Università degli studi di...

78

Università degli studi di Pavia Università degli studi di Pavia Università degli studi di Pavia Università degli studi di Pavia Facoltà di Economia Facoltà di Economia a.a. a.a. 2014 2014-2015 2015 Lesson 10 International Accounting Lelio Bigogno, Stefano Santucci 1

Transcript of Università degli studi di...

Università degli studi di PaviaUniversità degli studi di PaviaUniversità degli studi di PaviaUniversità degli studi di PaviaFacoltà di EconomiaFacoltà di Economia

a.a.a.a. 20142014--20152015

Lesson 10 International Accounting

Lelio Bigogno, Stefano Santucci

1

IAS/IFRS: IAS/IFRS: IFRSIFRS 3 Business 3 Business CombinationCombination

2

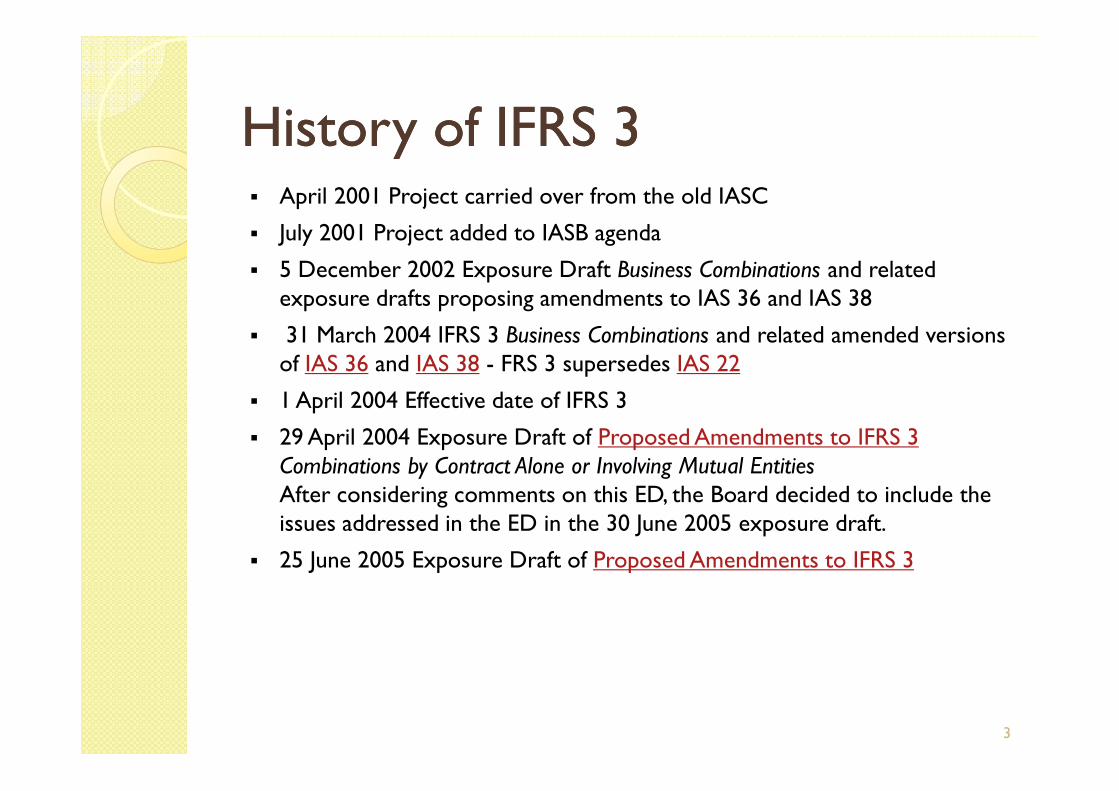

HistoryHistory of IFRS 3of IFRS 3� April 2001 Project carried over from the old IASC

� July 2001 Project added to IASB agenda

� 5 December 2002 Exposure Draft Business Combinations and related exposure drafts proposing amendments to IAS 36 and IAS 38

� 31 March 2004 IFRS 3 Business Combinations and related amended versions of IAS 36 and IAS 38 - FRS 3 supersedes IAS 22

� 1 April 2004 Effective date of IFRS 3 � 1 April 2004 Effective date of IFRS 3

� 29 April 2004 Exposure Draft of Proposed Amendments to IFRS 3Combinations by Contract Alone or Involving Mutual EntitiesAfter considering comments on this ED, the Board decided to include the issues addressed in the ED in the 30 June 2005 exposure draft.

� 25 June 2005 Exposure Draft of Proposed Amendments to IFRS 3

3

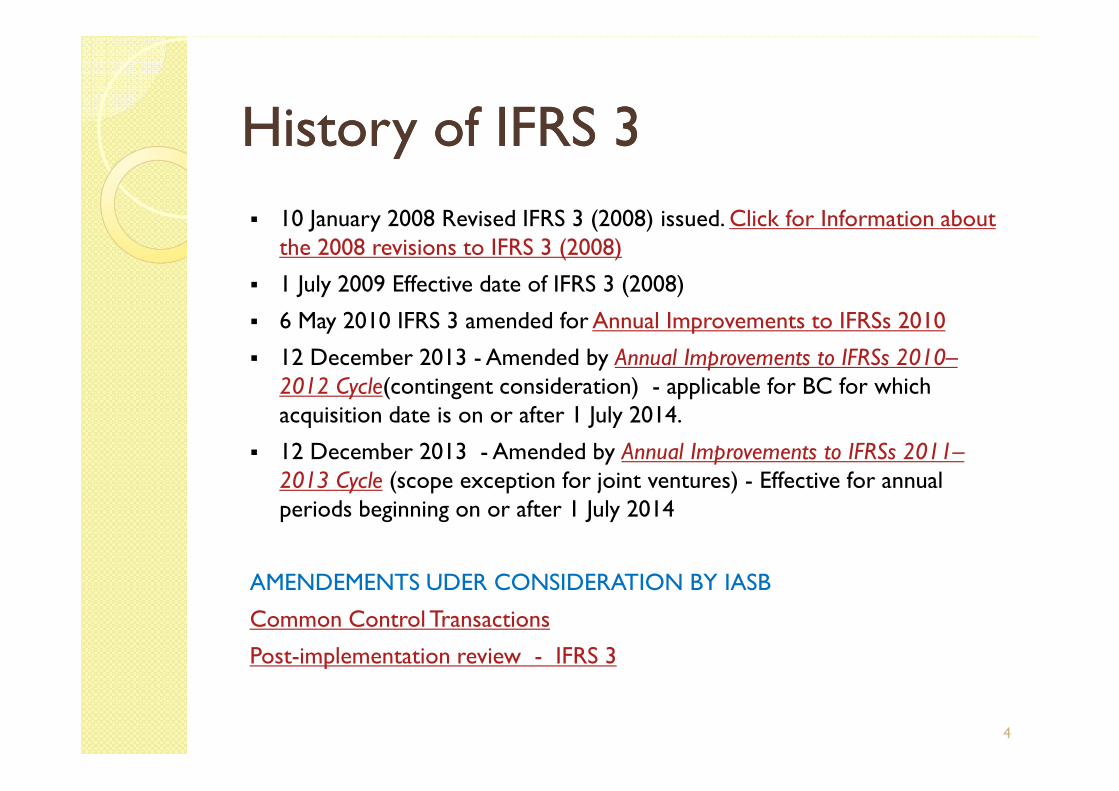

HistoryHistory of IFRS 3of IFRS 3

� 10 January 2008 Revised IFRS 3 (2008) issued. Click for Information about the 2008 revisions to IFRS 3 (2008)

� 1 July 2009 Effective date of IFRS 3 (2008)

� 6 May 2010 IFRS 3 amended for Annual Improvements to IFRSs 2010

� 12 December 2013 - Amended by Annual Improvements to IFRSs 2010–2012 Cycle(contingent consideration) - applicable for BC for which 2012 Cycle(contingent consideration) - applicable for BC for which acquisition date is on or after 1 July 2014.

� 12 December 2013 - Amended by Annual Improvements to IFRSs 2011–2013 Cycle (scope exception for joint ventures) - Effective for annualperiods beginning on or after 1 July 2014

