Crowdfunding birmingham. Massimo Colombo

38

Making a successful crowd-funding campaign: The role of social capital Massimo G. Colombo, Politecnico di Milano School of Management [email protected] ERC Understanding Small Business Growth Conference Birmingham, February 11 th , 2015

-

Upload

enterpriseresearchcentre -

Category

Business

-

view

74 -

download

0

Transcript of Crowdfunding birmingham. Massimo Colombo

Making a successful crowd-funding campaign:

The role of social capital

Massimo G. Colombo, Politecnico di Milano School of

Management

ERC Understanding Small Business Growth

Conference Birmingham,

February 11th, 2015

Outline of the talk

•WHAT WE KNOW ABOUT CROWDFUNDING

Definition of crowdfunding

Neighbouring phenomena

Crowdfunding @ Politecnico di Milano School of Management

•FACTORS THAT DETERMINE THE SUCCESS OF A

CROWDFUNDING CAMPAIGN: THE ROLE OF SOCIAL CAPITAL

Colombo M.G., Franzoni F., Rossi-Lamastra C. (2015) Internal

social capital and the attraction of early contributions in

crowdfunding projects. Entrepreneurship Theory and Practice, 39

(1), pp. 75-100

2

INTRODUCTION TO

CROWDFUNDING

3

Definition of crowdfunding

Crowdfunding involves an open call, mostly through dedicated

platforms on the Internet, for the provision of financial resources, either

in form of donation or in exchange for the future product or some form

of reward (Belleflamme, Lambert, & Schwienbacher, 2014, JBV)

•Open call: I wish to develop an entrepreneurial project/idea and I ask

for money on the Internet

•The evolution of an ancient practice, made possible by Web 2.0

•Often projects have a philanthropic content …

•… But crowdfunding is increasingly used to finance entrepreneurial

ventures and start-ups

Use of a dedicated platform: specific benefit from network effects and

dedicated services offered by the platform

•Financial resources: proponents receive more than money

Comments and suggestions to fine-tune their projects

4

What crowdfunding is not:

Neighbouring phenomena

Crowdfunding is part of a larger trend: involvement of users in innovation

processes (von Hippel, 2005)

Neighbouring phenomena:

•Crowdsourcing: firms asking Internet users for ideas and solutions to be

used in their innovation processes (Afuah and Tucci, 2012)

Crowd-science: scientists asking Internet users to contribute to scientific

projects in a decentralized way (Franzoni and Sauermann, 2014)

Open Source production: decentralized production of intangible and

tangible goods by developers who coordinate through the Internet

•Main phenomenon: Open Source Software (e.g., Linux, Apache)

•But also: Wikipedia, Local Motors (https://localmotors.com/) , …

5

Crowdfunding models

Types of crowdfunding platforms:

•Equity-based platforms: underwriting by the crowd of the risk

capital issued by a company

•Donation-based platforms: project funding motivated by

philanthropy or sponsorship, without any other remuneration for

crowdfunders

•Lending-based platforms: underwriting of debt contracts between

two parties (i.e., the lender and the borrower)

•Reward-based platforms: financing is provided in the expectation

of a rewards or a prize (material or not).

6

… And crowdfunding in Italy

7

8

Follow as on Facebook:

Entrepreneurship, Finance & Innovation at SoM POLIMI:

https://www.facebook.com/EntInno.PoliMI

•The Crowdfunding Observatory @ Politecnico di Milano School

of Management monitors the evolution of the crowdfunding industry

in Europe. It collects data on

Platforms and firms running these platforms

Projects and proponents

Crowdfunding @ Politecnico di Milano School

of Management

9

Researching crowdfunding @ Politecnico di

Milano School of Management

• What determines the success of a (reward) crowdfunding

campaign?

• Proponents’ reputation and human capital

• Use of content analysis to check the role of proponents’ optimism and

charisma

• The role of proponents’ social capital

• The geography of crowdfunding

• Why in some geographic areas there are many crowdfunding projects while

in other areas just a few projects are launched?

• Does the localisation of the proponent influences success?

