RELAZIONE FINANZIARIASEMESTRAL E AL 30 GIUGNO - lgh.it year... · RELAZIONE FINANZIARIASEMESTRAL E...

92

1 RELAZIONE FINANZIARIASEMESTRAL E AL 30 GIUGNO 2015 RELAZIONE FINANZIARIA HALF-YEAR CONDENSED CONSOLIDATED FINANCIAL REPORT AS AT JUNE 30, 2017

-

Upload

phungduong -

Category

Documents

-

view

222 -

download

0

Transcript of RELAZIONE FINANZIARIASEMESTRAL E AL 30 GIUGNO - lgh.it year... · RELAZIONE FINANZIARIASEMESTRAL E...

1

RELAZIONE

FINANZIARIASEMESTRALE AL

30 GIUGNO 2015

RELAZIONE FINANZIARIA

HALF -YEAR CONDENSED CONSOLIDATED FINANCIAL

REPORT AS AT JUNE 30, 2017

1

I. INTRODUCTION .............................................................................................................. 2

Activity ................................................................................................................................................................... 4

Group highlights and key financial indicators ........................................................................................................ 6

Structure and details of the companies in the LGH Group ..................................................................................... 8

IAS/IFRS accounting policies................................................................................................................................. 9

II. DIRECTORS’ BUSINESS REPORT ............................................................................................................ 10

Significant events occurring during the 1st half of 2017 ....................................................................................... 11

Summary of Group’s financial performance, equity and cash flows .................................................................... 11

Regulatory framework .......................................................................................................................................... 20

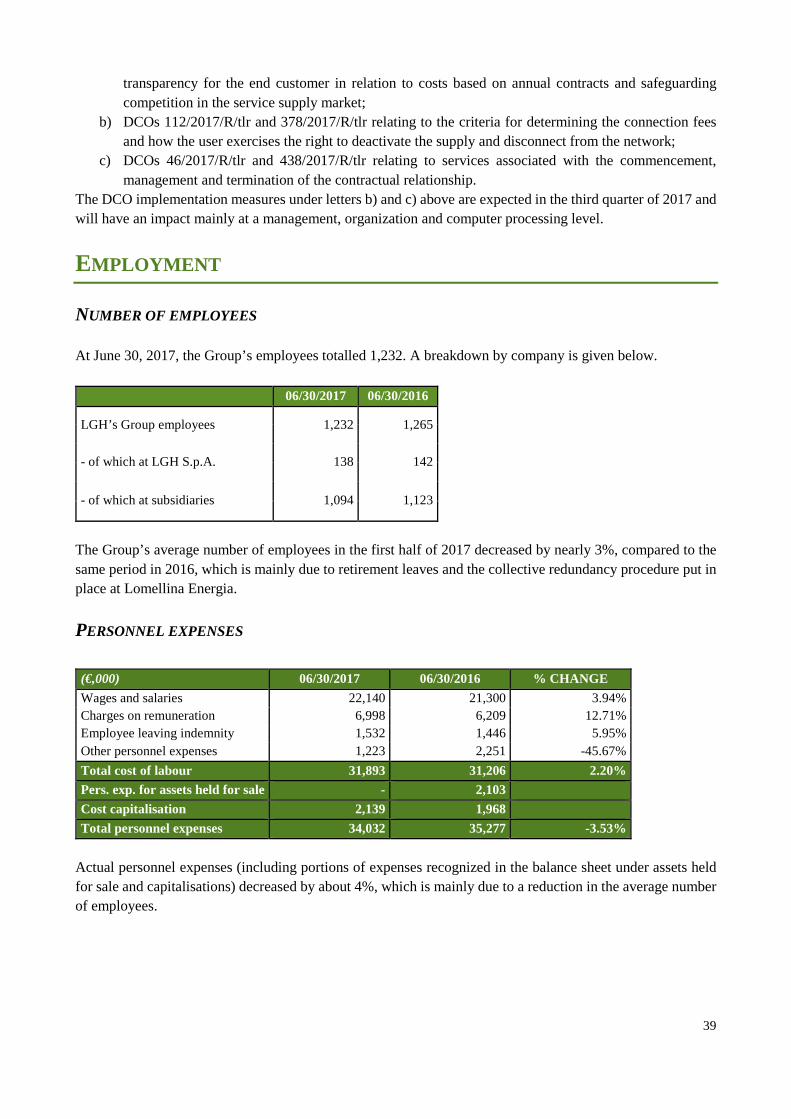

Employment .......................................................................................................................................................... 39

Corporate risk management .................................................................................................................................. 40

Other disclosures .................................................................................................................................................. 47

Significant events occurring after June 30, 2017 .................................................................................................. 50

Audit of the half-year condensed consolidated financial statements .................................................................... 50

III. CONSOLIDATED FINANCIAL STATEMENTS ............................................................................................ 52

Financial Statements ............................................................................................................................................. 53

Explanatory notes ................................................................................................................................................. 58

Accounting policy ................................................................................................................................................. 58

Explanatory notes ................................................................................................................................................. 64

2

I. INTRODUCTION

3

BOARD OF DIRECTORS CHAIRMAN Antonio Vivenzi CHIEF EXECUTIVE OFFICER Massimiliano Spiridione Masi BOARD MEMBERS Maria Ester Benigni Lorenzo Giorgio Giussani

Fulvio Roncari Emilia Rio Rita Daniela Giupponi Dino Martinazzoli Salvatore Nupieri Massimo Maria Mustarelli Fiorella Lazzari Paolo Formentini

BOARD OF AUDITORS CHAIRMAN Catia Rosa Sinelli STATUTORY AUDITORS Antonio Fezzi Patrizia Apostoli DEPUTY AUDITORS Luigi Foresti Simona Pezzolo De Rossi

INDEPENDENT AUDITORS EY S.p.A.

4

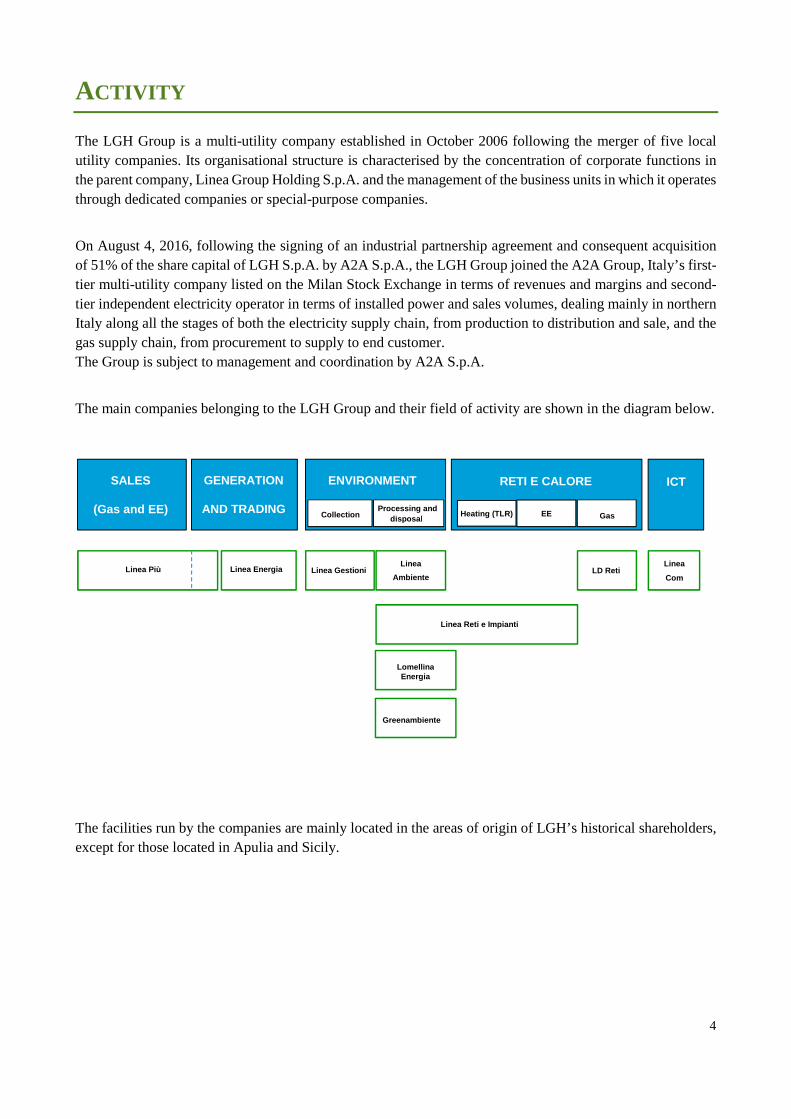

ACTIVITY The LGH Group is a multi-utility company established in October 2006 following the merger of five local utility companies. Its organisational structure is characterised by the concentration of corporate functions in the parent company, Linea Group Holding S.p.A. and the management of the business units in which it operates through dedicated companies or special-purpose companies.

On August 4, 2016, following the signing of an industrial partnership agreement and consequent acquisition of 51% of the share capital of LGH S.p.A. by A2A S.p.A., the LGH Group joined the A2A Group, Italy’s first-tier multi-utility company listed on the Milan Stock Exchange in terms of revenues and margins and second-tier independent electricity operator in terms of installed power and sales volumes, dealing mainly in northern Italy along all the stages of both the electricity supply chain, from production to distribution and sale, and the gas supply chain, from procurement to supply to end customer. The Group is subject to management and coordination by A2A S.p.A.

The main companies belonging to the LGH Group and their field of activity are shown in the diagram below.

The facilities run by the companies are mainly located in the areas of origin of LGH’s historical shareholders, except for those located in Apulia and Sicily.

Linea Reti e Impianti

Linea

Ambiente Linea Più LD Reti Linea Energia

Linea

Com

SALES

(Gas and EE)

