TEMPUS PECUNIA EST - Aracne editrice · Beatrice Venturi Università degli Studi di Cagliari...

20

TEMPUS PECUNIA EST COLLANA DI MATEMATICA PER LE SCIENZE ECONOMICHE FINANZIARIE E AZIENDALI

Transcript of TEMPUS PECUNIA EST - Aracne editrice · Beatrice Venturi Università degli Studi di Cagliari...

TEMPUS PECUNIA EST

COLLANA DI MATEMATICA PER LE SCIENZE ECONOMICHEFINANZIARIE E AZIENDALI

Direttore

Beatrice VUniversità degli Studi di Cagliari

Comitato scientifico

Umberto NUniversity of Maryland

Russel Allan JUniversità degli Studi di Firenze

Gian Italo BUniversità degli Studi di Urbino

Giuseppe AUniversità degli Studi di Cagliari

TEMPUS PECUNIA EST

COLLANA DI MATEMATICA PER LE SCIENZE ECONOMICHEFINANZIARIE E AZIENDALI

Al suo livello più profondo la realtà è la matematica della natura.

P

Questa collana nasce dall’esigenza di offrire al lettore dei trattati che aiutinola comprensione e l’approfondimento dei concetti matematici che caratter-izzano le discipline dei corsi proposti nelle facoltà di Scienze economiche,finanziarie e aziendali.

This work was supported by IRITMED — “Istituto di Ricerca per l’Innovazione e laTecnologia nel Mediterraneo” Research Area: DynMED — and a grant of the RomanianNational Authority for Scientific Research and Innovation, CNCS — UEFISCDI, projectnumber PN–II–RU–TE–––.

Massimiliano Ferrara, Daniel Stefan ArmeanuFlorentin Serban, Maria Viorica Stefanescu

Silvia Cristina Dedu

Portfolio optimization

Copyright © MMXVIAracne editrice int.le S.r.l.

via Quarto Negroni, Ariccia Rome

()

----

No part of this book may be reproducedby print, photoprint, microfilm, microfiche, or any other means,

without the publisher’s authorization.

I edition: July

Contents

Foreword

Introduction

Chapter IThe investment decision under uncertainty

.. Some theoretical aspects about utility and uncertainty, – .. Risk in theassets portfolio, – ... General considerations, – ... Risk attitudes, –.. Utility functions, – ... The classical utility functions, – ... Other classof utility functions, – .. Quantifying the performance of a stock portfolio, – ... Computation of portfolio return, – ... Benchmark, – ... Overall mea-surement of portfolio’s performance, – ... Performances measurement coefficientsof portfolios based on systematic risk, .

Chapter IIRisk Estimation

.. Concepts of risk theory, – .. Measures used to assess the risks, – .. Modeling the risk of portfolio with VaR risk measures, – ... Riskestimation using the measure Value–at–Risk (VaR), – ... Case studies, –.. Risk estimation using the measure Conditional Value–at–Risk (CVaR), – ... Comparative study of the risk measures VaR and CVaR, – ... Theparametric method, – ... Historical simulation method, .

Chapter IIIPortfolio optimization using different risk measures

.. Mean–risk models, – ... Mean–Variance Model, – ... Mean–VaRModel, – ... Comparison of Mean – Variance and Mean – VaR Models, –.. Two stage Optimization Approach, – ... Mean–Variance Model withMinimal VaR, – ... Mean–VaR Model with Minimal Variance, – .. Mean–Variance–VaR Model, – .. Portfolio Optimization with a VaR alternative:Limited Value–at–Risk, – ... The Mean–LVar Model, – ... ComputationalResults, .

Chapter IVModels and methods in the analysis of stock values

.. Inputs for assessment, – ... Flow rates, – ... Growth rates, –.. Method of discounted future incomes, – ... Stocks with dividends,

Contents

– ... Stocks paying dividends in progression, – .. Multipliers method, –... Price/Book Value (P/BV) and Book Value per stock (BV), – ... Price/profitper share (P/E or PER) and earnings per stock (EPS), – ... Price/Sales (P/S)and turnover per stock (S), .