• Mapping the crowdfunding industry in Europe

Role of newly created and incumbent firms (i.e., crowdfunding players) that

created and run crowdfunding platforms

9

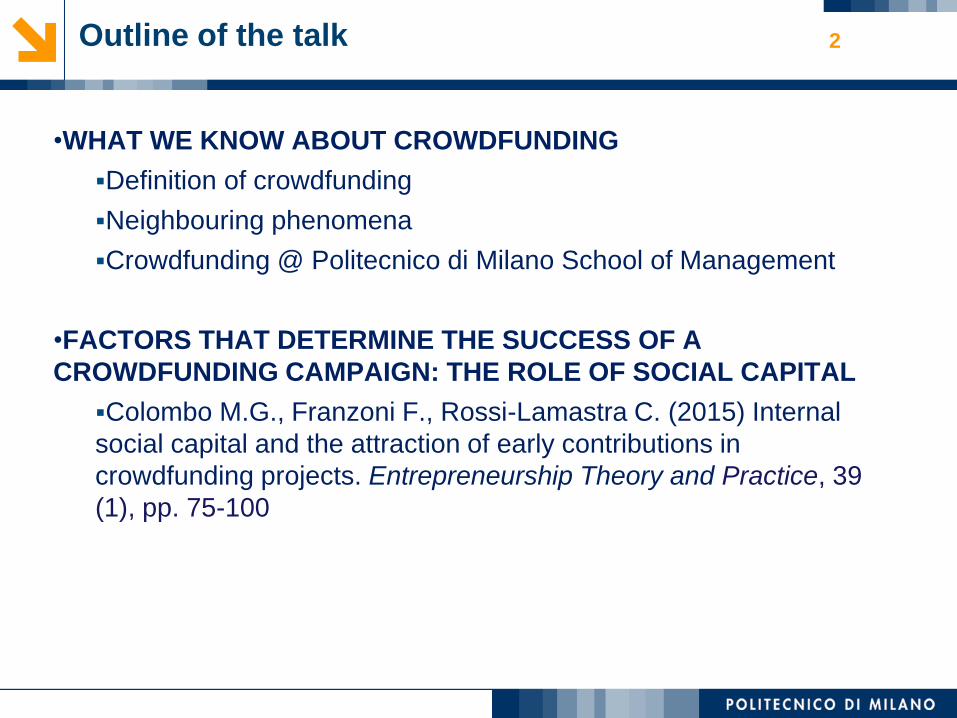

• Dushnitsky, G., Guerini, M., Piva, E., Rossi-Lamastra, C.,

The entry of crowdfunding players in the financial service

industry: the European case, Politecnico di Milano School of

Management Working Paper

Main results

• As of 2013, in the EU-15 countries there were 414 active

crowdfunding players

330 are de novo entrants, 84 are de alio entrants

40 players exited the market

The Crowdfunding Observatory:

Crowdfunding in Europe

7

• Number of active crowdfunding players active at the end of 2013 and

number of players per million of residents

• Players entering and exiting the crowdfunding segment per year

Crowdfunding in Europe:

Active players in EU-15 countries

7

•There are differences

across countries which are

not entirely explained by

population size

•Most players entered after

2010

•Exit is still a marginal,

though growing

phenomenon

• De novo entrants:

• are more numerous than de alio entrants: low entry costs and novelty

• are negatively associated with the strength of the financial service

industry

• De alio entrants:

• are positively associated with the number of crowdfunding platforms:

wait and see approach

Crowdfunding in Europe:

De novo and de alio entrants at the end of 2013

7

Internal social capital and the attraction of early

contributions in crowdfunding (CF)

Massimo G. Colombo, Chiara Franzoni, Cristina Rossi-Lamastra

The paper in a nutshell

• Aim: determinants of the early success of CF projects

Early contributions known to be crucial to lead to final success

• Empirical setting: crowdfunding projects on Kickstarter.com

4 classes: design, technology, film & video, videogames

• Theoretical lens/ Focus: Social Capital

Prior work documented the role of external social capital, i.e.

personal relationships (F&F, Facebook contacts) that

individuals have or not have independently of the

crowdfunding initiative

Focus on the social capital that the proponent establish within

the crowdfunding platform (internal social capital)

14

CONCEPUTAL BACKGROUND

15

Dynamics of CF: Role of early contributions

Regularity in the dynamics of CF projects

Contributions received at the outset of a crowdfunding project largely

anticipate success (Agrawal et al., 2014)

•Why are early contributions (both headcounts of backers and capital

pledged early in project life) so important?

