IL “ CATEGORY “ PER IL MERCATO INGLESE D r i nk i ng w at er Pu b l i c tr ans por t BS E GM M...

26

IL “ CATEGORY “ PER IL MERCATO INGLESE di David Buck

Transcript of IL “ CATEGORY “ PER IL MERCATO INGLESE D r i nk i ng w at er Pu b l i c tr ans por t BS E GM M...

IL “ CATEGORY “PER IL MERCATO INGLESE

di David Buck

La filieraLa filieraPrima del Category ManagementPrima del Category Management

SUPERMERCATO FORNITORE

DISTRIBUTORE

Consumatore

Supermercato Fornitore

Distributore

Category ManagementCategory Management

Ruolo del Supermercato

• Ruolo del compratore è cambiato ed è rivolto con maggiori attenzioni verso il consumatore e a ciò che accade nei negozi

• Marketing Research• Focus Group

• Dati statistici per la valutazione dei fornitori, KPI (Key Performance Indicators) Tabelle e Grafici

• Dà responsabilità al distributore

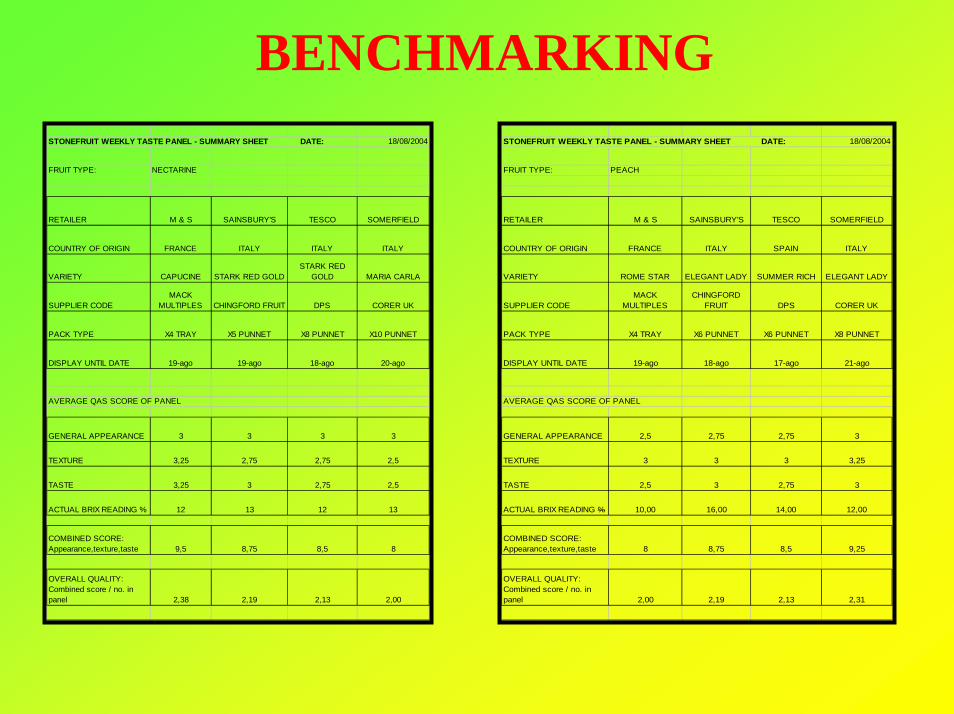

BENCHMARKINGSTONEFRUIT WEEKLY TASTE PANEL - SUMMARY SHEET DATE: 18/08/2004

FRUIT TYPE: NECTARINE

RETAILER M & S SAINSBURY'S TESCO SOMERFIELD

COUNTRY OF ORIGIN FRANCE ITALY ITALY ITALY

VARIETY CAPUCINE STARK RED GOLDSTARK RED

GOLD MARIA CARLA

SUPPLIER CODEMACK

MULTIPLES CHINGFORD FRUIT DPS CORER UK

PACK TYPE X4 TRAY X5 PUNNET X8 PUNNET X10 PUNNET

DISPLAY UNTIL DATE 19-ago 19-ago 18-ago 20-ago

AVERAGE QAS SCORE OF PANEL

GENERAL APPEARANCE 3 3 3 3

TEXTURE 3,25 2,75 2,75 2,5

