Lo Stato dell’Arte dei Metodi e Modelli di Controllo di ... · • TREND recenti del Controllo di...

58

S.A.F. SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO Lo Stato dell’Arte dei Metodi e Modelli di Controllo di Gestione: una prospettiva evolutiva Milano, 17 Settembre 2014 Francesco Aldo De Luca Segretario Commissione Finanza e Controllo di Gestione ODCEC Milano

Transcript of Lo Stato dell’Arte dei Metodi e Modelli di Controllo di ... · • TREND recenti del Controllo di...

S.A.F. SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO

Lo Stato dell’Arte dei Metodi e Modelli di Controllo di Gestione:

una prospettiva evolutiva

Milano, 17 Settembre 2014

Francesco Aldo De Luca Segretario Commissione Finanza e Controllo di Gestione ODCEC Milano

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 2

• Time-Lapse delle Tecniche di Accounting

• TREND recenti del Controllo di Gestione

• La Guida IFAC sul Business Reporting

• Il Planning Survey del BARC

• Lo Studio del Controllo di Gestione nelle Università

• Il Futuro del Controllo di Gestione

• Quantrix: le Nuove Sfide del Controllo di Gestione

Indice

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 3

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 4

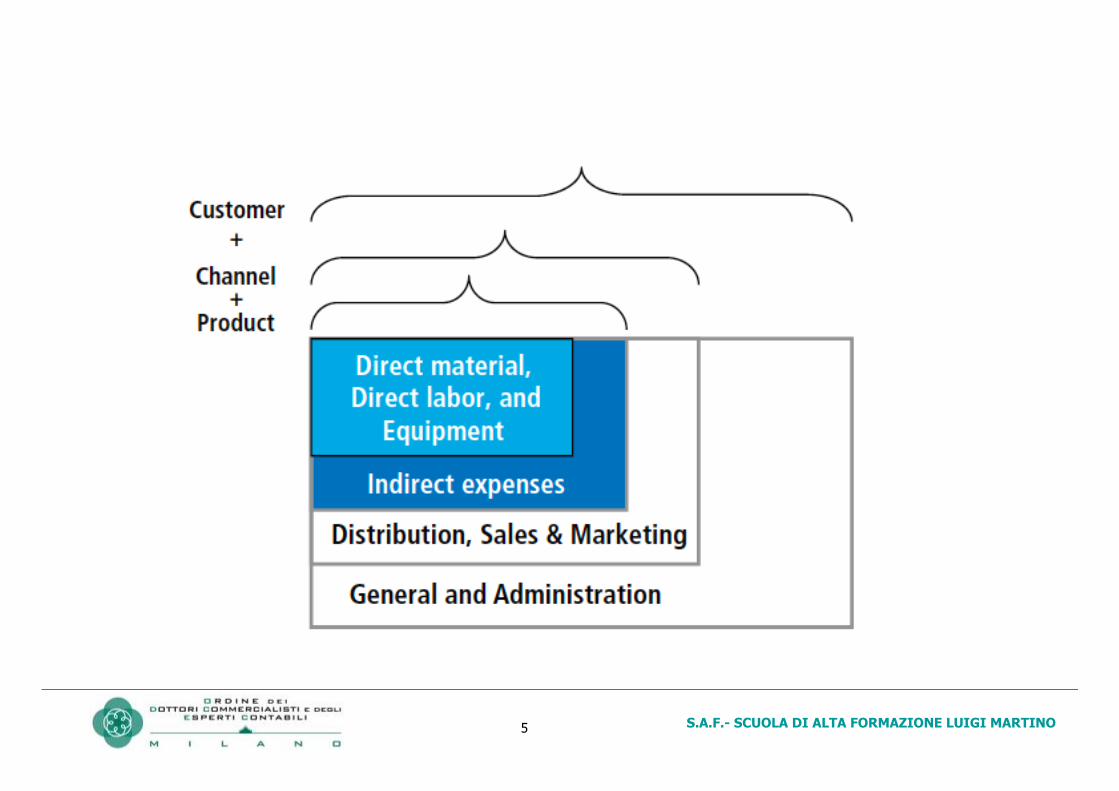

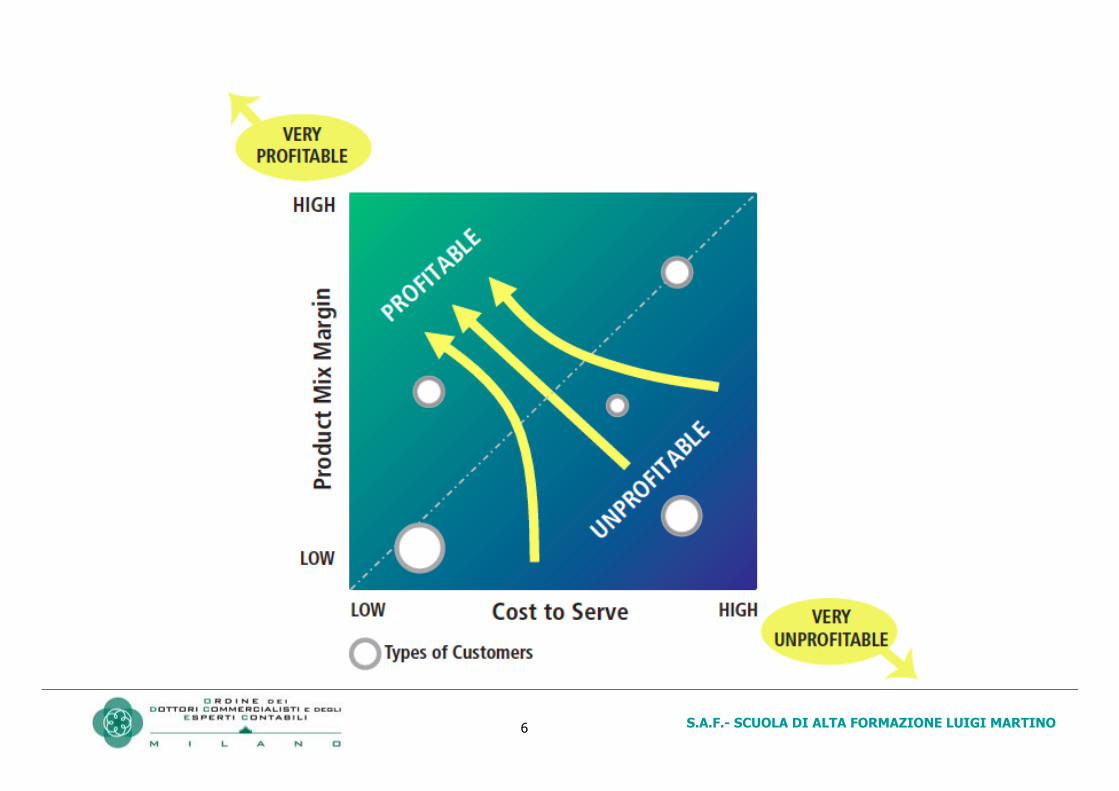

1. Expansion from product to channel and customer profitability analysis

Trend 1

https://www.youtube.com/watch?v=lCj4-gvH1WQ&list=PL7jmrwgbi8y1YyzRulQXqX4TvftOcPOK6&index=1

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 5

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 6

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 7

2. Management accounting’s expanding role with enterprise performance management (EPM)

Trend 2 https://www.youtube.com/watch?v=qcbpjkRgW9I&list=PL7jmrwgbi8y1YyzRulQXqX4TvftOcPOK6&index=2

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 8

The key point in trend No. 2 is integration. The various components of EPM are like gears in a machine: interconnected. Commercial software increasingly provides integration, so, for example, when profitability information is calculated, it is reflected directly in the performance measures of a balanced scorecard or operational dashboards.

2. Management accounting’s expanding role with enterprise performance management (EPM)

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 9

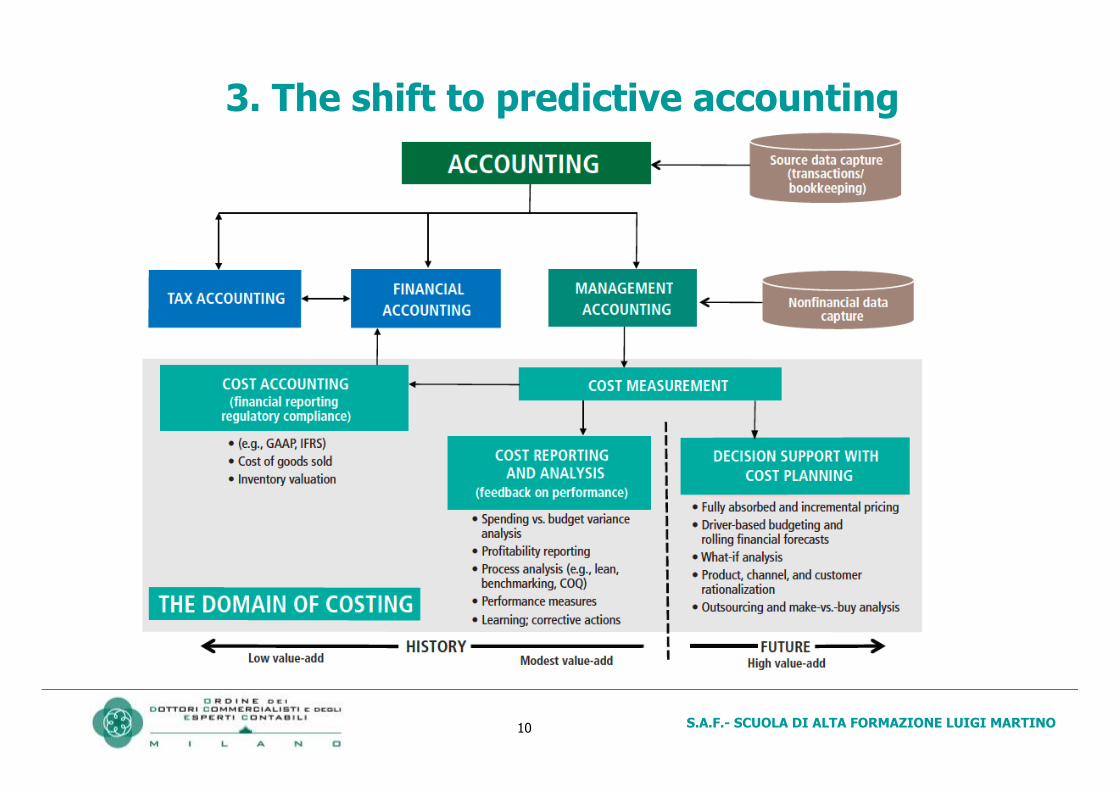

3. The shift to predictive accounting

Trend 3 https://www.youtube.com/watch?v=3cwdelVpNRA&list=PL7jmrwgbi8y1YyzRulQXqX4TvftOcPOK6&index=3