•At the outset of a crowdfunding project there is high uncertainty

about the

quality of the project

ability of proponent

Moreover, the project still is in a fluid state

16

Early contributions

Early contributions enable

1. Observational learning: when quality of projects is uncertain,

evidence of support from others functions as a signal of quality and

triggers imitation and herding behavior (Bikhchandani et al., 1998)

2. Word of mouth: early backers function as a marketing channel,

because they talk (or tweet) to other ‘potential’ backers

3. Feedback: CF platforms are a powerful development tool. A project

gets developed during the lifetime of the campaign and eventually

consolidate to meet needs of a broader customer base. More feedback in

early days means faster consolidation

Remains to be explained what triggers early contributions.

Social capital?

17

Social capital and early contributions

Social capital has been documented to be associated to project

contributions and success

The relevance of social capital that proponents have outside the

crowdfunding platform is documented in prior studies

Family & friends (Agrawal et al., 2011)

Facebook contacts (although not having Facebook is better than

having few Facebook contacts) (Mollick, 2013)

We call this EXTERNAL SOCIAL CAPITAL

This evidence is consistent with that of the entrepreneurial finance

literature (friend-funding phase)

•Social ties help overcome information asymmetries in the funding

phase (e.g. not having social ties makes it less likely to receive seed-

capital, Shane & Cable, 2002; Shane, 2009)

18

Internal social capital (1/2)

Proponents of can also rely on a second source of social capital,

which is created internally within the CF community

•Proponents develop social ties inside the CF platform by interacting

with other proponents

E.g. giving attention, money, feedback and visibility to the projects

of others

We call this INTERNAL SOCIAL CAPITAL

•Internal social capital attracts early contributions because it triggers

pro-social behavior in the form of obligation of reciprocity (Coleman,

1990)

19

Internal social capital (2/2)

In the realm of CF, reciprocity can happen in two ways

1. Specific reciprocity

“I help you because I want to show my gratitude for helping me in the

past” (Putnam, 1995)

2. Generalized reciprocity

“Regardless of whether or not you helped me, I help you because I

want to be a helping person/a good member of this community”

(Portes, 1998)

It is a social norm in the CF community: Members of the

community are prone to help because:

• They were helped in the past;

• They expect to be helped in the future.

20

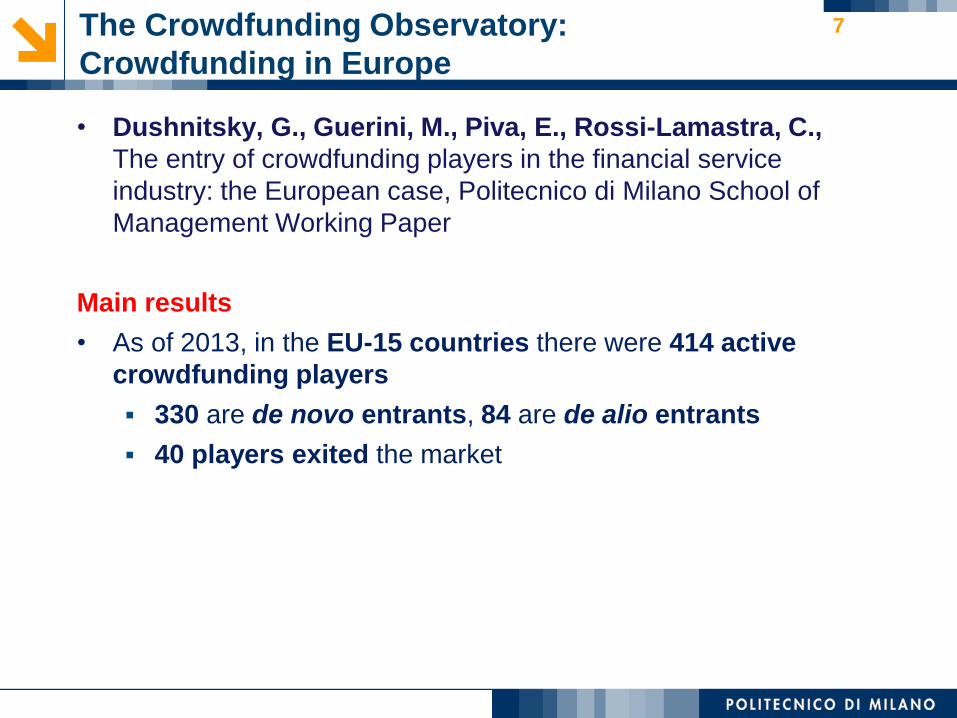

Research hypotheses

H1: Internal social capital is positively associated with the amount of

early capital raised by CF projects

H2: Internal social capital is positively associated with the number

of early backers of CF projects

The association of internal social capital and early contributions may

be non-linear or even become negative after a threshold (reversed-U

shaped)

