Buonocore Originial Lesson 1

20

Narration: Welcome to the first lesson in the Basic Flexible Benefits Plan training series. This lesson is the Introduction to Flexible Benefits Plans. An understanding of Flexible Benefits Plans will help increase your sales because the plan is a financial tool that provides preferential tax treatment. Which means to you; that you’ll be able to show your clients (employers and employees) a way to save additional tax dollars. And the real benefit to you is that you’ll be establishing a long term business relationship and creating a ‘benefits partner’. Click the next button to start the training. ____________________________________________ Facilitator Notes: Above is the narration text used for the self paced version of the lesson. This is the rough draft of what will eventually be the Facilitator Guide Notes, which is still being put together. This lesson is designed to be used for both CLA of NY training – there are no company specific information. There are also slides listed as (Hidden) which are in the presentation for the self paced version only and will be removed before the final Facilitator version is released. The slide animation is also contained in the Facilitator Notes – please make note of when animation comes into the slide (ie by click of the mouse, with previous, etc.). This will help you to make better use of the slide and get the anticipated impact of the animation. At this point you do not necessarily have to use the Unit Of Conviction as in the narration – this OUC is listed on the next slide with the topics that will be covered. 1 Lisa Buonocore EDET 709 Big Redesign

-

Upload

lisa-kolakowski -

Category

Documents

-

view

225 -

download

2

Transcript of Buonocore Originial Lesson 1

Narration: Welcome to the first lesson in the Basic Flexible Benefits Plan training series. This lesson is the Introduction to Flexible Benefits Plans. An understanding of Flexible Benefits Plans will help increase your sales because the plan is a financial tool that provides preferential tax treatment. Which means to you; that you’ll be able to show your clients (employers and employees) a way to save additional tax dollars. And the real benefit to you is that you’ll be establishing a long term business relationship and creating a ‘benefits partner’. Click the next button to start the training. ____________________________________________ Facilitator Notes: Above is the narration text used for the self paced version of the lesson. This is the rough draft of what will eventually be the Facilitator Guide Notes, which is still being put together. This lesson is designed to be used for both CLA of NY training – there are no company specific information. There are also slides listed as (Hidden) which are in the presentation for the self paced version only and will be removed before the final Facilitator version is released. The slide animation is also contained in the Facilitator Notes – please make note of when animation comes into the slide (ie by click of the mouse, with previous, etc.). This will help you to make better use of the slide and get the anticipated impact of the animation. At this point you do not necessarily have to use the Unit Of Conviction as in the narration – this OUC is listed on the next slide with the topics that will be covered.

1

Lisa Buonocore EDET 709 Big Redesign

Narration: The purpose of this training is to help you understand the basics of Flexible Benefits Plans, a value added service we offer to many of our accounts. The information in this training is at a high level. For more detailed information please refer to the resources noted throughout the lesson. On the Main Menu screen you can roll your mouse over each topic to get a brief explanation of that section. ___________________________________________ Facilitator Notes: Review the topics that you will be discussing during this lesson. Review the Unit Of Conviction: “Welcome to the first lesson in the Basic Flexible Benefits Plan training series. This lesson is the Introduction to Flexible Benefits Plans. An understanding of Flexible Benefits Plans will help increase your sales because the plan is a financial tool that provides preferential tax treatment. Which means to you; that you’ll be able to show your clients (employers and employees) a way to save additional tax dollars. And the real benefit to you is that you’ll be establishing a long term business relationship and creating a ‘benefits partner’. “

2

Lisa Buonocore EDET 709 Big Redesign

Narration: The training objective for the next 20 to 30 minutes is to supply you with a basic introduction and understanding of Flexible Benefits Plans – or Flex Plans for short. We will specifically be focusing on Premium Only Plans – or POP for this series of training lessons.