GENERATION

AND TRADING

ENVIRONMENT RETI E CALORE

Heating (TLR) EE Gas

ICT

Collection Processing and disposal

Linea Gestioni

Lomellina Energia

Greenambiente

5

6

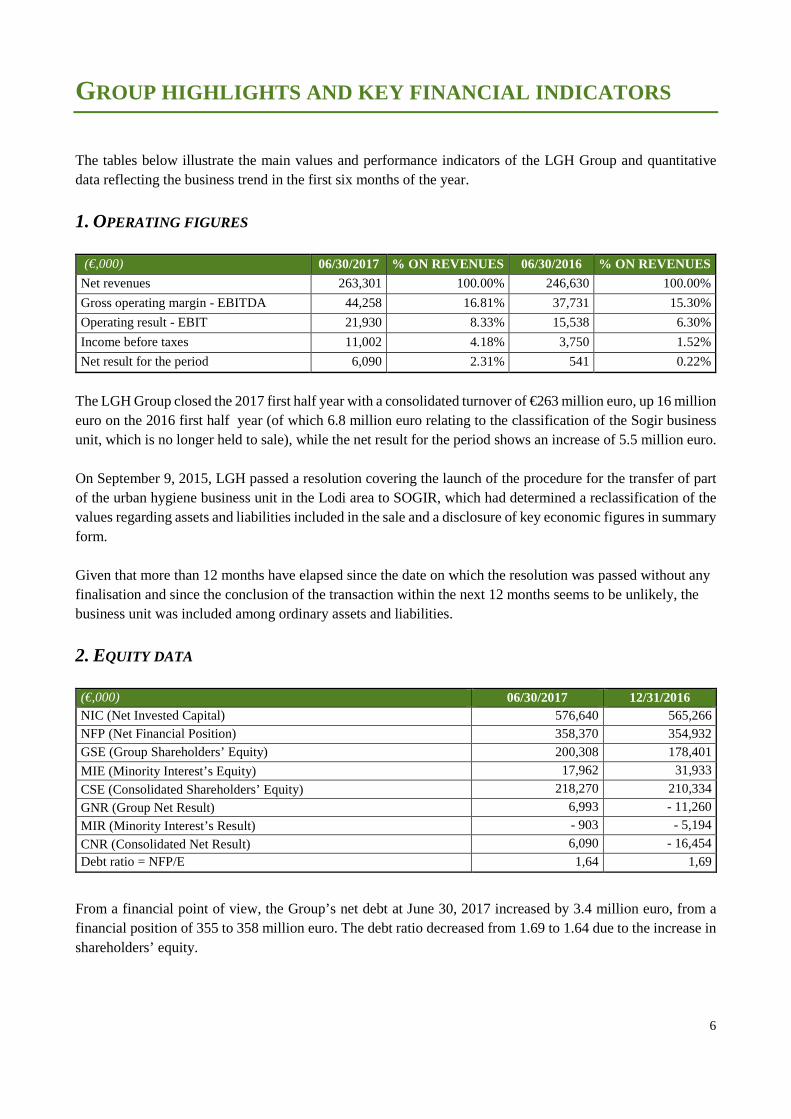

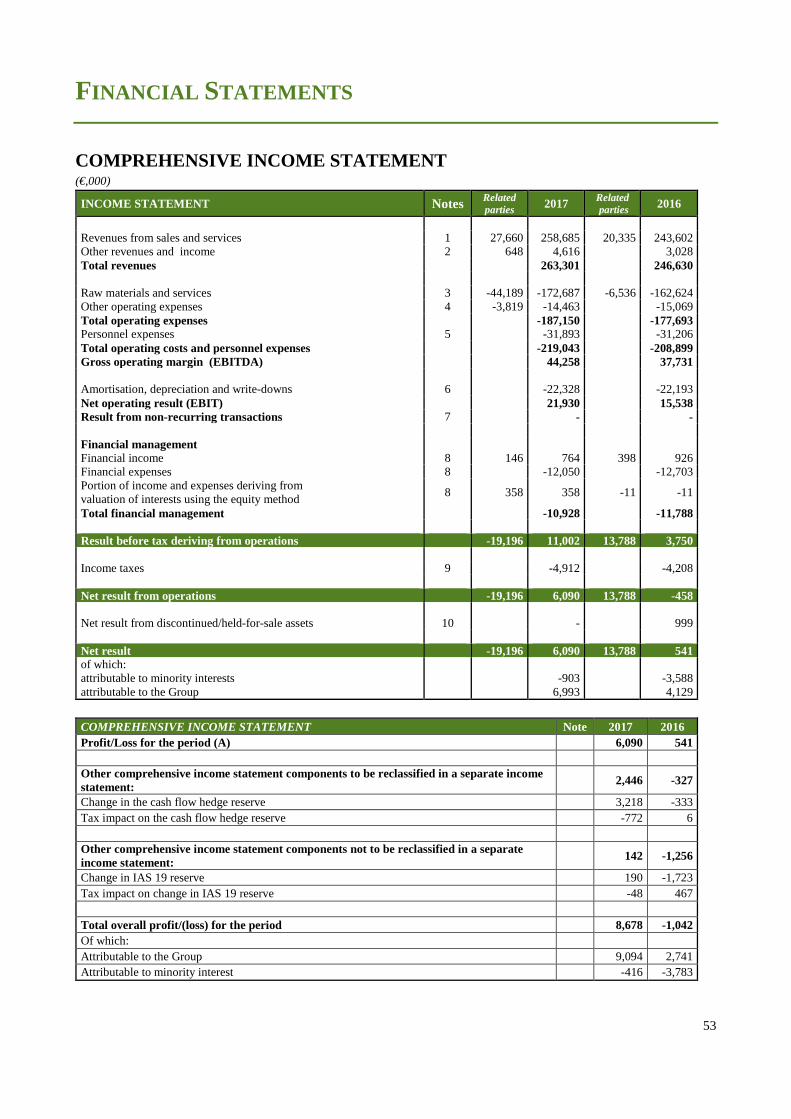

GROUP HIGHLIGHTS AND KEY FINANCIAL INDICATORS The tables below illustrate the main values and performance indicators of the LGH Group and quantitative data reflecting the business trend in the first six months of the year.

1. OPERATING FIGURES (€,000) 06/30/2017 % ON REVENUES 06/30/2016 % ON REVENUES

Net revenues 263,301 100.00% 246,630 100.00%

Gross operating margin - EBITDA 44,258 16.81% 37,731 15.30%

Operating result - EBIT 21,930 8.33% 15,538 6.30%

Income before taxes 11,002 4.18% 3,750 1.52%

Net result for the period 6,090 2.31% 541 0.22%

The LGH Group closed the 2017 first half year with a consolidated turnover of €263 million euro, up 16 million euro on the 2016 first half year (of which 6.8 million euro relating to the classification of the Sogir business unit, which is no longer held to sale), while the net result for the period shows an increase of 5.5 million euro. On September 9, 2015, LGH passed a resolution covering the launch of the procedure for the transfer of part of the urban hygiene business unit in the Lodi area to SOGIR, which had determined a reclassification of the values regarding assets and liabilities included in the sale and a disclosure of key economic figures in summary form. Given that more than 12 months have elapsed since the date on which the resolution was passed without any finalisation and since the conclusion of the transaction within the next 12 months seems to be unlikely, the business unit was included among ordinary assets and liabilities.

2. EQUITY DATA (€,000) 06/30/2017 12/31/2016 NIC (Net Invested Capital) 576,640 565,266 NFP (Net Financial Position) 358,370 354,932 GSE (Group Shareholders’ Equity) 200,308 178,401

MIE (Minority Interest’s Equity) 17,962 31,933

CSE (Consolidated Shareholders’ Equity) 218,270 210,334

GNR (Group Net Result) 6,993 - 11,260

MIR (Minority Interest’s Result) - 903 - 5,194

CNR (Consolidated Net Result) 6,090 - 16,454 Debt ratio = NFP/E 1,64 1,69

From a financial point of view, the Group’s net debt at June 30, 2017 increased by 3.4 million euro, from a financial position of 355 to 358 million euro. The debt ratio decreased from 1.69 to 1.64 due to the increase in shareholders’ equity.

7

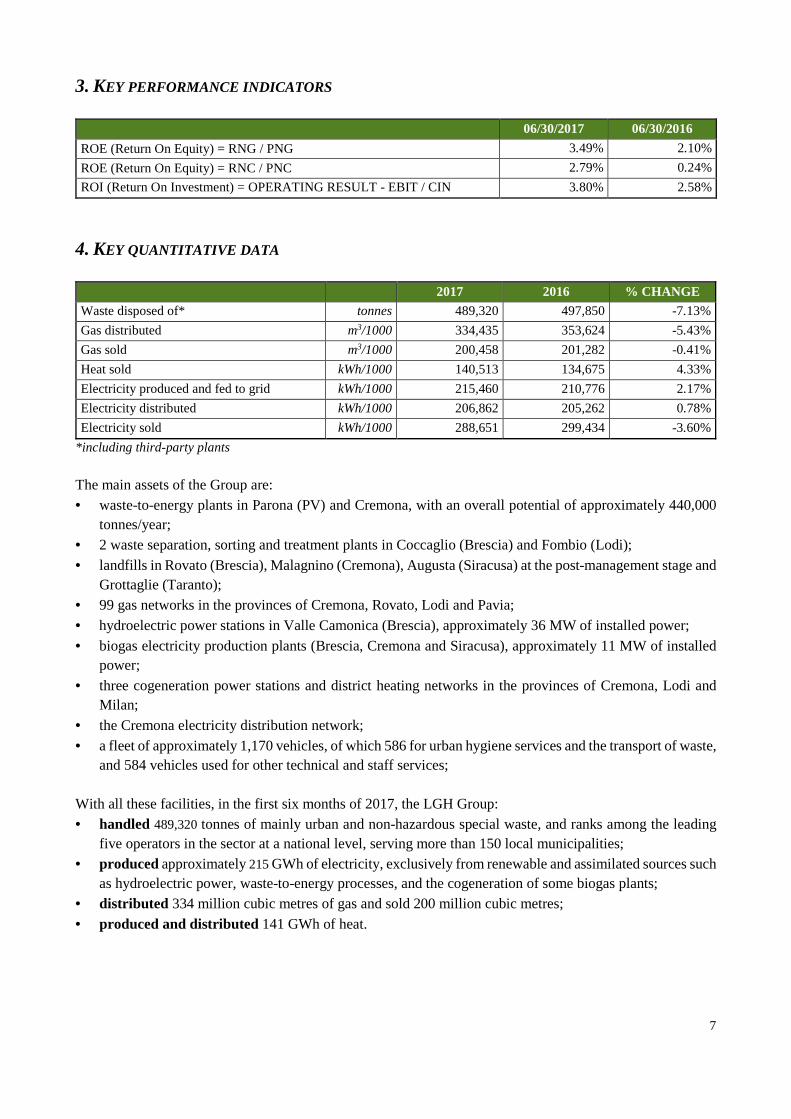

3. KEY PERFORMANCE INDICATORS 06/30/2017 06/30/2016

ROE (Return On Equity) = RNG / PNG 3.49% 2.10%

ROE (Return On Equity) = RNC / PNC 2.79% 0.24%

ROI (Return On Investment) = OPERATING RESULT - EBIT / CIN 3.80% 2.58%

4. KEY QUANTITATIVE DATA

2017 2016 % CHANGE

Waste disposed of* tonnes 489,320 497,850 -7.13%

Gas distributed m3/1000 334,435 353,624 -5.43%

Gas sold m3/1000 200,458 201,282 -0.41%

Heat sold kWh/1000 140,513 134,675 4.33%

Electricity produced and fed to grid kWh/1000 215,460 210,776 2.17%

Electricity distributed kWh/1000 206,862 205,262 0.78%

Electricity sold kWh/1000 288,651 299,434 -3.60%

*including third-party plants

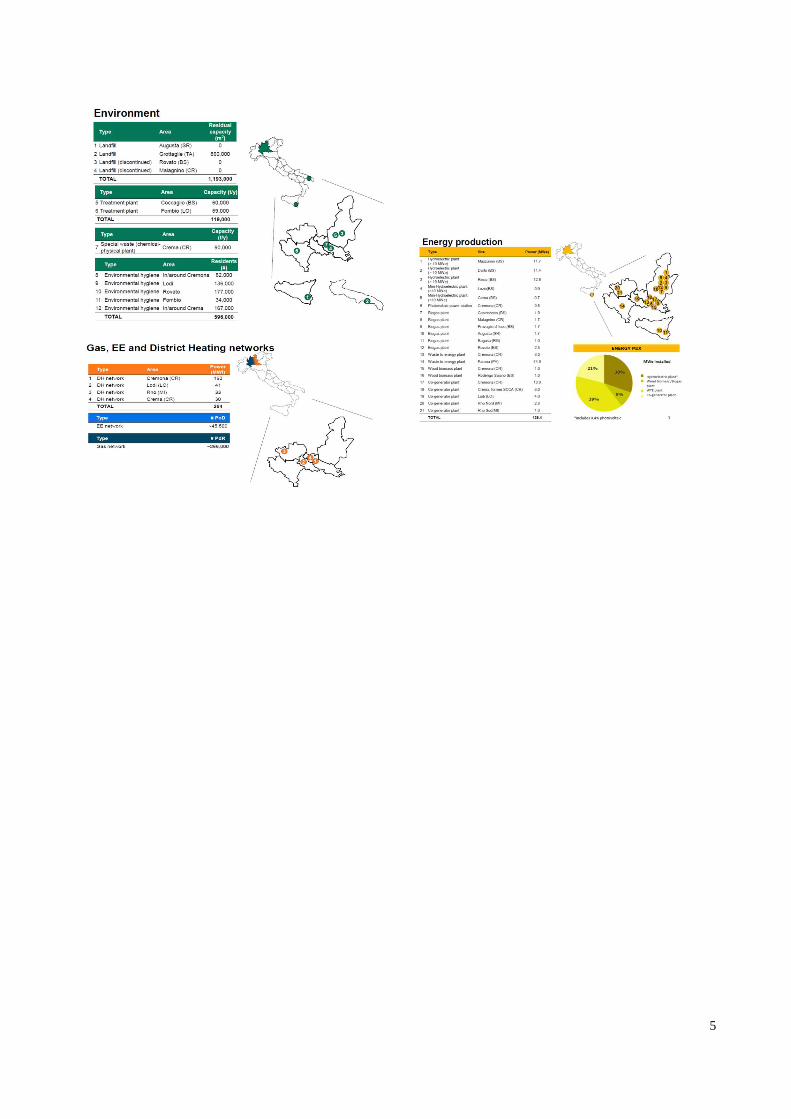

The main assets of the Group are: • waste-to-energy plants in Parona (PV) and Cremona, with an overall potential of approximately 440,000

tonnes/year; • 2 waste separation, sorting and treatment plants in Coccaglio (Brescia) and Fombio (Lodi); • landfills in Rovato (Brescia), Malagnino (Cremona), Augusta (Siracusa) at the post-management stage and

Grottaglie (Taranto); • 99 gas networks in the provinces of Cremona, Rovato, Lodi and Pavia; • hydroelectric power stations in Valle Camonica (Brescia), approximately 36 MW of installed power; • biogas electricity production plants (Brescia, Cremona and Siracusa), approximately 11 MW of installed

power; • three cogeneration power stations and district heating networks in the provinces of Cremona, Lodi and

Milan; • the Cremona electricity distribution network; • a fleet of approximately 1,170 vehicles, of which 586 for urban hygiene services and the transport of waste,

and 584 vehicles used for other technical and staff services; With all these facilities, in the first six months of 2017, the LGH Group: • handled 489,320 tonnes of mainly urban and non-hazardous special waste, and ranks among the leading

five operators in the sector at a national level, serving more than 150 local municipalities; • produced approximately 215 GWh of electricity, exclusively from renewable and assimilated sources such

as hydroelectric power, waste-to-energy processes, and the cogeneration of some biogas plants; • distributed 334 million cubic metres of gas and sold 200 million cubic metres; • produced and distributed 141 GWh of heat.

