23 maggio 2013 – Sezione di controllo per gli Affari...

57

Deliberazione n.4/2013. Certificazione bilancio CERN. SEZIONE DI CONTROLLO PER GLI AFFARI COMUNITARI ED INTERNAZIONALI IL COLLEGIO PER L’ATTIVITA’ DI CONTROLLO SUL CERN composto dai Magistrati: Dott. Giuseppe COGLIANDRO Presidente Dott. Michele COSENTINO Consigliere Dott. Carlo MANCINELLI Consigliere Vista la decisione del 29 marzo 2011 del Consiglio di Presidenza con la quale è stato deliberato di affidare alla Sezione di controllo per gli affari comunitari ed internazionali l’organizzazione delle funzioni di “External auditor” presso il CERN; Vista l’ordinanza n. 2/2012 con la quale è stato istituito, nell’ambito della suddetta Sezione, un apposito Collegio per la citata attività di revisione; Visti i principi INTOSAI; Visti i principi internazionali di Audit applicabili all’attività di certificazione dalle Istituzioni Superiori di Controllo (International Standards of Supreme Audit Institutions – ISSAI), richiamati dalla Dichiarazione di Lima; Visti i principi internazionali di Audit (International Standards on Auditing - ISA) emessi dall’International Auditing and Assurance Standards Board (IAASB), organo dell’ International Federation of Accountants (IFAC); Visti i principi contabili internazionali per il settore pubblico (International Public Sector Accounting Standards - IPSAS) che richiamano i principi contabili internazionali (International accounting standards – IAS); Viste le determinazioni assunte dall’apposito Collegio nella seduta del 23 maggio 2013 in merito alle risultanze dell’attività istruttoria concernente l’esame del bilancio del CERN chiuso al 31 dicembre 2012; Considerato concluso il relativo “financial audit”

-

Upload

trinhduong -

Category

Documents

-

view

217 -

download

0

Transcript of 23 maggio 2013 – Sezione di controllo per gli Affari...

Deliberazione n.4/2013. Certificazione bilancio CERN.

SEZIONE DI CONTROLLO PER GLI AFFARI COMUNITARI ED INTERNAZIONALI

IL COLLEGIO PER L’ATTIVITA’ DI CONTROLLO SUL CERN

composto dai Magistrati:

Dott. Giuseppe COGLIANDRO Presidente

Dott. Michele COSENTINO Consigliere

Dott. Carlo MANCINELLI Consigliere

Vista la decisione del 29 marzo 2011 del Consiglio di Presidenza con la quale è

stato deliberato di affidare alla Sezione di controllo per gli affari comunitari ed

internazionali l’organizzazione delle funzioni di “External auditor” presso il CERN;

Vista l’ordinanza n. 2/2012 con la quale è stato istituito, nell’ambito della

suddetta Sezione, un apposito Collegio per la citata attività di revisione;

Visti i principi INTOSAI;

Visti i principi internazionali di Audit applicabili all’attività di certificazione dalle

Istituzioni Superiori di Controllo (International Standards of Supreme Audit Institutions –

ISSAI), richiamati dalla Dichiarazione di Lima;

Visti i principi internazionali di Audit (International Standards on Auditing - ISA)

emessi dall’International Auditing and Assurance Standards Board (IAASB), organo

dell’ International Federation of Accountants (IFAC);

Visti i principi contabili internazionali per il settore pubblico (International Public

Sector Accounting Standards - IPSAS) che richiamano i principi contabili internazionali

(International accounting standards – IAS);

Viste le determinazioni assunte dall’apposito Collegio nella seduta del 23

maggio 2013 in merito alle risultanze dell’attività istruttoria concernente l’esame del

bilancio del CERN chiuso al 31 dicembre 2012;

Considerato concluso il relativo “financial audit”

DELIBERA

la certificazione - secondo i principi INTOSAI di legalità, regolarità e affidabilità - degli

atti contabili del bilancio del CERN chiuso al 31 dicembre 2012 “Annual Accounts

(Financial Statements) 2012” sulla base dell’allegata relazione riguardante: la

comparazione del budget con le relative entrate e uscite effettive (Statement of

comparison of budget and actual amounts); lo stato patrimoniale (Statement of

financial position); il conto economico (Statement of financial performance); il

rendiconto dei flussi di cassa (Cash-flow Statement) e relative note esplicative.