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 10

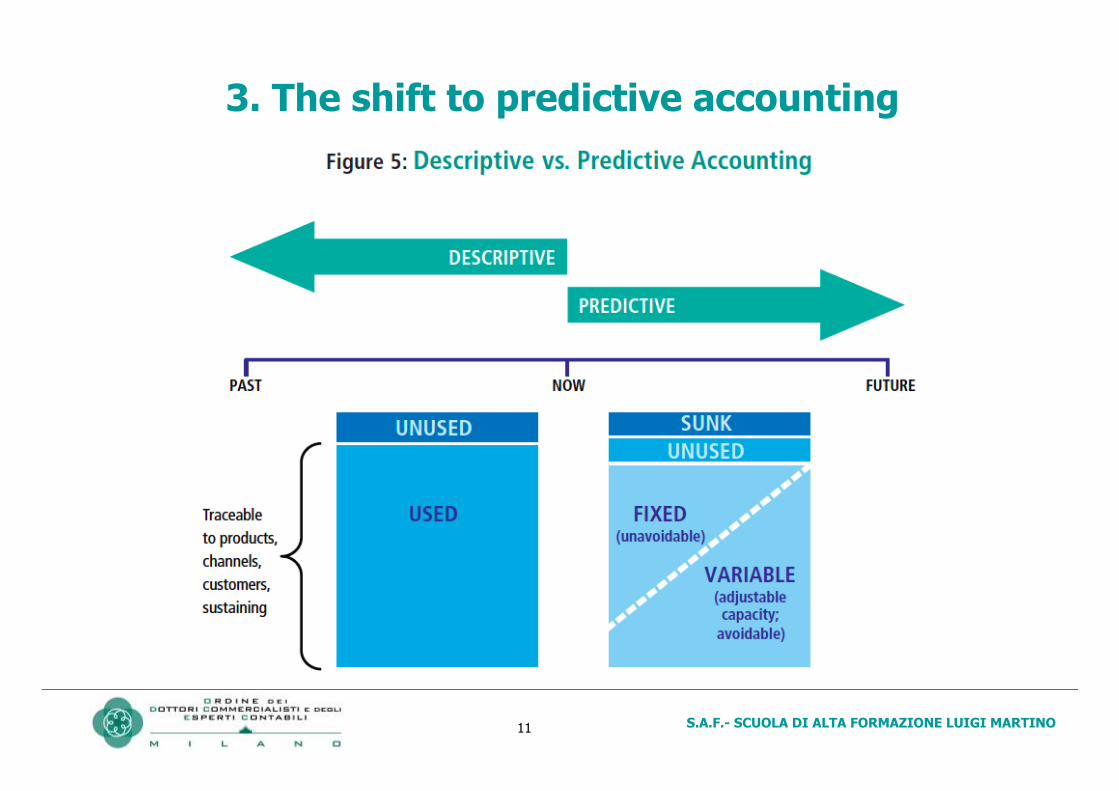

3. The shift to predictive accounting

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 11

3. The shift to predictive accounting

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 12

4. Business Analytics Embedded in EPM Methods

Trend 4 https://www.youtube.com/watch?v=1vZpk1-8cWE&list=PL7jmrwgbi8y1YyzRulQXqX4TvftOcPOK6&index=4

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 13

4. Business Analytics Embedded in EPM Methods

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 14

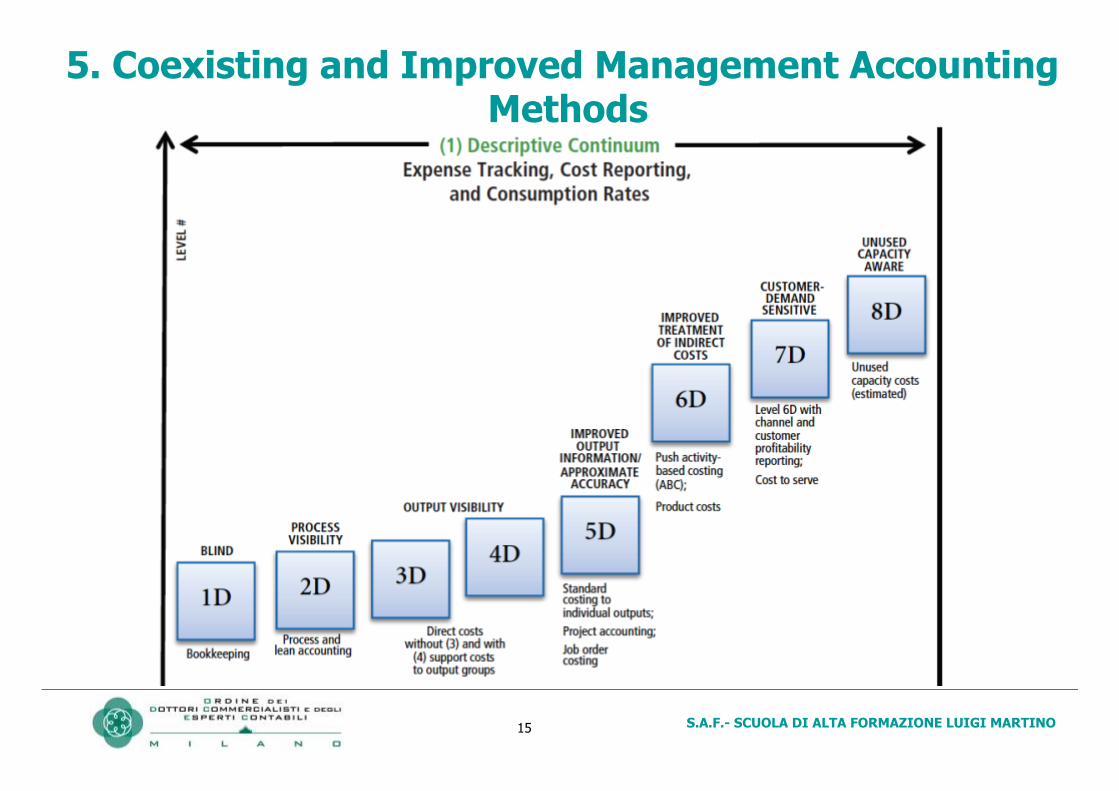

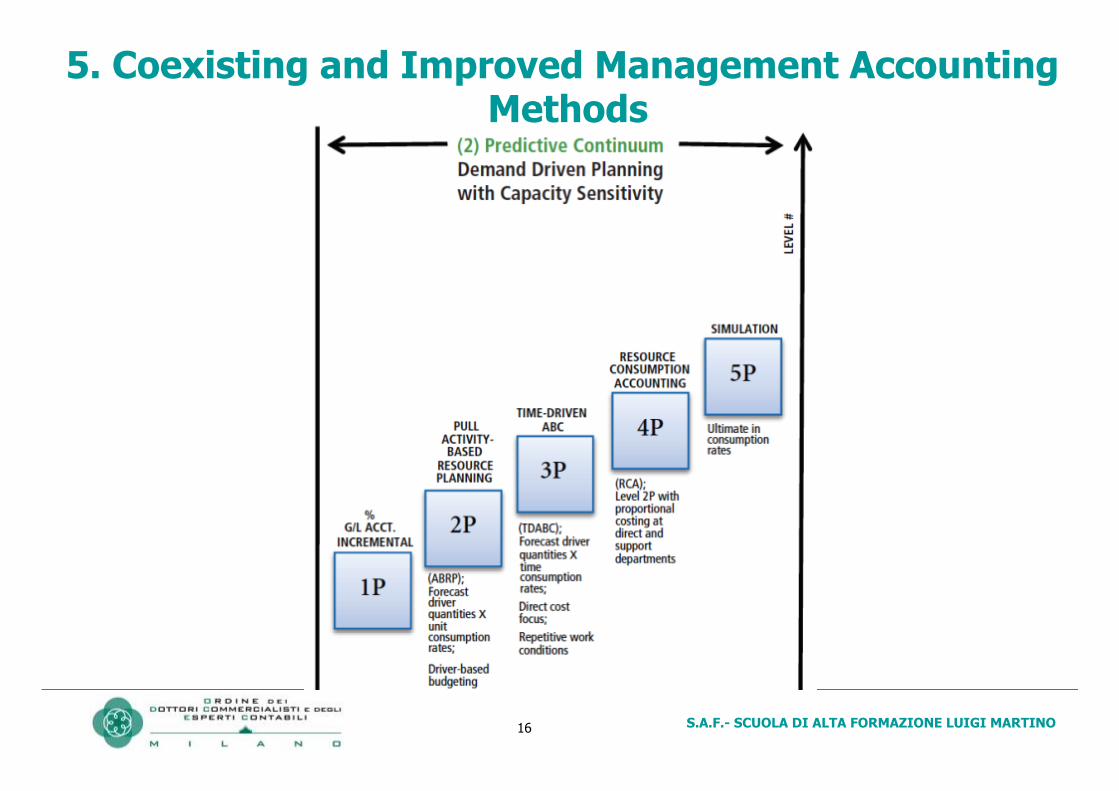

5. Coexisting and Improved Management Accounting Methods

Trend 5 https://www.youtube.com/watch?v=7iQLVxRVwH4&list=PL7jmrwgbi8y1YyzRulQXqX4TvftOcPOK6&index=5