3

Lisa Buonocore EDET 709 Big Redesign

Narration: Flexible Benefits Plans, also known as Section 125 plans, were created by Congress in 1978 as a result of Internal Revenue Code Section 125. At this time the practice of cost sharing the major medical premiums was becoming more and more popular in the work place. This had not always been the case – the cost of benefits for many years had been accepted as part of an employee’s compensation package. As the cost of health insurance began to increase this practice became more difficult to financially maintain for business owners and the concept of sharing the expense took hold in the workplace. Today you occasionally might find a company that still pays for 100% of an employee’s benefits, but that is no longer the norm. Seeing the need to assist the average working American to afford the additional cost of benefits premiums the government decided to allow a tax break for those premiums that were payroll deducted – we call this pre-taxing, or preferential tax treatment. •This section of the IRS code helps: •Address the benefits needs of America’s changing work force. •Contain the escalating costs of employee benefits programs. •Most importantly, make benefits more affordable through preferential tax treatment. Basically, with a Flex Plan in place, employees have a choice between tax free benefits and cash, which is a taxable benefit. Because these benefits are free from federal and state income taxes, an employee's taxable income is reduced, which increases the percentage of his/her take-home pay. And because the pre-tax benefits aren't subject to federal social security withholding taxes, employers win by not having to pay the Federal Insurance Contribution Act – more commonly known as FICA, taxes on those dollars. We offer our clients the opportunity to set up Flexible Benefits Plans that best fit their needs at little to no cost to them. ________________________________ Facilitator Notes: At this point you are setting the stage for the lesson. These points are covered in more detail in the other to lessons in this series – Positioning Flexible Benefit Plans To The Employer and Positioning Flexible Benefit Plans To The Employee.

4

Lisa Buonocore EDET 709 Big Redesign

Narration: The name “cafeteria plan”, “flex plan”, and “section 125 plan” are all other terms that are used to describe a flexible benefits plan. Plans may include one or all of the following design types: The first is a Premium Only Plan (also known as a POP). An employer may contribute to the premium for a plan that pays employees a benefit in the event of personal injury or sickness, disability, cancer, dental or vision care, and/or accidental death and dismemberment. These plans may be offered through a traditional insurance contract (i.e., major medical plan, individually owned and voluntary insurance), a health maintenance organization (HMO), or a self-insured program. When an employer makes such contributions, they are not taxable income to the employees who are covered. In addition, employees are not taxed on their pretax contributions to this plan because, under a flexible benefits plan, all contributions, whether made by an employee or an employer, are considered to be employer contributions for tax purposes. Simply put, a Premium Only Plan allows employees to pre-tax dollars for qualified insurance premium. The Premium Only Plan is the plan that we will be focusing on for the remainder of this lesson. Next is Medical Flexible Spending Account. Employers may establish a health care flexible spending account that reimburses employees for health care expenses not covered by the employer’s major medical plan or other insurance carrier. This allows employees to set aside pre-tax dollars to pay for qualified out-of-pocket health care expenses. And finally there is Dependent Care Flexible Spending Account. Employers may establish dependent care flexible spending accounts for their employees. Because the employer provides this benefit, it is not taxable. This allows employees to set aside pre-tax dollars to pay for qualified dependent day care expenses. __________________ Facilitator Notes: If you have the time, this would be a good time to lead a discussion with the class about their experiences with Flexible Benefits Plans. This will also allow you to gauge their knowledge level. EXTRA FOR YOUR INFORMATION Definitions: POP - Accident and Health Plan (IRC Section 106) Under Section 106, an employer may contribute to the premium for a plan that pays employees a benefit in the event of personal injury or sickness, disability, cancer, dental or vision care, and/or accidental death and dismemberment. These plans may be offered through a traditional insurance contract (i.e., major medical plan, individually owned and voluntary insurance), a health maintenance organization (HMO), a health savings account (HSA), or a self-insured program. When an employer makes such contributions, they are not taxable income to the employees who are covered. In addition, employees are not taxed on their pretax contributions to this plan because, under a flexible benefits plan, all contributions, whether made by an employee or an employer, are considered to be employer contributions for tax purposes. Medical FSA - Health Care Flexible Spending Account (IRC Section 105) Under Section 105, employers may establish a health care flexible spending account that reimburses employees for health care expenses not covered by the employer’s major medical plan or other insurance carrier. This may include expenses such as deductibles, co-payments, hospital and laboratory services, prescription drugs, certain over-the-counter medications, eyeglasses, hearing aids, and other medical aids or services as described in Section 213 of the IRC. Like the dependent care flexible spending account, this benefit is not taxable because it is provided by the employer. In return for this benefit, participants in a health care flexible spending account can agree to a reduction in salary to contribute pretax dollars to the plan to pay for these medical expenses. Refer to the “Health Care Flexible Spending Accounts” section of the Flexible Spending Accounts chapter for a detailed explanation of this program. Dependent Care FSA - Dependent Care Flexible Spending Account (IRC Section 129) Under Section 129, employers may establish dependent care flexible spending accounts for their employees. Because the employer provides this benefit, it is not taxable (within the limits set by Section 129). In return for this benefit, the employees can agree to reduce their salaries and contribute to the plan. If employees decide to participate in a dependent care flexible spending account, they elect to have a specified amount of pretax dollars deducted from their paychecks each pay period. Pretax dollars are taken from their gross earnings, before taxes are deducted. These dollars are then contributed to the plan. After employees submit receipts for acceptable expenses, they are reimbursed by the plan. The reimbursement is tax-free. However, the Internal Revenue Code limits the annual reimbursements to employees. These limits are discussed in detail in the “Dependent Care Flexible Spending Accounts” section of the Flexible Spending Accounts chapter. The dependent must meet the legal definition of a dependent, day care services must be performed by a qualified service provider, and the services must enable the employee and the spouse to work. Again, refer to the “Dependent Care Flexible Spending Accounts” section of the Flexible Spending Accounts chapter for a detailed explanation of this program.