Roma 23 maggio 2013

IL PRESIDENTEF.to Giuseppe Cogliandro

F.to Consigliere Michele Cosentino (relatore)

F.to Consigliere Carlo Mancinelli

Depositata in Segreteria il 18 luglio 2013

Il Dirigente

F.to Maria Teresa Macchione

CERN/FC/5740 CERN/3064 Original: English 1 June 2013

ORGANISATION EUROPEENNE POUR LA RECHERCHE NUCLÉAIRE

CERN EUROPEAN ORGANIZATION FOR NUCLEAR RESEARCH

Action to be taken Voting Procedure

TAKE NOTE

FINANCE COMMITTEE

344th Meeting 19 June 2013

-

TAKE NOTE

COUNCIL

167th Session 21 JUNE 2013

-

Report by the External Auditors

on the Financial Statements of CERN for the Financial Year 2012

Report from the Italian Court of Auditors

CERN/FC/5740 i CERN/3064

Report by the External Auditors on the Financial Statements of CERN for the Financial Year 2012

TABLE OF CONTENTS

1. INTRODUCTION ............................................................................................. 1 2. AUDIT CERTIFICATE .......................................................................................... 2 3. ENFORCEMENT OF IPSAS ............................................................................... 4 4. 2012 BUDGET OUT-TURN ................................................................................ 4 4.1 Budget and actual Amounts ..................................................................................... 5

4.1.1 Total expenses .......................................................................................................... 5

4.1.2 Total revenue ......................................................................................................... 7

4.2 Net Accounting Deficit ............................................................................................. 7

5. STRUCTURE OF THE ACCOUNTING STATEMENTS .................................. 9 6. STATEMENT OF FINANCIAL POSITION 2012 ............................................ 10 6.1 Assets ...................................................................................................................... 10

6.1.1 Non-current Assets .............................................................................................. 10

6.1.2 Current Assets ..................................................................................................... 20

6.2 Liabilities and Net Assets ....................................................................................... 22

6.2.1 Net Assets ........................................................................................................... 22

6.2.2 Non-current liabilities ......................................................................................... 23

6.2.3 Current liabilities ................................................................................................ 25

7. STATEMENT OF FINANCIAL PERFORMANCE 2012 ................................. 27 8. STATEMENT OF CHANGES IN NET ASSETS 2012 .................................... 28 9. STATEMENT OF NET DEFICIT & LOSSES RECOGNIZED DIRECTLY IN NET ASSETS ...................................................................................................................................... 29

10. CASH FLOW STATEMENT 2012 .................................................................... 29 11. INTERNAL AUDIT SERVICE ......................................................................... 30 12. FOLLOW-UP OF RECOMMENDATIONS 2006 - 2011 ................................ 31 ANNEX 1 ..................................................................................................................... 32

CERN/FC/5740 1CERN/3064

1. INTRODUCTION

The legal basis for the audit carried out by the External Auditors is given in the Financial Protocol annexed to the Convention for the establishment of a European Organization for Nuclear Research of 1 July 1953, as modified on 17 January 1971 and in the Financial Rules as approved by the Council (Rule 11 — Audit — and Annex II —Auditors).

After the transition of the accounting and financial statements to IPSAS, the revision of the current rules governing CERN's financial administration (Financial Rules and Internal Financial Regulations) was approved by the Council on 12 December 2008 and article 21 has been dedicated to External Auditors.

We have carried out the audit of the accounts for the Financial Year 2012 based on INTOSAI standards and, in particular, on IPSAS regime.

We have planned the working activities according to our audit strategy to obtain a reasonable assurance that the Financial Statements are free from material misstatement.

We have tested, on a sample basis, a number of transactions and relevant documentation and we have obtained sufficient and reliable evidence in relation to the accounts and disclosures in the Financial Statements.

We have evaluated the accounting principles and related estimates made by Management and we have assessed the adequacy of the presentation of information in the Financial Statements.

Thus, we have obtained through the audit a sufficient basis for the opinion given below.

A Letter of Representation referring to the Accounts for the Financial Year 2012, signed by the Director of Administration and General Infrastructure and the Head of Finance, Procurement and Knowledge Transfer Department, was handed over and it is an integral part of the audit documentation.