Chapter VBond financing

.. Technical elements of bond issuance, – ... Bonds, – ... The bondissuing process, – .. Bond valuation, – .. Repayment techniques for bondfinancing loans, – ... Bond financing repayment, – ... Equal principalpayments per period, – ... Final repayment, – ... Bullet amortization(single coupon), – .. Other indicators for bond analysis, – ... Bondyields, – ... Duration and sensitivity of a bond, .

Chapter VIOptions trading strategies

.. Simple transactions with options, – ... Long call, – ... Shortcall, – ... Long put, – ... Short put, – .. Strategies with op-tions, – ... Straddle, – ... Strangle, – ... Butterfly, .

Chapter VIIClassical models of portfolio management

.. The Markowitz Model of portfolio diversification, – .. The market’srentability (Sharpe), – ... Securities risk – the resulting composition betweenmarket risk and specific risk, – ... The equation of Sharpe’s market model, –.. The evaluation of financial assets CAPM, – .. Criticism of Markowitzand CAPM Models, – .. Arbitrage Pricing Theory Model, .

Chapter VIIIAlgorithm for hierarchical classification, based on an ultrametric dis-tance

.. Algorithm based on an Ultrametric Distance, – .. Empirical study onstocks listed on Bucharest Stock Exchange, – ... Financial ratios used in thestocks evaluation, – ... A Microsoft Visual Studio Application based on CLASSAlgorithm used for portfolio selection, – ... Evolution of the CLASS portfolio, .

Chapter IXThe conceptual and methodological approach of the portfolio optimiza-tion of financial assets in mean–VaR framework

.. Stage of selection of assets, – .. Phase estimation risk, – .. Opti-mization portfolio phase, – .. Application of optimization of a portfolio ofstocks listed on BSE, – ... Financial ratios used in the stocks evaluation, – ... Principal components analysis (selection of assets), – ... Risk estima-tion, – ... Portfolio optimization, – ... Portfolio performance, –

Contents

... Conclusions, – .. The relationship risk–return for constructing a opti-mal portfolio in mean–VaR framework composed from two risky assets and arisk–free asset, – ... The efficient frontier of the risk–return framework, – ... Case ρ = , – ... Case ρ = −, – ... Case − < ρ < , –... Case for assets, – .. Case study: Romanian Market, – ... Con-struction of an optimal portfolio made of risky assets, – ... Efficient frontierfor portfolio of two risky assets and a risk–free asset, .

References

Foreword

The research area targeted through this book is the Portfolio Management,as part of the financial theory and the experimental finance which in thelast decades have received special attention by a wide range of readers andnot only academicians.

We will use theories and concepts from two different fields: mathematicsand economics. Even if they work with different concepts and researchparadigms, the combination of the two fields makes possible the devel-opment of financial decision–making modelling. Through the rigorousmathematical model, the economics benefits from more realistic optimalsolutions, while mathematics benefits from being enriched with new con-cepts that have their origins in economic issues.

The project of our work is focused on the logic of optimization of theportfolio of financial assets such as the investment decision under uncer-tainty, risk estimation, portfolio optimization using various risk measures,models and methods in the analysis of stock values, bond financing, op-tions transaction and strategy, classical models in portfolio optimization,algorithms for hierarchical classification based on an ultrametric distanceand last but not least the conceptual and methodological approach of theportfolio optimization.

This book addresses students in economics, specialists in banking andfinance and others interested in improving assetts in general and, in par-ticular, portfolio of financial assets. Through, the novelty of approach andmodels, of algorithms and theoretical concepts which will be applied, webelieve that may have a significant impact on the portfolio managementdomain.

We hope that readers find this book a real support for study and researchand we welcome any message which suggests how can we improve itscontent in future editions.

Introduction

This book focuses on Portfolio Management, as an aspect of financialtheory and experimental finance, which in recent decades has receivedspecial attention from a lot of researchers and investors. Theories andconcepts from two different fields, mathematics and economics, are used.Though these two disciplines operate with different concepts and re-search paradigms, the combination of the two fields makes possible thedevelopment of financial decision–making modelling. The use of rigorousmathematical models enables more realistic optimal solutions to be ap-plied to the economics, while the new concepts which have their origins ineconomic issues enrich the mathematics. The focusis on the optimizationof financial asset portfolios.

In Chapter I, Investment decisions under uncertainty, the main concepts ofthe investment decision under uncertainty are analyzed.