5

Lisa Buonocore EDET 709 Big Redesign

Narration: This series of lessons will be focusing on the most popular form of Flexible Benefits Plans – the Premium Only Plan. POPs allow employees to pay their share of the cost of qualified benefit plans with pre-tax salary dollars through premium conversion. Premium conversion (sometimes called salary redirection) is a process in which the premiums that employees pay for qualified benefits are deducted from their salaries before income and Social Security (FICA) taxes are calculated. As a result, employees’ taxable incomes are decreased. Our products and services help employers build a customized flexible benefits plan. Employees have a menu of benefits to choose from which gives them the opportunity to tailor their benefits package to meet their individual needs. In addition, employees who choose to purchase our qualified products have the option of pre-taxing the premiums for most products. We offer administration of this Premium Only Plan (POP) through an external vendor at no charge to an employer as a value added service , as long as they maintain a minimum of $1,800 in annualized premium. The account needs to maintain this minimum in order for us to continue to pay the vendor fee for them. The Employer is the “plan sponsor” and is responsible for maintaining compliance with federal and state regulations. _____________________________ Facilitator Notes: Premium Only Plan (POP) POP plans are the most popular use of cafeteria plans and allow employees to pay their share of the cost of qualified benefit plans with pre-tax salary dollars.

6

Lisa Buonocore EDET 709 Big Redesign

Narration: Let’s look at who benefits from a Premium Only Plan? First the benefits to the employer are that: •It enhances the employer’s current benefits program by offering additional choices to meet the individual needs of the employees. •It makes benefits more affordable for employees through preferred tax treatment. •And finally, it reduces an employer’s payroll taxes.

These benefits to pre-taxing help an employer attract and maintain quality employees through a well rounded benefits package. And of course, what employer doesn’t like the idea of adding to their bottom line by saving taxes. So the employer “wins” with a Flexible Benefits Plan! An employer can implement a flexible benefits plan with little expense. The potential cost considerations include fees paid to a lawyer or professional tax advisor, third-party administrative services fees, and the cost of updating the payroll system to accommodate pretax deductions. Although the plan is the employer’s plan, some insurance companies (ourselves included) can help provide the employer with the communication support and documentation required to implement the flexible benefits plan. It is recommended that employers start by implementing a premium only plan, at least for the first plan year. At the plan anniversary, the employer may add a dependent care and/or health care flexible spending account as additional benefits choices. <SLIDE ANIMATION HERE– have the win situation appear>

7

Lisa Buonocore EDET 709 Big Redesign

Narration: Now – what can a Premium Only Plan do for an employee? The benefits to the employee from a POP are that: •It provides employees the ability to tailor a benefits program to their individual needs. •It offers preferential tax treatment, which makes the purchase of employee benefits more affordable through federal, state, and FICA tax savings. •And it gives a potential increase in spendable income, or the opportunity to purchase additional benefits with the tax savings. The conversion of qualified insurance premiums to pretax dollars allows the employer and the employee to take advantage of the additional choice and tax savings without a major disruption in the benefits program, and is a fairly simple concept to communicate to employees. This is now a WIN – WIN SITUATION!! <SLIDE ANIMATION HERE– have the win – win situation appear>