8

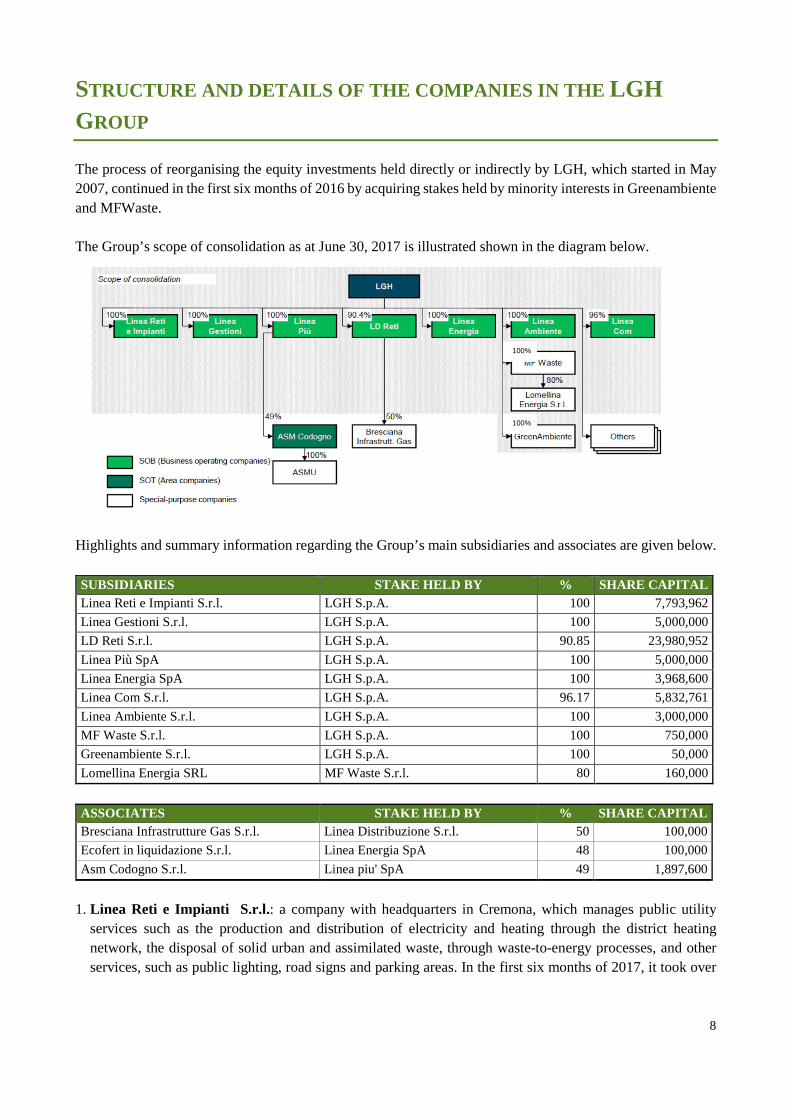

STRUCTURE AND DETAILS OF THE COMPANIES IN THE LGH

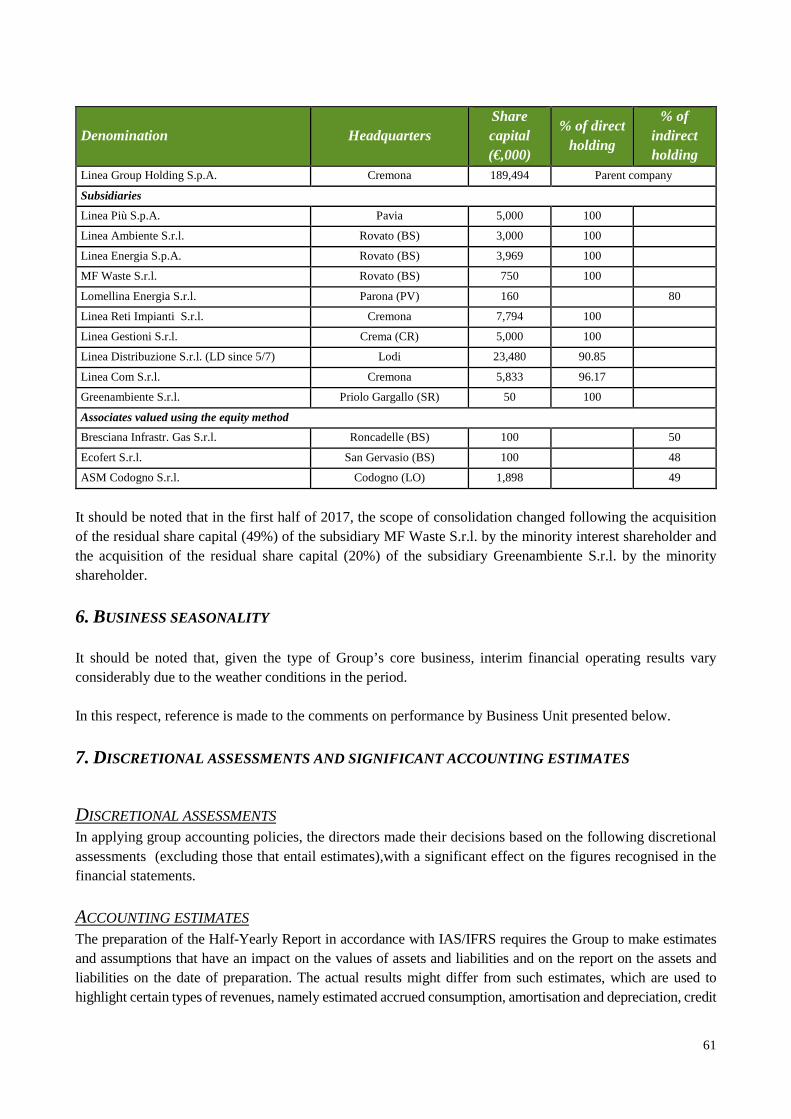

GROUP The process of reorganising the equity investments held directly or indirectly by LGH, which started in May 2007, continued in the first six months of 2016 by acquiring stakes held by minority interests in Greenambiente and MFWaste. The Group’s scope of consolidation as at June 30, 2017 is illustrated shown in the diagram below.

Highlights and summary information regarding the Group’s main subsidiaries and associates are given below. SUBSIDIARIES STAKE HELD BY % SHARE CAPITAL Linea Reti e Impianti S.r.l. LGH S.p.A. 100 7,793,962

Linea Gestioni S.r.l. LGH S.p.A. 100 5,000,000

LD Reti S.r.l. LGH S.p.A. 90.85 23,980,952

Linea Più SpA LGH S.p.A. 100 5,000,000

Linea Energia SpA LGH S.p.A. 100 3,968,600

Linea Com S.r.l. LGH S.p.A. 96.17 5,832,761

Linea Ambiente S.r.l. LGH S.p.A. 100 3,000,000

MF Waste S.r.l. LGH S.p.A. 100 750,000

Greenambiente S.r.l. LGH S.p.A. 100 50,000

Lomellina Energia SRL MF Waste S.r.l. 80 160,000

ASSOCIATES STAKE HELD BY % SHARE CAPITAL Bresciana Infrastrutture Gas S.r.l. Linea Distribuzione S.r.l. 50 100,000

Ecofert in liquidazione S.r.l. Linea Energia SpA 48 100,000

Asm Codogno S.r.l. Linea piu' SpA 49 1,897,600

1. Linea Reti e Impianti S.r.l.: a company with headquarters in Cremona, which manages public utility

services such as the production and distribution of electricity and heating through the district heating network, the disposal of solid urban and assimilated waste, through waste-to-energy processes, and other services, such as public lighting, road signs and parking areas. In the first six months of 2017, it took over

100%

100%

9

the biomass treatment business unit from Lodi Energia S.r.l. Soc. Agricola, a plant already connected to the Lodi district heating network, which belongs to the Group.

2. LD Reti S.r.l.: a company with headquarters in Lodi, which deals with natural gas distribution in the area covered by the Group for a total of 99 municipalities;

3. Linea Più S.p.A.: a company with headquarters in Pavia, which deals with the procurement, purchase and sale of raw materials and end customer management in the gas and electricity sectors;

4. Linea Energia S.p.A.: an engineering company with headquarters in Rovato, Brescia, which specialises in developing and performing activities relating to energy, from design to implementation and management of energy production plants; in 2016 it incorporated Franciacorta Rinnovabili S.r.l. and Rovato Energia Scarl;

5. Linea Com S.r.l.: a company with headquarters in Cremona, which supplies mobile and landline telephone and web services through broadband fibre optic and WiMAX networks in the cities of Cremona and Pavia and parts of the province. It also provides services and offers ICT technological support to LGH Group companies, information system service and management activities for the municipalities and deals with special projects for local authorities;

6. Linea Ambiente S.r.l.: a company with headquarters in Rovato, Brescia, which manages urban and special waste collection, transportation, treatment and disposal activities, including operations at landfills owned by the company. It carries out design activities to implement services and systems, and business management of the flows of waste generated and managed by all the companies belonging to the LGH Group;

7. Linea Gestioni S.r.l.: a company with headquarters in Crema (Cremona), which manages Environmental hygiene services for 120 municipalities in the city of Crema and other municipalities in the Franciacorta area and in the province of Lodi;

8. MF Waste S.r.l.: a company with headquarters in Rovato, Brescia, which holds 80% stake in Lomellina Energia S.r.l.;

9. Greenambiente S.r.l.: a company with headquarters in Priolo Gargallo, Siracusa, which owns and runs the waste disposal plant in Augusta, Siracusa;

10. Lomellina Energia S.r.l.: a company with headquarters in Parona, Pavia, which manages LGH Group's most important waste-to-energy plant;

11. Bresciana Infrastrutture Gas S.r.l.: a company with headquarters in Roncadelle, Brescia, which was set up in 2013 by Linea Distribuzione, which holds a 50% stake, for the management of the gas distribution network of the town of Palazzolo sull’Oglio;

12. Ecofert in liquidazione S.r.l.: an associate operating in the field of the recovery and the preparation for the recycling of urban and industrial solid waste and biomasses in San Gervasio Bresciano;

13. Asm Codogno S.r.l.: a multi-service company based in Codogno operating in the field of the environment and energy;

IAS/IFRS ACCOUNTING POLICIES

The parent company has adopted the International Financial Reporting Standards (IFRS) in drawing up its financial statements since December 31, 2009, in compliance with the procedure under art. 6 of EC Regulation no. 1606/2002 of the European Parliament and Council of July 19, 2002 on the application of the IFRS.

Since 2014, the financial statements of most of the subsidiaries and the parent company have been prepared in accordance with international accounting policies.

Further details are provided in the explanatory notes.

10

II. DIRECTORS’ BUSINESS REPORT

11

SIGNIFICANT EVENTS OCCURRING DURING THE 1ST HALF OF

2017 The following significant events occurred in the first six months of 2017:

- the takeover of the biomass treatment business unit from Lodi Energia S.r.l. Soc. Agricola, a plant already connected to the Lodi district heating network, which belongs to the Group.

- the acquisition of 49% equity stake in MF Waste S.r.l., now 100% owned;

- the acquisition of 20% equity stake in Greenambiente S.r.l., now 100% owned;

- completion of Lomellina Energia’s financing project.

SUMMARY OF GROUP’S FINANCIAL PERFORMANCE , EQUITY AND

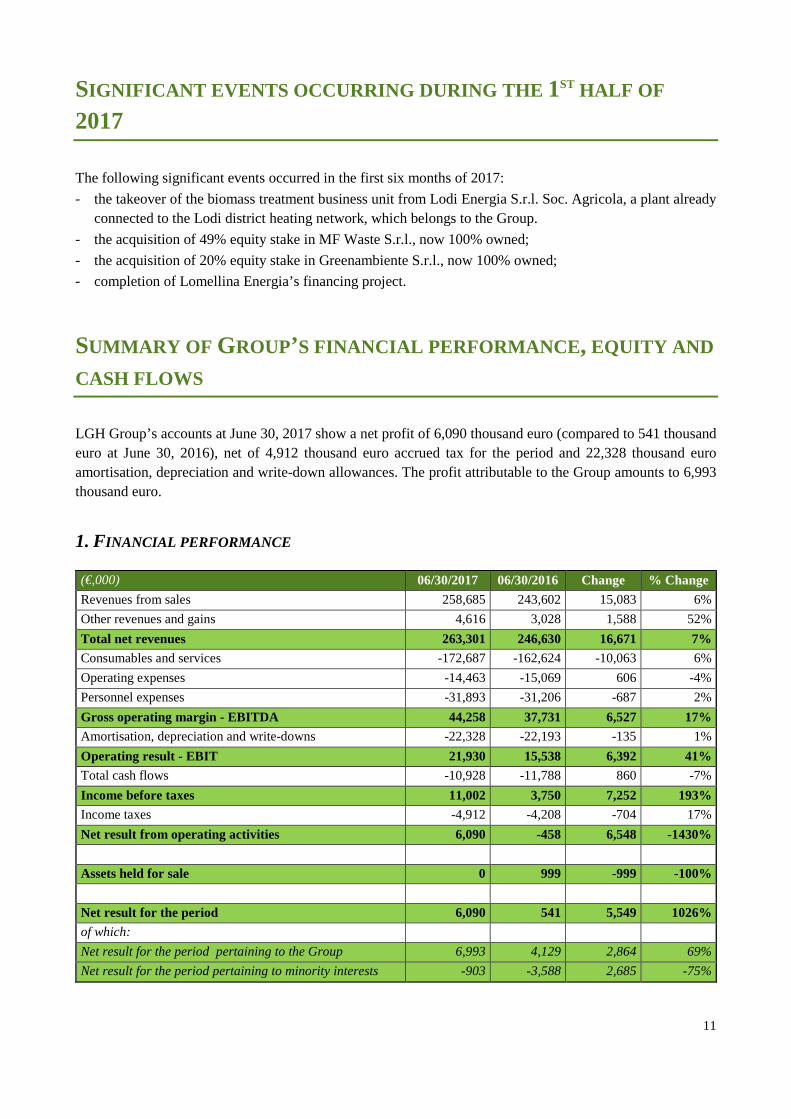

CASH FLOWS LGH Group’s accounts at June 30, 2017 show a net profit of 6,090 thousand euro (compared to 541 thousand euro at June 30, 2016), net of 4,912 thousand euro accrued tax for the period and 22,328 thousand euro amortisation, depreciation and write-down allowances. The profit attributable to the Group amounts to 6,993 thousand euro.