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 15

5. Coexisting and Improved Management Accounting Methods

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 16

5. Coexisting and Improved Management Accounting Methods

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 17

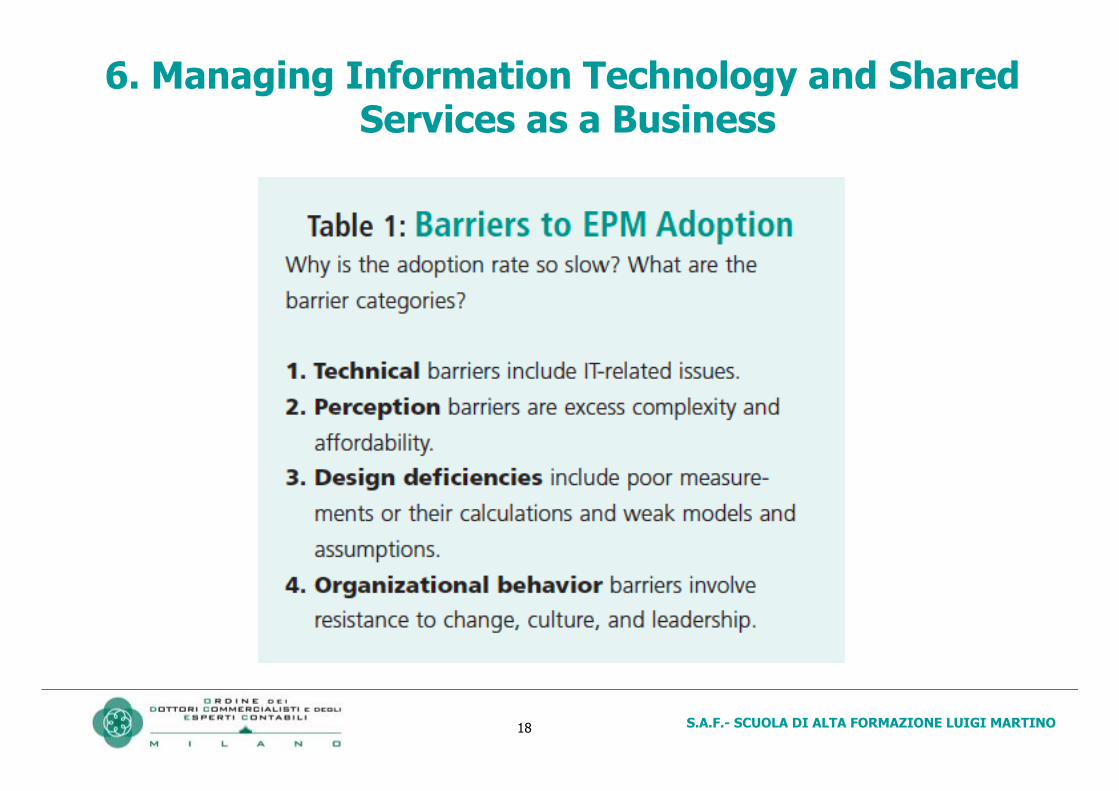

6. Managing Information Technology and Shared Services as a Business

Trend 6 https://www.youtube.com/watch?v=prHH8zuxrFI&list=PL7jmrwgbi8y1YyzRulQXqX4TvftOcPOK6&index=6

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 18

6. Managing Information Technology and Shared Services as a Business

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 19

7. The Need for Better Skills and Competency with Behavioral Cost Management

Trend 7 https://www.youtube.com/watch?v=W5IaDO_N3B8&list=PL7jmrwgbi8y1YyzRulQXqX4TvftOcPOK6&index=7

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 20

Trend No. 7 requires change-agent management accoun- tants to motivate mid-level managers and other “champi- ons” to demonstrate to their coworkers that progressive management accounting and EPM methodologies make sense to implement. There are personal rewards and satisfaction in explaining the importance of overcoming social, behavioral, and cultural barriers so organizations can take next steps.

7. The Need for Better Skills and Competency with Behavioral Cost Management

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 21

1. Expansion from product to channel and customer profitability analysis

2. Management accounting’s expanding role with enterprise performance

management (EPM)

3. The shift to predictive accounting

4. Business Analytics Embedded in EPM Methods

5. Coexisting and Improved Management Accounting Methods

6. Managing Information Technology and Shared Services as a Business

7. The Need for Better Skills and Competency with Behavioral Cost

Management

7 Trends in Management Accounting: Recap

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 22

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 23

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 24

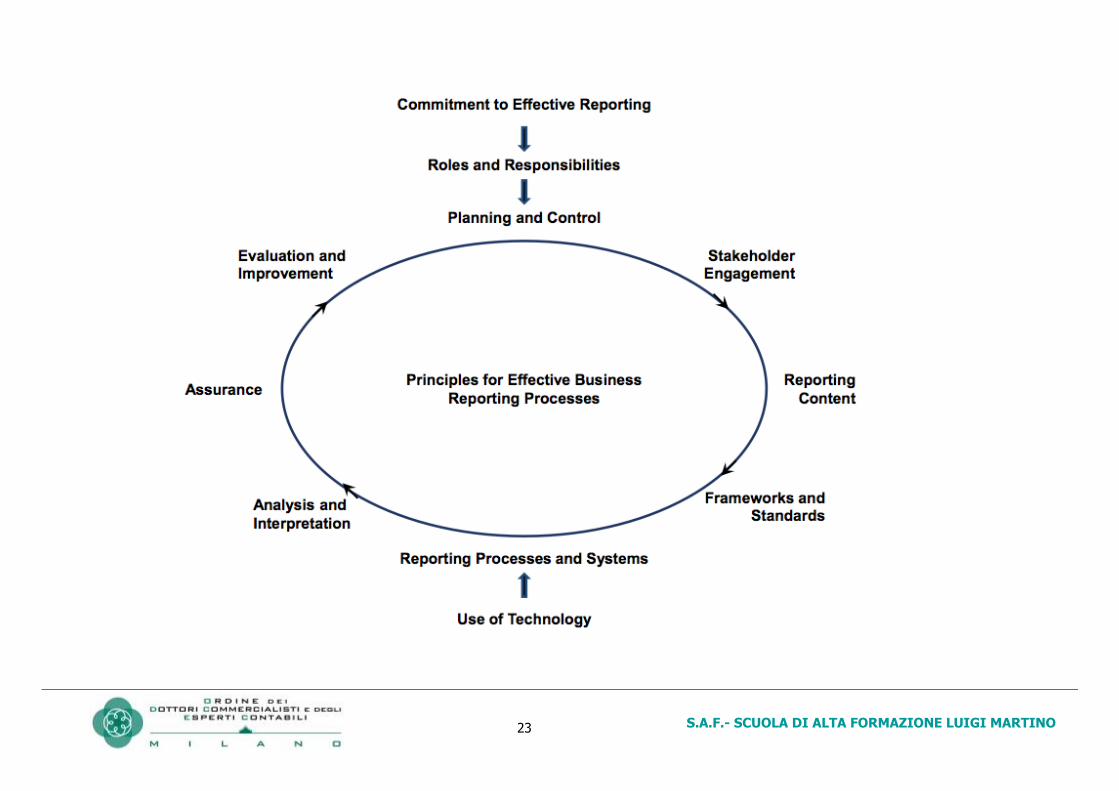

Principle A—Committing to Effective Reporting Processes Senior management should assume leadership for high-quality reports through effective reporting processes. The governing body should demonstrate commitment to high-quality reports and provide strategic input into, and oversight over, the organization’s reporting processes.

Principle B—Determining Roles and Responsibilities The organization should determine the various roles, responsibilities, and consequential capabilities in the reporting process, appoint the appropriate personnel, and coordinate collaboration among those involved in the reporting process.

Principle C—Planning and Controlling the Reporting Processes The organization should develop and implement an effective planning and control cycle for its reporting processes in the context of, and in alignment with, its wider planning and control cycles.

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 25

Principle D—Engaging Stakeholders To ensure the provision of high-quality information, the organization should regularly engage with its internal and external stakeholders and understand their information needs with regard to past, present, and future activities and results of the organization.

Principle E—Defining the Reporting Content Based on the outcomes of its stakeholder engagement, and taking cost-benefit considerations into account, the organization should define the content to be included in its reports and also decide on the audience, layout, and timing of reports.

Principle F—Selecting Frameworks and Standards The organization should have a process in place to ensure that the most appropriate reporting frameworks and standards are selected and that the requirements of those frameworks and standards are aligned with stakeholder information needs.

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 26

Principle G—Determining Reporting Processes The organization should determine what information needs to be captured, processed, analyzed, and reported, and how to organize the information processes and related systems for effective reporting.

Principle H—Using Reporting Technology The organization should (a) identify, analyze, and select appropriate communications tools and (b) decide how to optimize distribution of the organization’s reporting information via the various communications channels.

Principle I—Analyzing and Interpreting Reported Information The organization should ensure that reported information is sufficiently analyzed and interpreted before it is provided to internal and external stakeholders.

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 27

Principle J—Obtaining Assurance and Providing for Accountability When obtaining internal or external assurance is not a matter of compliance, the organization should consider voluntary internal or external assurance on its reports and reporting processes.

Principle K—Evaluating and Improving Reporting Processes The organization should regularly evaluate its reporting processes and systems in order to identify and carry out further improvements required for maintaining reporting effectiveness.