In Chapter II, Risk estimation, the fundamental concepts of risk theoryare examined.

In Chapter III, Portfolio optimization using various risk measures, the mean–risk approach is reviewed, using both variance and risk measures suchas Value–at–Risk. A new risk measure, Limited Value–at–Risk (LVaR), isproposed and a new model for portfolio selection, the mean–LVaR model,is constructed, in which risk is evaluated using the LVaR risk measure.

In Chapter IV some models and methods used in the analysis of stock valuesare presented.

Chapter V, Bond financing, addresses the issue of bond financing, incorpo-rating the main characteristics of bonds, specifically the technical elements,and the ways of establishing a bond financing system.

In Chapter VI, Option transactions and strategies with options are appraised.In Chapter VII, Classical models of portfolio management, the Markowitz

model of portfolio diversification, the market’s profitability and risk securi-ties model (Sharpe) and the evaluation of financial assets CAPM model areintroduced, along with the criticism of Markowitz and CAPM models.

In Chapter VIII an algorithm for hierarchical classification, based on an ultra-metric distance is introduced and applied to the Bucharest Stock Exchange.

In Chapter IX a conceptual and methodological approach to portfolio opti-mization in the Mean–VaR framework is put forward. Finally the relationshipbetween rentability and risk for an optimal portfolio consisting of two

Introduction

risky assets and a risk–free asset is examined and applied to the case of theRomanian market.

This book is intended for students of economics, specialists in the fieldof banking finance and anyone interested in improving risk managementand, in particular, financial asset portfolio management. The book clarifiesthe fundamental concepts of risk management and provides models whichcan be used to analyze risk more effectively and to reduce the likelihood ofa failure in portfolio management.

We hope that this book will be a useful contribution to the developingfield of financial asset portfolio management and it will lead to improvedpractice within this field.

Chapter I

The investment decision under uncertainty

Introduction

Before making a decision concerning an uncertain problem we shouldbuild a functional model of assessing the level of satisfaction of the decisionmaker to whom the risk belongs. If such a functional model is obtained, thedecision problems can be solved by finding the decision which maximizesthe decision–maker’s satisfaction.

The fundamental objective of the utility theory under uncertainty isgiven by rationalizing the economic choices in risky situations in the finan-cial markets and beyond. Economics studies how people and society chooseamong options for allocating limited resources over time. The economictheory acknowledges that different consumers may have different prefer-ences, but it has little to say about the reason or cause of their existence.

There are other behavior theories providing details about the theory ofchoice, such as social sciences, psychology, political science, sociology andso as. However, there is still much to discuss about the theory of choiceunder uncertainty, for example, why a years–old person has less riskaversion than the same person on their or why some people prefer meatproducts while others prefer vegetables.

In this Chapter we intend to present the main concepts of the invest-ment decision under uncertainty: lottery, attitude towards risk, expectedutility certain equivalent, risk premium, the main types of utility functions,assesing the performance of a stock portfolio.