1. FINANCIAL PERFORMANCE

(€,000) 06/30/2017 06/30/2016 Change % Change

Revenues from sales 258,685 243,602 15,083 6%

Other revenues and gains 4,616 3,028 1,588 52%

Total net revenues 263,301 246,630 16,671 7%

Consumables and services -172,687 -162,624 -10,063 6%

Operating expenses -14,463 -15,069 606 -4%

Personnel expenses -31,893 -31,206 -687 2%

Gross operating margin - EBITDA 44,258 37,731 6,527 17%

Amortisation, depreciation and write-downs -22,328 -22,193 -135 1%

Operating result - EBIT 21,930 15,538 6,392 41%

Total cash flows -10,928 -11,788 860 -7%

Income before taxes 11,002 3,750 7,252 193%

Income taxes -4,912 -4,208 -704 17%

Net result from operating activities 6,090 -458 6,548 -1430%

Assets held for sale 0 999 -999 -100%

Net result for the period 6,090 541 5,549 1026%

of which:

Net result for the period pertaining to the Group 6,993 4,129 2,864 69%

Net result for the period pertaining to minority interests -903 -3,588 2,685 -75%

12

Net revenues amounted to 263.3 million euro, up 7% on the same period in 2016. Costs for raw materials, supplies, consumables, goods and services totalled 172.7 million euro, up 6% on the same period in 2016. Personnel cost came to 31.9 million euro, up 2% on the same period in 2016. Amortisation, depreciation and write-downs came to 22.3 million euro, up 1% on the same period in 2016. In the first of half of 2017, cash flows came to -10.9 million euro, an improvement of 7% on the same period in 2016. Income before tax came to 11 million euro, up 193% on the same period in 2016. Consolidated taxes amounted to -4,9 million euro, up 17% on the same period in 2016. Net result for the period came to 6 million euro, up 5.5 million euro on the 2016 result for the period. ELECTRICITY AND GAS NETWORKS

The Electricity and Gas Networks Business Unit handles operations regarding the technical and operational management of the electricity distribution network in the municipality of Cremona and the natural gas distribution networks; it also handles the management of public lighting (only two months in 2017), traffic control systems and third-party heating systems (heating management). (€,000)

QUANTITATIVE DATA 2017 2016 CHANGE % CHANGE

Electricity distributed (GWh) 206,9 205,3 +1.6 +0.8%

Gas distributed (Mcm) 334,4 353,6 -19.1 -5.4%

Electricity output in 2017 amounted to 207 GWh (net of 7.4 GWh transited in the interconnection points in the network of the Municipality of Cremona but pertaining to Enel), which is basically in line with the previous year. Gas output declined (-5.4%) due to a heating season characterised by mild temperatures. (€,000)

GAS DISTRIBUTION 2017 2016 % CHANGE

Revenues 30,635 19,223 +59.3%

Costs 23,295 11,997 +94.2%

GROSS OPERATING MARGIN - EBITDA 7,340 7,237 +1.4%

Amortisation, depreciation and allowances 3,943 3,935 +0.2%

OPERATING RESULT - EBIT 3,397 3,301 +2.9%

Regardless of volumes transited, revenues increased by 11.4 million euro, mainly due to the different presentation of TEE trading in the financial statements: in 2017, TEE operations are recorded in the income statement according to the cash principle (which also generates cost increases), while in 2016 only the margin was recorded when rights and obligations matured. Total revenue pertaining to the period rose slightly by 0.4 million euro due to the effect of increased investments recognized in tariffs (+0,7 million), with respect to a lesser contribution in “recovery in productivity”. Gross operating margin (EBITDA) has a positive deviation of +0.1 million euro, mainly due to:

13

• A decrease (-1.1 million euro) in margin resulting from the trading of energy efficiency titles (TEE) generated by the rise in market prices, as a result of late trading of purchase contracts and the resulting partial coverage by the Energy Service Provider (GSE).

• Increased total revenues due to the update of tariffs of the regulatory authority for electricity, gas and water (AEEGSI) and increased incentives (0.4 million euro) for AEEGSI Safety Recovery and reduced overhead expenses (0.6 million euro);

• Less contingent liabilities for lease payable to municipalities for previous years (+0.2 million euro). (€,000)

Despite a slight decrease in revenues, gross operating margin (EBITDA) increased by 0.8 million euro, thanks to 0.6 million less overhead expenses (ordinary maintenance, personnel and general expenses), in addition to the increase in revenues resulting “distribution constraints” for 0.2 million euro (recognition in tariffs of previous years’ investments). DISTRICT HEATING NETWORK

The District Heating Networks Business Unit deals with the management of district heating networks and the associated co-generation plants.

A summary of the main quantitative and economic data regarding this Business Unit is given below. DISTRICT HEATING 2017 2016 CHANGE % CHANGE SOURCES (GWh) Heat produced by co-generation plants: 118.03 111.25 6.78 6.10% Heat produced by CHP plants and boilers, Cremona 43.87 42.22 1.65 3.90% Heat produced by CHP plants and boilers, Lodi 35.29 31.64 3.65 11.55% Heat produced by CHP plants and boilers, Rho 19.67 18.87 0.80 4.25% Heat produced by CHP plants and boilers, Crema 19.20 18.52 0.68 3.67% Heat purchased: 46.31 51.15 -4.83 -9.45% Other third-party owned plants 0.00 3.55 -3.55 100% Heat purchased by the Environment BU 46.31 47.60 -1.29 -2.70%

TOTAL SOURCES 164.34 162.39 1.95 1.20% USES Heat sold – Total volumes (GWh) 140.5 134.7 5.8 4.33% Network losses (GWh) 23.8 28.0 -4.2 -14.96%

TOTAL USES 164.34 162.39 1.9 1.20%

Electricity from Co-generation – production (GWh) 46.27 46.62 -0.35 -0.75%

ELECTRICITY DISTRIBUTION 2017 2016 % CHANGE

Revenues 7,387 7,548 -2.1%

Costs 4,754 5,757 -17.4%

GROSS OPERATING MARGIN - EBITDA 2,633 1,790 +47.1%

Amortisation, depreciation and allowances 1,489 1,447 +2.9%

OPERATING RESULT - EBIT 1,144 343 +233.3%

14

The sales of heat to end users in 2017 increased by 4.33%, compared to the previous year. This result is attributable to connection of new customers in the municipality of Lodi (+4.2 GWh), following the planned enlargement of the network. The heating effect is basically null in both periods. (€,000)

DISTRICT HEATING 2017 2016 % CHANGE Revenues 16,104 13,412 +20.1%

Costs 11,325 10,221 +10.8%

GROSS OPERATING MARGIN - EBITDA 4,778 3,191 +49.8% Amortisation, depreciation and allowances 1,760 1,794 -1.9%

OPERATING RESULT - EBIT 3,018 1,396 116.2%

Revenues in 2017 came to 16.1 million euro, with a 20% increase attributable to:

• +1.1 million euro increase in heat distribution turnover and the sale of produced electricity and steam; • +0.5 million euro due to non-recurring items relating to the acquisition of «SCCA» and the Lodi

biomass treatment plant; • +1.1 million euro revenues resulting from auxiliary services relating to the management of heat and

the Lodi biomass treatment plant. Gross operating margin (EBITDA) came to 4.8 million euro, with an increase of 1.6 million euro compared to the 2016 figure (+50%); in addition to the above non-recurring positive items (+0.5 million euro), the increase in margin is mainly attributable to increased quantities delivered and the positive effect of prices (+0.8 million euro), improved revenues from the transfer of TEEs and heat management and the increased margin of the Lodi biomass treatment plant (scope of consolidation difference). COMMERCIAL

The Commercial Business Unit comprises the retail sale of electricity and natural gas to customers of the deregulated market and those served in regulated markets.

The table below provides a summary of the main quantitative and economic figures. COMMERCIAL 2017 2016 CHANGE % CHANGE

Electricity sold Total EE sold in the deregulated market (GWh) 282.04 289.50 -7.46 -2.58% Total EE sold in the regulated market (GWh) 28,27 29.02 -0.76 -2.61%

Total electricity sold (GWh) 310.30 318.52 -8.22 -2.58% EE sold - No. of meters 77,896 68,574 9,322 13.59%

Gas sold Gas sold (Mmc) – External free market 117.63 115.96 1.67 1.44% Gas sold (Mmc) – Regulated market 83,86 88.15 -4.29 -4.87%

Total gas sold (Mmc) 201.49 204.11 -2.62 -1.28% Gas sold – No. of customer meters 216,415 220,915 -4,500 -2.04%

Quantities sold are shown net of losses The first half of 2017 shows a slight decrease in the sale volumes of both gas (-1.3%) and electricity (-2.6%).

15

The decrease in the gas sector is attributable to the loss of industrial corporate customers, which was only partly offset by a strengthening of supplies for the production of heat in the district heating sector and the indirect sales channel. The reduction of about 8GWh in electricity volumes compared to the same period in 2016 is attributable to the increasing competitive pressure, especially in the corporate segment, which recorded a decrease in the number of customers due to negative outcome of bids for tender and contract renewals; this decline was partly offset, however, by increased supplies for the household sector. (€,000)

COMMERCIAL 2017 2016 % CHANGE

Revenues 139,381 138,270 +0.8%

Costs 130,072 130,851 -0.6%

GROSS OPERATING MARGIN - EBITDA 9,309 7,420 +25.5%

Amortisation, depreciation and allowances 1,703 1,220 -39.6%

OPERATING RESULT - EBIT 7,606 6,200 +22.7%

In order to provide a homogeneous period-on-period comparison, the figures for the year 2016 were reinstated according to the new pricing logics adopted in the trading segment, which generates a negative effect on the margin of the gas regulated market. Overall, gross operating margin (EBITDA) of the commercial Business Unit amounted to 9.3 million euro, with a 1.9 million euro increase (+25.5%), which is the result of the following effects:

• +2.4 million euro di gross margin, due to the positive effect of the price upward trend (quantities virtually equal);

• -0.6 million euro due to increased operating costs, of which 0.4 million euro relating to commissions paid to sales agents following the strengthening of the indirect sales channel;

• a slight increase in the electricity market (+0.1 million euro), characterised by a positive price upward trend, eroded by a reduction in volumes sold.

Amortisation, depreciation and allowances increased by 0.5 million euro, mainly due to higher amounts allocated to the provision for doubtful debts (+0.6 million euro). ELECTRICITY GENERATION AND TRADING The Generation and Trading Business Unit encompasses the management of hydroelectric power plants, the Cremona photovoltaic system and the trading of energy commodities

The table below provides a summary of the main quantitative and economic figures. ELECTRICITY GENERATION AND TRADING 2017 2016 CHANGE % CHANGE SOURCES (GWh) Net output 61.19 61.08 0.11 0.18% EE from hydroelectric power plants – output (GWh) 60.90 60.81 0.09 0.14% EE from photovoltaic systems – output (GWh) 0.29 0.27 0.02 7.26% Purchases 1,217.57 964.46 253.12 26.24% EE purchased on the stock exchange 30.00 27.16 2.84 10.45% EE purchased from third-party wholesalers 251.33 287.51 -36.18 -12.58% EE purchased from speculative trading portfolio 936.24 649.79 286.46 44.08%

TOTAL SOURCES 1,278.76 1.025,53 253.23 24.69%

16

ELECTRICITY GENERATION AND TRADING 2017 2016 CHANGE % CHANGE USES (GWh) EE intercompany sales (incl. network losses) 281.33 298.55 -17.22 -5.77% EE sold to other wholesalers (third-party) 61.19 58.44 2.75 4.70% EE sold on the stock exchange 0.00 18.76 -18.76 -100.00% EE sold to speculative trading portfolio 936.24 649.79 286.46 44.08%

TOTAL USES 1,278.76 1,025.53 253.23 24.69% The figures shown are inclusive of losses

During the reporting period, the production of electricity amounted to 61 GWh, to which purchases must be added for 1,217 GWh, giving an overall increase in availability of 26%. Production is in line with the previous year: the decrease in the amount of electricity generated by hydropower stations as a result of unfavourable weather conditions (less rainfalls) is offset by the additional contribution of the Mazzunno plant, which was acquired at the start of 2017. GAS TRADING 2017 2016 CHANGE % CHANGE SOURCES (Mcm) Gas purchased – Procurement 219.38 226.82 -7.45 -3.28% Gas purchased – Withdrawals from stocks 0.15 3.42 -3.27 -95.54% Gas purchased – Self-cons./GNC (gas not cont.) -0.33 -0.25 -0.07 28.28% Gas purchased – Speculative Trading Portfolio 24.81 18.62 6.19 33.27%

TOTAL SOURCES 244.01 248.60 -4.59 -1.85% USES(Mcm) Gas sold – Commercial BU 206.01 205.99 0.03 0.01% Gas sold on the stock exchange 0.00 0.00% Gas sold – Wholesalers 13.19 24.00 -10.81 -45.03% Gas sold - Speculative Trading Portfolio 24.81 18.62 6.19 33.27%

TOTAL USES 244.01 248.60 -4.59 -1.85% The quantities shown relate to standard cubic metres reported in the LHV of 38,100 MJ on re-delivery.

At the end of the first six months of 2017, the gas volumes purchased accounted for 244 Mcm, on decline (approx. -5 Mcm), compared to the 2016 figure, due to both less outsourced gas (-3%) and the considerable reduction in the use of stored gas; conversely, gas trading portfolio purchases increased (+6 Mcm), generated by an increase in exchange activities on national and international platforms. Gas sold to the Commercial Business Unit remained virtually unchanged, while sales on wholesale markets shows a significant increase in the quantities delivered (-11 Mcm). (€,000)

GENERATION AND TRADING 2017 2016 % CHANGE Revenues 83,468 89,861 -7.1%

Costs 79,013 81,692 -3.3%

GROSS OPERATING MARGIN - EBITDA 4,455 8,170 -45.6% Amortisation, depreciation and allowances -1,328 2,050 +164.8%

OPERATING RESULT - EBIT 5,784 6,120 -5.5%

17

In order to uniformly represent the comparison between the two periods, it was necessary to restate 2016 figures with the following adjustments (the first two with an impact on gross operating margin – EBITDA):

• the adoption of a different pricing system in the relations with the commercial BU; • a reclassification of active and passive items relating to the recognition of fair value on energy and gas

derivatives from financial management to sales revenues and purchase of materials; • the adoption of the revenue netting system and speculative portfolio costs.