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 28

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 29

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 30

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 31

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 32

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 33

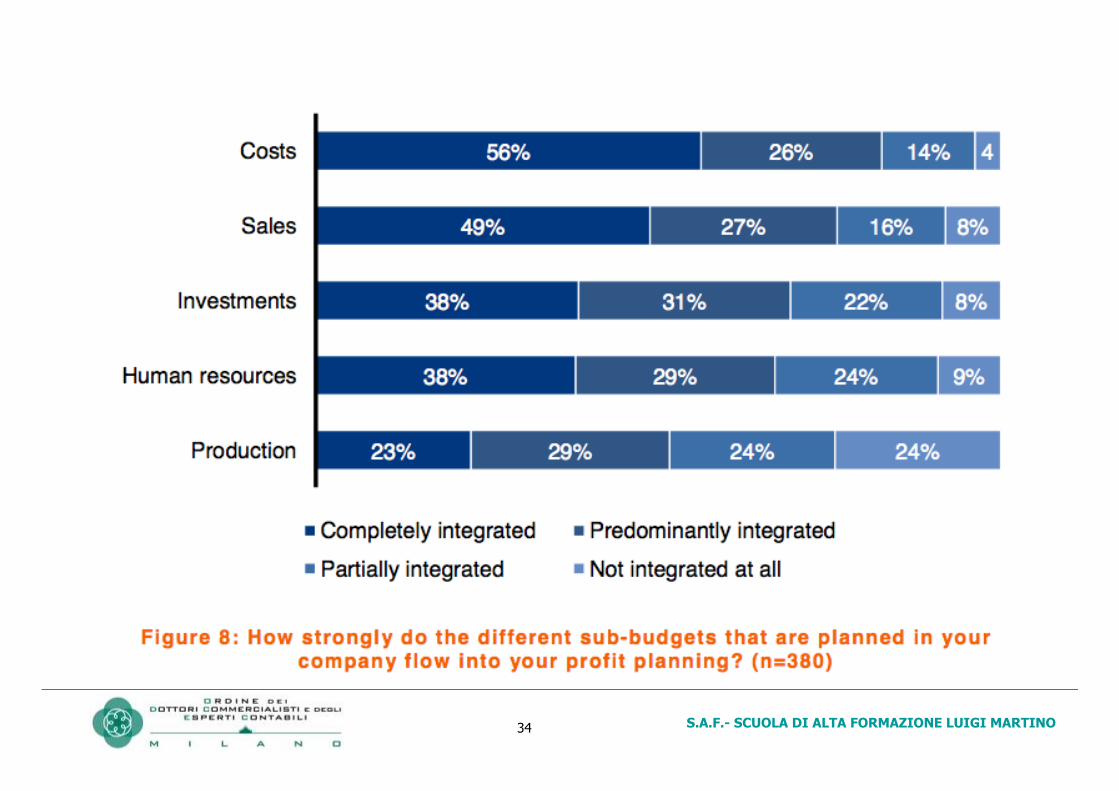

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 34

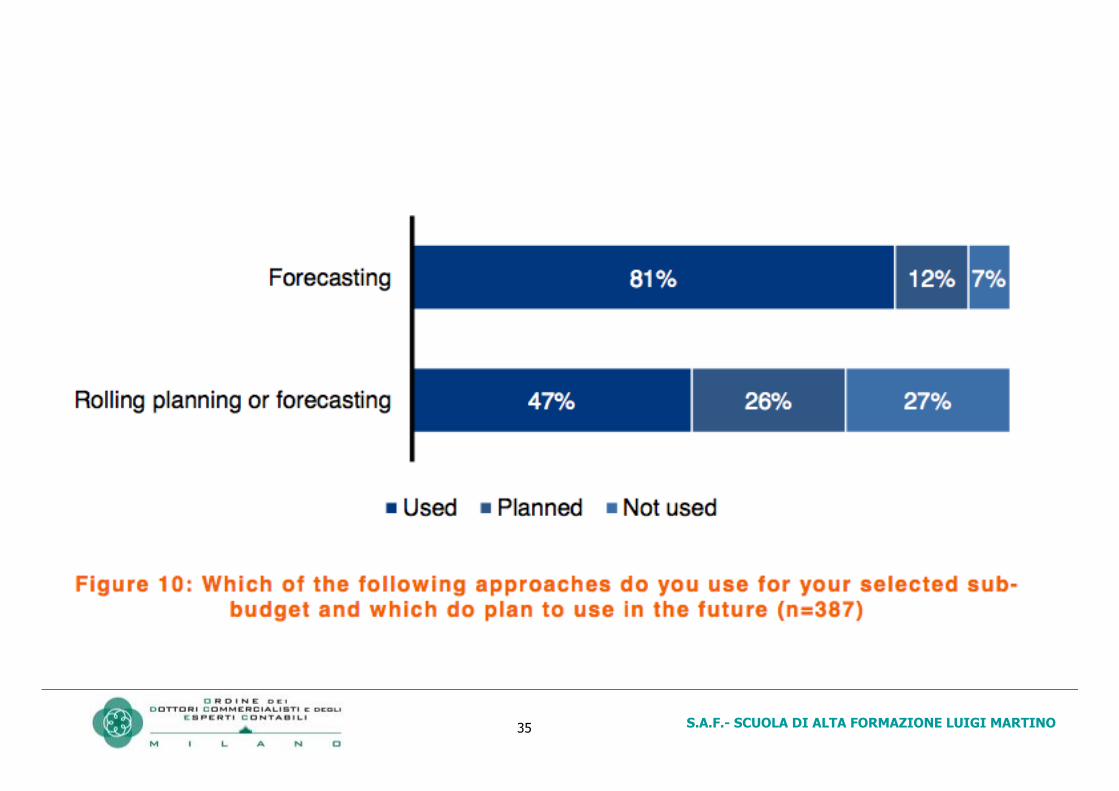

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 35

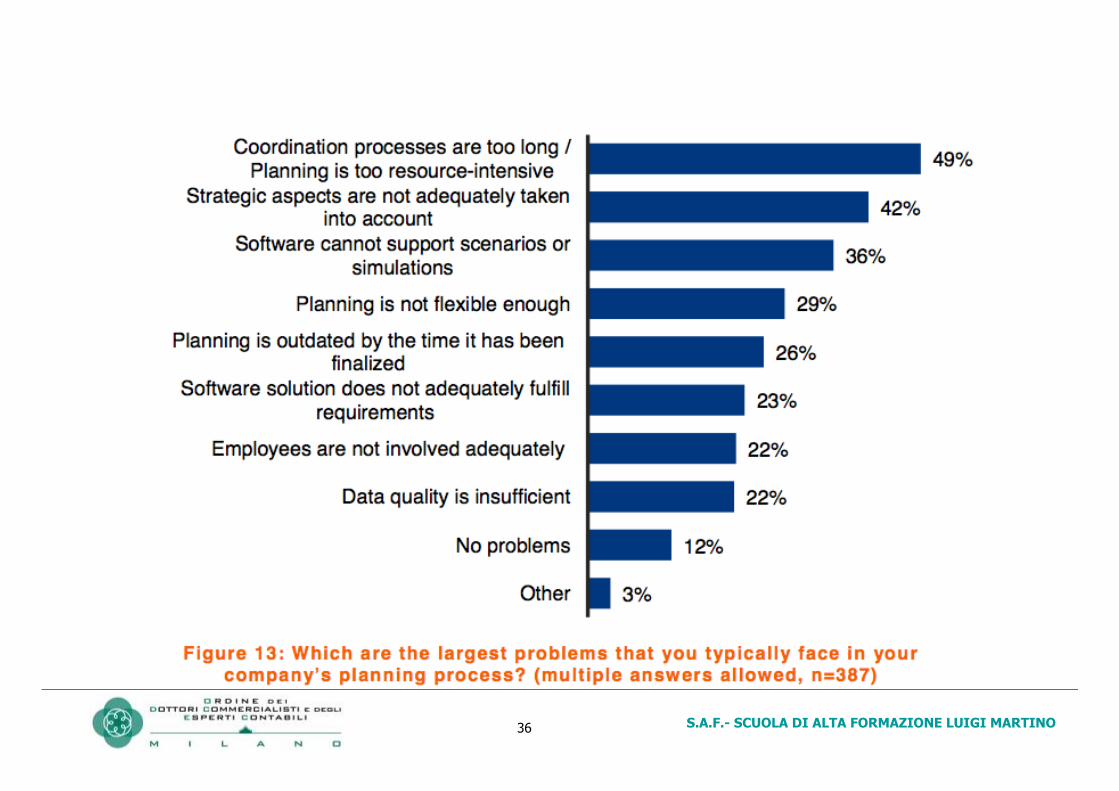

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 36

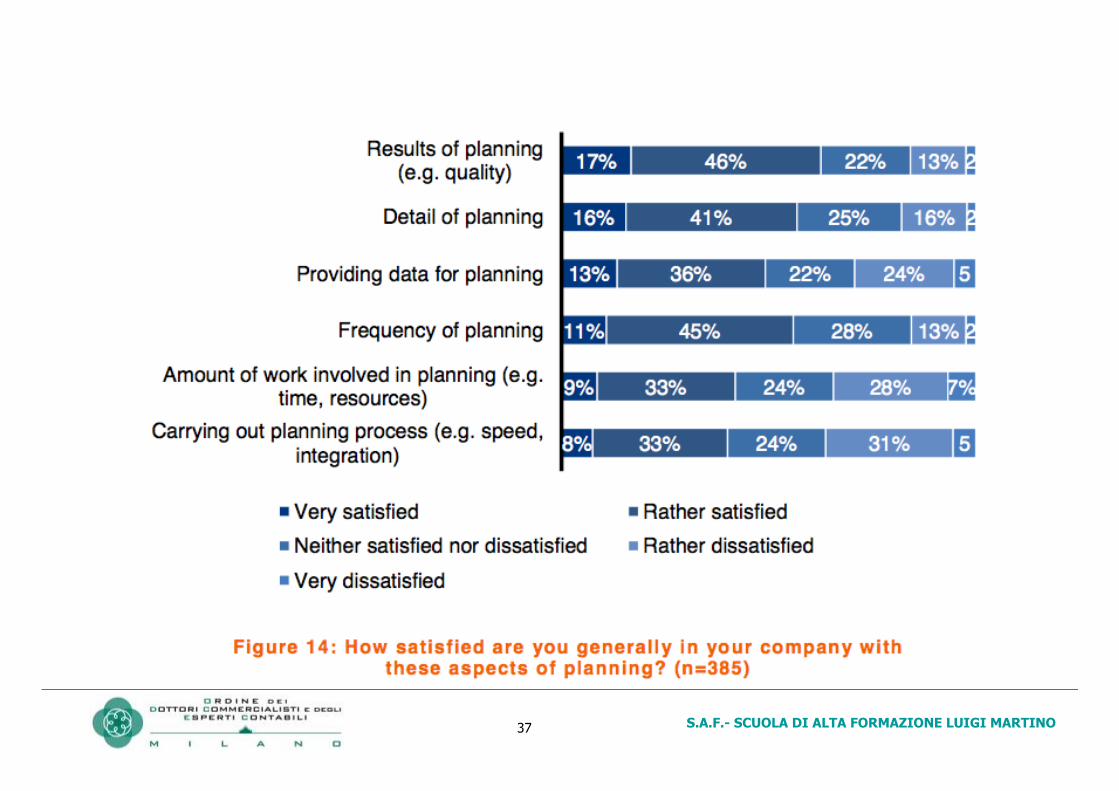

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 37

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 38

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 39

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 40

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 41

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 42

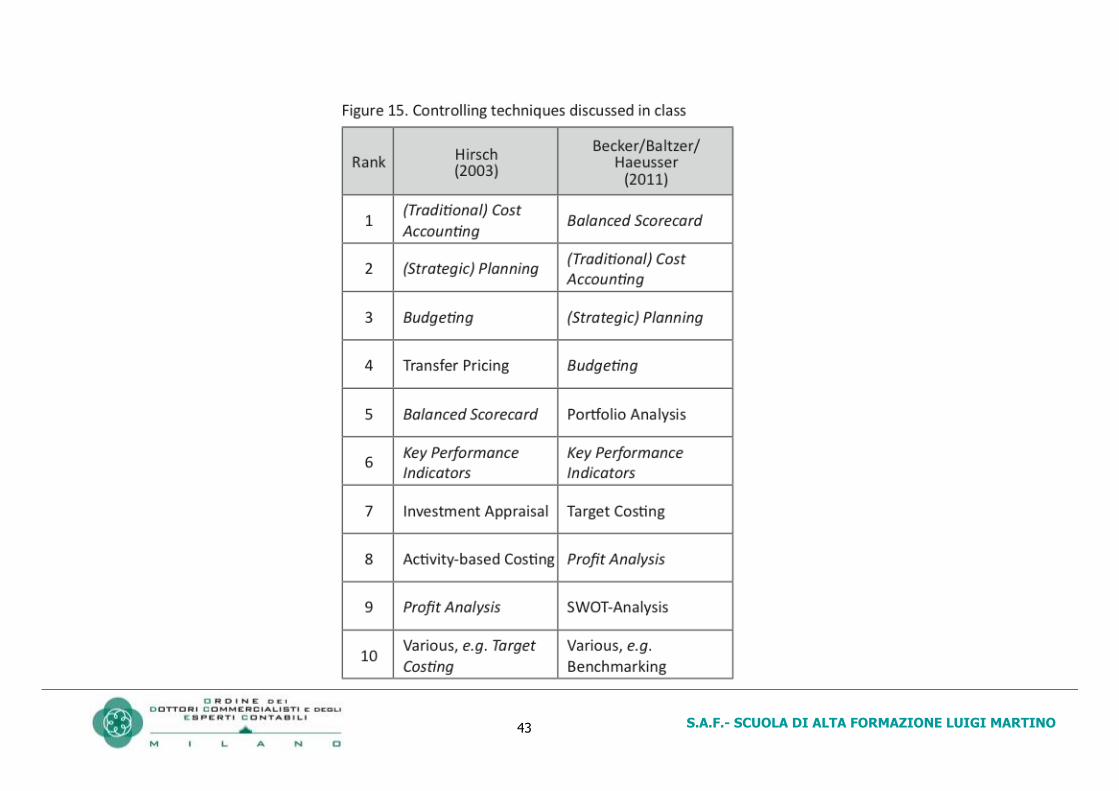

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 43

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 44

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 45

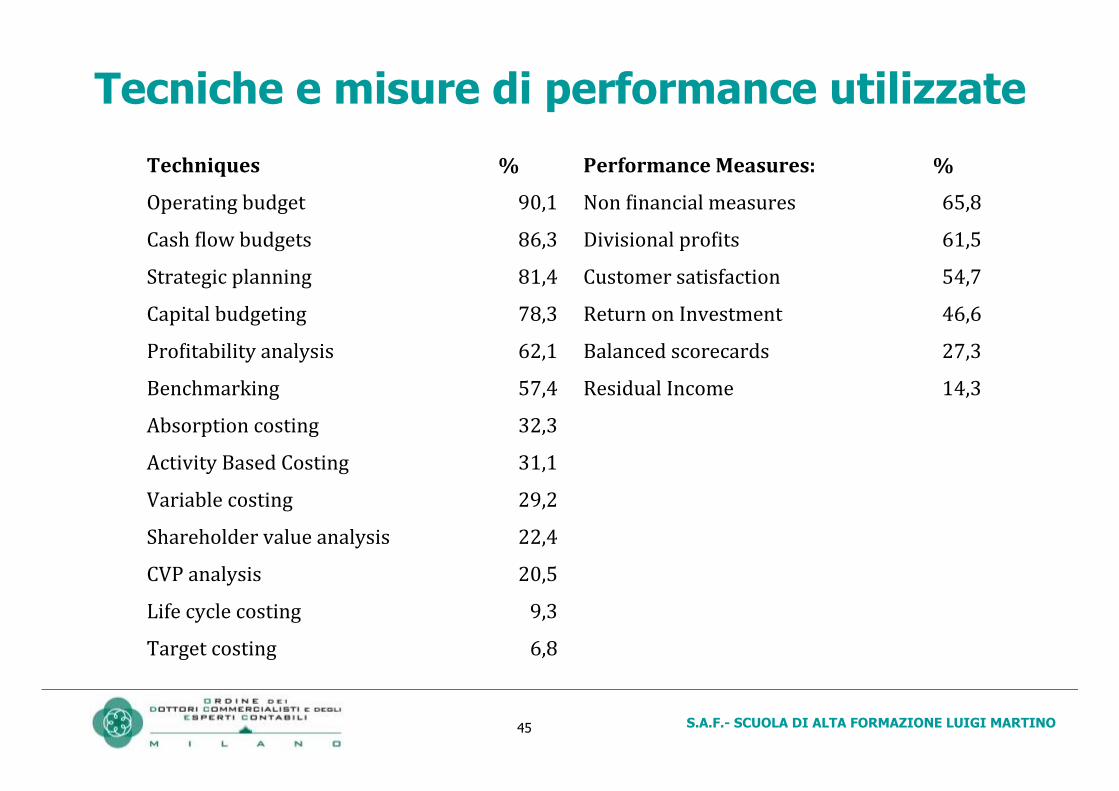

Tecniche e misure di performance utilizzate

Techniques % Performance Measures: %

Operating budget 90,1 Non 4inancial measures 65,8

Cash 4low budgets 86,3 Divisional pro4its 61,5

Strategic planning 81,4 Customer satisfaction 54,7

Capital budgeting 78,3 Return on Investment 46,6

Pro4itability analysis 62,1 Balanced scorecards 27,3

Benchmarking 57,4 Residual Income 14,3

Absorption costing 32,3

Activity Based Costing 31,1

Variable costing 29,2

Shareholder value analysis 22,4

CVP analysis 20,5

Life cycle costing 9,3

Target costing 6,8

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 46

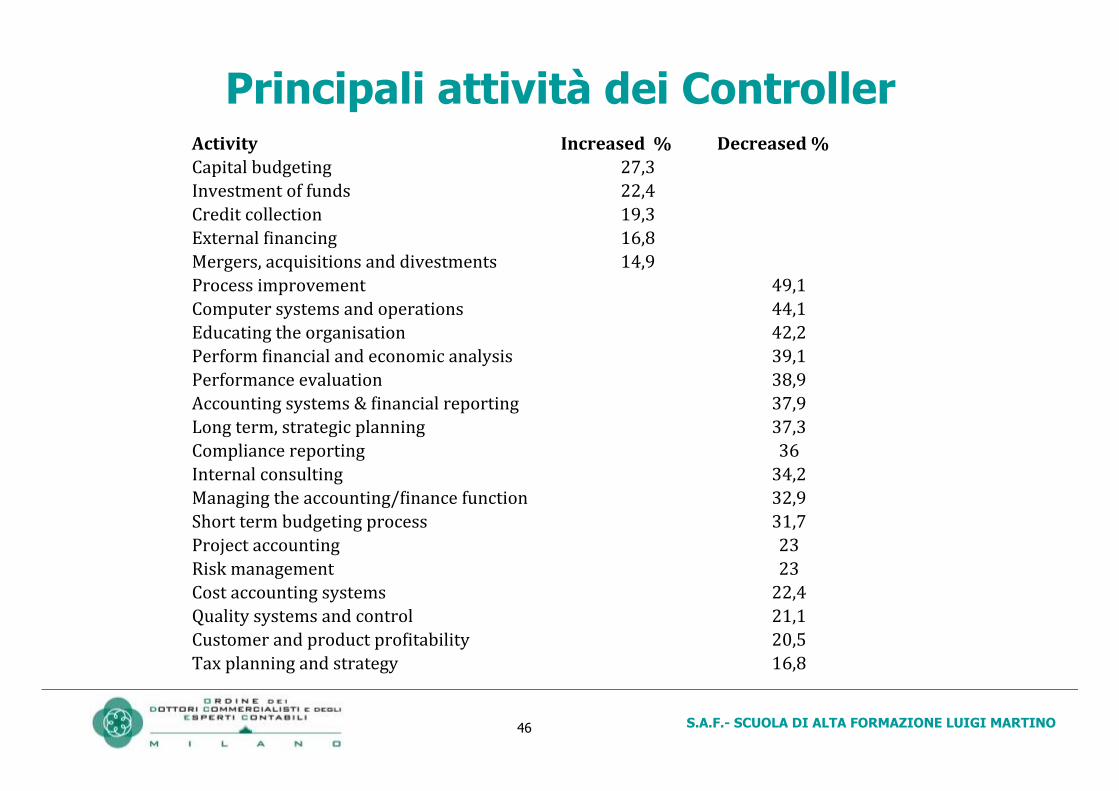