AMENDEMENTS UDER CONSIDERATION BY IASB

Common Control Transactions

Post-implementation review - IFRS 3

4

Key Key DefinitionsDefinitions

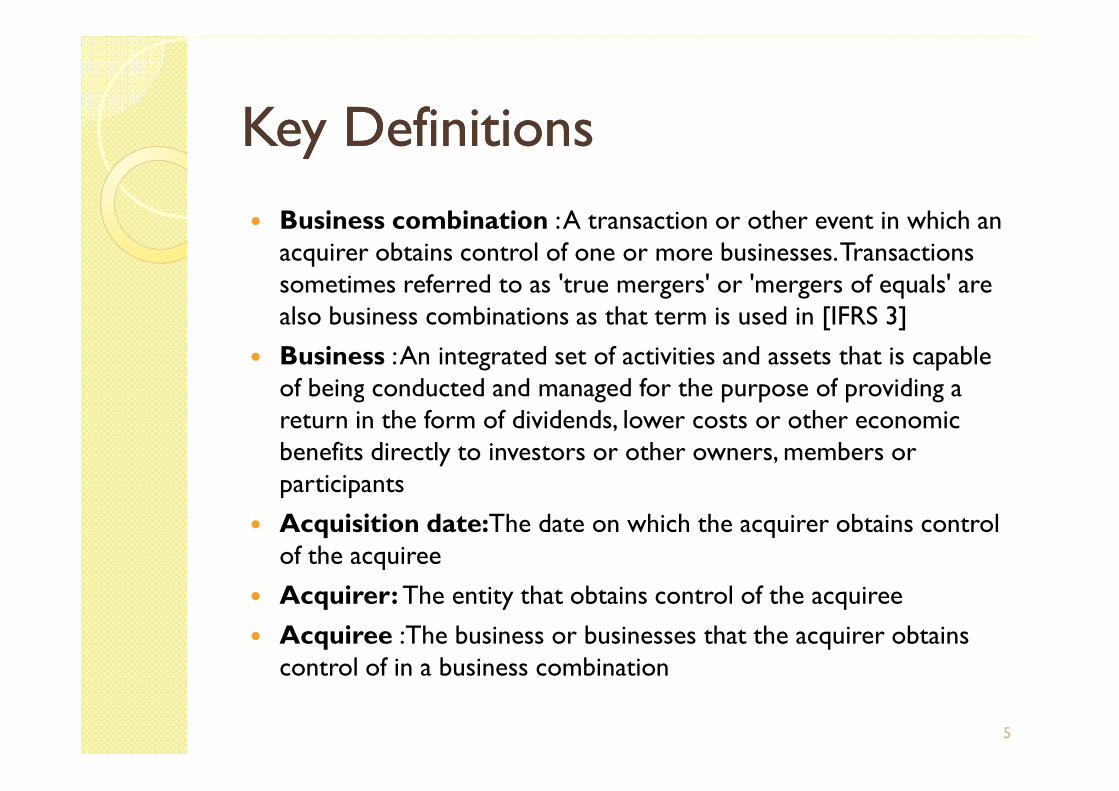

� Business combination : A transaction or other event in which anacquirer obtains control of one or more businesses. Transactionssometimes referred to as 'true mergers' or 'mergers of equals' are also business combinations as that term is used in [IFRS 3]

� Business : An integrated set of activities and assets that is capableof being conducted and managed for the purpose of providing a of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs or other economicbenefits directly to investors or other owners, members or participants

� Acquisition date:The date on which the acquirer obtains controlof the acquiree

� Acquirer: The entity that obtains control of the acquiree

� Acquiree :The business or businesses that the acquirer obtainscontrol of in a business combination

5

ScopeScope

IFRS 3 must be applied when accounting forfor

business combination

6

ScopeScope

but does not apply to:

� The formation of a joint venture*

� The acquisition of an asset or group of assets� The acquisition of an asset or group of assetsthat is not a business, although general guidanceis provided on how such transactions should beaccounted for

* Annual Improvements to IFRSs 2011–2013 Cycle, effective for annual periods beginning

on or after 1 July 2014, amends this scope exclusion to clarify that is applies to theaccounting for the formation of a joint arrangement in the financial statements ofthe joint arrangement itself

7

ScopeScope

� Combinations of entities or businesses under common control (the IASB has a separate agenda project on common controltransactions) transactions)

� Acquisitions by an investment entity of a subsidiary that is required to be measured at fair value through profit or loss under IFRS 10 Consolidated Financial Statements.

8

DeterminingDetermining whenwhen a a transactiontransaction isis a a BCBC

IFRS 3 provides additional guidance on determining whether a transaction meets the definition of a business combinationdefinition of a business combination

9

DeterminingDetermining whenwhen a a transactiontransaction isis a a BCBC

This guidance includes:

� Business combinations can occur in variousways, such as by transferring cash, incurringBusiness combinations can occur in variousways, such as by transferring cash, incurringliabilities, issuing equity instruments (or anycombination thereof), or by not issuingconsideration at all (i.e. by contract alone)

10

DeterminingDetermining whenwhen a a transactiontransaction isis a a BCBC

� Business combinations can be structured in various ways to satisfy legal, taxation or otherobjectives, including one entity becoming a subsidiary of another, the transfer of net assetssubsidiary of another, the transfer of net assetsfrom one entity to another or to a new entity

11

DeterminingDetermining whenwhen a a transactiontransaction isis a a BCBC

● The business combination must involve the acquisition of a business, which generally hasthree elements: three elements:

12

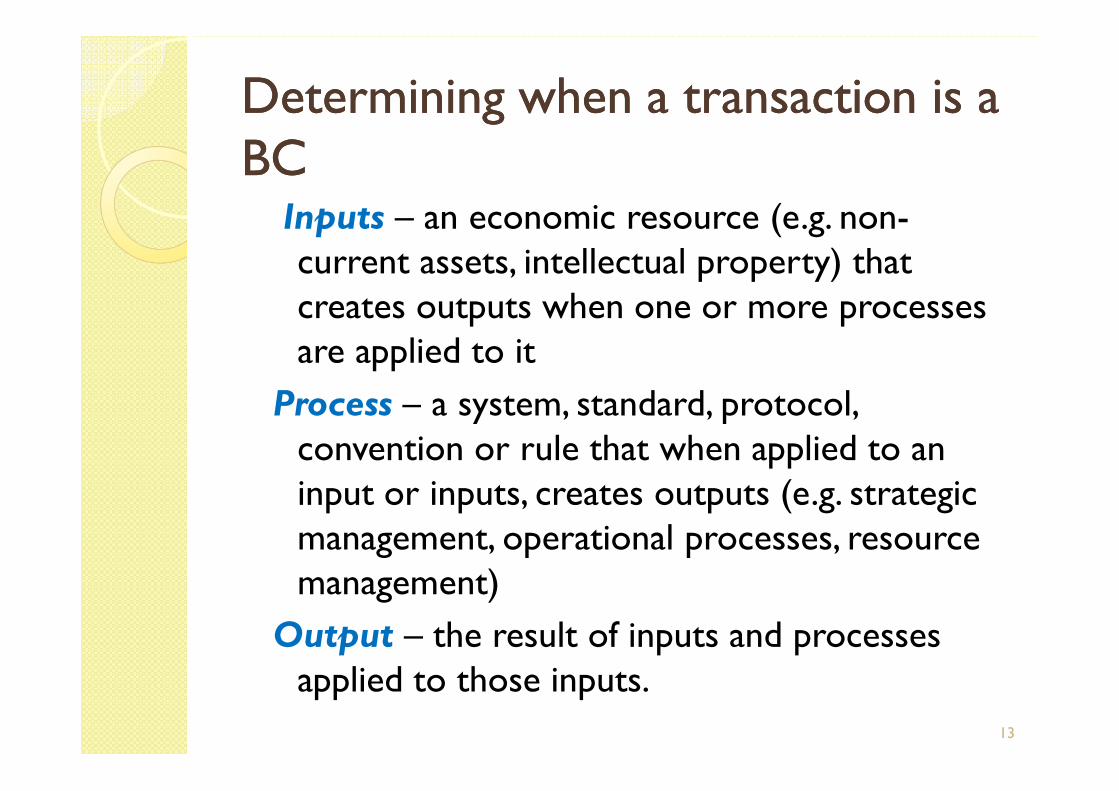

DeterminingDetermining whenwhen a a transactiontransaction isis a a BCBC

Inputs – an economic resource (e.g. non-current assets, intellectual property) thatcreates outputs when one or more processesare applied to it

Process – a system, standard, protocol, Process – a system, standard, protocol, convention or rule that when applied to aninput or inputs, creates outputs (e.g. strategicmanagement, operational processes, resourcemanagement)

Output – the result of inputs and processesapplied to those inputs.

13

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations

Acquisition method

The acquisition method is used for allbusiness combinations.business combinations.

14

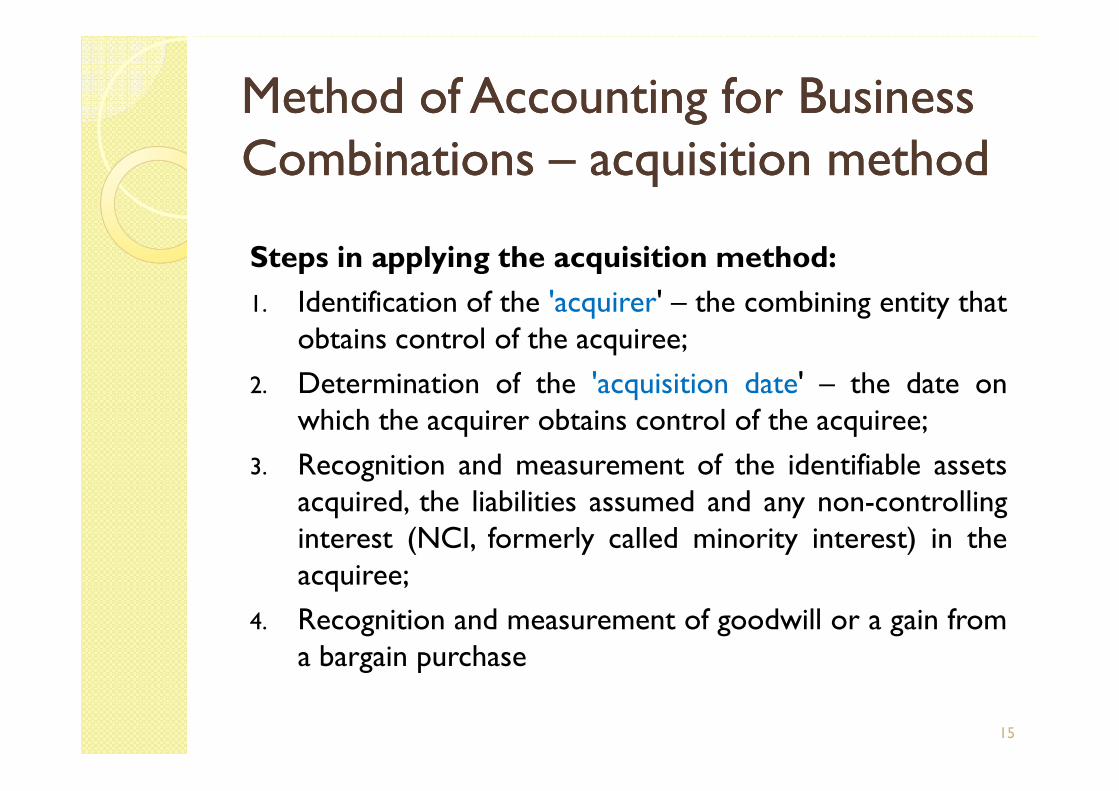

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– acquisitionacquisition methodmethod

Steps in applying the acquisition method:

1. Identification of the 'acquirer' – the combining entity thatobtains control of the acquiree;

2. Determination of the 'acquisition date' – the date on2. Determination of the 'acquisition date' – the date onwhich the acquirer obtains control of the acquiree;

3. Recognition and measurement of the identifiable assetsacquired, the liabilities assumed and any non-controllinginterest (NCI, formerly called minority interest) in theacquiree;

4. Recognition and measurement of goodwill or a gain froma bargain purchase

15

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition methodmethod

The acquirer is usually the entity that

transfers cash or other assets where the business combination is effected in this manner

16

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

If the guidance in IFRS 10 does not clearlyindicate which of the combining entities is anacquirer, IFRS 3 provides additional guidancewhich is then consideredwhich is then considered

� …….