TASTE 3,25 3 2,75 2,5

ACTUAL BRIX READING % 12 13 12 13

COMBINED SCORE: Appearance,texture,taste 9,5 8,75 8,5 8

OVERALL QUALITY: Combined score / no. in panel 2,38 2,19 2,13 2,00

STONEFRUIT WEEKLY TASTE PANEL - SUMMARY SHEET DATE: 18/08/2004

FRUIT TYPE: PEACH

RETAILER M & S SAINSBURY'S TESCO SOMERFIELD

COUNTRY OF ORIGIN FRANCE ITALY SPAIN ITALY

VARIETY ROME STAR ELEGANT LADY SUMMER RICH ELEGANT LADY

SUPPLIER CODEMACK

MULTIPLESCHINGFORD

FRUIT DPS CORER UK

PACK TYPE X4 TRAY X6 PUNNET X6 PUNNET X8 PUNNET

DISPLAY UNTIL DATE 19-ago 18-ago 17-ago 21-ago

AVERAGE QAS SCORE OF PANEL

GENERAL APPEARANCE 2,5 2,75 2,75 3

TEXTURE 3 3 3 3,25

TASTE 2,5 3 2,75 3

ACTUAL BRIX READING % 10,00 16,00 14,00 12,00

COMBINED SCORE: Appearance,texture,taste 8 8,75 8,5 9,25

OVERALL QUALITY: Combined score / no. in panel 2,00 2,19 2,13 2,31

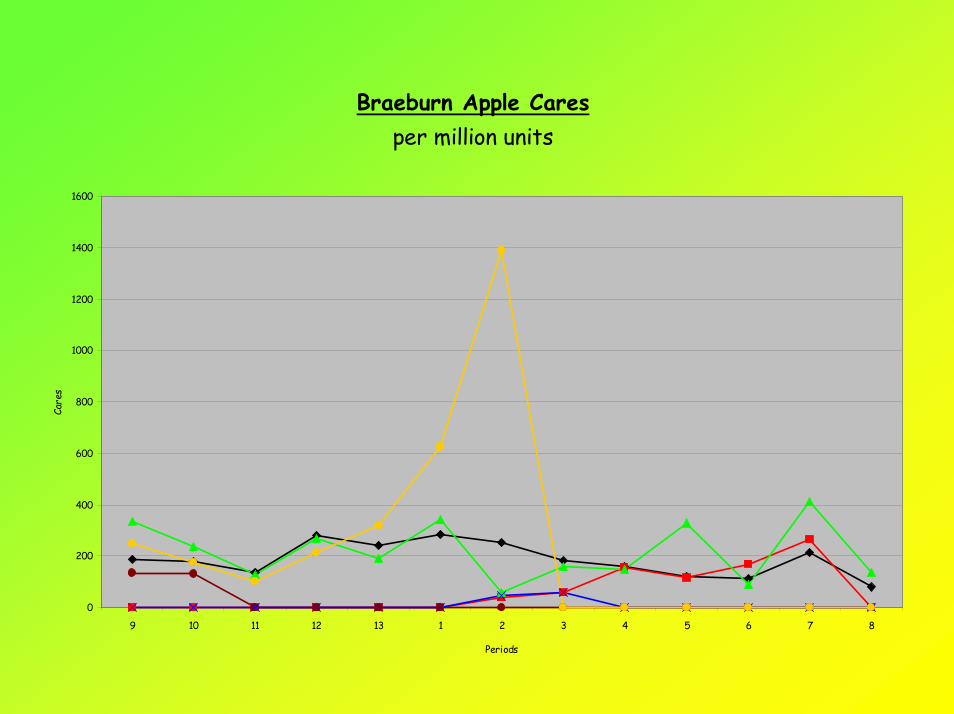

Braeburn Apple Caresper million units

0

200

400

600

800

1000

1200

1400

1600

9 10 11 12 13 1 2 3 4 5 6 7 8

Periods

Care

s

Golden Delicious Apple Caresper million units

0

100

200

300

400

500

600

700

800

900

1000

9 10 11 12 13 1 2 3 4 5 6 7 8

Periods

Care

s

Granny Smith Apple Caresper million units

0

100

200

300

400

500

600

700

9 10 11 12 13 1 2 3 4 5 6 7 8

Periods

Care

s

Tot Stonefruit Tot Peach Tot NectarineTrade % cge yr on yr (Expenditure) -4,47 20,10 -19,19