Gross operating margin (EBITDA) came to 4.4 million euro, decreasing by 3.7 million euro compared to 2016 (-45.5%). The energy trading sector recorded an overall negative result of -4.4 million euro, due to:

• -5 million euro generated by a 2017 electricity market scenario that was radically unfavourable with respect to portfolio positions (due to extraordinary maintenance of the French nuclear park, hydroelectric power production at the lowest level ever recorded over the last 10 years and the rise in coal prices), together with the cessation of operations on strategic imbalance;

• -0.7 million euro margin of gas trading portfolio due to reduced transfers to wholesalers and increase in materials purchase costs;

• +1,3 million euro from differences in the derivatives market value, especially on electricity trading. The hydroelectric sector was characterised by an increase of +0.5 million euro in energy transfer revenues, compared to the previous year, due mainly to the uptrend of transfer unit prices, jointly with an increase in the sale of green certificates for +0.1 million euro. The item “Amortisation, depreciation and allowances” declined considerably by 3.4 million euro, due to:

• -2,6 million euro release of the provision in 2016 to cover the risk of sanctions relating to trading operations on strategic electricity imbalance;

• -1 million euro allowances to the provision for sundry risks recorded in 2016 (photovoltaic and electricity trading);

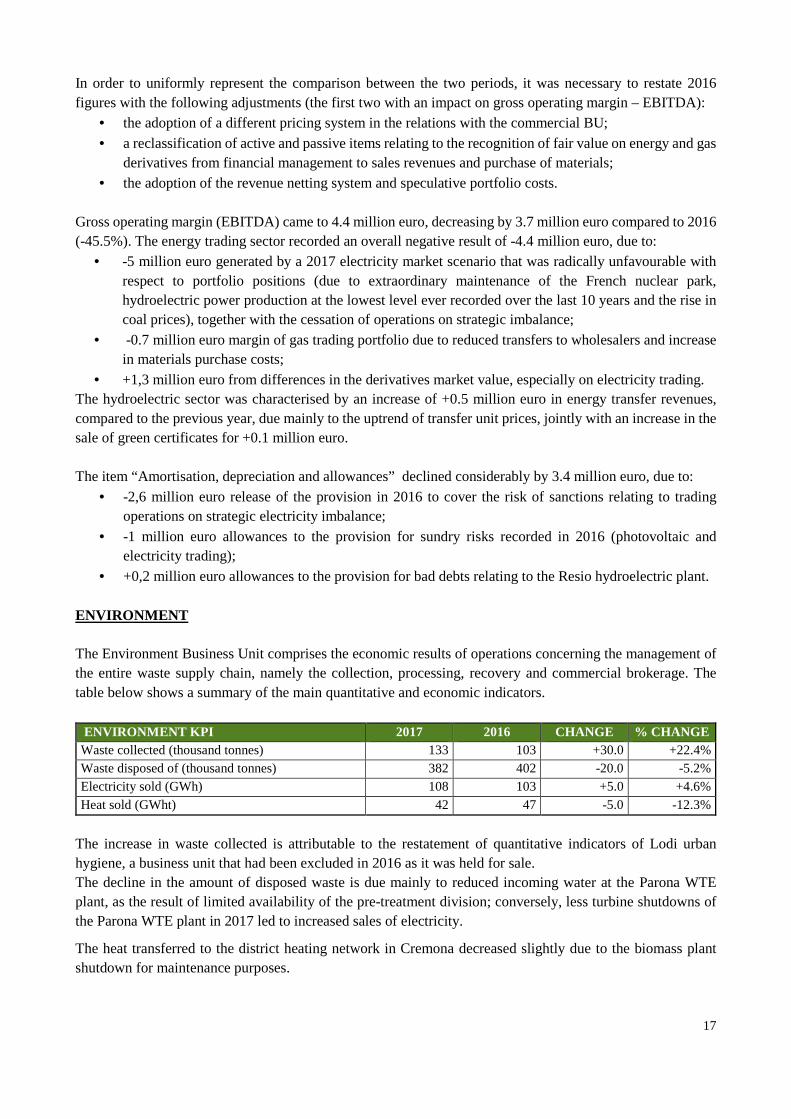

• +0,2 million euro allowances to the provision for bad debts relating to the Resio hydroelectric plant. ENVIRONMENT The Environment Business Unit comprises the economic results of operations concerning the management of the entire waste supply chain, namely the collection, processing, recovery and commercial brokerage. The table below shows a summary of the main quantitative and economic indicators. ENVIRONMENT KPI 2017 2016 CHANGE % CHANGE Waste collected (thousand tonnes) 133 103 +30.0 +22.4% Waste disposed of (thousand tonnes) 382 402 -20.0 -5.2% Electricity sold (GWh) 108 103 +5.0 +4.6% Heat sold (GWht) 42 47 -5.0 -12.3%

The increase in waste collected is attributable to the restatement of quantitative indicators of Lodi urban hygiene, a business unit that had been excluded in 2016 as it was held for sale. The decline in the amount of disposed waste is due mainly to reduced incoming water at the Parona WTE plant, as the result of limited availability of the pre-treatment division; conversely, less turbine shutdowns of the Parona WTE plant in 2017 led to increased sales of electricity.

The heat transferred to the district heating network in Cremona decreased slightly due to the biomass plant shutdown for maintenance purposes.

18

(€,000)

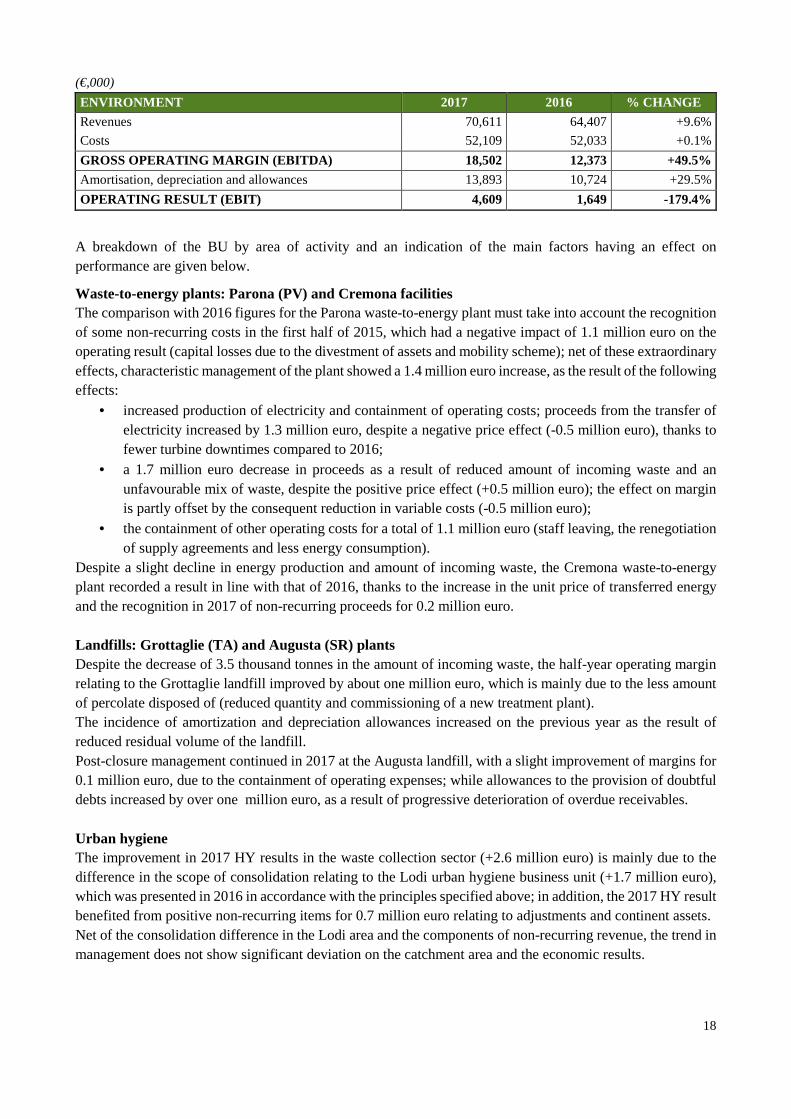

ENVIRONMENT 2017 2016 % CHANGE

Revenues 70,611 64,407 +9.6%

Costs 52,109 52,033 +0.1%

GROSS OPERATING MARGIN (EBITDA) 18,502 12,373 +49.5%

Amortisation, depreciation and allowances 13,893 10,724 +29.5%

OPERATING RESULT (EBIT) 4,609 1,649 -179.4%

A breakdown of the BU by area of activity and an indication of the main factors having an effect on performance are given below.

Waste-to-energy plants: Parona (PV) and Cremona facilities The comparison with 2016 figures for the Parona waste-to-energy plant must take into account the recognition of some non-recurring costs in the first half of 2015, which had a negative impact of 1.1 million euro on the operating result (capital losses due to the divestment of assets and mobility scheme); net of these extraordinary effects, characteristic management of the plant showed a 1.4 million euro increase, as the result of the following effects:

• increased production of electricity and containment of operating costs; proceeds from the transfer of electricity increased by 1.3 million euro, despite a negative price effect (-0.5 million euro), thanks to fewer turbine downtimes compared to 2016;

• a 1.7 million euro decrease in proceeds as a result of reduced amount of incoming waste and an unfavourable mix of waste, despite the positive price effect (+0.5 million euro); the effect on margin is partly offset by the consequent reduction in variable costs (-0.5 million euro);

• the containment of other operating costs for a total of 1.1 million euro (staff leaving, the renegotiation of supply agreements and less energy consumption).

Despite a slight decline in energy production and amount of incoming waste, the Cremona waste-to-energy plant recorded a result in line with that of 2016, thanks to the increase in the unit price of transferred energy and the recognition in 2017 of non-recurring proceeds for 0.2 million euro. Landfills: Grottaglie (TA) and Augusta (SR) plants Despite the decrease of 3.5 thousand tonnes in the amount of incoming waste, the half-year operating margin relating to the Grottaglie landfill improved by about one million euro, which is mainly due to the less amount of percolate disposed of (reduced quantity and commissioning of a new treatment plant). The incidence of amortization and depreciation allowances increased on the previous year as the result of reduced residual volume of the landfill. Post-closure management continued in 2017 at the Augusta landfill, with a slight improvement of margins for 0.1 million euro, due to the containment of operating expenses; while allowances to the provision of doubtful debts increased by over one million euro, as a result of progressive deterioration of overdue receivables. Urban hygiene The improvement in 2017 HY results in the waste collection sector (+2.6 million euro) is mainly due to the difference in the scope of consolidation relating to the Lodi urban hygiene business unit (+1.7 million euro), which was presented in 2016 in accordance with the principles specified above; in addition, the 2017 HY result benefited from positive non-recurring items for 0.7 million euro relating to adjustments and continent assets. Net of the consolidation difference in the Lodi area and the components of non-recurring revenue, the trend in management does not show significant deviation on the catchment area and the economic results.

19

Waste treatment and recycling plants Among the Group’s other waste treatment plants, the results of the biomass plants located in Fombio and Coccaglio improved slightly by about 0.4 million euro, thanks to a larger volume of material processed and reduced operating expenses.

CORPORATE AND ICT The Corporate and ICT Business Unit comprises the operating results for ICT operations and the corporate services supplied by Linea Group Holding for the entire Group. (€,000)

CORPORATE AND ICT 2017 2016 % CHANGE Revenues 14,705 14,649 +0.4% Costs 17,465 17,098 +2.1%

GROSS OPERATING MARGIN (EBITDA) -2,760 -2,450 +12.7% Amortisation, depreciation and allowances 867 1,022 -15.2%

OPERATING RESULT (EBIT) -3,627 -3,472 +4.5%

The increase in costs is mainly attributable to the increase in personnel expenses in the corporate segment, following the centralisation of some operations at the parent company and staff secondment from A2A. The decrease in amortisation, depreciation and allowances is due to the recognition in 2016 of an impairment loss relating to 0.2 million euro equity interest in Steam.