17

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

………

� The acquirer is usually the entity that transferscash or other assets where the business combination is effected in this mannercombination is effected in this manner

18

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

● The acquirer is usually, but not always, the entityissuing equity interests where the transaction iseffected in this manner, however the entity alsoconsiders other pertinent facts and circumstancesincluding:including:

◦ relative voting rights in the combined entity after the business combination

◦ the existence of any ilarge minority interest if no otherowner or group of owners has a significant voting interest

◦ the composition of the governing body and senior management of the combined entity

◦ the terms on which equity interests are exchanged

19

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

� The acquirer is usually the entity with the largestrelative size (assets, revenues or profit)

� For business combinations involving multiple entities, � For business combinations involving multiple entities, consideration is given to the entity initiating the combination, and the relative sizes of the combiningentities

20

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

Acquisition date

� An acquirer considers all pertinent facts and circumstances when determining the acquisition date, i.e. the date on which it obtains control of the acquiree. i.e. the date on which it obtains control of the acquiree. The acquisition date may be a date that is earlier or later than the closing date.

21

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

� IFRS 3 does not provide detailed guidanceon the determination of the acquisition date and the date identified should reflect all relevantfacts and circumstances. facts and circumstances.

22

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

Considerations might include, among others, the date a public offer becomes unconditional (witha controlling interest acquired), when the acquirer can effect change in the board ofdirectors of the acquiree, the date ofdirectors of the acquiree, the date ofacceptance of an unconditional offer, when the acquirer starts directing the acquiree's operating and financing policies, or the date competition or other authorities providenecessarily clearances.

23

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinationsMeasurement of acquired assets and liabilities.IFRS 3 establishes the following principles in relation tothe recognition and measurement of items arising in abusiness combination:business combination:

� Recognition principle. Identifiable assets acquired, liabilities assumed, and non-controlling interests in the acquiree, are recognised separately from goodwill

� Measurement principle. All assets acquired and liabilities assumed in a business combination are measured at acquisition-date fair value.

24

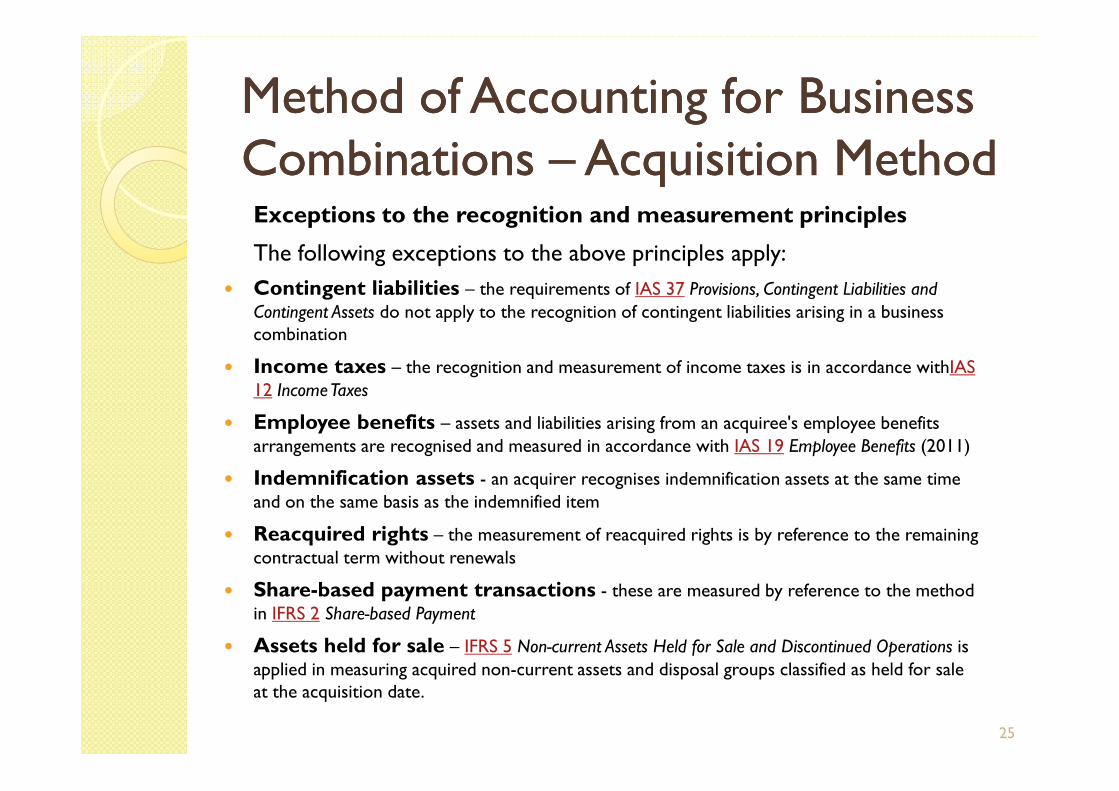

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethodExceptions to the recognition and measurement principles

The following exceptions to the above principles apply:

� Contingent liabilities – the requirements of IAS 37 Provisions, Contingent Liabilities and

Contingent Assets do not apply to the recognition of contingent liabilities arising in a business combination

� Income taxes – the recognition and measurement of income taxes is in accordance withIAS

12 IncomeTaxes12 IncomeTaxes

� Employee benefits – assets and liabilities arising from an acquiree's employee benefits

arrangements are recognised and measured in accordance with IAS 19 Employee Benefits (2011)

� Indemnification assets - an acquirer recognises indemnification assets at the same time

and on the same basis as the indemnified item

� Reacquired rights – the measurement of reacquired rights is by reference to the remaining

contractual term without renewals

� Share-based payment transactions - these are measured by reference to the method

in IFRS 2 Share-based Payment

� Assets held for sale – IFRS 5 Non-current Assets Held for Sale and Discontinued Operations is

applied in measuring acquired non-current assets and disposal groups classified as held for sale at the acquisition date.

25

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

In applying the principles, an acquirer classifiesand designates assets acquired and liabilitiesassumed on the basis of the contractualassumed on the basis of the contractualterms, economic conditions, operatingand accounting policies and other pertinentconditions existing at the acquisition date

26

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

For example, this might include the identification of derivative financial instrumentsas hedging instruments, or the separation ofas hedging instruments, or the separation ofembedded derivatives from host contracts.

27

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

For example, this might include the identification of derivative financial instrumentsas hedging instruments, or the separation ofas hedging instruments, or the separation ofembedded derivatives from host contracts.

28

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

However, exceptions are made for leaseclassification (between operating and finance leases) and the classification of contracts asleases) and the classification of contracts asinsurance contracts, which are classified on the basis of conditions in place at the inception ofthe contract.

29

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations –– AcquisitionAcquisition MethodMethod

Acquired intangible assets must berecognised and measured at fair value in

accordance with the principles if it is separableor arises from other contractual rights, or arises from other contractual rights, irrespective of whether the acquiree hadrecognised the asset prior to the business combination occurringNB: This is because there is always sufficient information toreliably measure the fair value of these assets.

30

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations

Measurement NCI (Non-controlling interest)IFRS 3 allows an accounting policy choice, available on atransaction by transaction basis, to measure NCI eithertransaction by transaction basis, to measure NCI eitherat:

◦ fair value (sometimes called the full goodwill method),or

◦ the NCI's proportionate share of net assets of theacquiree.

31

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations

The choice in accounting policy applies only topresent ownership interests in the acquiree thatentitle holders to a proportionate share of the entity's net assets in the event of a liquidationentity's net assets in the event of a liquidation(e.g. outside holdings of an acquiree's ordinaryshares).

32

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations

Other components of non-controlling interestsat must be measured at acquisition date fair values or in accordance with other applicableIFRSs (e.g. share-based payment transactionsIFRSs (e.g. share-based payment transactionsaccounted for under IFRS 2 Share-basedPayment).