Cash value (000's) £46.259 £7.614 £16.273Cash value of yr on yr growth (000's) -£2.164 £1.274 -£3.864% contribution to Total Stone Fruit 16,46% 35,18%

Sainsbury Market Share 2004 18,07 12,06 18,48Market Share 2003 18,91 9,09 19,49% cge yr on yr (Expenditure) -8,73 59,31 -23,41Cash value (000's) £8.358 £918 £3.006Cash value of yr on yr growth (000's) -£799 £342 -£919% contribution to Total Stone Fruit 10,99% 35,97%

Tesco Market Share 2004 22,77 21,56 23,62Market Share 2003 23,79 20,74 24,90% cge yr on yr (Expenditure) -8,56 24,84 -23,32Cash value (000's) £10.533 £1.641 £3.844Cash value of yr on yr growth (000's) -£986 £327 -£1.169% contribution to Total Stone Fruit 15,58% 36,50%

Safeway Market Share 2004 6,59 8,57 6,95Market Share 2003 8,79 10,00 9,41% cge yr on yr (Expenditure) -28,31 2,93 -40,36Cash value (000's) £3.050 £653 £1.130Cash value of yr on yr growth (000's) -£1.204 £19 -£765% contribution to Total Stone Fruit 21,40% 37,07%

Morrisons Market Share 2004 5,08 7,77 6,19Market Share 2003 3,99 4,64 4,48% cge yr on yr (Expenditure) 21,49 100,88 11,76Cash value (000's) £2.350 £591 £1.008Cash value of yr on yr growth (000's) £416 £297 £106% contribution to Total Stone Fruit 25,16% 42,89%

Asda Market Share 2004 10,24 12,27 11,78Market Share 2003 9,09 13,03 10,24% cge yr on yr (Expenditure) 7,69 13,07 -7,01Cash value (000's) £4.738 £934 £1.917Cash value of yr on yr growth (000's) £338 £108 -£144% contribution to Total Stone Fruit 19,71% 40,46%

M & S Market Share 2004 8,32 3,67 7,15Market Share 2003 8,49 7,16 5,60% cge yr on yr (Expenditure) -6,35 -38,41 3,17Cash value (000's) £3.849 £279 £1.163Cash value of yr on yr growth (000's) -£261 -£174 £36% contribution to Total Stone Fruit 7,26% 30,22%

Waitrose Market Share 2004 4,23 5,07 3,39Market Share 2003 3,15 4,44 2,89% cge yr on yr (Expenditure) 28,23 37,19 -5,25Cash value (000's) £1.957 £386 £551Cash value of yr on yr growth (000's) £431 £105 -£31% contribution to Total Stone Fruit 19,74% 28,18%