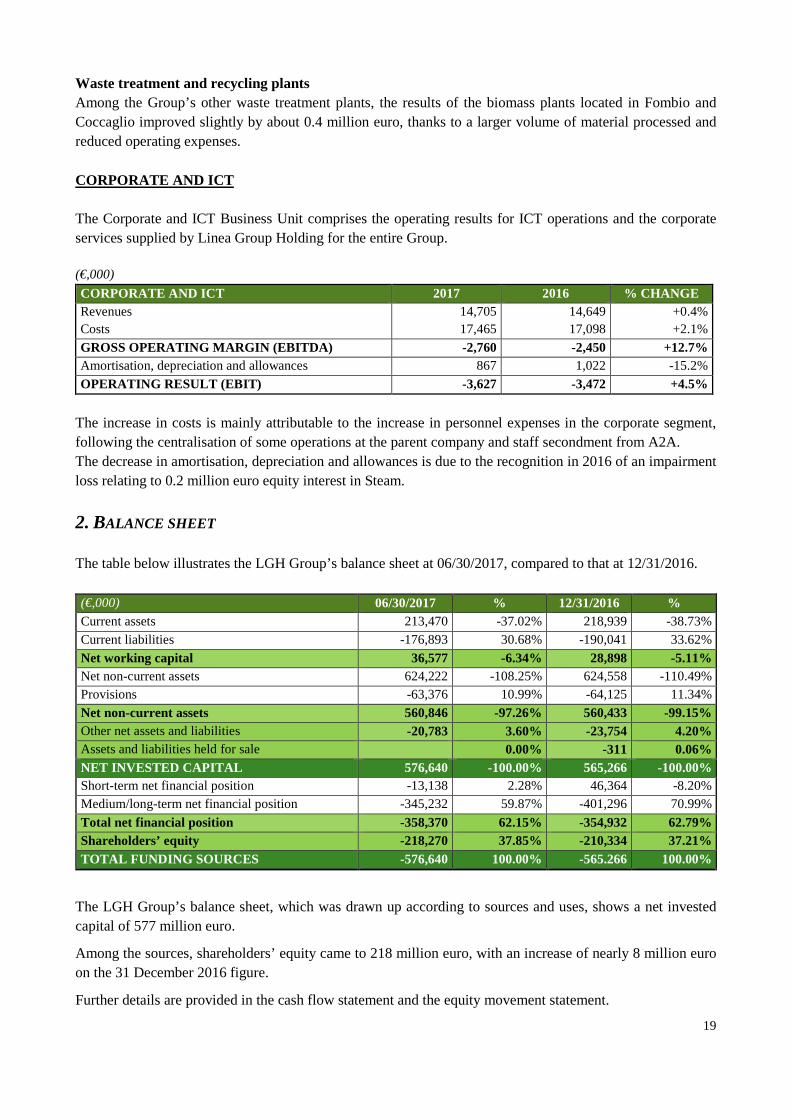

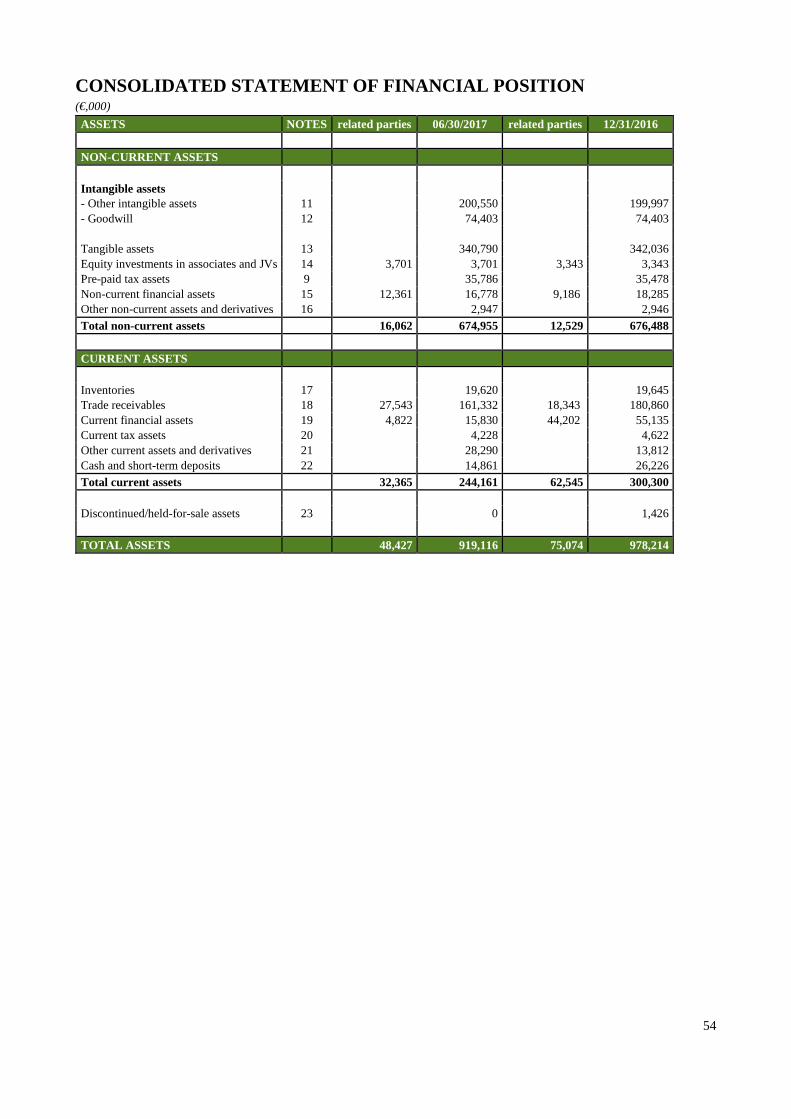

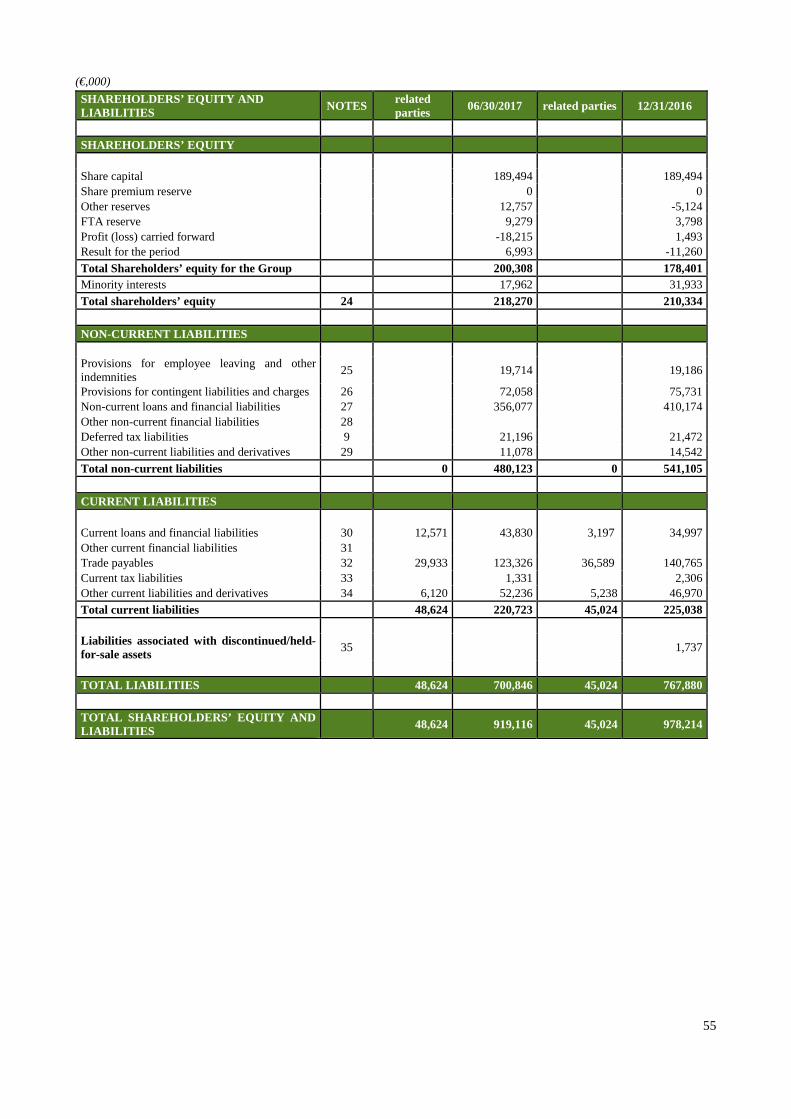

2. BALANCE SHEET The table below illustrates the LGH Group’s balance sheet at 06/30/2017, compared to that at 12/31/2016. (€,000) 06/30/2017 % 12/31/2016 % Current assets 213,470 -37.02% 218,939 -38.73% Current liabilities -176,893 30.68% -190,041 33.62%

Net working capital 36,577 -6.34% 28,898 -5.11% Net non-current assets 624,222 -108.25% 624,558 -110.49% Provisions -63,376 10.99% -64,125 11.34%

Net non-current assets 560,846 -97.26% 560,433 -99.15% Other net assets and liabilities -20,783 3.60% -23,754 4.20% Assets and liabilities held for sale 0.00% -311 0.06% NET INVESTED CAPITAL 576,640 -100.00% 565,266 -100.00% Short-term net financial position -13,138 2.28% 46,364 -8.20% Medium/long-term net financial position -345,232 59.87% -401,296 70.99%

Total net financial position -358,370 62.15% -354,932 62.79% Shareholders’ equity -218,270 37.85% -210,334 37.21% TOTAL FUNDING SOURCES -576,640 100.00% -565.266 100.00%

The LGH Group’s balance sheet, which was drawn up according to sources and uses, shows a net invested capital of 577 million euro.

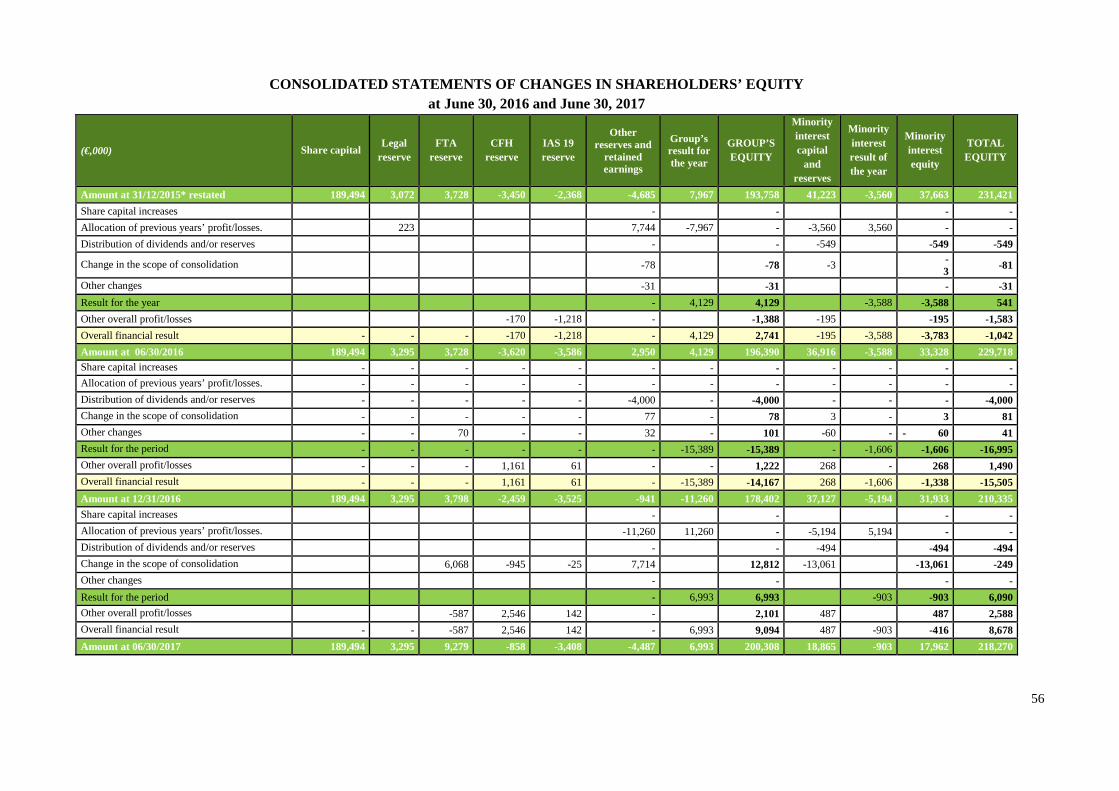

Among the sources, shareholders’ equity came to 218 million euro, with an increase of nearly 8 million euro on the 31 December 2016 figure.

Further details are provided in the cash flow statement and the equity movement statement.

20

REGULATORY FRAMEWORK ELECTRICITY GENERATION AND TRADING BUSINESS UNIT Remuneration of electricity generating capacity The production capacity-based remuneration mechanism applicable in Italy is so-called “capacity payment” scheme, introduced in 2003 by Legislative Decree no. 379, as transitional administered system, whose purpose is to ensure the appropriateness of the electricity system in the days identified by Terna and defined as critical, when the difference between supply and demand could be at the lowest levels. Effective in 2004 onwards, the Regulatory Authority has envisaged the preliminary calculation of amounts collected from electricity bills and delivered via two payments (called CAP1 and S) to facilities authorized to dispatching services. Legislative Decree no. 379 set out that, at full generating capacity, the remuneration of capacity would rest upon a market mechanism (capacity market), later defined by Authority Resolution ARG/elt 98/11. The final scheme envisages trading in the form of auctions, where awarded operators acquire the right to receive a premium (in €/MW/year) and the obligation to offer the awarded capacity on energy (MGP) and Service (MSD) markets, by returning the difference between the market and the strike price (in €/MWh) to Terna, if positive. Technically speaking, this is a “one-way contract for differences”. Initially, the capacity market envisaged three-yearly auctions with a four-year timeline planning. By Resolution 95/2015/I/eel, the Authority proposed the Ministry for Economic Development (MiSE) to reduce to one year the period elapsing between auctioning and delivery, by introducing new yearly contracts (so-called first-adoption stage). In April 2015, the European Commission launched a survey to ascertain whether the capacity-based remuneration mechanisms are compatible with the State aid rules and ensure adequate security in electricity procurement without distorting competition in the European single market. In August 2015, the Italian government informally informed the Directorate General for Competition of the capacity-based remuneration mechanism under Resolution ARG/elt 98/11. Over these two years, numerous contacts have been established between the Directorate General from Competition and Directorate General for Energy with the Ministry for Economic Development, the Regulatory Authority and Terna. In November 2016, the Commission terminated the survey and acknowledged that the remuneration of the availability in energy-only markets is required to give the system signs of long-term price for investments in new electricity generating capacity. Between October 2016 and February 2017: � Terna published 3 consultation documents (DCO) on a detailed discipline, whose main elements are:

� first adoption: access by production units of a capacity of less than 10MVA (provided they do not receive incentives from the Energy Service Provider (GSE) or they reject said incentives) to renewable generation and to application activated on Ancillary Services Market (MSD);

� steady-rate operation: in addition to the rules specified for first adoption, direct access to foreign resources, duration of the annual (not three yearly) contract, limited appreciation of the resource flexibility characteristics for access to the remuneration mechanism (at present only one selection priority of resource flexibility is provided when several bids are quoted against the marginal price auction);

� change to Terna demand curve, which is simplified and made compliant with European standards. The new curve is particularly influenced by government choices in terms of both maximum acceptable expenditure and safety level (function of the Loss of Load Expectation (LOLE) parameter, which

21

represents the maximum post-load acceptable at country level. This parameter is established by the Ministry for Economic Development);

� The Authority publishes 1 DCO on the obligations for plants under contract, where the offer of the capacity on the Day-Ahead Market (MGP) is more strongly incentivized at values less or equal to the strike price and the maximum premium ceiling (cap) is 75,000 €/MW/year.