33

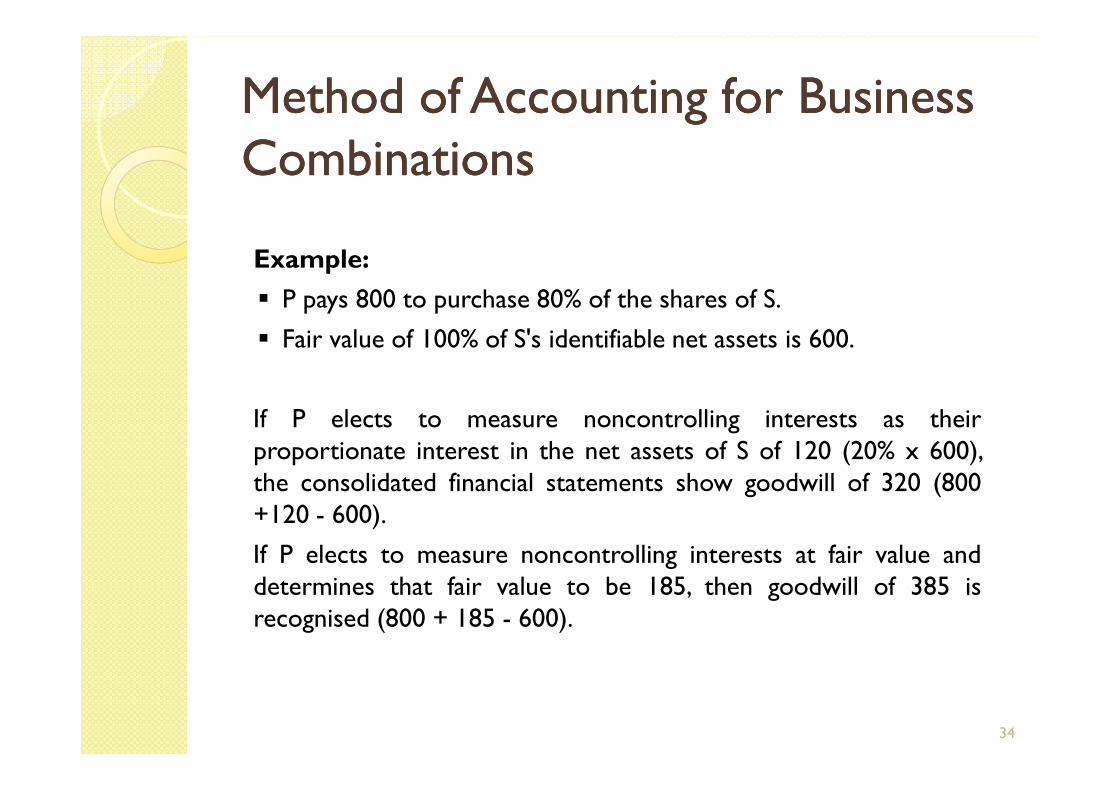

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations

Example:

� P pays 800 to purchase 80% of the shares of S.

� Fair value of 100% of S's identifiable net assets is 600.

If P elects to measure noncontrolling interests as theirproportionate interest in the net assets of S of 120 (20% x 600),the consolidated financial statements show goodwill of 320 (800+120 - 600).

If P elects to measure noncontrolling interests at fair value anddetermines that fair value to be 185, then goodwill of 385 isrecognised (800 + 185 - 600).

34

MethodMethod of Accounting of Accounting forfor Business Business CombinationsCombinations

The fair value of the 20% noncontrolling interest in Swill not necessarily be proportionate to the price paidby P for its 80%, primarily due to control premium ordiscount as explained in paragraph B45 of IFRS 3.

35

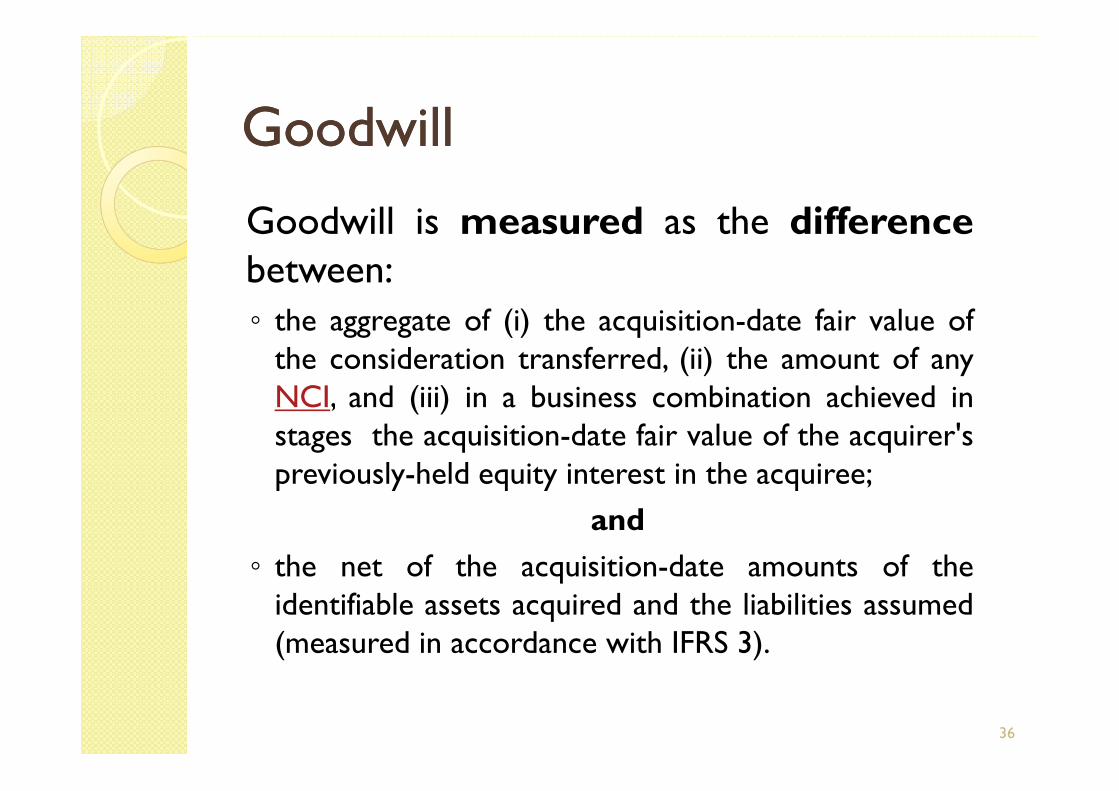

GoodwillGoodwill

Goodwill is measured as the differencebetween:◦ the aggregate of (i) the acquisition-date fair value of

the consideration transferred, (ii) the amount of anyNCI, and (iii) in a business combination achieved inNCI, and (iii) in a business combination achieved instages the acquisition-date fair value of the acquirer'spreviously-held equity interest in the acquiree;

and

◦ the net of the acquisition-date amounts of theidentifiable assets acquired and the liabilities assumed(measured in accordance with IFRS 3).

36

GoodwillGoodwill

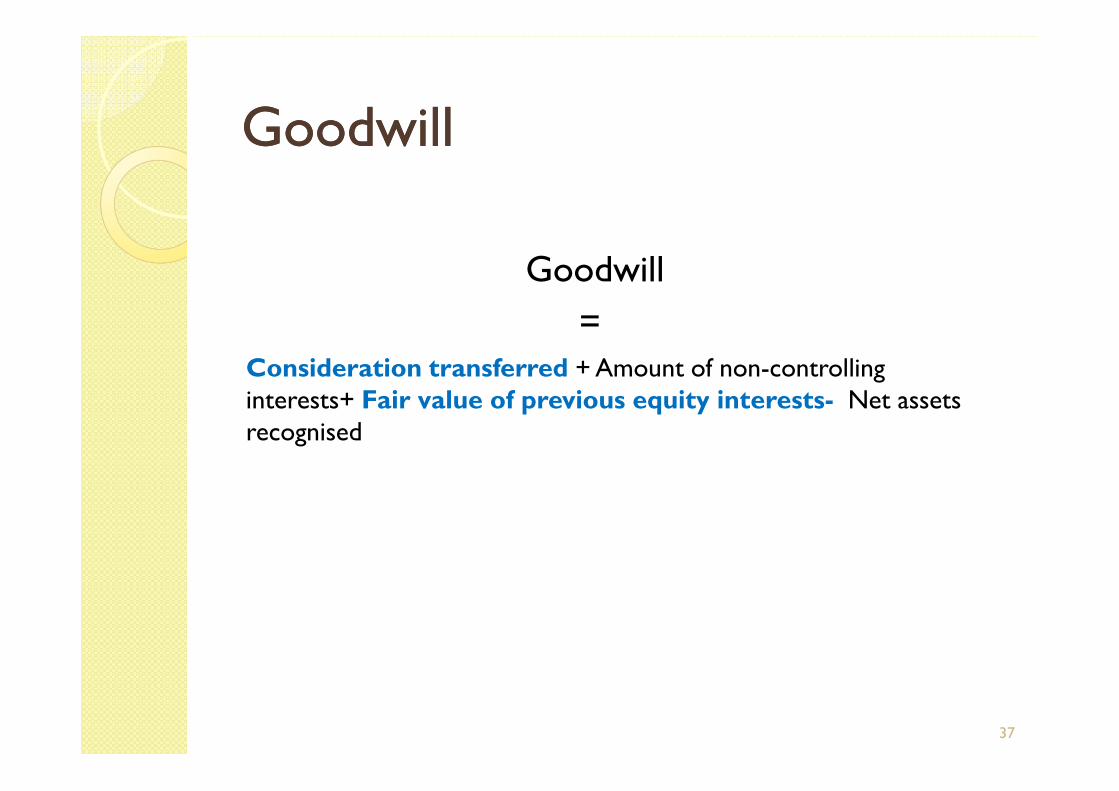

Goodwill

=Consideration transferred + Amount of non-controllinginterests+ Fair value of previous equity interests- Net assetsinterests+ Fair value of previous equity interests- Net assetsrecognised

37

GoodwillGoodwill

If the difference above is negative, the resultinggain is recognised as a bargain purchase in profitor loss.

38

GoodwillGoodwill

However, before any bargain purchase gain isrecognised in profit or loss, the acquirer isrequired to undertake a review to ensurethe identification of assets and liabilities isthe identification of assets and liabilities iscomplete, and that measurements appropriatelyreflect consideration of all available information

39

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

� Prior to control being obtained, the investment isaccounted for under IAS 28, IAS 31, or IAS 39, asappropriate;

� On the date that control is obtained, the fair values of� On the date that control is obtained, the fair values ofthe acquired entity's assets and liabilities, includinggoodwill, are measured (with the option to measure fullgoodwill or only the acquirer's percentage of goodwill).