MARKET SHARE

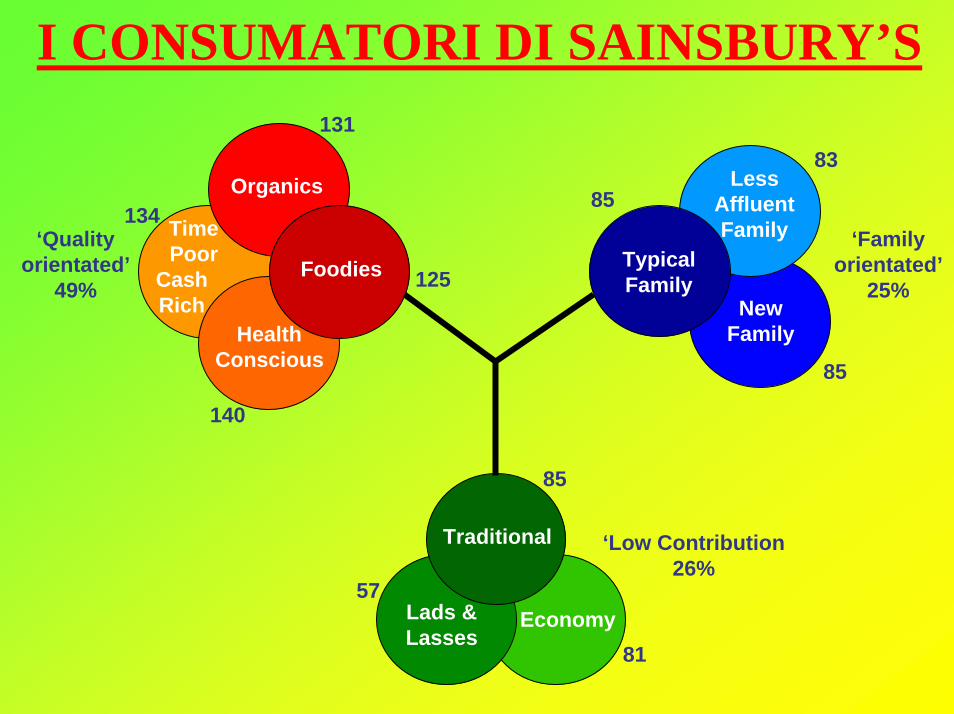

I CONSUMATORI DI SAINSBURY’S

Organics

TimePoor

CashRich

HealthConscious

Foodies TypicalFamily

LessAffluentFamily

NewFamily

Traditional

Lads &Lasses

Economy

‘Qualityorientated’

49%

‘Familyorientated’

25%

‘Low Contribution26%

85

81

57

85

83

85

131

125

140

134

CAPIRE I CONSUMATORI INFLUENZA LO STILE ARCHITETTONICO DEL SUPERMERCATO

TailoredOffers Formats Organisation Property

PortfolioPresente CustomerOpportunity

PropertyPortfolio

DifferentialOffer

RelevantCustomersPassato Organisation Formats

Q FB Q F Q FF

B

Q

Main+ AverageMain Average Main HighMain+ Low

Main Low

Q F

MixedGrab & Go

MixedMeals

Q F

P S+ ESP S+ ES P S+ ES P S+ ES P S+ ES P S+ ES

☺☺ ☺☺ ☺☺ ☺☺☺ ☺££

£ ££ £ ££

Qv

Qv

Qv

Qv

Qv

Qv

Qv

Qv

Proposition First for Food

Toolkit

Environment

Marc Profile

Own Label

Range / Choice

Q = Quality (TDD, BGTY, Premium Brands)F = Family (Standard+, Standard, Some Economy)B = Budget (Extended Economy, Tertiary Brands)

P = Premium S = StandardS+ = Standard Plus E = Economy

No Frills + GM----------------------------------------------

No Frills First for Foodies

Superior Food + GMFor Family and Home

-----------------------------------------------

First for Foodies & Typical Families

Fast, Fresh, NewAnd ExcitingFirst for Fresh

BusinessBenchmark

Extended

BasicNo Frills

Standard Flagship

+ Non-Food Starbuys + Non-Food Starbuys

Profile 18 Profile xxProfile 14 Avg: Profile 12High: Profile 13 Profile 11

TIPO DI SUPERMERCATI

Promotions

Service

Brand

DISTRIBUTORI / SUPERMERCATI12*2

231

* Da confermare dopo l’acquisto dellada parte di

Responsabilità del Distributore• Protegge il fatturato, il margine, il profitto del

supermercato• Fornire 52 settimane all’anno / Programmi• Prodotto secondo le specifiche di qualità del prodotto• Più libertà di scegliere i fornitori o paesi d'origine, tra

quelli approvati dal supermercato.• Il distributore deve inoltre garantire:

– Eurep Gap BRC Nature’s Choice (Certificazioni di qualità)– Carichi Diretti - Trasporto – Packaging, tecnologia, – Nuove varietà

IL DOVERE DEL FORNITORE

• Capacità di coprire i programmi• Specifiche di qualità del prodotto• Rispettare le regole di Assicurazione Qualità

(BRC - Eurep GAP – Nature’s Choice)• Fedeltà reciproca

COSA VUOLE IL CONSUMATORE

• Prodotto sano e sicuro• Prodotto disponibile tutto l’anno con stessa qualità

e caratteristiche• Prodotto che soddisfi i propri gusti

– facile da mangiare (senza semi)– sempre più dolce (Kiwi, Ananas)

• Confezioni adatte• Al consumatore non interessa la provenienza del

prodotto

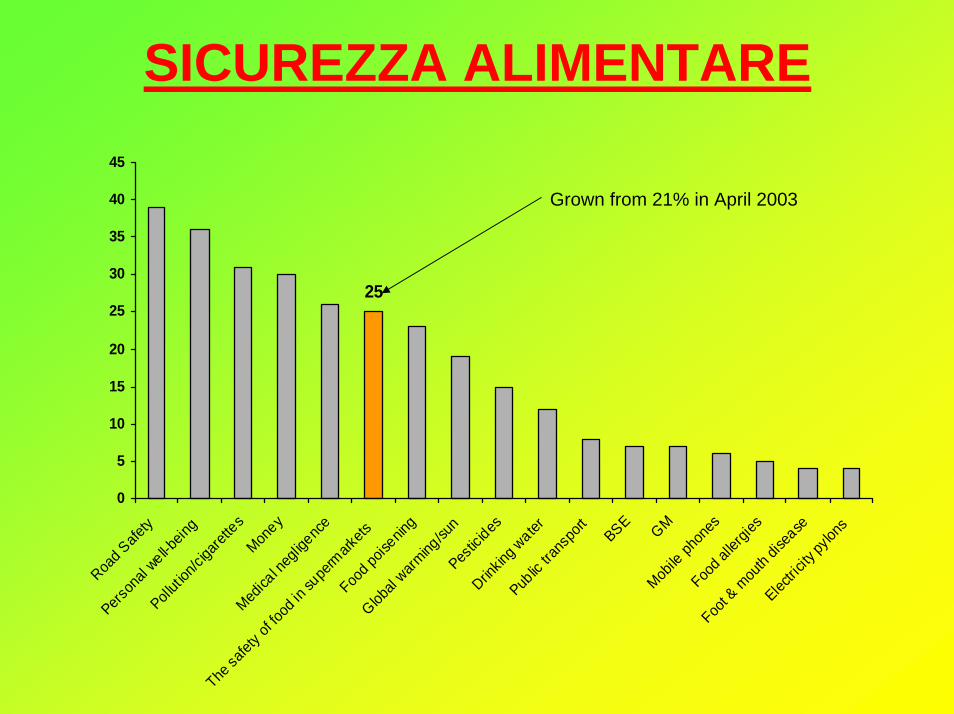

SICUREZZA ALIMENTARE

25

0

5

10

15

20

25

30

35

40

45

Road S

afety

Person

al well-b

eing

Pollut i

on/ci

garet

tesMon

ey

Medica

l neg

ligenc

e

The sa

fety o

f food

in su

perm

arkets

Food p

oisenin

g

Global

warming

/sun

Pestic

idesDrin

king w

ater

Public

trans

port

BSE GMMob

ile ph

ones

Food a

llergi

es

Foot &

mou

th dis

ease

Electric

ity py

lons

Grown from 21% in April 2003

0

10

20

30

40

50

60

70

80

90

100

Salmon

ella &

E-Coli

BSE in bee

fHigh s

ugar/fa

tBSE in

lamb

Pesticid

e res

idues o

n prod

uce

Quality

chec

ked fo

r SSL

Misleadin

g lab

elling

High salt

levels

Caged h

ens

DNA trace

ability

of bee

f GMPes

ticides

Artificia

l flavo

uring

sFoo

d colou

rings

Suppo

rting B

ritish

farm

ersFarm

assu

rance

GM in anim

al fee

d

Environ

mental

damag

e thro

ugh fa

rming

Animal w