8

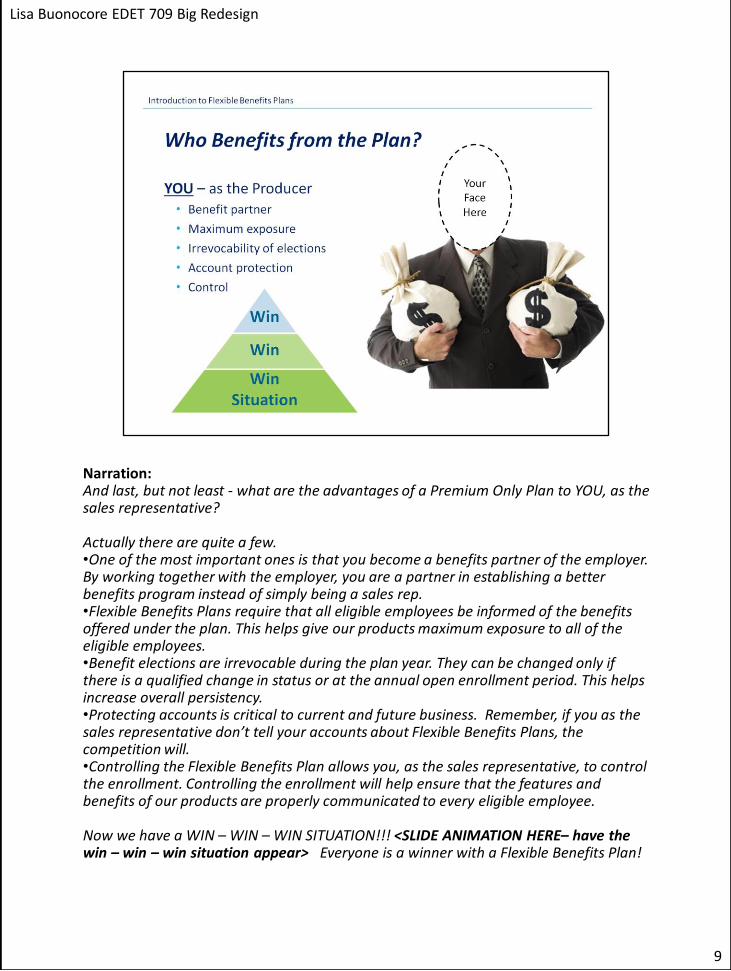

Lisa Buonocore EDET 709 Big Redesign

Narration: And last, but not least - what are the advantages of a Premium Only Plan to YOU, as the sales representative? Actually there are quite a few. •One of the most important ones is that you become a benefits partner of the employer. By working together with the employer, you are a partner in establishing a better benefits program instead of simply being a sales rep. •Flexible Benefits Plans require that all eligible employees be informed of the benefits offered under the plan. This helps give our products maximum exposure to all of the eligible employees. •Benefit elections are irrevocable during the plan year. They can be changed only if there is a qualified change in status or at the annual open enrollment period. This helps increase overall persistency. •Protecting accounts is critical to current and future business. Remember, if you as the sales representative don’t tell your accounts about Flexible Benefits Plans, the competition will. •Controlling the Flexible Benefits Plan allows you, as the sales representative, to control the enrollment. Controlling the enrollment will help ensure that the features and benefits of our products are properly communicated to every eligible employee. Now we have a WIN – WIN – WIN SITUATION!!! <SLIDE ANIMATION HERE– have the win – win – win situation appear> Everyone is a winner with a Flexible Benefits Plan!

9

Lisa Buonocore EDET 709 Big Redesign

Narration: As an employer-provided program, flexible benefits plans allow employees to pay for certain qualified benefits with pretax dollars. Examples of qualified benefits include:

•Accident and health plans, including spouse and dependent coverage. •Group term life insurance (employee only). •Contributions to a dependent care flexible spending account. •Contributions to a health care flexible spending account. •Adoption assistance. •401(k) plans. •Health Savings Accounts (HSAs).