40

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

�As part of accounting for the businesscombination, the acquirer remeasures anypreviously held interest at fair value and takesthis amount into account in the determinationthis amount into account in the determinationof goodwill as noted above .

� Any resultant gain or loss is recognised inprofit or loss or other comprehensive incomeas appropriate

41

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

� The accounting treatment of an entity's pre-combination interest in an acquiree is consistent withthe view that the obtaining of control is a significanteconomic event that triggers a remeasurement.economic event that triggers a remeasurement.Consistent with this view, all of the assets and liabilitiesof the acquiree are fully remeasured in accordance withthe requirements of IFRS 3 (generally at fair value).

42

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

�Accordingly, the determination of goodwilloccurs only at the acquisition date.

43

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

EXAMPLE

Entity A achieved 80% equity of B in 2 steps:

Step 1: in 2010 Entity A purchases 15% equity, cashStep 1: in 2010 Entity A purchases 15% equity, cashpayment €100. Shares are posted in “Assets available forsales”: fair value between 2010 and 2012 was €20,posted in profit and loss, other comprehensive income;

44

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

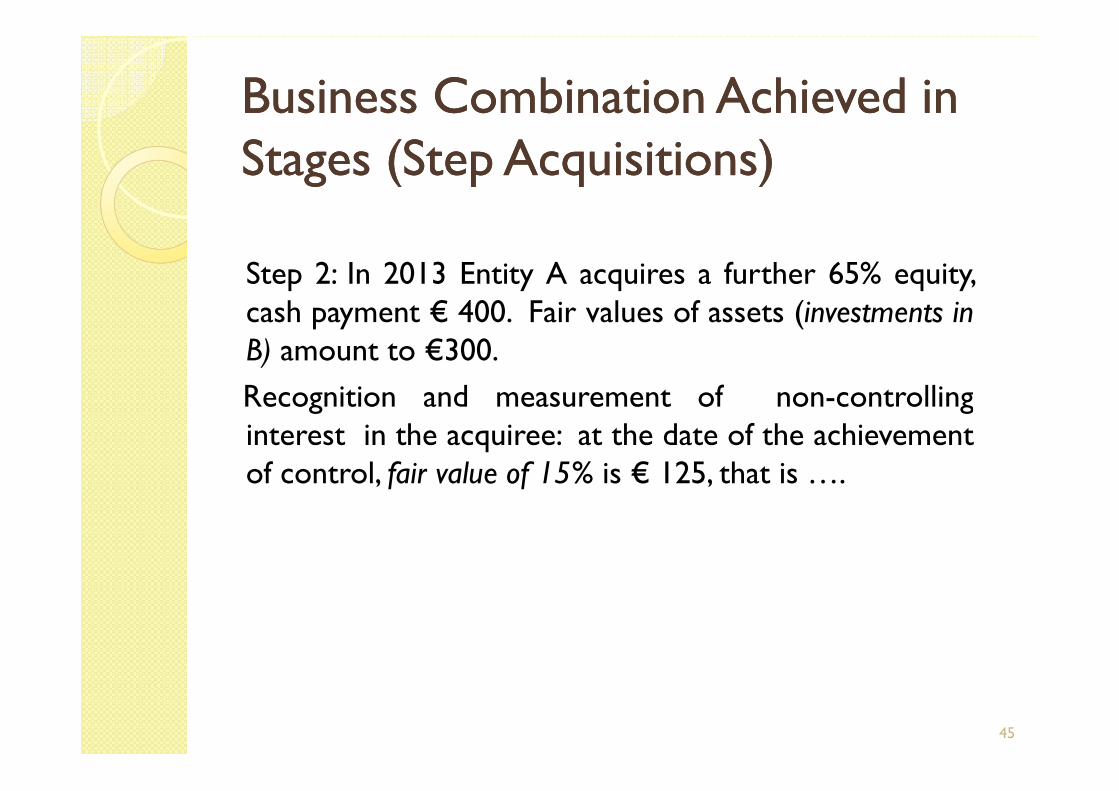

Step 2: In 2013 Entity A acquires a further 65% equity,cash payment € 400. Fair values of assets (investments inB) amount to €300.

Recognition and measurement of non-controllingRecognition and measurement of non-controllinginterest in the acquiree: at the date of the achievementof control, fair value of 15% is € 125, that is ….

45

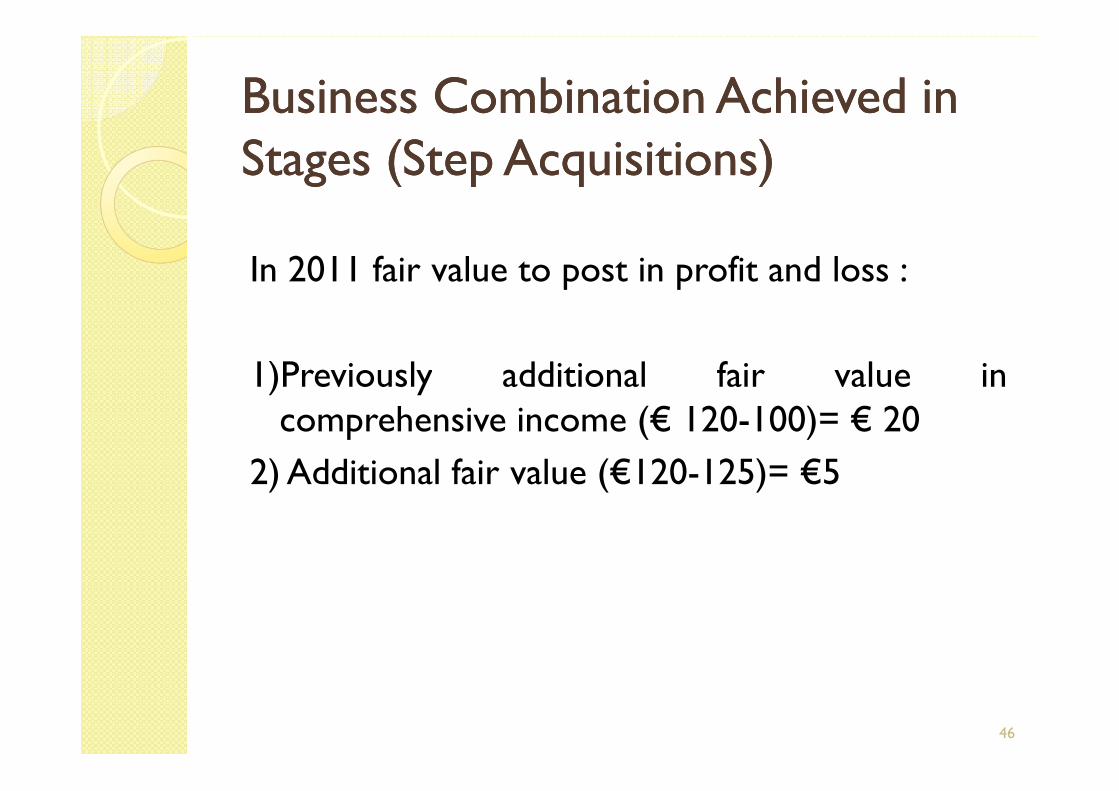

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

In 2011 fair value to post in profit and loss :

1)Previously additional fair value incomprehensive income (€ 120-100)= € 20

1)Previously additional fair value incomprehensive income (€ 120-100)= € 20

2) Additional fair value (€120-125)= €5

46

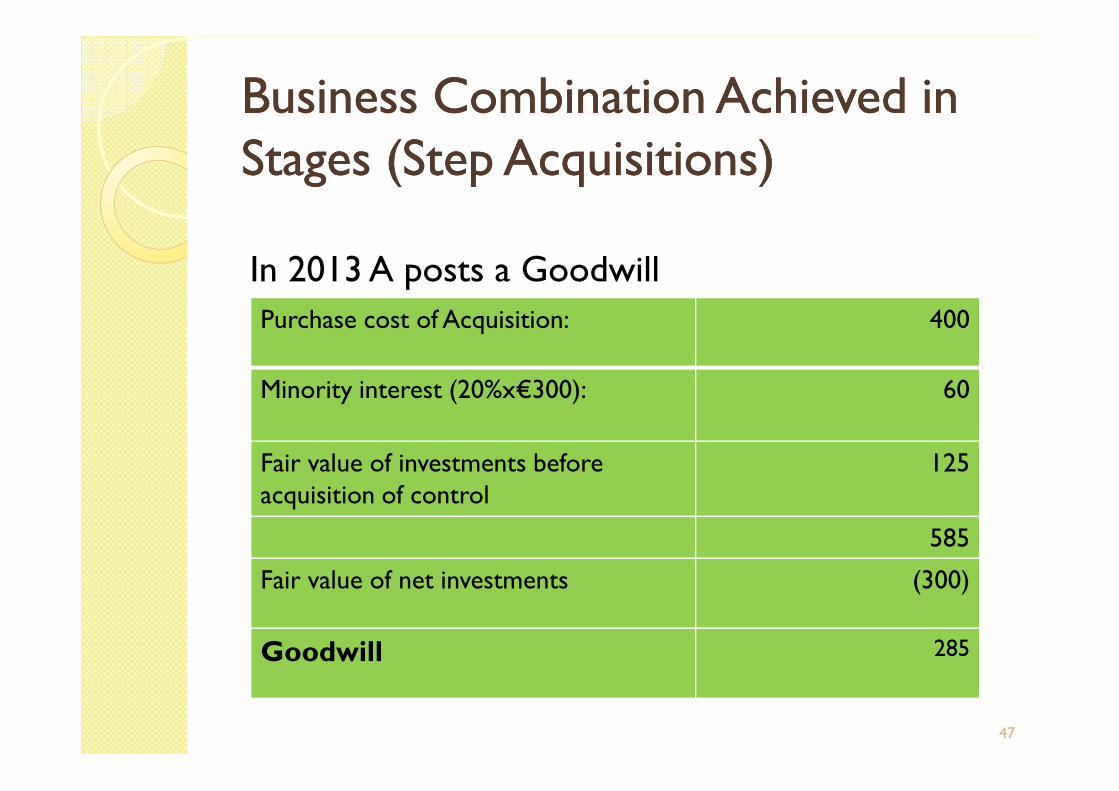

Business Business CombinationCombination AchievedAchieved in in StagesStages ((StepStep AcquisitionsAcquisitions))