elfare

in m

eat/e

gg pr

oduct

ion

Preserv

atives

in fo

od

Antibiot

ics in

anim

al tre

atmen

t

Unhealt

hy kid

's foo

d

Recycling

- pac

kagin

g

Ingredie

nt au

thenti

city

0

10

20

30

40

50

60

70

80

90

100

Pollutio

n

Fair tra

de prod

uctsLo

cal sourc

ing

Food wast

age in

store

Colours in

an imal feed

Animal m

atter

in an

imal

feed

SSL outdoor re

ared ra

nge

Socially

respon

sible tra

ding

On pack tem

perature

Food a llergies

/range

Artific ia l sw

eeteners

Mecha

nically

recov

ered m

eat

Recycling

facili

ties in

store

Added water in

meat/fi

sh produc

ts

Sourcing

from th

e wildBiodiv

ersityFortif

icatio

nFoo

d miles

British organic

farm

ersOrgan

ic foo

d5-a

-day

Highest

organ

ic standa

rds

Use of w

ords li

ke trad

itiona

l/assur

ed

Irradia

tion of fo

od

Marine Stew

ardship

Council

Nov 2002 Nov 2004Nov 2003 Biggest increases

SICUREZZA ALIMENTARE

SICUREZZA ALIMENTARE

• Eurep Gap/ BRC / Tracciabilità/Nature’s Choice• Prodotti Biologici• Cattiva pubblicità sulla stampa ed in TV• Name & Shame• Commercio Equo - Solidale• Social Responsible Trading ( es. SA 8000 )

NETTARINE

• PUNTI FORTI – Buone varietà apprezzate dal mercato inglese– Buone quantità, disponibili in maniera uniforme durante

tutta la stagione.– Il mercato in leggera crescita a scapito delle pesche.

• PUNTI DEBOLI– Mancanza di proposte di nuova varietà in confronto alla

Spagna.– Non adeguati controlli di qualità e di shelf life durante le

operazioni di confezionamento.– Prodotto non uniforme.