Activity Increased % Decreased % Capital budgeting 27,3 Investment of funds 22,4 Credit collection 19,3 External 4inancing 16,8 Mergers, acquisitions and divestments 14,9 Process improvement 49,1 Computer systems and operations 44,1 Educating the organisation 42,2 Perform 4inancial and economic analysis 39,1 Performance evaluation 38,9 Accounting systems & 4inancial reporting 37,9 Long term, strategic planning 37,3 Compliance reporting 36 Internal consulting 34,2 Managing the accounting/4inance function 32,9 Short term budgeting process 31,7 Project accounting 23 Risk management 23 Cost accounting systems 22,4 Quality systems and control 21,1 Customer and product pro4itability 20,5 Tax planning and strategy 16,8

Principali attività dei Controller

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 47

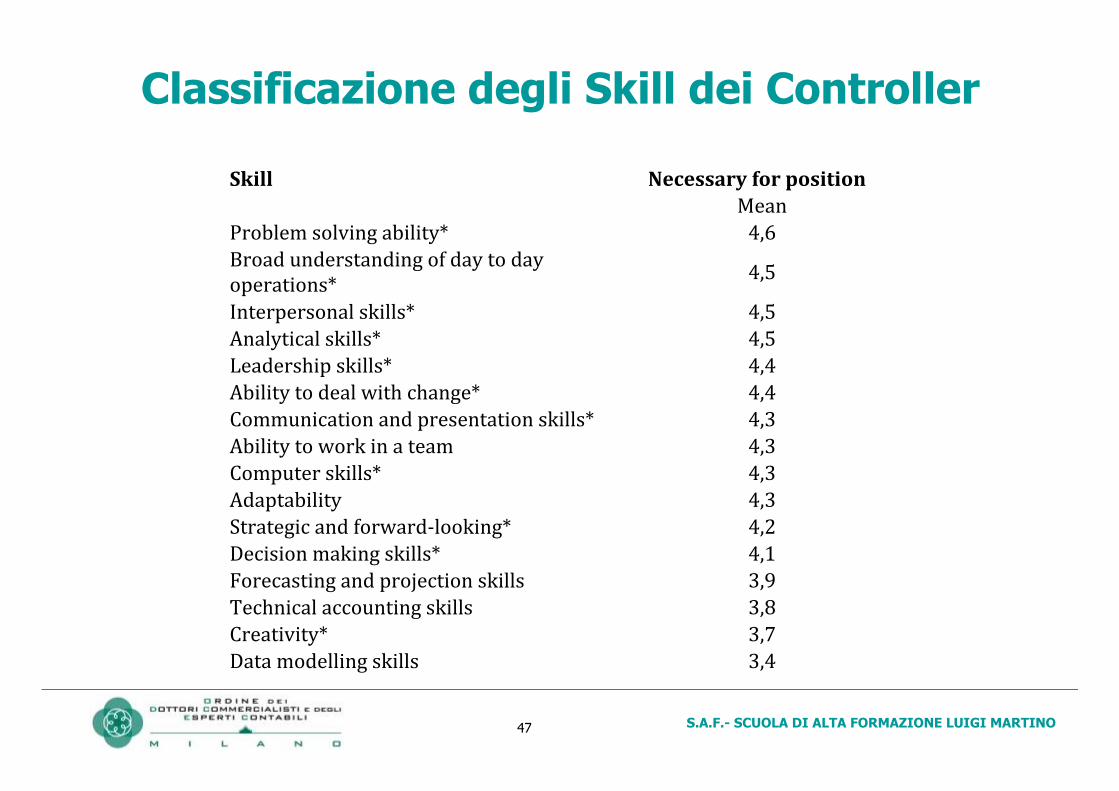

Skill Necessary for position Mean

Problem solving ability* 4,6 Broad understanding of day to day operations* 4,5

Interpersonal skills* 4,5 Analytical skills* 4,5 Leadership skills* 4,4 Ability to deal with change* 4,4 Communication and presentation skills* 4,3 Ability to work in a team 4,3 Computer skills* 4,3 Adaptability 4,3 Strategic and forward-‐looking* 4,2 Decision making skills* 4,1 Forecasting and projection skills 3,9 Technical accounting skills 3,8 Creativity* 3,7 Data modelling skills 3,4

Classificazione degli Skill dei Controller

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 48

Conclusioni dello Studio

CONCLUSIONS

The results of this study show quite clearly that those working as a management

accountant perceive their role as a changing one, and points to evidence that the

change is mainly in the tasks that management accountants must undertake.

Much more emphasis is being placed on strategy and decision-making roles,

rather than the more traditional areas of costing and financial analysis. The one

traditional area to remain high on the list of important areas for management

accounting is budgeting.