In 2013 A posts a Goodwill

Purchase cost of Acquisition: 400

Minority interest (20%x€300): 60

47

Minority interest (20%x€300): 60

Fair value of investments before acquisition of control

125

585

Fair value of net investments (300)

Goodwill 285

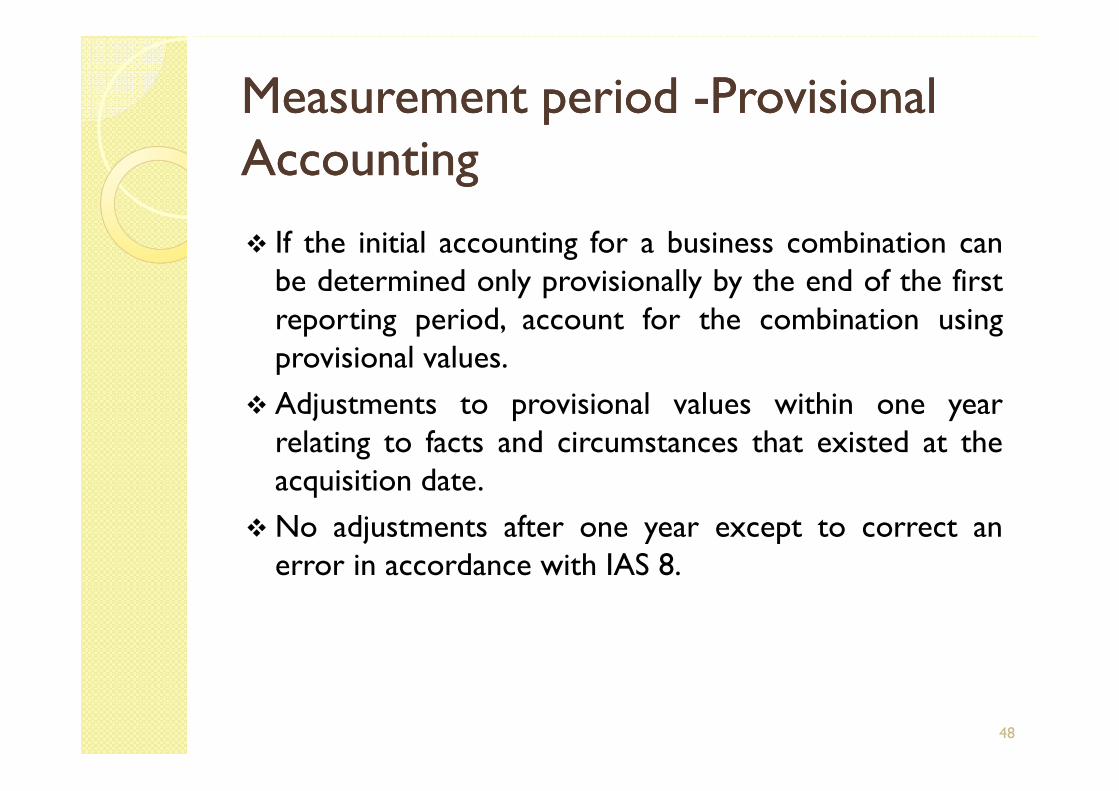

MeasurementMeasurement periodperiod --ProvisionalProvisionalAccountingAccounting

� If the initial accounting for a business combination canbe determined only provisionally by the end of the firstreporting period, account for the combination usingprovisional values.

� Adjustments to provisional values within one year� Adjustments to provisional values within one yearrelating to facts and circumstances that existed at theacquisition date.

� No adjustments after one year except to correct anerror in accordance with IAS 8.

48

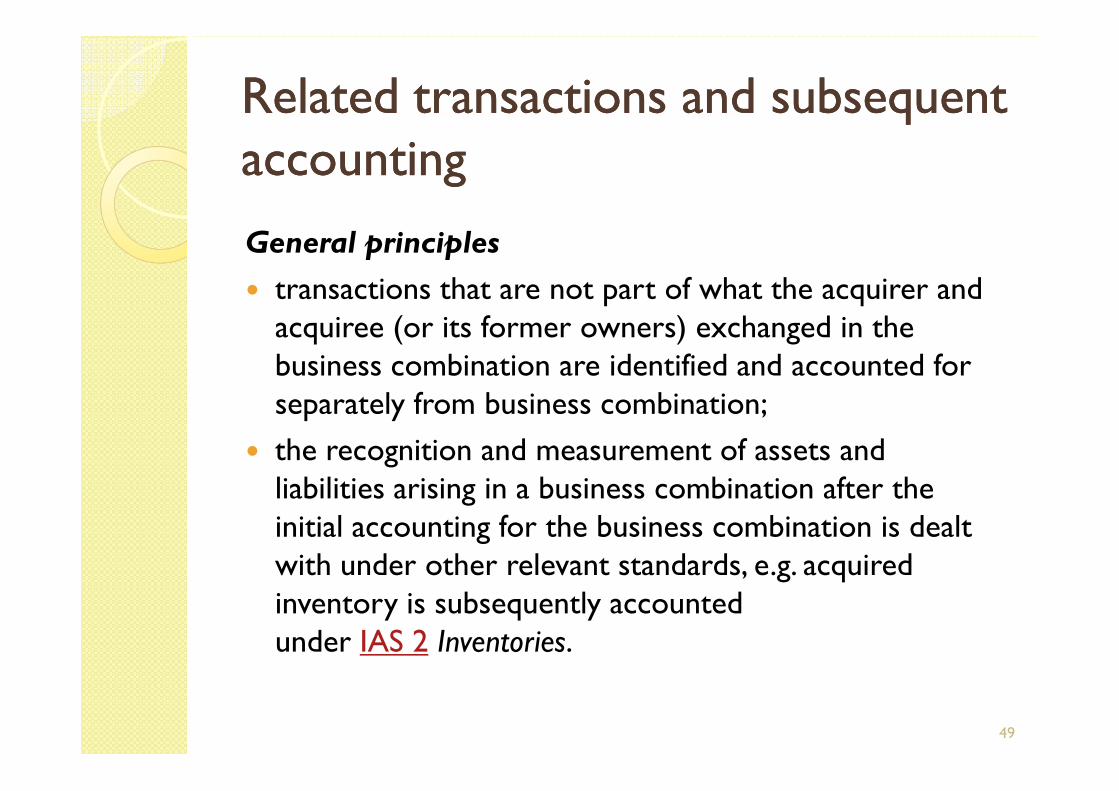

RelatedRelated transactionstransactions and and subsequentsubsequentaccountingaccounting

General principles

� transactions that are not part of what the acquirer and acquiree (or its former owners) exchanged in the business combination are identified and accounted forseparately from business combination;separately from business combination;

� the recognition and measurement of assets and liabilities arising in a business combination after the initial accounting for the business combination is dealtwith under other relevant standards, e.g. acquiredinventory is subsequently accountedunder IAS 2 Inventories.

49

RelatedRelated transactionstransactions and and subsequentsubsequentaccountingaccounting

When determining whether a particular item is part ofthe exchange for the acquiree or whether it is separate from the business combination, an acquirer considersthe reason for the transaction, who initiated the the reason for the transaction, who initiated the transaction and the timing of the transaction

50

ContingentContingent ConsiderationConsideration

Contingent consideration must be measured at fair value at the time of the business combination and istaken into account in the determination of goodwill.

51

ContingentContingent ConsiderationConsideration

If the amount of contingent consideration changes as a result of a post-acquisition event (such as meeting anearnings target), accounting for the change in earnings target), accounting for the change in consideration depends on whether the additionalconsideration is classified as an equity instrument or anasset or liability:

52

ContingentContingent ConsiderationConsideration● If the contingent consideration is classified as an equity

instrument, the original amount is not remeasured

� If the additional consideration is classified as an asset or liability that is a financial instrument, the contingentconsideration is measured at fair value and gains and losses are recognised in either profit or loss or otherlosses are recognised in either profit or loss or othercomprehensive income in accordance with IFRS 9 Financial Instruments or IAS 39 Financial Instruments: Recognition and Measurement

� If the additional consideration is not within the scope ofIFRS 9 (or IAS 39), it is accounted for in accordancewith IAS 37 Provisions, Contingent Liabilities and ContingentAssets or other IFRSs as appropriate.

53

ContingentContingent ConsiderationConsiderationNote: Annual Improvements to IFRSs 2010–2012 Cycle changes these requirements for business combinations for which the acquisition date is on or after 1 July 2014.

Under the amended requirements, contingentUnder the amended requirements, contingentconsideration that is classified as an asset or liability ismeasured at fair value at each reporting date and changes in fair value are recognised in profit or loss, both for contingent consideration that is within the scope of IFRS 9/IAS 39 or otherwise.