Operators have called for solutions intended to increase both the premium cap and the strike price (acting implicitly as a price cap) and have highlighted the lack of appreciation of the flexibility characteristics of plants. In the meantime, the European Commission has approved the availability remuneration mechanisms adopted in the United Kingdom (capacity obligation), France (exchange certificates) and Germany (Network Reserve). Next steps: the Ministry for Economic Development, the Authority and Terna are working out to notify the Italian mechanism to the Commission while finalising some key aspects, including the strike price and the LOLE. Terna should call the auction for the first adoption stage at the end of 2017 for delivery in 2018. Quantification of imbalances for electricity - Period July 2012 – August 2014 (excluding June 2014)

Resolution no. 111/06 defines the rules and calculation methods for the quantification of imbalances to be applied to differences between the feed-in and consumption plans and actual production and withdrawals.

The imbalance policy has been the subject of several amendments by the Authority in order to align the regulation to the need for an efficient market configuration so as to encourage operators to always make the best production and consumption forecasts and avoid price brokerage on different markets. The containment of imbalances is desirable because it favours the reduction in the costs charged in end customer bills because Terna – with more accurate forecasts by dispatching users – uses less resources to balance the system in real time. For this reason, the imbalance policy has been subject to various changes by the Authority in order to align regulation with the need for efficient market configuration so as to drive operators to make better production and consumption forecasts, thus avoiding price arbitrage on different markets. Following the appeal filed by some operators, Resolutions no. 342/2012, no. 239/2013 and no. 285/2013 amending the above policy were annulled by the administrative judge for the period July 2012-August 2014 (excluding June 2014) on the ground of lack of motivation on the urgency and lack of consultation. Terna recalculated the imbalance prices according to the regulation in force before the annulled resolutions, and the necessary adjustment bills were directly offset at 30 June 2015, despite claims raised by A2A Group companies. In response to the requests made by some dispatching service users, the Authority initiated a process (contested by some operators) for the valorisation of the actual imbalances between 2012 and 2014, by means of resolution no. 333/2015/R/eel. After about a year of consultations, Resolution no. 333/2016/R/eel concluded the valorisation process of imbalances for the period 2012-2014, thereby arranging for Terna to return the amount offset in June 2015 to the companies by 1 November 2016. Some operators have appealed against Resolution 333/16//R/eel by invoking the precedent clause, which has been denied. The meeting of the Lombardy Regional Administrative Court, originally scheduled on 13 April 2017, was adjourned to 2018. - Definition of the new regulation effective on and after 1 August 2016

With Resolution 444/2016/R/eel, subsequently amended by resolution no. 800/2016/R/eel, the regulatory

22

framework on actual imbalances has been amended with effect on and after August 1, 2016.

The measures introduced some mechanisms aimed at providing more effective incentives to be planned with diligence, skill, prudence and foresight, and enabling, at the same time, the Authority to systematically detect any breach of this obligation (for all purposes, including the adoption of prescriptive and/or sanctioning measures). More specifically, the resolutions introduced amendments to the method of calculation of imbalances, by differentiating it in the case of production units (relevant, not relevant supplied by non-programmable renewable sources or not enabled, other than that supplied by renewable sources) or consumption units, with the application of the single price or the mix single-dual price scheme and providing different exemption thresholds. Pending the regulation of system imbalances, which will probably be implemented in 2019 and is likely to provide nodal imbalance prices, by Resolution 419/2017/R/eel, the Authority has introduced:

• effective on and after 1 July 2017 macro-zonal non-arbitrage fees, in order to eliminate distortions deriving from the determination of imbalance prices at a macro-zone level, at the presence of market prices determined at a zonal level;

• effective on and after 1 September 2017, the restoration of single price calculation of imbalances for all not enabled production units as well as a new less predictable method of calculation of the zonal sign implemented by Terna.

First opening of the Ancillary Services Market (MSD)1 to demand/accumulation systems/not yet enabled production units By resolutions 300/2017/R/eel and 372/2017/R/eel, the Authority ordered a first MSD opening through specific voluntary, demand-driven pilot projects, (non-programmable, relevant and non-relevant) FER2 programmable units not yet enabled and accumulation systems. In general, the scheme sets out:

• that PUs and CUs can participate either individually or through various types of aggregation: only production (UVAP3), only consumption (UVAC4) or mixed (UVA/UVAN5). Relevant PUs can aggregate each other and/or with other non-relevant UPs and any UCs only if they all come under the same node of the national transmission grid (UVAN). Both UVAC and UVAP may expect the presence of CU/PU in different despatching contracts with the need for explicit consent by the dispatching user (DU);

• a specific timetable for the presentation of projects by Terna to the Authority: within 30/06/17 for the UVAC pilot project and within 31/07/17 for the UVAP pilot project;

• among the main pilot project characteristics: - the possibility for operators to propose additional pilot projects to Terna for the supply of

individual services but also services which are not remunerated to date; - bidding obligations and methods in line with those currently provided for already enabled PUs; - CUs must be connected at HV, MV or LV, but processed on a hourly basis; - reduced role of distributors in this first stage; - no forms of economic incentives are envisaged in favour of pilot projects.

The first project implemented concerns the UVACs (single or multiple consumption facilities located in the same province or group of provinces) and consists of 2 activities:

1 MSD – Mercato del Servizio di Dispacciamento, Ancillary Services Market 2 FER – Fonti Energetiche Rinnovabili – Renewable Energy Sources 3 UVAP – Unità Virtuali Abilitate di Produzione – Virtual Production Enabled Units 4 UVAC – Unità Virtuali Abilitate al Consumo – Virtual Consumption Enabled Units 5 UVAN – Unità Virtuali Abilitate Nodali – Virtual Nodal Enabled Units

23

1. the participation of UVACs to the MSD for the supply of the Tertiary Replacement Reserve (RTs) and balancing from June 2017. The expected remuneration is limited to the activation of resources on MSD (€/MWh);

2. the possible participation to forward procurement of RTs by Terna and MSD balancing by enabled UVACs in North and Mid-North areas for the June-September 2017 period. This is a downward auction with fixed remuneration (base: 30,000 €/MW/year) and variable remuneration (€/MWh activated) with a strike price of 400 €/MWh. At July 1, 2017, 46 MW were assigned out of 500 MW auctioned.

In order to seize the opportunities offered by the new regulatory framework, an internal task force was set up within the A2A Group to implement UVAC and UVAP projects.

Incentives to production from renewable sources and conversion of the Green Certificate in tariffs Italian Legislative Decree no. 28/2001, implementing Directive 2009/28/EC, establishes the incentive schemes aimed at achieving the production targets from renewable sources by 2020, which were later put into force by Ministerial Decree of July 6, 2012 and June 23, 2016, for application by electric power plants supplied by renewable sources other than photovoltaic systems. The above decrees establish that production plants below a set power threshold are eligible for incentive tariffs (of the feed-in-premium type), which are accessible either directly or after entry into a dedicated registry, while an auction procedure is envisaged for plants of a higher capacity. According to the decrees, renewable energy plants that entered into operation prior to December 31, 2012 and have acquired the right to use Green Certificates (GC) are entitled to receive incentives paid by the Energy Services Operator (GSE) on net production for the remaining after-2015 period of entitlement to GC, in addition to revenues from the sales of production on the market. This incentive (I) is calculated as follows:

• I= k x (180 – Re) x 0.78; • k = technological coefficient of 1 for plants that entered into operation prior to December 31, 2007

and, for subsequent ones, the values set out by Law no. 244/2007 apply: • Re = is the sale price of electricity on the market, which was recorded in the previous year and

communicated by the Authority. The value of the incentive in 2017 amounts to 107.34 €/MWh. The same method applies to plants that benefit from green certificates for district heating (CV-TLR), the value of which is established at 84.34 €/MWh. Effective for period beginning on and after January 1, 2016, incentives are paid quarterly by the GSE by the end of the second quarter following that of reference and on the basis of the signing of an Agreement and upon registration and validation of the plants on the GSE portal. On March 25, 2016, GSE published a disclosure on the deadlines of GCs for 2014 and 2015, the collection of which can be requested to the GSE by March 31, 2017 and March 31, 2018, respectively. This clarification, which was strongly advocated by operators, is a confirmation of the bankability of the certificates and the possibility of using the storage of GCs until their expiration date. Large-scale hydroelectric concessions Despite the introduction of rules aiming to allow the conduction of tenders, the evolution of national legislative framework over the last few years, actually entails a continuation of existing large-scale concessions by the current holders, even when they are formally expired. Article 37, subsection 4, of Law no. 134/2012, converting Legislative Decree no. 83/2012, the “Growth Decree”, confirmed the term of 5 years before the expiry of the concession as the time limit for calling a tender for reassignment and, for new concessions, established a term of 20 years extendible to 30 years, depending on the extent of investments, according to criteria established by an implementing Ministerial Decree not yet

24

enacted. In addition, a special transitional (accelerating) scheme is established for calling tenders for concessions already expired or expiring by December 31, 2017 (for which it was impossible to comply with the tender-calling requirement of 5 years). These tenders shall be called within 2 years of the date on which said Ministerial Decree is enacted. The non-issuance to date of the “Ministerial Decree for Tenders” inevitably results in an extension of the management of concessions by the current concessionaires, including those falling due after 2017. As part of the formal default notice received from the European Commission affirming the opposition of Italian legislation to the rules and regulations of EU law, the Italian Government decided to propose to the Commission a future amendment to said rules, as part of an overall reorganization of the sector. At a regional legislation level, the Lombardy Regional Authority amended Regional Law no. 26/2003, first by Act no. 19/2010 and later by Act no. 35/2014, by adding article 53-bis that allowed outgoing concession-holders to temporarily continue to operate and imposed an additional fee. Lastly, with art. 62 of Law no. 221/2015 (“Collegato Ambientale”), the legislator equalized upward the unit value of the BIM supra-fee due from holders of small-scale concessions, of a nominal capacity exceeding 220 kW, making it identical to the fee due by the holders of large-scale concessions of a capacity exceeding 3 MW. Article 1, subsection 671, of the 2916 Stability Law, requires the reimbursement of additional hydroelectric fees paid to the State in the years 2006-2007 for the renewal of concessions. This provision was actually declared unconstitutional by the Constitutional Court. By Regional Council Resolution 5130-2016 of May 9, 2016, the Lombardy Regional Authority provisionally quantified the “additional fee” for hydroelectric concessions of expired large-scale concessions, which was introduced by Regional Law no. 19/2010 but have never been implemented up to now, to 20 €/kW of average nominal capacity, subject to subsequent increase (and related adjustment) if the studies being conducted by the regional authority reveal that the so-called “revenue” of expired concessions was higher. This Resolution was adopted despite the pending appeal filed by the National Government to the Constitutional Court against Lombardy Regional Law no. 22/2015. The arguments put forward by the Government are identical to those of the operators and A2A, which challenged previous regional resolutions on “temporary continuation of operations” of its concessions on the basis of the principle of homogeneity of the concession fees on the national territory as it falls under competition rules (art. 37, subsection 7, Law no. 134/2012), and as the “Bersani Decree” (Legislative Decree no. 79/99, art. 12, subsection 8bis) is clear in stating that the operation of expired concessions have continued by the outgoing concession-holder at the same terms and conditions until new assignment, without this requiring any regional measure. Instead, the regional authority justifies the additional fee on the assumption that it has already title to the hydroelectric plants and facilities by applying the former art. 25, subsection 1, of the Consolidated Act 1775/33, superseded by art. 37 of Law no. 134/2012. The additional fee would therefore represent the consideration for the enjoyment of said assets by the “former concession-holders”, on which, however, they continue to pay IMU (property tax) and other charges. It is noted that the Constitutional Court ruled in favour of the fees imposed by the Piedmont Regional Authority (Judgement no. 158, May 3, 2016) by Regional Law no. 22/2014 that is considered legitimate in the absence of Ministerial Decree provided by art. 37, subsection 7, of Law no. 134/2012, which shall set forth the general criteria for determining the maximum values of the fees of hydroelectric concessions on the part of the regional authorities, according to the principles of cost-effectiveness and reasonableness. By Council Resolution no.13993 of December 28, 2016, the Lombardy Regional Authority established, for the period January 1, 2011 to December 31, 2016, the amounts due as additional fees relating to large-scale concessions that have expired and have been authorised to temporary continue their operations, by quantifying the amounts on the basis of the unit amount of the additional fee of 20 €/kW of the average annual nominal power, previously determined in recognition of Council Resolution no. 5130 of May 9, 2016.