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 49

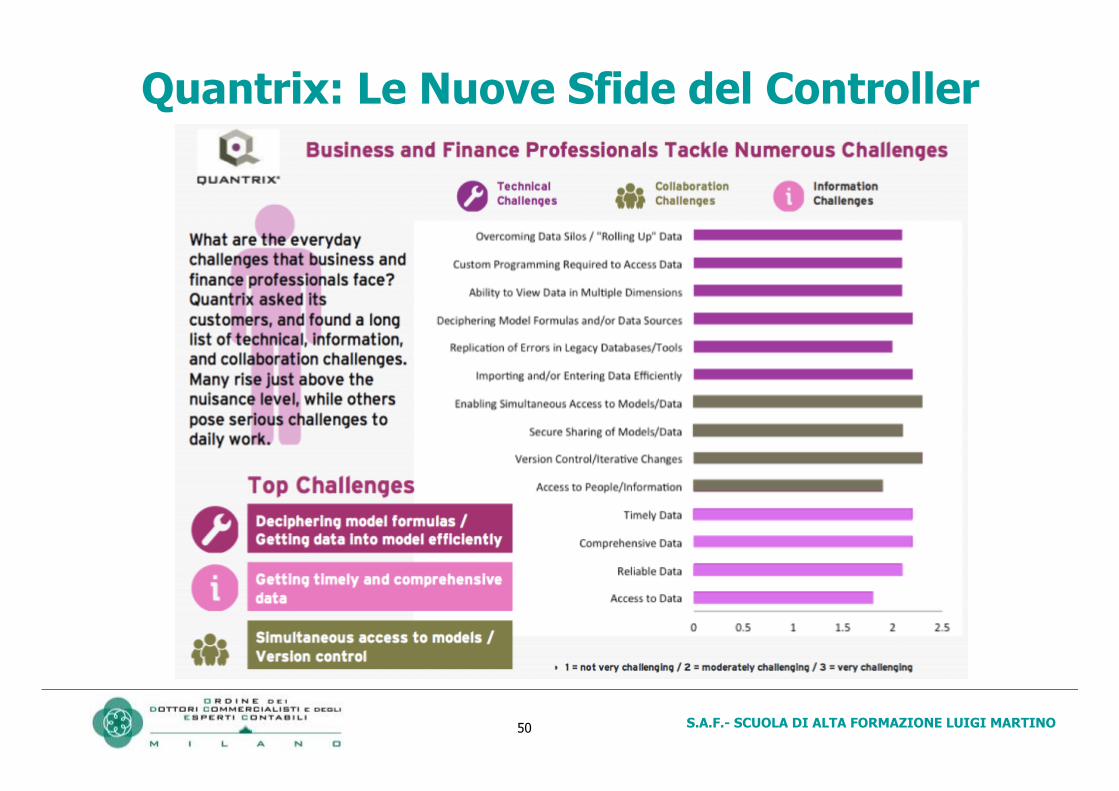

Quantrix: Le Nuove Sfide del Controller

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 50

Quantrix: Le Nuove Sfide del Controller

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 51

Quantrix: Utilizzo del Cloud

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 52

Quantrix: Frequenza di Presentazione Dati

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 53

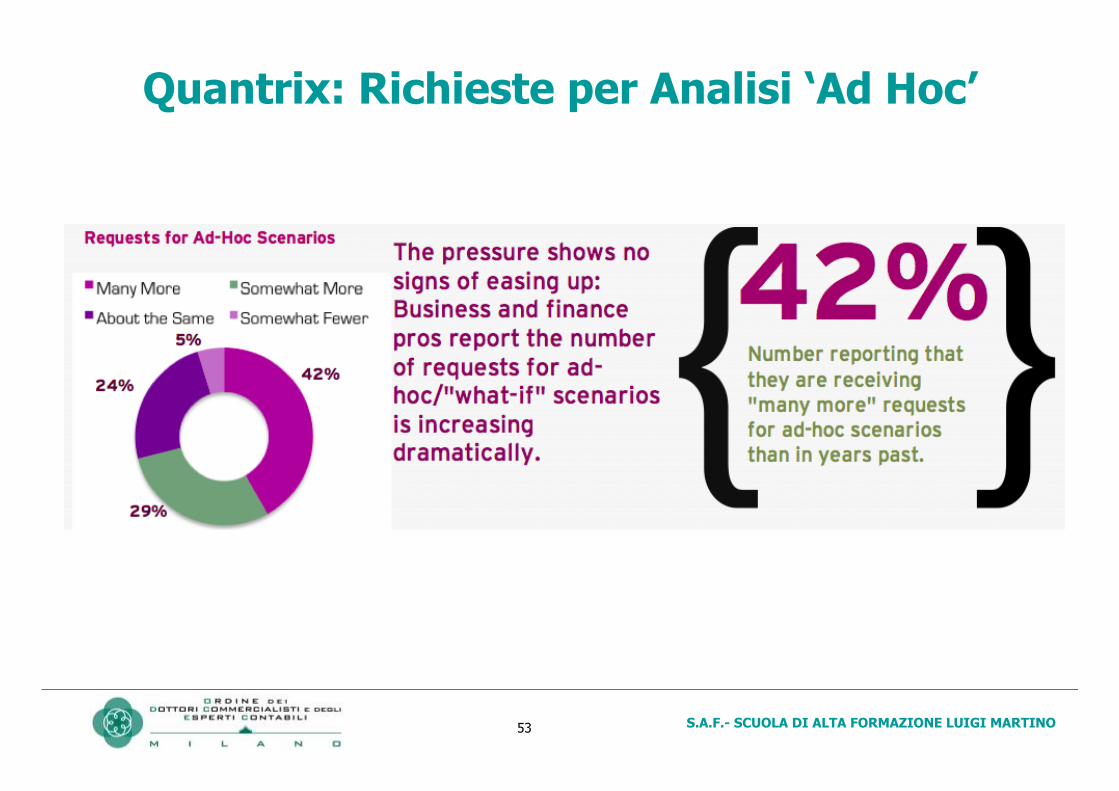

Quantrix: Richieste per Analisi ‘Ad Hoc’