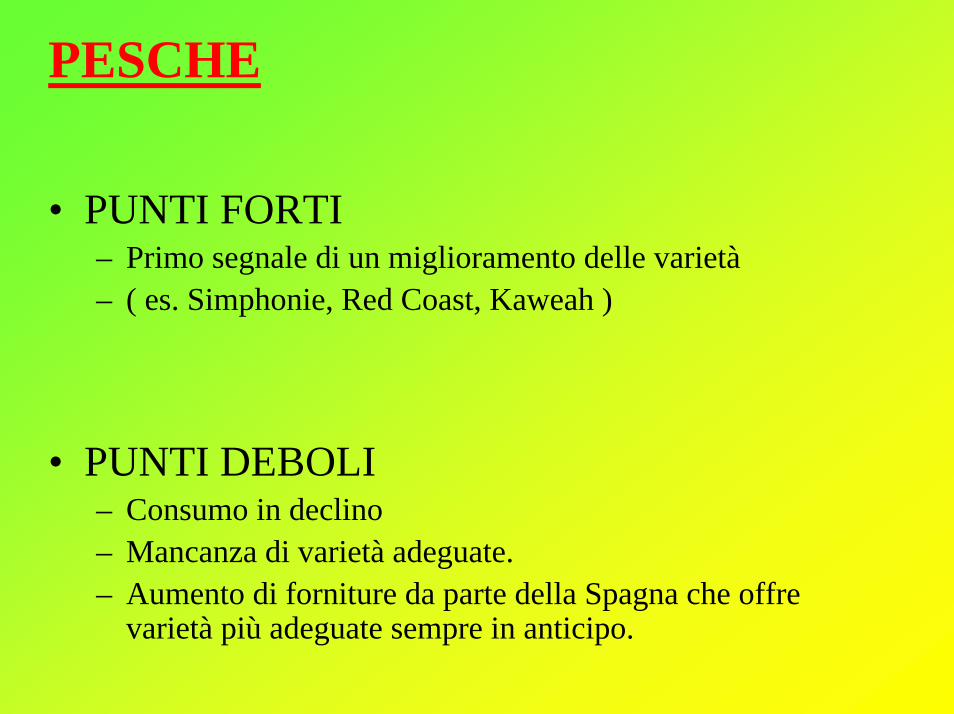

PESCHE

• PUNTI FORTI– Primo segnale di un miglioramento delle varietà – ( es. Simphonie, Red Coast, Kaweah )

• PUNTI DEBOLI– Consumo in declino– Mancanza di varietà adeguate.– Aumento di forniture da parte della Spagna che offre

varietà più adeguate sempre in anticipo.

TECNOLOGIA

• Per innalzare il livello medio qualitativo e per portare un maggiore uniformità e fiducia al consumatore occorre sfruttare le nuove tecnologie

• Lo strumento FTA ( Pressione )• La tecnologia NIR ( °Bx – Difetti Interni)

VENDITE IN % DEI PRODOTTI DI LARGO CONSUMO

Percentage contribution of individual sub-categories

2 0.9 6 % 2 2 .4 2 % 1 9 .4 3 %2 5 .1 9 % 2 3 .6 9 %

1 4 .7 0%1 9 .3 9 %

2 4 .4 6 %

1 3 .4 0%1 5 .2 1 % 1 8 .01 %

1 9 .5 3 %1 8 .1 6 %

1 0.2 8 %

1 6 .2 3 %

2 0.8 5 %

1 7 .7 7 %1 7 .8 7 % 1 7 .03 %

1 6 .7 3 %1 6 .6 9 %

1 4 .00%

1 7 .7 5 %

1 6 .1 7 %

7 .6 7 % 8 .4 2 %

7 .8 4 %7 .4 9 %

1 4 .9 4 %

8 .3 8 %

8 .7 2 %1 1 .8 6 %

1 3 .1 3 % 1 2 .4 2 %

1 2 .4 5 %1 1 .2 4 %

1 3 .6 1 %

1 0.06 %

1 0.8 7 %8 .1 7 %

8 .2 9 % 7 .7 2 %8 .04 %

8 .9 8 %

1 2 . 9 1 % 1 2 . 4 3 %8 . 7 5 %

2 3 . 1 5 %1 5 . 2 2 %

8 . 4 3 %

4 .2 6 %

4 .4 0% 3 .8 1 %

5 .1 8 %

5 .9 1 %5 .3 7 %

4 .5 0%4 .8 6 %

1 0.4 8 %

6 .2 2 %6 .9 4 %

4 .1 2 %

5 . 9 3 %1 0 . 4 9 %

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sainsbury Tesco Saf eway Asda Morr isons Marks andSpencer

Wait rose Somerf ield

Apple Bananas Citrus Pears Stone-fruit Grapes Tropical Soft fruit

CONCLUSIONI

• Il consumatore è la figura più importante della filiera

• I Supermercati UK hanno quasi monopolizzato la distribuzione ( 80% )

• Il paese d’origine del prodotto ha adesso poca importanza

CONCLUSIONI

• I fornitori diventano sempre più specializzati e per “selezione naturale” il loro numero si riduce

• Chi non rispetta le regole imposte dal Supermercato è fuori…comunque coloro che le rispettano hanno accesso al canale di vendita più importante del mercato UK (80%)

…E FINALMENTE !!!!!!!

![CPDLViolino [I] T T T T ˝ ‘ Violino [II] T ˝ ‘ ‘ • ‘ ˝ ˝ ‘ Cornetto [I] T T T T ˝ ‘ Cornetto [II] T ˝ ‘ ‘ • ‘ ˝ ˝ ‘ Cornetto [III] T T T](https://static.fdocumenti.com/doc/165x107/603c519bcaf49e6c0f1d3476/violino-i-t-t-t-t-a-violino-ii-t-a-a-a-a-a-cornetto.jpg)