Some of the benefits that do not qualify to be offered under a flex plan:

•Universal life insurance. •Whole life insurance. •Long-term care insurance. •Dependent life insurance. •403(b) and 457 plans. •Health Reimbursement Arrangements (HRAs).

10

Lisa Buonocore EDET 709 Big Redesign

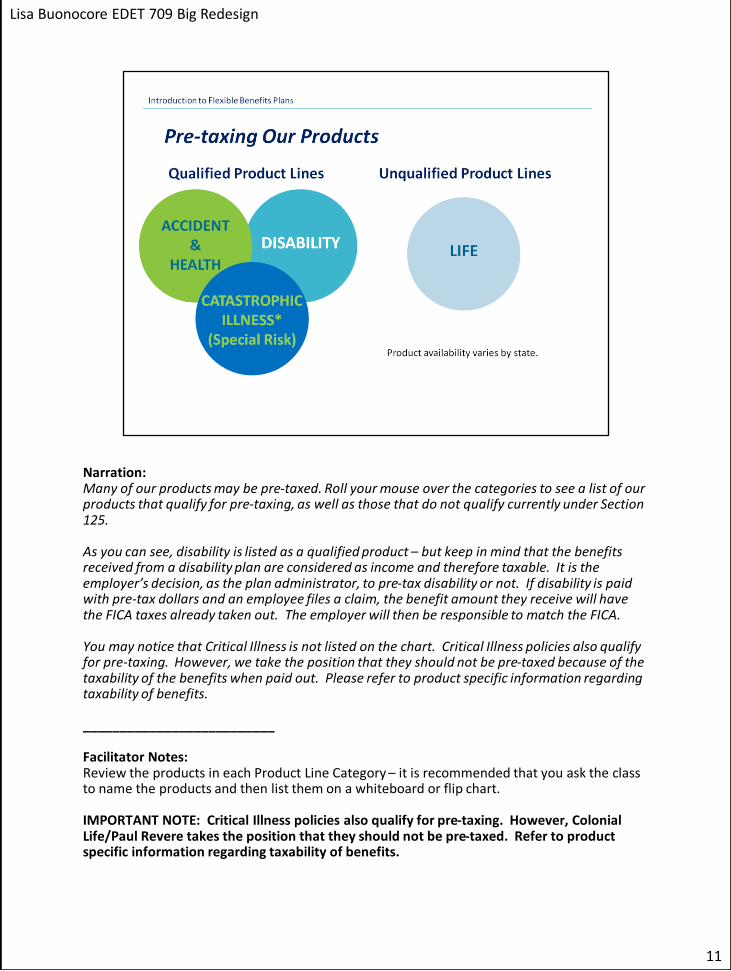

Narration: Many of our products may be pre-taxed. Roll your mouse over the categories to see a list of our products that qualify for pre-taxing, as well as those that do not qualify currently under Section 125. As you can see, disability is listed as a qualified product – but keep in mind that the benefits received from a disability plan are considered as income and therefore taxable. It is the employer’s decision, as the plan administrator, to pre-tax disability or not. If disability is paid with pre-tax dollars and an employee files a claim, the benefit amount they receive will have the FICA taxes already taken out. The employer will then be responsible to match the FICA. You may notice that Critical Illness is not listed on the chart. Critical Illness policies also qualify for pre-taxing. However, we take the position that they should not be pre-taxed because of the taxability of the benefits when paid out. Please refer to product specific information regarding taxability of benefits. __________________________ Facilitator Notes: Review the products in each Product Line Category – it is recommended that you ask the class to name the products and then list them on a whiteboard or flip chart. IMPORTANT NOTE: Critical Illness policies also qualify for pre-taxing. However, Colonial Life/Paul Revere takes the position that they should not be pre-taxed. Refer to product specific information regarding taxability of benefits.

