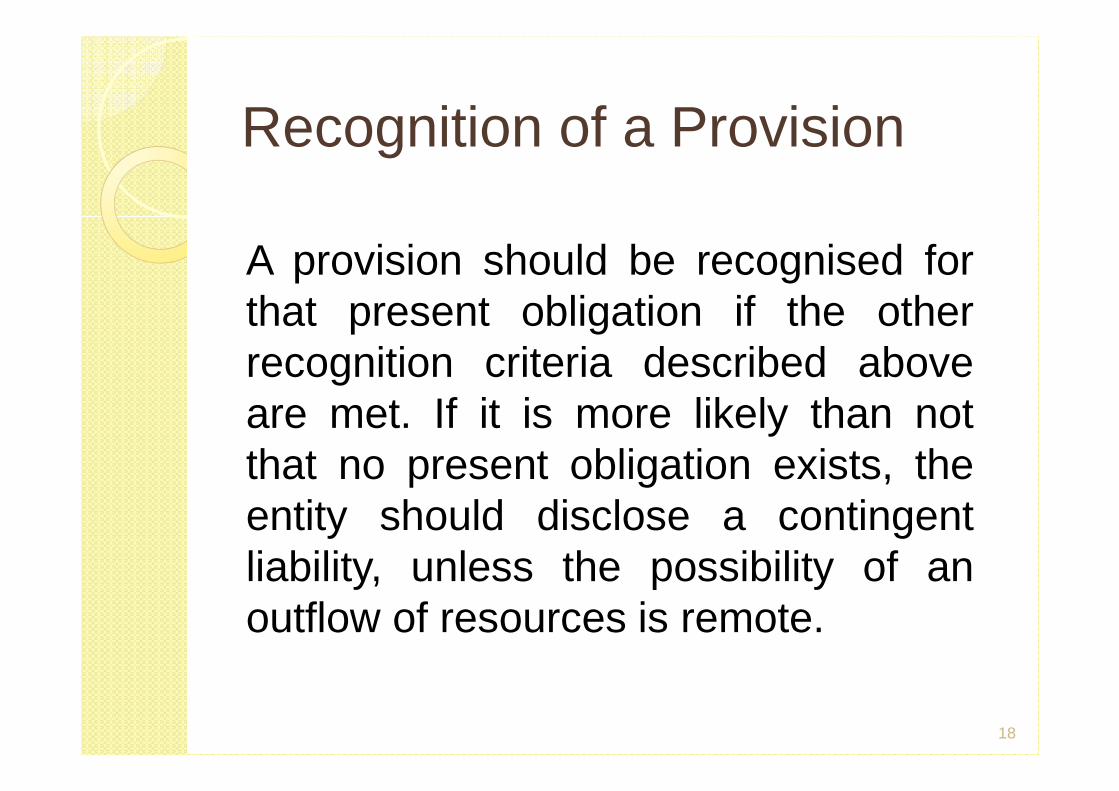

A provision should be recognised forthat present obligation if the otherrecognition criteria described aboveare met. If it is more likely than notthat no present obligation exists, theentity should disclose a contingentliability, unless the possibility of anoutflow of resources is remote.

18

Measurement of Provisions

The amount recognised as a provisionshould be the best estimate of theexpenditure required to settle thepresent obligation at the balancesheet date, that is, the amount that anentity would rationally pay to settlethe obligation at the balance sheetdate or to transfer it to a third party

19

Measurement of Provisions

This means: � Provisions for one-off events

(restructuring, environmental clean-up,settlement of a lawsuit) are measuredat the most likely amount;

� Provisions for large populations ofevents (warranties, customer refunds)are measured at a probability-weighted expected value.

20

Measurement of Provisions

Both measurements are atdiscounted present value using apre-tax discount rate that reflects thecurrent market assessments of thetime value of money and the risksspecific to the liability.

21

Measurement of Provisions

In reaching its best estimate, the entityshould take into account the risks anduncertainties that surround theunderlying events.