25

Efficient User Systems Efficient User Systems (SEU and SEESEU) are Simple Production and Consumption Systems consisting of at least one production plant and one consumption unit directly connected through a private link without obligation of connection to third parties, and connected directly or indirectly to the public network via at least one point. The awarding of the qualification as SEU or SEESEU, issued by the GSE, allows the recognition of facilitated tariff conditions on the electricity consumed and not withdrawn from the network, limited to the variable components of the system overheads, as envisaged by Legislative Decree no. 115/08. Decree Laws no. 91/14 and no. 116/14 and Authority Resolution no. 578/2013/R/eel define the regulatory framework of the SEUs that can fall within a scheme in which there is one Consumption Unit and Production Unit which, if recognized as such, allows for the payment of 5% overheads. To be eligible for this benefit as of January 1, 2014, the SEUs that commenced operations before December 31, 2014 had to be qualified by GSE, according to any of the possible types envisaged, by September 30, 2015. It is also possible to qualify the system after that date; however, the benefits will be calculated from the month following the qualification. For systems that became operational after January 1, 2015, it will be necessary to apply for the qualification after the entry into operation. In a clarification issued on June 12, 2015, the Authority specified that the generation auxiliary services are identified as ancillary services, according to Unipede (now Eurelectric) definition and therefore also plants that are ancillary to production, such as fuel handling equipment and heating, lighting and office systems directly related to power plant operations. The value of the SEUs and the clarification provided by the authority on auxiliary services is twofold because it allows:

- the plant self-consumptions to benefit from the exemption to pay 95% of system charges on self-produced and consumed energy;

- the plant to formulate investment proposals for the installation of systems generating electricity from renewable sources at industrial users.

It is also worth noting that the normative and regulatory framework is currently evolving: • by Municipal Decree DCO no. 255/2016/R/eel, the Authority proposed, pursuant to art. 3 of Legislative

Decree no. 210/2015 (so-called “Milleproroghe 2015”), effective for period beginning on and after January 1, 2016, a reform of the general charges of the electricity system applied to non-domestic customers, according to three different distribution options, namely fixed component (€/year), capacity component (€/kW) and variable component (€/kWh).

• Legislative Decree no. 244/2016 (so-called “Milleproroghe 2017”) set forth the postponement to January 1, 2018, of the reform concerning overheads and also established that “the variable components of system overheads are applied to electricity withdrawn from the public grid with mandatory third-party connection”.

By Resolution 481/17/R/eel, the Authority also set out the future mode of collection of charges differentiated into a fixed portion, a power portion and a variable portion. REMIT – European regulation on wholesale energy market integrity and transparency and start of procedures for potential market abuse European Parliament and Council Regulation no. 1227/2011/EU of October 25, 2011 (REMIT) on the integrity and transparency of the wholesale energy market, has established common rules to prevent abuse practices in wholesale electricity and natural gas markets. This regulation imposes an obligation on market operators to: a. publish inside privileged information; b. report to ACER (Agency for the Cooperation among National Energy Regulators), either directly or

indirectly, the data concerning operations carried out on wholesale energy products, both sale and purchase orders and executed transactions (reporting obligation).

As to reporting, by implementing the REMIT, the Commission adopted Regulation no. 1348/2014

26

(Implementing Acts), which established fulfilment procedures and timing. The data to be reported relates to standard contracts executed on organized markets and non-standard contracts executed bilaterally, contracts relating to the transport of electricity and gas and the key data relating to storage systems. The market operators involved are required to send the data to ACER through the organized markets where the transaction was carried out (ex. GME) or through the electricity and gas trading brokerage platforms. Effective from October 2015, the companies subject to reporting to ACER standard contracts executed on organised markets and non-standard contracts are required to be entered in the National Registry of market operators kept by the Authority (REMIT Registry). An administrative pecuniary fine of 10,000 to 200,000 euro is imposed on each non-registered operator acting in wholesale energy markets subject to this obligation. Article 22 of Law no. 61/2014 also attributes to the Authority full investigation and sanction powers for the application of the REMIT. By Resolutions no. 342/16/E/eel and 459/2016/E/eel, the Authority commenced two proceedings for the adoption of measures to promote competition and ensure proper operation of the markets, by adopting prescriptive measures or asymmetrical regulation measures against certain conduct on the part of dispatching service users in the electricity wholesale market, which may have detrimental effects on energy markets and can be potentially configured as market abuse under the REMIT. The conduct of users can be configured as: • potential market abuse, in accordance with article 5 of the REMIT – for the effects or signals sent (or

likely to be sent) – on the offer, the demand or the price of wholesale energy products; • possible breach of article 14, subsection 6, of Resolution no. 111/06, limited to programming strategies not

complying with the principles of diligence, prudence, expertise and foresight that should characterise the conduct of an operator in the dispatching service field.

By Resolution no. 813/2016/R/eel, the Authority intervened by providing for the first filing of individual proceedings implemented under Resolution 342/2016/R/eel. MIFID II (Directive 2014/65/EU) Directive 2014/65/UE – also known as MIFID II – reviews and replaces MIFID I (Directive 2004/39/EC), with the aim of developing a single market for financial services in Europe, where transparency and investor protection are guaranteed. The MIFID II extends its scope to previously unregulated financial instruments (commodities) and also applies to entities currently operating on different financial markets, including so-called over-the-counter transactions. Member States shall transpose the directive in their national law by July 3, 2017, and the MIFID II will be fully effective on and after January 1, 2018. As far as the energy market is concerned, the Directive and its regulations apply to financial instruments both on regulated markets and in OTC transactions, as well as to emission allowances (EUAs) wholesale energy products that are derivative contracts, with the exception of those envisaging physical delivery obligation. The definition of "Physical delivery obligation" is central to identifying which instruments are outside the scope of the financial instruments and therefore not subject to MIFID II obligations. In order to obtain the exemption to operate as investment firm, the companies operating on commodity derivatives shall pass the “ancillary test” to demonstrate that the trading activity is “ancillary” to the main one. The MIFID II will have an impact both at a strategic level in order not to exceed certain thresholds to be eligible for exemption and at an operational level, by requiring interventions on computer processes, procedures and infrastructures for the reporting and annual notification of the exemption.

27

COMMERCIAL BUSINESS UNIT Competition Delegated Decree, SIMILAR Protection6 and PLACET7 offer: elimination of the price protection system At the hearing held on October 7, 2015, the Parliament approved the annual draft bill for the market and competition (so-called “Competition Delegated Decree), which is still being discussed at the Senate as part of the process of conversion into Law. The section on “Energy” consists of series of articles establishing the end of gas protection and the improved protection of electricity effective from July 1, 2019, a set of rules on bid comparability, the monitoring by the Authority of the degree of liberalisation of both sectors and the creation of a list of vendors.

Numerous amendments had already been proposed in 2016 to the method of treating customers in the electricity sector (domestic and other LV utility customers) who, as of July 1, 2019, will be still served by the historical supplier. According to the current formulation of the text, as amended by the Parliament on 22 May 2017, bidding procedures are no longer envisaged by geographical area to identify suppliers for customers who have not chosen a supplier on the free market (auctions still apply – as now – for the safeguard service). The legislative measure is pending final approval by the Senate. At the same time, the Authority has pursued its own process of reform in order to promote the overcoming of the greater electricity protection scheme through increased customer capacity. By Resolution 369/2016/R/eel, the Authority introduced the price SIMILAR protection scheme (TS – similar to a supply in the Italian Retail Electricity Free Market) that is offered by sellers selected by the Sole Purchaser and can be chosen on a voluntary basis by customers still operating under the greater protection scheme via a portal operated by the same Sole Purchaser. The mechanism is characterised by contractual and economic conditions that are established by the Authority unless a one-off bonus (€/PoD) freely determined by operators is applied. Subsequently, the Authority proposed a consultation of its guidelines on the offer called “PLACET” (the acronym of Prezzo Libero A Condizioni Equiparate di Tutela, meaning an offer at free prices at conditions equivalent to those of protection), by specifying the contractual terms and conditions and the price components and structure that all free-market sellers shall apply to their domestic and non-domestic customers effective from January 1, 2018. Functional unbundling and Brand unbundling By Resolution no. 296/2015/R/com, the Authority adopted provisions on brand unbundling for vendors who operate in the free market and also under the greater protection service, by regulating:

- by June 30, 2016, as later extended to January 1, 2017, pursuant to Resolution no. 327/2016/R/eel: the use of separate communication policies and brands for the conduct of both activities, while maintaining the corporate distinctive features;

- by January 1, 2017: the conduct of commercial activities by using separate information channels, physical space and personnel.

Charge of the TV licence fee in the electricity bill Subsections 152-164, article 1, of Act no. 208/2015 on the “Provisions for the preparation of the State’s annual and multi-year budget” (so-called 2016 Stability Act), regulated the charging of the TV licence fee in the electricity bills issued by electricity companies to their customers. For the implementation of the above act, the Ministry for Economic Development (MiSE), jointly with the

6 Translator's Note: "Tutela SIMILE" is the name of an electricity delivery mechanism that offers customers protection similar to the free market. 7 Translator’s Note: a PLACET offer is an offer at free prices at conditions equivalent to those of protection.

28

Ministry of Finance, issued the Decree on "Regulation implementing article 1, subsection 154, of Act no. 208 of December 28, 2015 (TV licence fee charged in the electricity bill)", under which the companies entrusted to collect the television licence fee shall receive a reimbursement of costs sustained equivalent to 14 million euro in 2016 and a further 14 million euro in 2017. By Resolution 291/2017/R/eel, the Authority set out the criteria for the breakdown of the lump-sum contribution, by making a distinction between contributions covering investments and those covering operating costs; a fixed portion and a variable portion are envisaged according to the number of TV licence fees to be levied and taking into account the differences in the cost structure and economies of scale the characterize operators of different sizes. The amounts owed to each company will be calculated directly by the Single Buyer and communicated to the Inland Revenue agency. Economic conditions of the electricity sales service: a) Greater protection By Resolution no. 354/2016/R/eel, the Authority updated the economic conditions of the greater protection service for the third quarter of 2016, by applying a 4.3% increase, following the recognition in tariffs of so-called dispatching service extra-costs incurred by Terna and the subject of incorrect conduct on the part of operators (pursuant to Resolutions no. 342/2016/E/eel and 459/2016/E/eel). On the basis of the appeal filed with the Lombardy Regional Administrative Court (TAR) by the consumers’ associations Codacons and Comitas against Resolution no.354/2016/R/eel, by means of a monocratic precautionary decree, on July 19, the Judge suspended the tariff updating resolution, pending the hearing of the Regional Council scheduled on September 15. The Authority immediately filed a request for revocation against the monocratic precautionary decree, which was however rejected by the Regional Administrative Court (TAR), which upheld the rejection of increases in electricity tariffs effective as of July 1 onwards. In the hearing held on September 15, the Regional Administrative Court confirmed, however, the updates pursuant to Resolution no. 354/2016 until the February 16, 2017 hearing. At the same time, the Court ordered AEEGSI to adopt a measure to pre-determine the arrangements for the liquidation and automatic repayment, without the need for a specific request by end customers, in the event of a favourable outcome of the dispute. By Resolution 575/2016/R/eel, the Authority established an automatic return mechanism to users of the amounts recovered by Terna, under:

- any prescriptive measures regarding certain dispatching service users in withdrawal and feed-in (units not enabled) that already foreshadow a recovery procedure and whose outcomes will also derive from the debate at court between each operator and Terna;

- asymmetric regulation measures intended for dispatching service users in feed-in (enabled units) to be adopted.

The return mechanism envisages the inclusion of the amounts recovered in the determination of the uplift fee of the first quarter available, thus allowing their immediate recognition to dispatching service users and, through them, to the customers of both the free market and regulated market (without distinction). Pending the closing of the proceedings, the entities exercising greater protection have applied the economic conditions of the second quarter in certain periods (until July 19), and those of the third quarter in other periods (from September 15). At the hearing held on last February 16 at the Lombardy Regional Administrative Court, the applicants declared, in the light of the decisions made by the Authority by Resolution 575/2016, their lack of interest in the appeal and so the Court declared its impracticability (Codacons found that the Authority is finding overall resources to be recovered in favour of the users, by introducing mandatory measures). By Resolution no. 369/2016/R/eel, the Authority also changed the economic terms applied to the sale of electricity under greater protection effective beginning on and after January 1, 2017. This reform, which is detailed in the subsequent Resolution no. 633/2016/R/eel, established the Reformed Greater Protection Service

29

(MTR8), which is characterised as follows: - the energy price (PE) component of the energy and dispatching service fee (PED), covering the

purchasing costs of electricity supplied to greater protection customers, will be determined beforehand according to the quarterly average of the prices in the spot energy market (MGP9 and MPI), appropriately weighted with the withdrawal profile of the various types of customers in the reference quarter, the estimated operating cost of the Sole Purchaser, and taking into account the estimated financial expenses associated with the purchase and sale of electricity. The PE fee will be subject to a mechanism for the equalisation of costs, as currently envisaged;

- the dispatching service (PD) component of the energy and dispatching service fee (PED), will be determined as the quarterly average of dispatching service fees applicable pursuant to the TIS10, weighted with the withdrawal profile of the various types of customers belonging to each type of contract (except for non-domestic customers, for which the estimate is made on a monthly basis).