Too much internal social capital is less beneficial or may even be harmful

due to excess cohesion or homologation

H3: Internal social capital is positively associated with the success of

CF projects, but the association is mediated by the number of

early backers and the amount of early capital. Its impact fades

when the amplifying mechanisms are set in place

21

The model

earlybackers

earlycapital

success/ failure

22

INTERNAL SOCIAL CAPITAL

H1

H2

H3

success/ failure

EMPIRICAL ANALYSIS

23

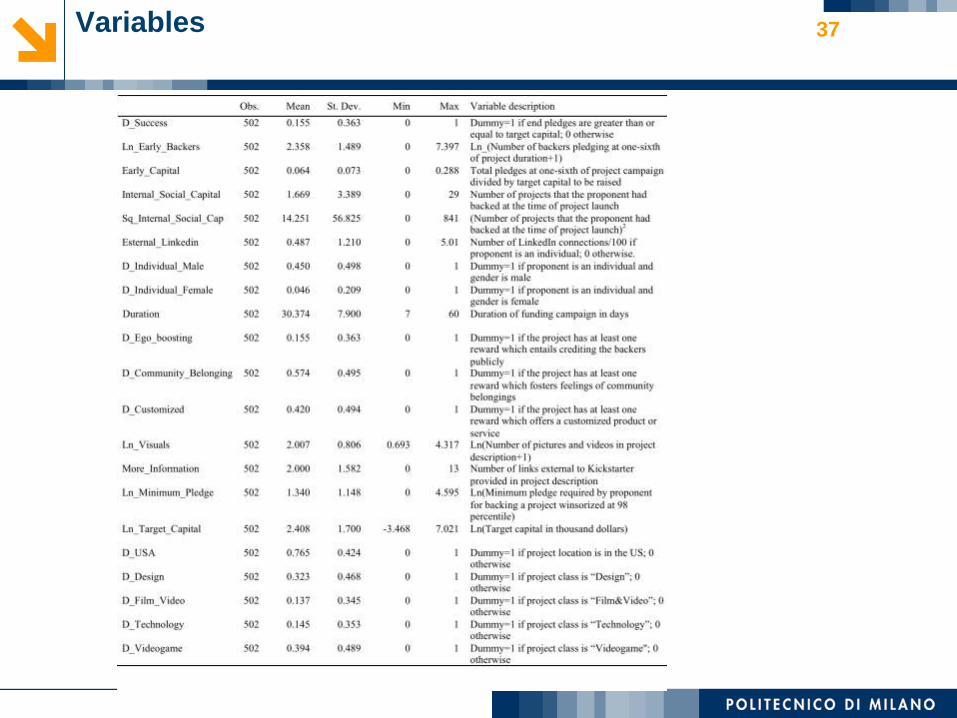

The sample and the variables (1/2)

Empirical analysis based on 669 crowdfunding projects on Kickstarter

• In design, technology, film & video, and videogames

• Posted since October 20, 2012 and closed by January 10, 2013

• Early contributions: conventionally observed at 1/6 of total campaign

duration.

Most projects span 30 days: this definition considers early the

capital and the backers coming in the first 5 days after the start

24

The sample and the variables (2/2)

Rate of success: 37.4%

About 11% of project quit before reaching the deadline

25

Empirical strategy

- Show the amplifying mechanisms

- Model impact of internal social capital on early capital (H1)

- Model impact of internal social capital on early backers (H2)

- Model impact of internal social capital on success with or without

early capital and early backers (H3)

Pi =fAi + dBi+ gISCi+ gECi + ei

Pi success (1;0)

Ai vector of project characteristics (pj class, US/non-US, duration of campaign, target

capital, minimum pledge, number of visuals (video & images), number of links to external

websites, reward types (ego-boosting, community-belonging, customized rewards)

Bi vector of individual proponent characteristics (company/individual; individualXgender;

individualXnumber of linkedin connections);

ISCi = number of projects backed by the proponent at the time of launching the

project

ECi Early Capital = % of total capital collected at 1/6 of pj campaign

EBi Early Backers = log(number of backers at 1/6 of pj campaign)