2 CERN/FC/5740 CERN/3064

2. AUDIT CERTIFICATE

2.1 Independent Auditor’s Report

We have audited the financial statements at 31 December 2012 of the European

Organization for Nuclear Research (CERN), comprising the Statement of financial

position, the Statement of financial performance, the Statement of net deficit and gains

and losses recognized directly in net assets, the Statement of changes in net assets, the

Statement of comparison of budget and actual amounts and the cash-flow Statement

for the year ending on that date, as well as a summary of the main accounting policies

and other explanatory notes.

2.2 Responsibility of the CERN Director-General for the financial statements

It is the responsibility of the Director-General to draw up and faithfully present the

financial statements in line with the requirements laid down in the International Public

Sector Accounting Standards (IPSAS) and in the CERN Financial Rules and

Regulations. Furthermore, the Director-General is responsible for designing,

implementing and maintaining the internal control system as it deems necessary to

ensure the preparation and fair presentation of financial statements that are free from

material misstatement, whether as a result of fraud or errors.

2.3 Responsibility of the auditor

It is our responsibility to express an opinion on CERN's financial statements based on

our audit. We conducted our audit in accordance with the International Standards of

Supreme Audit Institutions, published by International Organization of Supreme Audit

Institutions (INTOSAI). Those standards require us to comply with ethical

requirements, and to plan and perform the audit in such a way as to obtain reasonable

assurance that the financial statements are free from material misstatement.

Audit involves performing procedures to gather evidence attesting about the amounts

and the data provided and disclosures in the financial statements. The choice of

procedures is left to the discretion of the auditor, including assessment of the risk of

material misstatement of the financial statements, whether due to fraud or errors. In

making those assessments, the auditor considers internal control system in place in the

entity for preparation and fair presentation of the financial statements, in order to

determine audit procedures that are appropriate in the circumstances, but not with the

aim of expressing an opinion on the efficient functioning of the entity's internal control

CERN/FC/5740 3CERN/3064

system. Audit also includes assessment of the validity of the accounting methods

adopted and of whether the accounting estimates made by the Director-General are

reasonable, as well as appraisal of the overall presentation of the financial statements.

We believe that the evidence obtained provides a sufficient and appropriate basis for

our opinion.

2.4 Opinion

In our opinion, the financial statements present fairly, in all essential points, the

financial position of CERN as at 31 December 2012, and its financial performance, the

net deficit and gains and losses recognized directly in net assets, the changes in net

assets, the comparison of budget and actual amounts and the cash-flow, in accordance

with IPSAS and the CERN Financial Rules and Regulations. We have also issued a

detailed report, dated 24 May 2013, on our audit of the financial statements.

Without qualifying our opinion, we draw the Council’s attention to the fact that the

Statement of Financial Position shows a negative Net Assets (-2.554.351.000 CHF)

due to the impact of gains and losses recognized directly in Net Assets of -219.453.000

CHF, mainly originated by provisions for actuarial liability for post-employment

benefits totalling 8.776.079.000 CHF (5.318.737.000 CHF for Pension Scheme and

3.457.342.000 CHF for Health Insurance Scheme). Details of our analysis are included

in our report.

Remedial measures are urgent and necessary and Management is monitoring the

effectiveness of the measures submitted by the Management to the Council and

approved in December 2010. Management has assured us that it will continue to

monitor these and will adapt them should a change in situation arise. We would like to

point out that remedial measures also depend on unforeseeable events, for instance,

developments on the investment markets.

f. y. ending 31 December 2012

Rome 24 May 2013

Michele Cosentino Giuseppe Cogliandro

External Auditors of the Italian Court of Auditors

4 CERN/FC/5740 CERN/3064

3. ENFORCEMENT OF IPSAS

Regarding the financial year 2012, from the analysis of the annual accounts and

following interviews with the CERN Management, we conclude that IPSAS have been

correctly implemented by the CERN Management. IPSAS 28, 29 and 30 relating to

Financial Instruments that will become effective in 2013 are not the subject to early

adoption by the Management, as stated in Note 1.7 of the Annual Accounts.