22

Measurement of Provisions

If some or all of the expenditure required tosettle a provision is expected to bereimbursed by another party, thereimbursement should be recognised as aseparate asset, and not as a reduction ofthe required provision, when, and onlywhen, it is virtually certain thatreimbursement will be received if the entitysettles the obligation. The amountrecognised should not exceed the amountof the provision.

23

Measurement of Provisions

In measuring a provision consider future events as follows:

� forecast reasonable changes in applyingexisting technology;

� ignore possible gains on sale of assets;� consider changes in legislation only if

virtually certain to be enacted.

24

Measurement of Provisions

Remeasurement of Provisions

1. Review and adjust provisions at eachbalance sheet date;

2. If outflow no longer probable, reverse theprovision to income.

25

Some examples of Provisions

�Restructuring by sale of an operation�Accrue a provision only after a binding sale agreement;

�Restructuring by closure or reorganisation� Accrue a provision only after a detailed formal plan is adopted and announced publicly. A Board decision is not enough;

�Warranty� Accrue a provision (past event was the sale of defective goods)

26

Some examples of Provisions

�Land contamination� Accrue a provision ifthe company's policy is to clean up even ifthere is no legal requirement to do so (pastevent is the obligation and publicexpectation created by the company'spolicy);

�Customer refunds� Accrue if theestablished policy is to give refunds (pastevent is the customer's expectation, at timeof purchase, that a refund would beavailable)

27

Some examples of Provisions

�Offshore oil rig must be removed and seabed restored � Accrue a provision wheninstalled, and add to the cost of the asset;

�Abandoned leasehold, four years to run�Accrue a provision;

�CPA firm must staff training for recentchanges in tax law� No provision (there isno obligation to provide the training);

28

Some examples of Provisions

�Major overhaul or repairs� No provision(no obligation);

�Onerous (loss-making) contract� Accrue aprovision

29

Restructuring

A restructuring is: � sale or termination of a line of business;� closure of business locations;� changes in management structure;� fundamental reorganisation of a company.

30

Restructuring

Restructuring provisions should be accrued as follows:

� Sale of operation: accrue provision onlyafter a binding sale agreement. If thebinding sale agreement is after balancesheet date, disclose but do not accrue;

� Closure or reorganisation: accrue onlyafter a detailed formal plan is adopted andannounced publicly. A board decision is notenough.

31

Restructuring

� Future operating losses: provisionsshould not be recognised for futureoperating losses, even in a restructuring;

� Restructuring provision on acquisition:accrue provision only if there is anobligation at acquisition date.Restructuring provisions should includeonly direct expenditures caused by therestructuring, not costs that associated withthe ongoing activities of the entity.

32

What Is the Debit Entry?

�When a provision (liability) isrecognised, the debit entry for aprovision is not always an expense;

�Sometimes the provision may formpart of the cost of the asset.Examples: obligation forenvironmental cleanup when a newmine is opened or an offshore oil rig isinstalled.

33

Use of Provisions

�Provisions should only be used for thepurpose for which they were originallyrecognised.

�They should be reviewed at each balancesheet date and adjusted to reflect thecurrent best estimate. If it is no longerprobable that an outflow of resources willbe required to settle the obligation, theprovision should be reversed.

34

Contingent Liabilities

Since there is common ground asregards liabilities that are uncertain,IAS 37 also deals with contingencies.It requires that entities should notrecognise contingent liabilities - butshould disclose them, unless thepossibility of an outflow of economicresources is remote.

35

Contingent Assets

Contingent assets should not berecognised - but should be disclosedwhere an inflow of economic benefitsis probable. When the realisation ofincome is virtually certain, then therelated asset is not a contingent assetand its recognition is appropriate.

36

DisclosuresReconciliation for each class of provision: � opening balance � additions � used (amounts charged against the

provision) � released (reversed) � unwinding of the discount � closing balance A prior year reconciliation is not required.

37

Disclosures

For each class of provision, a briefdescription of:

� nature� timing� uncertainties� assumptions� reimbursement, if any.

38