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 54

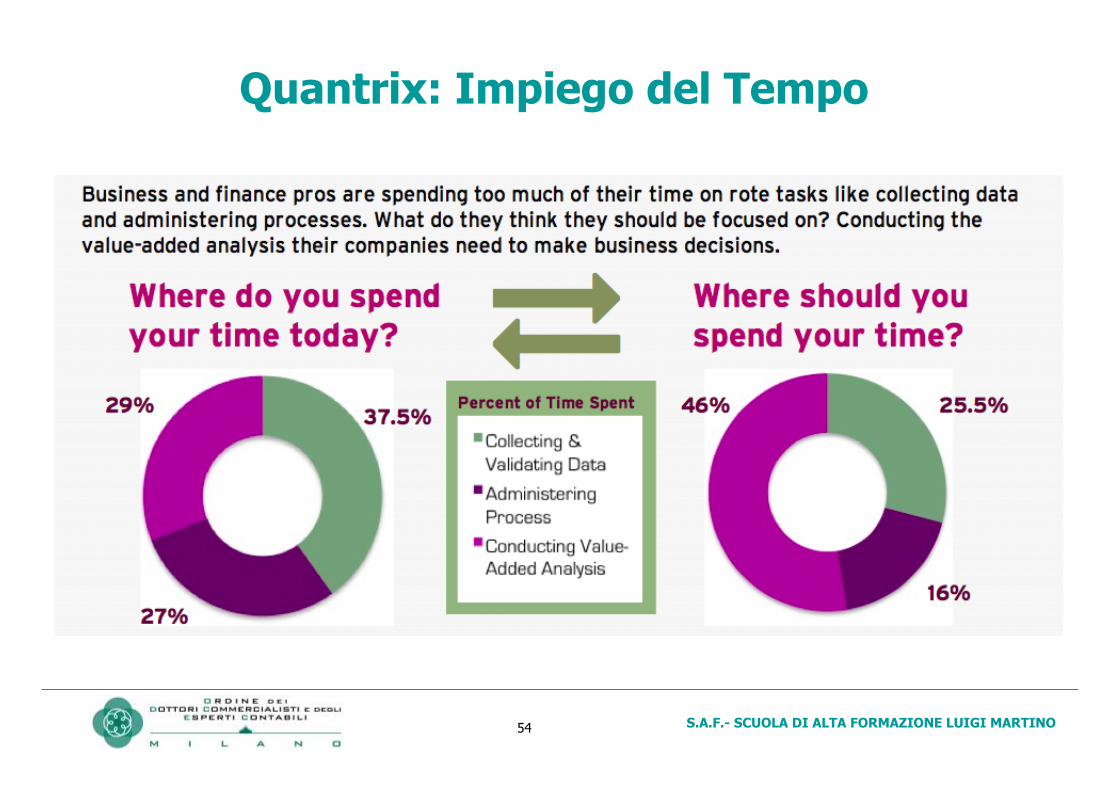

Quantrix: Impiego del Tempo

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 55

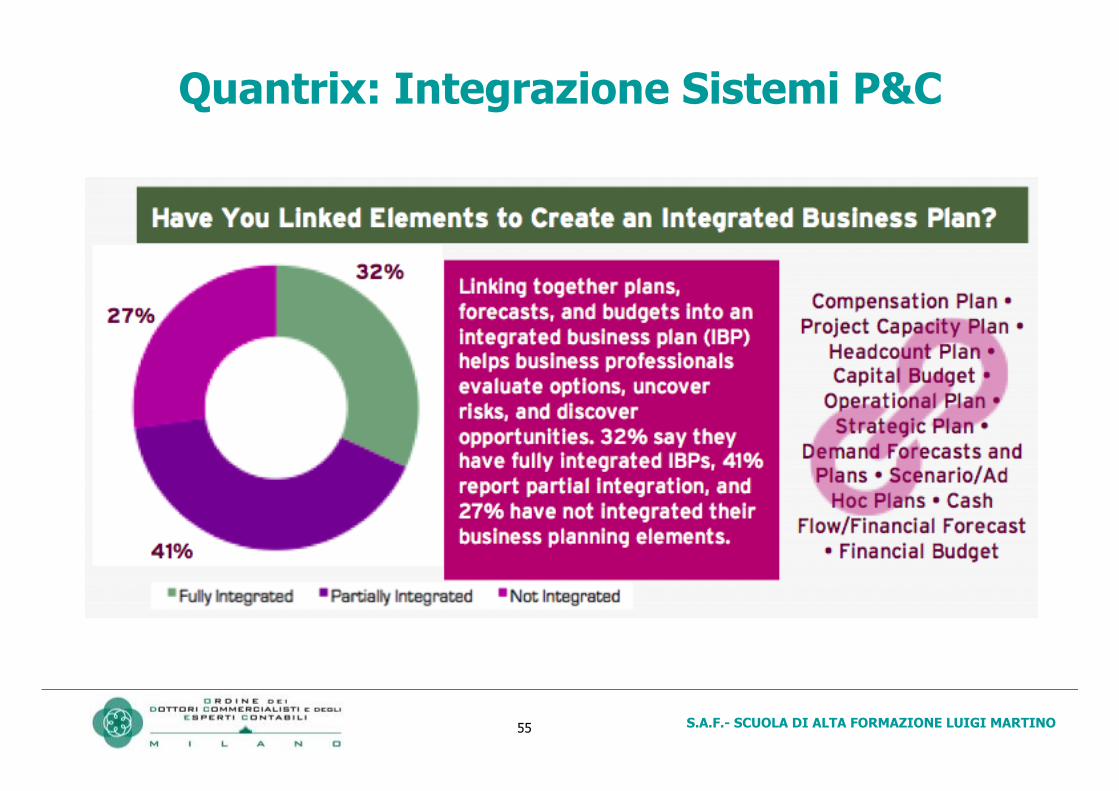

Quantrix: Integrazione Sistemi P&C

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 56

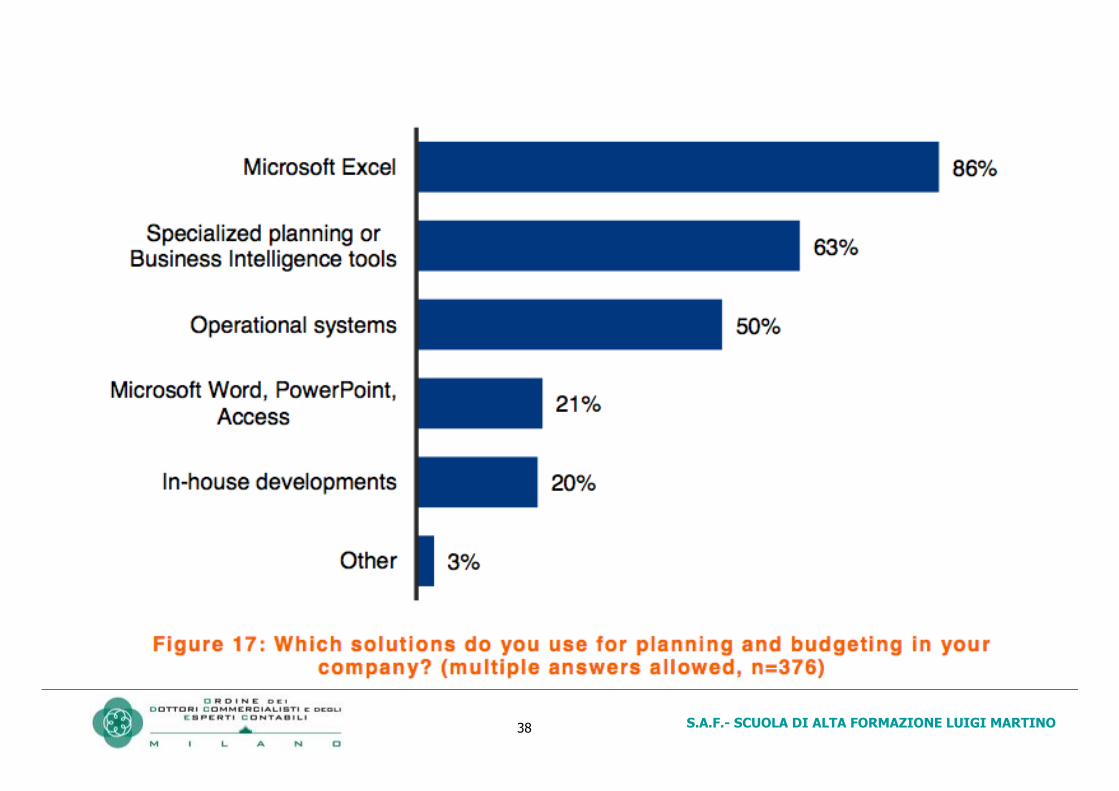