.. Some theoretical aspects about utility and uncertainty

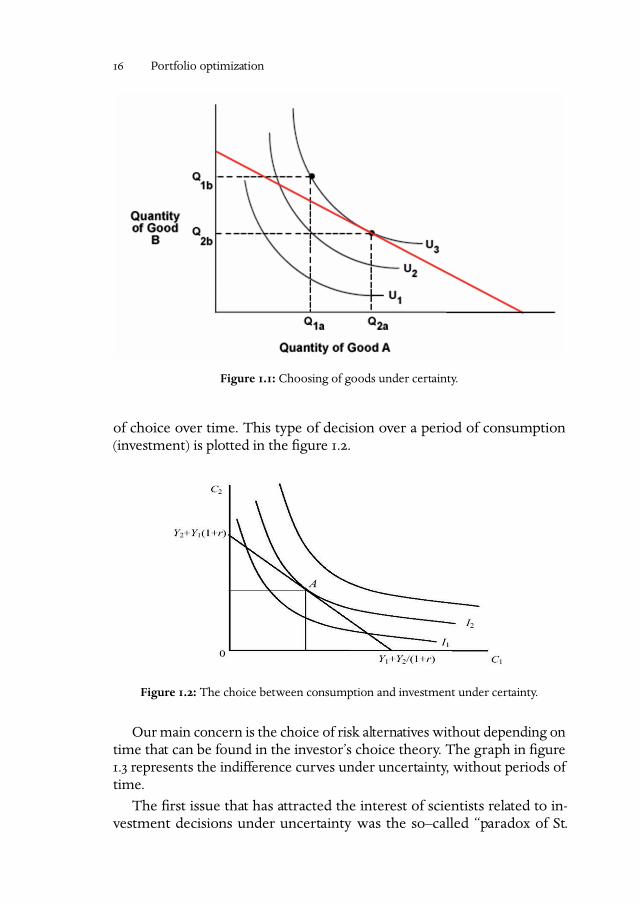

Investor choice theory is part of what came to be known as the utilitytheory. Price theory of microeconomics deals with elections made oninterchangeable goods, like apples and oranges, in the same time. Theresulting indifference curves are shown in the figure ..

Another type of choice that is available to individuals is to consume nowor to save (invest) in order to consume more at a later date. This is the theory

Portfolio optimization

Figure .: Choosing of goods under certainty.

of choice over time. This type of decision over a period of consumption(investment) is plotted in the figure ..

Figure .: The choice between consumption and investment under certainty.

Our main concern is the choice of risk alternatives without depending ontime that can be found in the investor’s choice theory. The graph in figure. represents the indifference curves under uncertainty, without periods oftime.

The first issue that has attracted the interest of scientists related to in-vestment decisions under uncertainty was the so–called “paradox of St.

. The investment decision under uncertainty

Figure .: The choice between risk and return.

Petersburg”. His statement is as follows: In a game of chance a player re-ceives a coin to be tossed until a “head” appears. If it appears at the tossnumber n, then he will pay another person a sum Sn = n− m.u. The prob-ability to have a “head” on the fist toss is ½ so to obtain a “head” on then toss is pn = (/)n. In these conditions, the expected value of this game’spayout C is:

E(C) =∞∑

n=

pn · Sn =∞∑

n=

n· n− =

∞∑

n=

=∞ (.)

The paradox is that any realistic person does not appreciate this gain tobe infinite, but to a maximum of – m.u. To resolve this paradox we needto introduce the concept of expected utility. According to this theory, anyindividual who would participate in the game doesn’t care about the gainitself, but the utility of the gain. Bernoulli, using the logarithmic function asutility function, showed that the expected utility of the gain is a finite value,around a total of m.u.

The description of an uncertain environment contains two differenttypes of information. First, it is need to list all possible outcomes. One out-come is a set of variables that influence the state of the decision maker. Theset can give a statement of one’s health, some meteorological parameters,and levels of pollution or different quantities of consumed goods.

As long as we don’t save we will assume that the result can be measuredin money, as one–dimensional unit (used at a given time). For example, let

Portfolio optimization

X be a set of possible outcomes. To avoid technical details, we assume thatthe number of outcomes is finite, so we can write:

X = {Xs}≤s≤n (.)

A second feature of an uncertain environment is probability vector forthe possible outcomes. Let

ps >

be the probability of occurring:

Xs : P(Xs) = ps (.)

Because X vector contains all possible outcomes, the following equalityis therefore:

n∑

s=

ps = (.)

Some numbers associated with the results of his actions cannot alwaysgive an appreciation of the value of these results only by measurement.There must be associated with these results other numbers, regardless ofthe results “size”, which helps providing another assessment rather than thedimensional one. Such numbers that represent the importance or usefulnessof these results are called simply “utility”.

If we define S as the set of uncertain alternatives, and on this set weinduce a binary operation “�” then the axioms underlying the rational andconsistent behavior of individuals are:

Axiom .. For any two entities x, y ∈ S one and only one of the followingsituation always occurs: x � y, y � x, x ∼ y. The binary relation � defines thefollowing cases:

x � y : x is preferred to y (.)y� x : y is preferred to x (.)x ∼ y : entity x or y is indifferent (.)

Axiom .. If x � z and z� y then x � y. We say that the preference relation istransitive.

Axiom .. If x � y, then x � (x,α, y, − α) for any α ∈ (, ). This means thatx is preferred to any experiment or lottery that includes x and y.