Last year we recommended a full implementation of IPSAS 20 “Related Party

Disclosures”. We acknowledge the fact that Management, following this

recommendation, has inserted this year an additional Note (Note 28) in the 2012

Financial Statements.

However, we consider that the requirements of IPSAS 20 are wider than what has been

stated in the Note of the 2012 CERN annual accounts. While almost all the IPSAS 20

requirements have been addressed in Note 28, we consider the disclosure could be

improved with additional information regarding related party relationships and

transactions between key management personnel and external parties. We refer

specifically to IPSAS 20.15 and more generally to IPSAS 20.27-20.28. We therefore

recommend to the Management to enhance their related party information collection

and reporting for the purpose of accountability.

4. 2012 BUDGET OUT-TURN

The table "Statement of Comparison of Budget and Actual Amounts" is compliant

with IPSAS 24 which requires a comparison of budget amounts and actual

amounts arising from execution of the budget to be included in the Financial

Statements.

The Standard also requires disclosure of the reasons for material differences

between budget and actual amounts.

With respect to this, we acknowledge that our recommendations issued last year

have been implemented by the Management and we have closed them in the table

of Annex 1.

CERN/FC/5740 5CERN/3064 4.1 Budget and Actual Amounts

4.1.1 Total expenses

In 2012 the difference between budget expenses (1.165,9 MCHF) and the actual

amounts of the expenses (1.078,6 MCHF) resulted in a reduction of 87,3 MCHF

(-7.5 %). As regards expenses, we observed that the deviation from the budgeted

amounts is due to i) a considerable decrease in materials expenses (-16.9%), mainly

due to the re-profiling of multi-annual scientific projects and to the delays in

procurement ii) an increase in the actual amount of the personnel expenses of 5,2

MCHF equal to an increase of +0.88 (in year 2011, personnel increased of 15,2

MCHF, equivalent to +2,7% and in 2010 increased of +9,9 MCHF equal to +1,9%) –

mainly due to the implementation of the 5 yearly review - and iii) the increase in

Interest and Financial Costs expenses (+2,2 MCHF equivalent to +14.7%, meanwhile

in 2011 the increase in financial cost expenses was equivalent to +0,9 MCHF; +5,3%).

Personnel expenses

The Personnel expenses amounted to 594,6 MCHF compared to 574,3 MCHF in

2011, with a rise of 20 MCHF (+3.5%).

The total number of staff members in post at year-end reduced from 2.544 in 2007

to 2.400 in 2008 and, subsequently, to 2.377 in 2009. During financial year 2010,

Personnel increased to 2.427 staff members in post (+2,1%), explaining the 2010

increase in expenses of +4,4%.

In 2011, the total number of staff members in post slightly decreased to 2.424 (-3

units) but, as stated above, the personnel expenses of last year increased by 36,2

MCHF comparing to 2010 (+6,9%).

In 2012, the total number of staff members in post increased to 2.512 (+ 88 units,

equivalent to 3,6%) and this partly explains the rise in the personnel expenses of

20 MCHF comparing to 2011 (+3,5%), as stated above.

Staff members in post on 31 December 2012 (2.512) is slightly lower with respect to

31 December 2007 number of staff in post (2.544), but higher than the number of

staff from 2008 (2.400) till 2011. However, since 2007, personnel expenses (which