11

Lisa Buonocore EDET 709 Big Redesign

Narration: To ensure compliance with the discrimination requirements of Flexible Benefits Plans, all employees should be eligible to participate in the plan. Exceptions should be stated in the plan document and must follow the regulations established by the IRS. These exceptions should be made only on advice from the employer’s legal counsel. The term employee does not include self-employed individuals or 1099 workers. Section 125 was designed to assist the average American worker to benefit from the preferential tax treatment. Based on the type of company, some owners may not be eligible to participate in the Flexible Benefits Plan. If it is a Sole Proprietorship – the owner, their spouse and legal dependents do not qualify to participate. If the owner’s spouse or legal dependent is an actual employee who is on the payroll, they may qualify. All other employees qualify to participate. If the company is a Partnership – the partners, their spouses and legal dependents do not qualify to participate. If the partners’ spouses or legal dependents are actual employees who are on the payroll, they may qualify. All other employees qualify to participate. ____________________________________ Facilitator Notes: Definitions- Sole Proprietorship. Business or financial venture that is carried on by a single person and is not a trust or corporation. A sole proprietor (sole owner) has unlimited liability. Schedule C of Form 1040 is used to report income and expenses of a sole proprietorship. Partnership. Association of two or more persons or entities that conduct a business for profit as co-owners. Except in the case of the limited liability partnership, which shares with the corporation the characteristic of being treated as a single entity whose members have limited personal liability, a partnership is traditionally viewed as an association of individuals rather than an entity with a separate and independent existence. A partnership cannot exist beyond the lives of the partners. The partners are taxed as individuals and are personally liable for torts and contractual obligations. Each is viewed as the agent of the others, and traditionally all are jointly and severally liable for the tortious acts of any partner.

12

Lisa Buonocore EDET 709 Big Redesign

Narration: If the company is a Subchapter-S Corporation – 2% or more stockholders, spouses, legal dependents, and attributed owners do not qualify to participate in the Flexible Benefits Plan. All other employees do qualify to participate. If the company is a Corporation – the shareholders, as long as they are employees, and all other employees qualify to participate. A corporate has two major characteristics that set it apart from a sole proprietorship and a partnership: (1st) a corporation is a legal entity that is separate from its owners. The corporation’s debts and liabilities belong to the corporation, not the owners. Corporations can sue or be sued, can enter into contracts, and can own property. (2nd) a corporation continues beyond the death of any or all of its owners. There are some companies that may be classified as Limited Liability Companies. Many states provide for the establishment of limited liability companies (LLCs). LLCs allow employers many of the advantages of corporate status—limited liability, transferability of interest, etc.—with the potential advantage of being treated as a partnership for tax purposes. As a result, the members/owners of an LLC cannot generally participate in a Flexible Benefits Plan. _______________________ Facilitator Notes: Definitions- Subchapter-S Corporation. A corporation with a limited number of stockholders (75 or fewer) that elects not to be taxed as a regular corporation, and meets certain other requirements. Shareholders include, in their personal tax return, their pro-rata share of capital gains, ordinary income, tax preference items, and so on. Corporation. Legal entity that is created by the authority of a governmental unit and that is separate and distinct from the people who own it.A corporate has two major characteristics that set it apart form a sole proprietorship and a partnership: (1) a corporation is a legal entity that is separate from its owners. The corporation’s debts and liabilities belong to the corporation, not the owners. Corporations can sue or be sued, can enter into contracts, and can own property. (2) a corporation continues beyond the death of any or all of its owners.

Limited Liability Company: Many states provide for the establishment of limited liability companies (LLCs). LLCs allow employers many of the advantages of corporate status—limited liability, transferability of interest, etc.—with the potential advantage of being treated as a partnership for tax purposes. As a result, the members/owners of an LLC cannot generally participate in a Flexible Benefits Plan. In some rare cases an LLC may be treated as a corporation for tax purposes. In such cases, the members/owners may be eligible to participate in a Flexible Benefits Plan, provided the corporation is not a subchapter-S corporation. All other employees who are not owners should be qualified to participate; however, the determination of eligibility is the sole responsibility of the plan sponsor.