. The investment decision under uncertainty

Axiom . carries the name of the substitution axiom and it can be gener-ally reformulated like this: for all x, y, z be three alternatives so x � y and forall α ∈ (, ], then:

αx + (− α)z� αy + (− α)z (.)

This axiom states that if an alternative x is preferred to another y, thenany alternative made from a combination of x and a third alternative z ispreferred to an alternative made from a combination of y and z in the sameproportions as before.

Axiom .. “Archimedean axiom”. For all alternatives x, y, z ∈ S, if x � y� zthen there is α,β ∈ (, ) so:

αx + (− α)z� y�βx + (−β)z (.)

In other words, whatever the three different risky x, y, z in descendingorder of preference, then there are two proportions that variants x and zcan be combined in order to obtain two alternatives, one preferred to y andone not.

These are the main axioms underlying cardinal utility theory. On themit was built scaffolding, culminating in efficient capital market theory andmodels for assets valuation in those markets.

The four axioms are the foundation of financial theory of capital markets,because the relation of preference as described by them can conduct to acardinal utility function which we denote U.

Function U is a utility function if the following conditions are met:

. ∀x, y,∈ S , if x � y, then U(x) > U(y) (utility is monotonically increas-ing against preference);

. ∀x, y,∈ S and ∀α ∈ [, ] ,then:

U[αx + (− α)y] = αU(x) + (− α)U(y) (.)

(utility of an alternative equals the average of utilities for all possibleoutcomes of this alternative).

Also, if U is an utility function and V(t) = at + b, a > is a linear function,then the compound function V◦U is also an utility function. To demonstratethis important property, let’s first notice that the compound function V ◦Ulooks like this:

V(U(t)) = aU(t) + b (.)

Portfolio optimization

Now let x, y ∈ S with x � y. Since U is an utility function, we haveU(x) > U(y), we obtain:

aU(x) + b > aU(y) + b⇒ V(U(x)) > V(U(y)) (.)

Let’s consider now x, y ∈ S and Sα ∈ [, ]. We obtain:

V[U(αx+(−α)y)] = aU[αx+(−α)y]+b = a[αU(x)+(−α)U(y)]+b (.)

Processing relationship () results:

V[U(αx+(−α)y)] = α[aU(x)+b]+(−α)[aU(y)+b] = αV(U(x))+(−α)V(U(y))(.)

From relations () and () we deduct that application V meets all theconditions to be an utility function.

.. Risk in the assets portfolio

... General considerations

Defining risk is not an easy task in terms of qualitative and quantitativeapproaches determined by this subject. Thus, we find the concept of riskexplained by various keywords.

Finance – guide proposed by The Economist Books, defines risk as thepossibility of loss. For assumed risks, investors obtain a benefit. Generally,the greater the risk is, the greater the benefits are. Investors who remainsecure (for example, by buying only government bonds) are said to haverisk aversion.

Paul Halpern, J. Fred Weston, Eugene F. Brigham in Managerial Financedefine the risk of an asset as the possible variation of the future return ofthe asset.

Dictionary of ergonomics, author Constantin Rosca, defines risk as thepossibility of occurrence of some less known or unknown circumstanceswithin an activity or action, having adverse effects on the possible results(positive or negative) and on those expected from a future action, subject tothe influence of random factors.

The explanatory dictionary of the Romanian language defines risk as prob-ability of getting into trouble, having to face a problem or to bear a loss;potential peril.

![Apprendimento Automatico: Apprendimento per Rinforzo Roberto Navigli Apprendimento Automatico: Apprendimento per Rinforzo Cap. 13 [Mitchell] Cap. 21 [Russel.](https://static.fdocumenti.com/doc/165x107/5542eb4f497959361e8beef6/apprendimento-automatico-apprendimento-per-rinforzo-roberto-navigli-apprendimento-automatico-apprendimento-per-rinforzo-cap-13-mitchell-cap-21-russel.jpg)

![Rob-Intro-09-10.ppt [modalità compatibilità] - RobIntro.pdf · • Lung-Wen Tsai [Univ. of Maryland, MD] “R b t A l i ”“Robot Analysis ...](https://static.fdocumenti.com/doc/165x107/5b5ba3e27f8b9a2d458e1145/rob-intro-09-10ppt-modalita-compatibilita-lung-wen-tsai-univ-of.jpg)