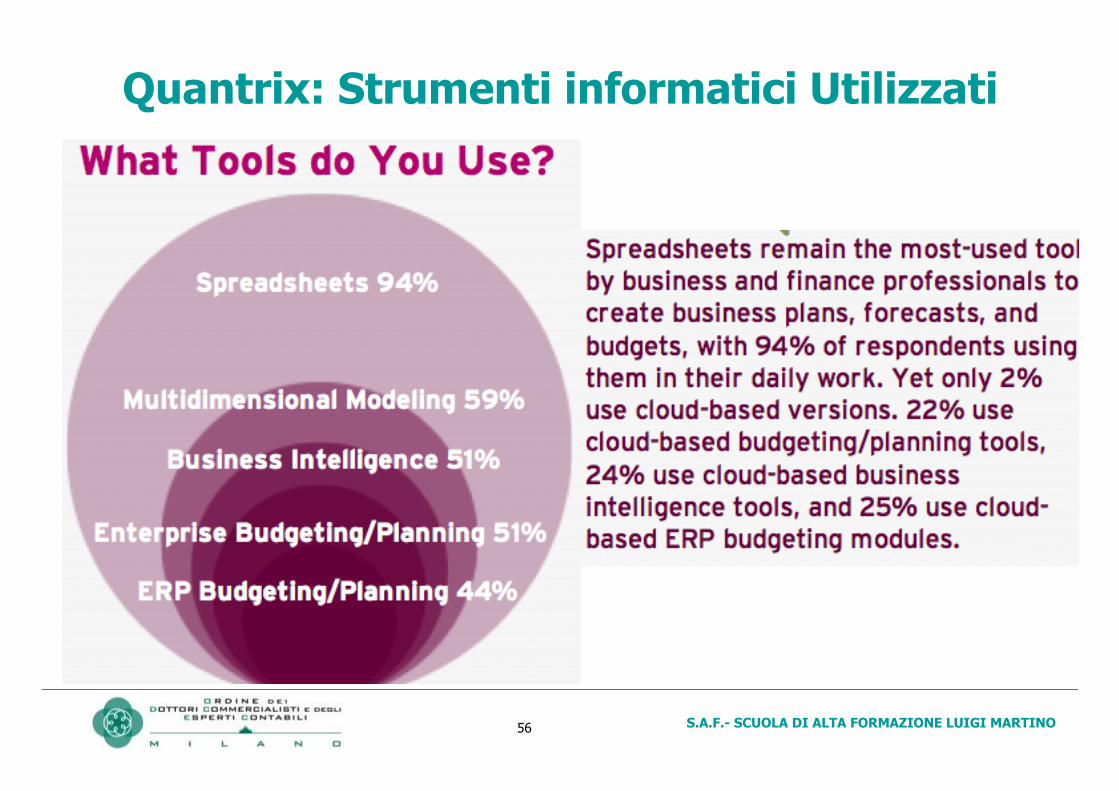

Quantrix: Strumenti informatici Utilizzati

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 57

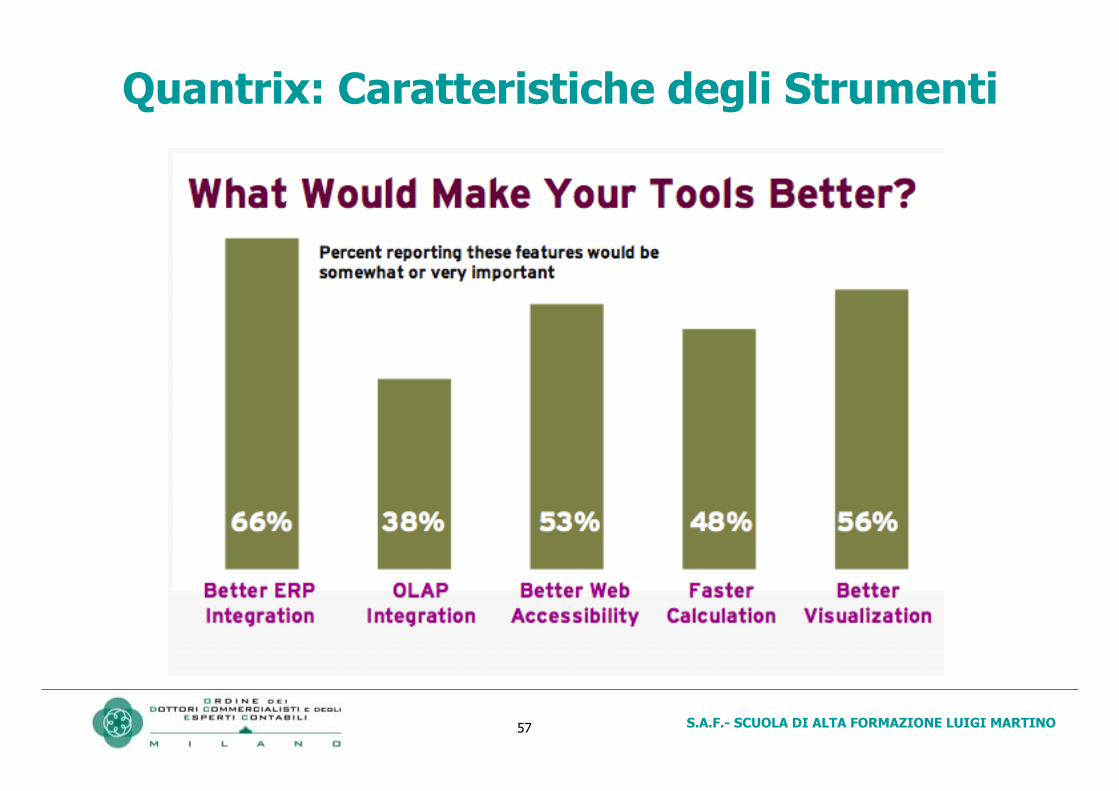

Quantrix: Caratteristiche degli Strumenti

S.A.F.- SCUOLA DI ALTA FORMAZIONE LUIGI MARTINO 58

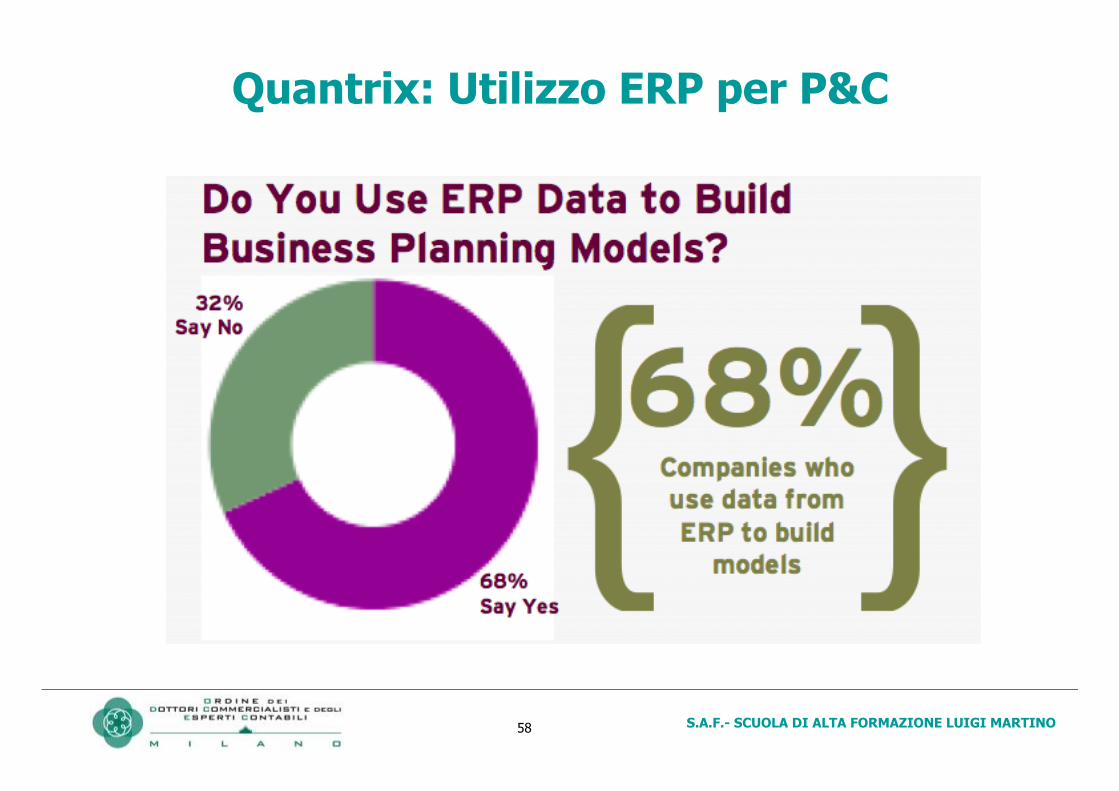

Quantrix: Utilizzo ERP per P&C