54

ContingentContingent ConsiderationConsideration

Where a change in the fair value of contingentconsideration is the result of additionalinformation about facts and circumstancesinformation about facts and circumstancesthat existed at the acquisition date, thesechanges are accounted for as measurementperiod adjustments if they arise during the measurement period

55

CostCost of of anan AcquisitionAcquisition

Measurement

� Consideration for the acquisition includes theacquisition-date fair value of contingentacquisition-date fair value of contingentconsideration.

�Changes to contingent consideration resultingfrom events after the acquisition date must berecognised in profit or loss.

56

CostCost of of anan AcquisitionAcquisition

Acquisition costs

� Costs of issuing debt or equity instruments areaccounted for under IAS 32 and IAS 39.

� All other costs associated with the acquisition must beexpensed, including reimbursements to the acquiree forexpensed, including reimbursements to the acquiree forbearing some of the acquisition costs. Examples of coststo be expensed include finder's fees; advisory, legal,accounting, valuation and other professional orconsulting fees; and general administrative costs,including the costs of maintaining an internalacquisitions department.

57

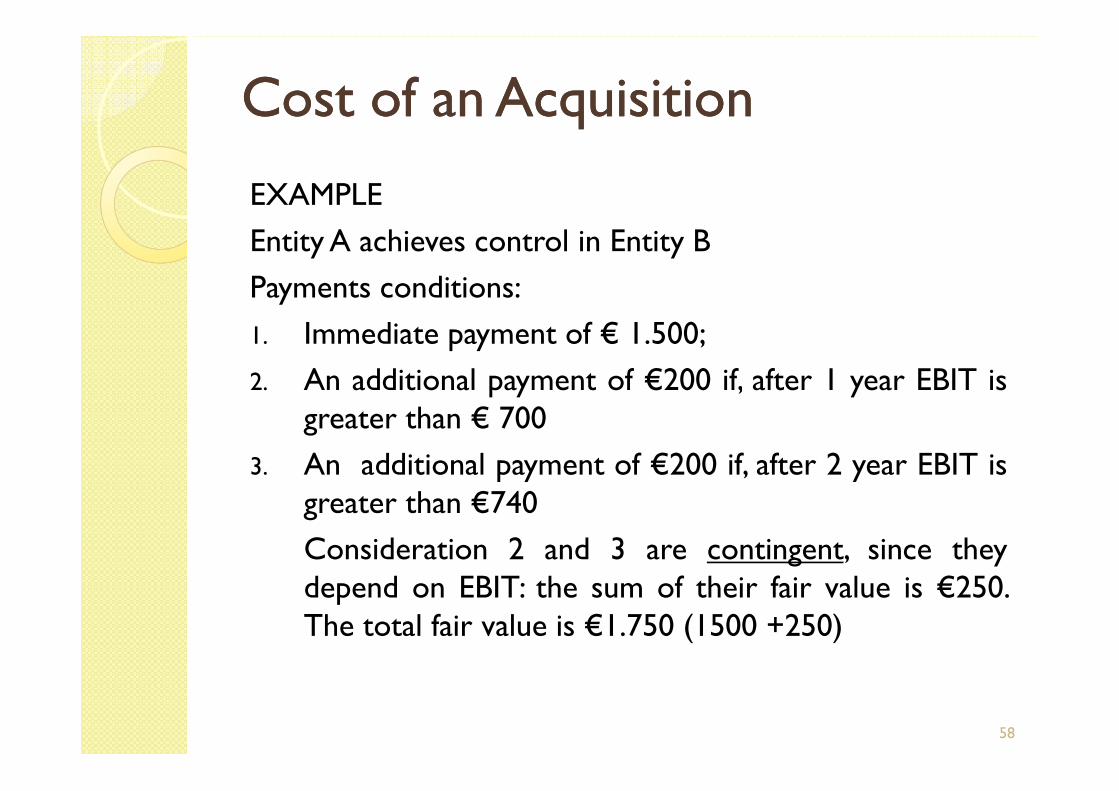

CostCost of of anan AcquisitionAcquisition

EXAMPLE

Entity A achieves control in Entity B

Payments conditions:

1. Immediate payment of € 1.500;

2. An additional payment of €200 if, after 1 year EBIT isgreater than € 700

2. An additional payment of €200 if, after 1 year EBIT isgreater than € 700

3. An additional payment of €200 if, after 2 year EBIT isgreater than €740

Consideration 2 and 3 are contingent, since theydepend on EBIT: the sum of their fair value is €250.The total fair value is €1.750 (1500 +250)

58

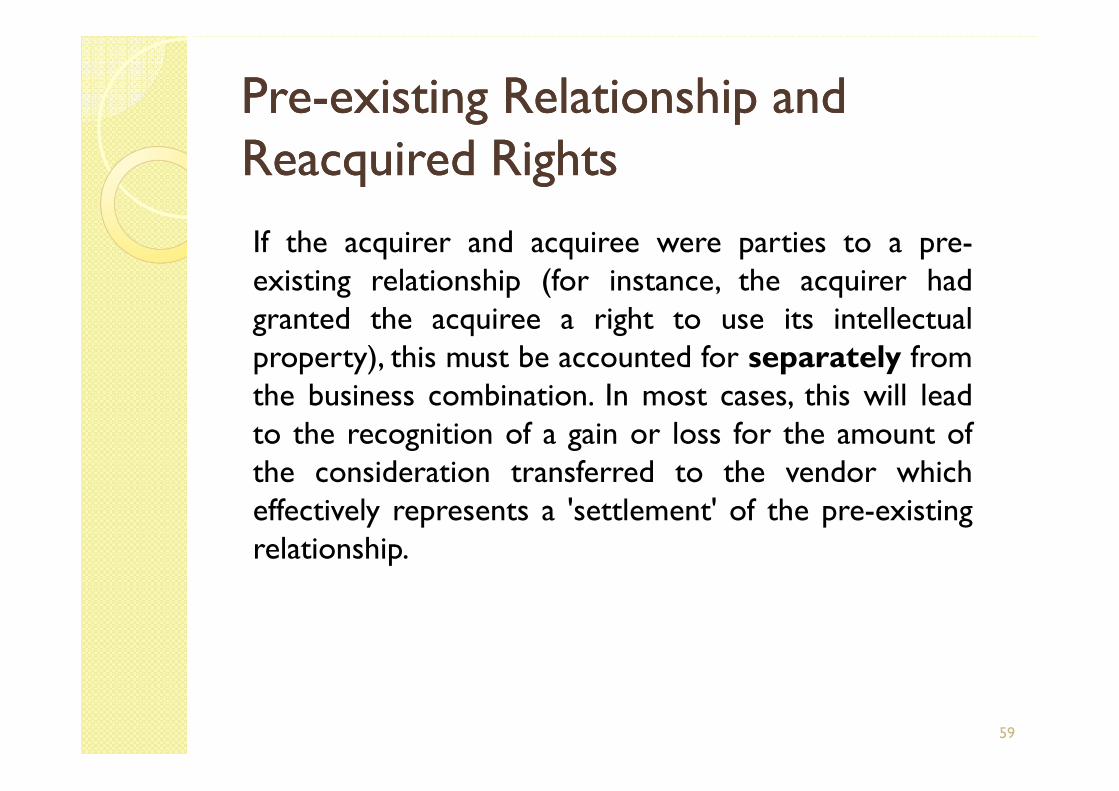

PrePre--existingexisting RelationshipRelationship and and ReacquiredReacquired RightsRights

If the acquirer and acquiree were parties to a pre-existing relationship (for instance, the acquirer hadgranted the acquiree a right to use its intellectualproperty), this must be accounted for separately fromthe business combination. In most cases, this will lead

59

the business combination. In most cases, this will leadto the recognition of a gain or loss for the amount ofthe consideration transferred to the vendor whicheffectively represents a 'settlement' of the pre-existingrelationship.

PrePre--existingexisting RelationshipRelationship andandReacquiredReacquired RightsRights

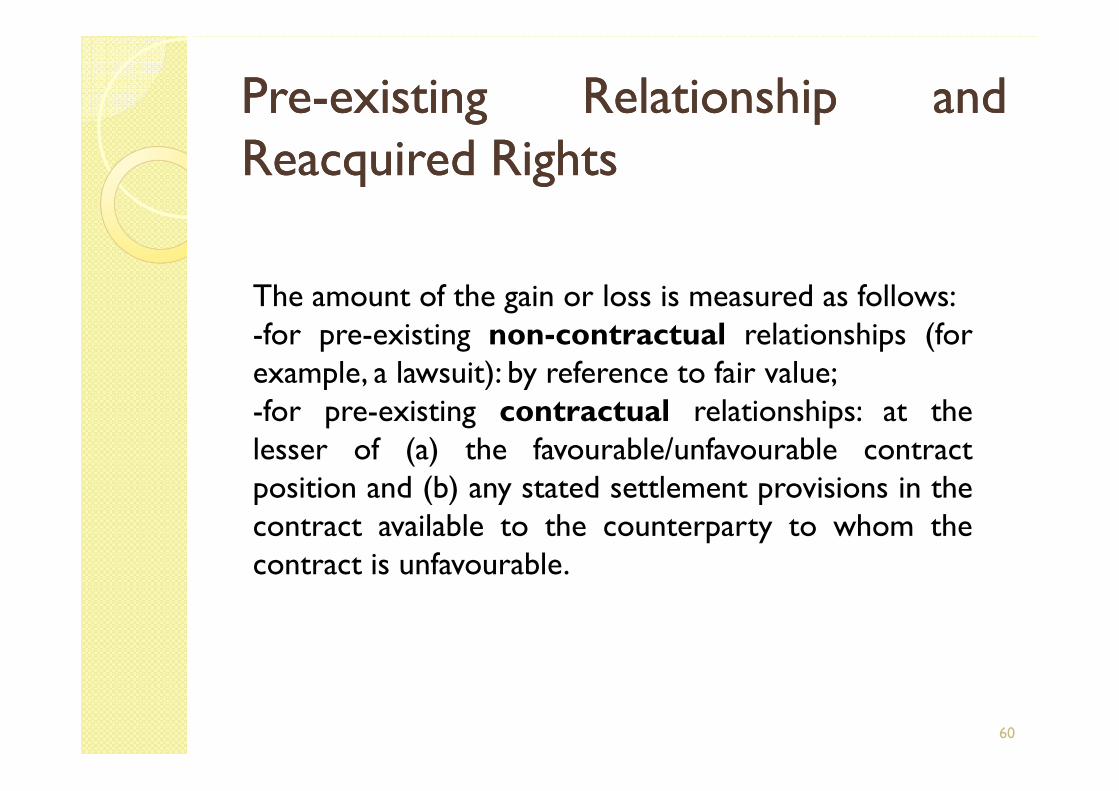

The amount of the gain or loss is measured as follows:-for pre-existing non-contractual relationships (forexample, a lawsuit): by reference to fair value;-for pre-existing contractual relationships: at the

60

-for pre-existing contractual relationships: at thelesser of (a) the favourable/unfavourable contractposition and (b) any stated settlement provisions in thecontract available to the counterparty to whom thecontract is unfavourable.