13

Lisa Buonocore EDET 709 Big Redesign

Narration:

There are some areas of concern for flexible benefits plans with regards to market conduct risk. •The company’s role as a legal advisor. We are not licensed to provide legal or tax advice, and therefore will not provide a legal opinion on how to administer a flexible benefits plan or other legal areas, such as how to amend plan documents to make changes requested by an employer. •Reduction in Social Security benefits. Because the dollars redirected into the flexible benefits plan are not considered wages for the calculation of Social Security, such reductions may result in a decrease in the amount of Social Security benefits paid at retirement or disability. However, Social Security benefits are based on the entire work history minus the lowest 20 quarters – so any reduction in benefits should be minimal. •Free-look provision. If the enrollment for a flexible benefits plan is not concluded with a sufficient amount of time prior to the beginning of the plan effective date, problems may develop regarding a policyholder’s rights under the free-look provision. If the free-look provision extends past the plan effective date and the employee exercises his free-look option, the IRS does not make provisions for employers to stop the salary reductions. •Effective dates. The date a participant’s plan becomes effective is important, for our purposes, because the effective date directly impacts future billings and claims. When the effective date is not communicated properly, it can cause multiple service problems and may even cause legal problems. With a flexible benefits plan, problems with effective dates occur most often with newly eligible employees or existing employees who experience a status change.

14

Lisa Buonocore EDET 709 Big Redesign

Narration: So, why do we offer a Flexible Benefits Plan? It is a value added service that can sometimes make the difference for an employer when deciding to partner with us. For you as a sales representative, it comes back to the win – win – win scenario and is worth repeating these five points. •ONE - By working together with the employer, you are a partner in establishing a better benefits program instead of simply being an insurance agent. •TWO - Flexible Benefits Plans require that all eligible employees be informed of the benefits offered under the plan. This helps give our products maximum exposure to all of the eligible employees. •THREE - Benefit elections are irrevocable during the plan year. They can be changed only if there is a qualified change in status or at the annual open enrollment period. This helps increase overall persistency. •FOUR - Protecting accounts is critical to current and future business. Remember, if you as the sales representative don’t tell your accounts about Flexible Benefits Plans, the competition will. •FIVE - Controlling the Flexible Benefits Plan allows you, as the sales representative, to control the enrollment. Controlling the enrollment will help ensure that the features and benefits of our products are properly communicated to every eligible employee.

15

Lisa Buonocore EDET 709 Big Redesign

Narration: We have many excellent resources and tools when it comes to Flexible Benefits Plans. All of the marketing materials can be ordered and shipped to you – and many can be printed right from ProducerNet. On the screen you see several Internet links where you will find all the information about our partnership with AmeriFlex, as well as many useful forms and processes. Please take the time to review all the information you can about Section 125 and Flexible Benefits Plans. Now let’s see how much you’ve learned with a short quiz! Links: Ameriflex ePOP: https://www.epopdocs.com//index.php?template=colonial ProducerNet: https://producer.coloniallife.com/Departments/Marketing/FlexibleBenefits/FlexibleBenefits.asp Guide to Flexible Benefits: https://producer.coloniallife.com/Departments/Training/GuideToFlexBenefits/default.asp Flex125.com: https://www.flex125.com/af_site2/home.asp

16

Lisa Buonocore EDET 709 Big Redesign

Facilitator Notes: The following three slides are questions that you can ask the class and see if they learned anything! Question One: Which Flexible Benefit Plan option below allows employees to pay their share of the cost of medical coverage with pre-tax salary dollars?

DDC POP URM HSA

The correct answer is b – POP. A Premium Only Plan or POP allows participants to use pre-tax dollars to pay for qualified coverage premiums.

17

Lisa Buonocore EDET 709 Big Redesign

Question Two: Pre-taxing the premium for a qualified coverage reduces the cost of the coverage to the policyholder.

True False

The correct answer is b – False. Pre-taxing a premium does not have any impact on the cost, or premium, for that product. Pre-taxing allows the premium to be deducted prior to taxes being calculated saving federal, State, and FICA taxes.

18

Lisa Buonocore EDET 709 Big Redesign

Question Three: Who benefits from a Flexible Benefits Plan?

The Employer by reducing payroll taxes

The Employee by having a greater choice of benefits and saving Federal, State, and FICA taxes The Producer by establishing a Benefits Partner A and B only All of the above

The correct answer is e – All of the above. By implementing a Flexible Benefits Plan a “win – win – win” situation is created. The employer, the employee, and you, the producer, benefit.

19

Lisa Buonocore EDET 709 Big Redesign

Lisa Buonocore EDET 709 Big Redesign

20