26

Models: Amplifying mechanism 27

Robust probit

• Both early backers and

early capital have

positive impact on

success

• Impact of early capital

is stronger

• 1s EB = +83%

likelihood of success

• 1s EC = +133%

likelihood of success

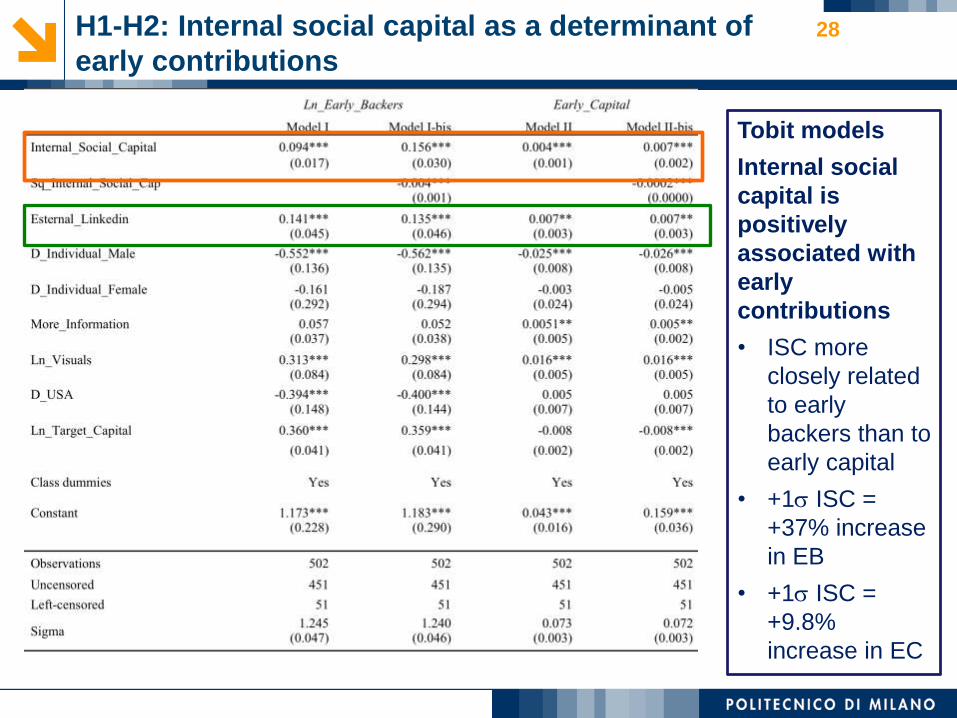

H1-H2: Internal social capital as a determinant of

early contributions28

Tobit models

Internal social

capital is

positively

associated with

early

contributions

• ISC more

closely related

to early

backers than to

early capital

• +1s ISC =

+37% increase

in EB

• +1s ISC =

+9.8%

increase in EC

H3 Determinants of early contributions 29

Homologation/

less divergent

thinking?

ISC^2 exhibits a

negative

coefficient

However,

inflection point

is at a level of

ISC links which

corresponds to

more than 99%

of the sample

H3 Early contributions are a mediator of

internal social capital30

Rob. Probit

Dep Var:

1=success;

0=failure

ISC is a predictor

of project success,

but the number of

early backers and

the percentage of

target capital

raised early fully

mediate this

relationship (they

capture 65% of

total effect)

Assess magnitude/ statistical significance

of the mediation effect

Product of coefficient approach (Sobel, 1982; MacKinnon & Dwyer,

1993).

•Because final dependent variable is dichotomous, we used the Stata

command binary_mediation (Ender, 2006), which allows for

dichotomous dependent variables and multiple mediators

Confidence level are computed through Bootstrapping

Total effect of Internal_Social_Capital on the likelihood of

success=0.189**

Total indirect effect =0.123**

Direct effect=0.067 not significant (half than total)

31

Conclusions

What determines the success of a newly-launched CF project?

•Internal social capital triggers social behavior because of specific and

generalized reciprocity

•This attracts early contributions in the form of capital pledged and

headcounts of backers, despite high uncertainty

Observational learning, word of mouth, and feedback from early

contributions do the rest

•Once these mechanisms are in place, the impact of internal social

capital vanishes

Implications for investigating CF

•CF platforms are a collective where social capital formation takes place

•Because of the amplifying mechanism/success-breeds-success

mechanism, the determinants of success of CF are best visible/should be

investigated in the early days of a campaign

32

Crowdfunding @POLIMI

THANK YOU!

33

ADDITIONAL SLIDES

PAPER

APPENDIX

35

36Distribution of total capital pledged at

closure

Truncated at 500000$

37Variables

38VIF

Truncated at 90^th centile