PrePre--existingexisting RelationshipRelationship andandReacquiredReacquired RightsRights

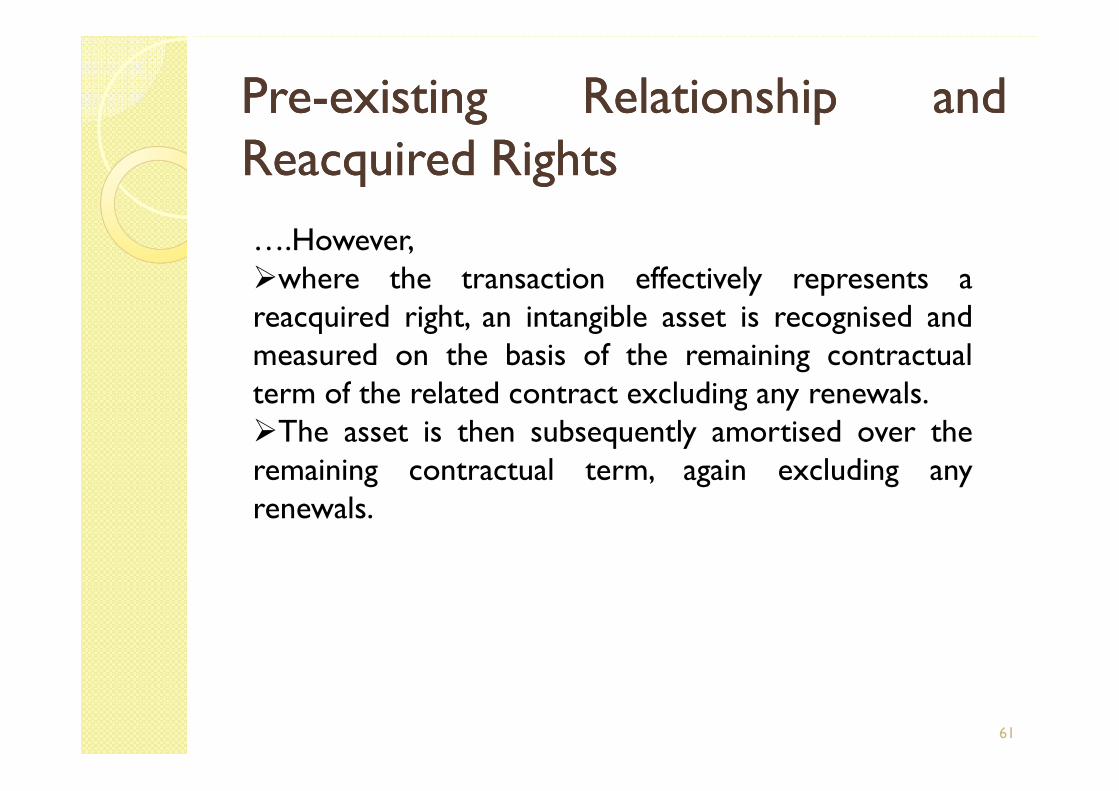

….However,�where the transaction effectively represents areacquired right, an intangible asset is recognised andmeasured on the basis of the remaining contractualterm of the related contract excluding any renewals.

61

term of the related contract excluding any renewals.�The asset is then subsequently amortised over theremaining contractual term, again excluding anyrenewals.

ContingentContingent LiabilitiesLiabilities

Until a contingent liability is settled, cancelled orexpired, a contingent liability that was recognised in theinitial accounting for a business combination ismeasured at the higher of the amount the liabilitywould be recognised under IAS 37 Provisions, Contingent

62

would be recognised under IAS 37 Provisions, ContingentLiabilities and Contingent Assets, and the amount lessaccumulated amortisation under IAS 18 Revenue.

ContingentContingent paymentspayments totoemployeesemployees and and shareholdersshareholders

As part of a business combination, anacquirer may enter into arrangementswith selling shareholders or employees.

63

ContingentContingent paymentspayments totoemployeesemployees and and shareholdersshareholders

In determining whether such arrangements are part ofthe business combination or accounted for separately,the acquirer considers a number of factors, including:-whether the arrangement requires continuingemployment (and if so, its term),

64

employment (and if so, its term),- the level or remuneration compared to otheremployees,- whether payments to shareholder employees areincremental to non-employee shareholders,-the relative number of shares owns, linkages tovaluation of the acquiree,-how the consideration is calculated, and otheragreements and issues.

ContingentContingent paymentspayments totoemployeesemployees and and shareholdersshareholders

Where share-based payment arrangements ofthe acquiree exist and are replaced, the value ofsuch awards must be apportioned betweenpre-combination and post-combination service

65

pre-combination and post-combination serviceand accounted for accordingly

IndemnificationIndemnification assetsassets

Indemnification assets recognised at theacquisition date (under the exceptions to thegeneral recognition and measurementprinciples noted above) are subsequentlymeasured on the same basis of the indemnified

66

measured on the same basis of the indemnifiedliability or asset, subject to contractual impactsand collectibility. Indemnification assets are onlyderecognised when collected, sold or whenrights to it are lost

OtherOther issuesissues

In addition, IFRS 3 provides guidance on some specificaspects of business combinations including:

� business combinations achieved without the transfer ofconsideration;

reverse acquisitions;� reverse acquisitions;

� identifying intangible assets acquired ;

67

DisclosuresDisclosures

Disclosure of information about current businesscombinations

The acquirer shall disclose information that enablesusers of its financial statements to evaluate the natureand financial effect of a business combination thatand financial effect of a business combination thatoccurs either during the current reporting period orafter the end of the period but before the financialstatements are authorised for issue

68

DisclosuresDisclosures

Among the disclosures required to meet the foregoing objective are the following:

� name and a description of the acquiree;

� acquisition date;� acquisition date;

� percentage of voting equity interests acquired;

� primary reasons for the business combination and adescription of how the acquirer obtained control of theacquiree. description of the factors that make up thegoodwill recognised ;

69

DisclosuresDisclosures

� qualitative description of the factors that make up thegoodwill recognised, such as expected synergies fromcombining operations, intangible assets that do notqualify for separate recognition;

� acquisition-date fair value of the total considerationtransferred and the acquisition-date fair value of eachmajor class of consideration;

70

DisclosuresDisclosures

� details of contingent consideration arrangements andindemnification assets

� details of acquired receivables

� the amounts recognised as of the acquisition date for� the amounts recognised as of the acquisition date foreach major class of assets acquired and liabilitiesassumed

� details of contingent liabilities recognised

71

DisclosuresDisclosures

� total amount of goodwill that is expected to bedeductible for tax purposes

� details of any transactions that are recognisedseparately from the acquisition of assets and assumptionseparately from the acquisition of assets and assumptionof liabilities in the business combination

� information about a bargain purchase ('negativegoodwill')

72

DisclosuresDisclosures

� for each business combination in which the acquirerholds less than 100 per cent of the equity interests inthe acquiree at the acquisition date, various disclosuresare required

� details about a business combination achieved in stages

73

DisclosuresDisclosures

� information about the acquiree's revenue and profit orloss;

� information about a business combination whose� information about a business combination whoseacquisition date is after the end of the reporting periodbut before the financial statements are authorised forissue.

74

DisclosuresDisclosures

Disclosure of information about adjustments ofpast business combinations

The acquirer shall disclose information that enablesusers of its financial statements to evaluate the financialusers of its financial statements to evaluate the financialeffects of adjustments recognised in the currentreporting period that relate to business combinationsthat occurred in the period or previous reportingperiods.

75

DisclosuresDisclosures

Among the disclosures required to meet the foregoingobjective are the following:

◦ details when the initial accounting for a business combination isincomplete for particular assets, liabilities, non-controllinginterests or items of consideration (and the amounts recognisedinterests or items of consideration (and the amounts recognisedin the financial statements for the business combination thushave been determined only provisionally);

◦ follow-up information on contingent consideration;

76

DisclosuresDisclosures

� follow-up information about contingent liabilitiesrecognised in a business combination;

� a reconciliation of the carrying amount of goodwill at� a reconciliation of the carrying amount of goodwill atthe beginning and end of the reporting period, withvarious details shown separately.

77

DisclosuresDisclosures

� the amount and an explanation of any gain or lossrecognised in the current reporting period that both:

◦ (i) relates to the identifiable assets acquired orliabilities assumed in a business combination that waseffected in the current or previous reporting period,effected in the current or previous reporting period,and

◦ (ii) is of such a size, nature or incidence thatdisclosure is relevant to understanding the combinedentity's financial statements.

78