include basic salaries and overheads) have increased more than the personnel

component of the Cost-Variation Index (CVI). The following table represents an

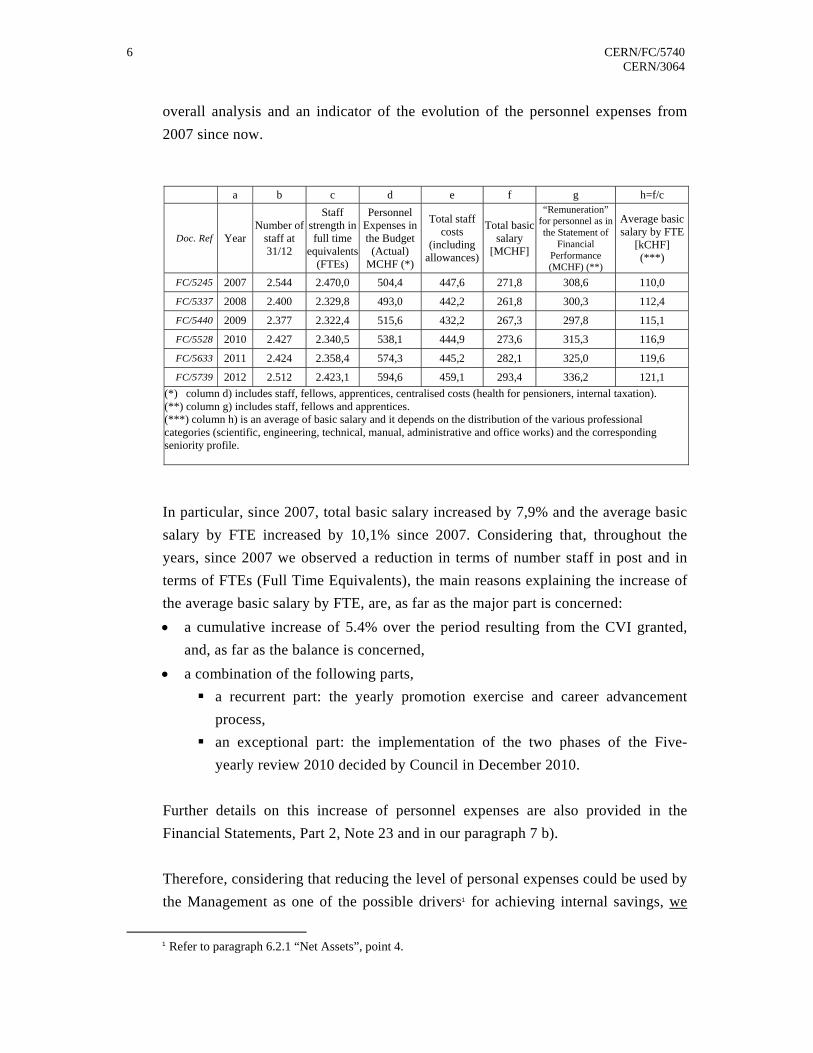

6 CERN/FC/5740 CERN/3064

overall analysis and an indicator of the evolution of the personnel expenses from

2007 since now.

a b c d e f g h=f/c

Doc. Ref Year Number of

staff at 31/12

Staff strength in full time

equivalents (FTEs)

Personnel Expenses in the Budget

(Actual) MCHF (*)

Total staff costs

(including allowances)

Total basic salary

[MCHF]

“Remuneration” for personnel as in the Statement of

Financial Performance (MCHF) (**)

Average basic salary by FTE

[kCHF] (***)

FC/5245 2007 2.544 2.470,0 504,4 447,6 271,8 308,6 110,0

FC/5337 2008 2.400 2.329,8 493,0 442,2 261,8 300,3 112,4

FC/5440 2009 2.377 2.322,4 515,6 432,2 267,3 297,8 115,1

FC/5528 2010 2.427 2.340,5 538,1 444,9 273,6 315,3 116,9

FC/5633 2011 2.424 2.358,4 574,3 445,2 282,1 325,0 119,6

FC/5739 2012 2.512 2.423,1 594,6 459,1 293,4 336,2 121,1

(*) column d) includes staff, fellows, apprentices, centralised costs (health for pensioners, internal taxation). (**) column g) includes staff, fellows and apprentices. (***) column h) is an average of basic salary and it depends on the distribution of the various professional categories (scientific, engineering, technical, manual, administrative and office works) and the corresponding seniority profile.

In particular, since 2007, total basic salary increased by 7,9% and the average basic

salary by FTE increased by 10,1% since 2007. Considering that, throughout the

years, since 2007 we observed a reduction in terms of number staff in post and in

terms of FTEs (Full Time Equivalents), the main reasons explaining the increase of

the average basic salary by FTE, are, as far as the major part is concerned:

a cumulative increase of 5.4% over the period resulting from the CVI granted,

and, as far as the balance is concerned,

a combination of the following parts,

a recurrent part: the yearly promotion exercise and career advancement

process,

an exceptional part: the implementation of the two phases of the Five-

yearly review 2010 decided by Council in December 2010.

Further details on this increase of personnel expenses are also provided in the

Financial Statements, Part 2, Note 23 and in our paragraph 7 b).

Therefore, considering that reducing the level of personal expenses could be used by

the Management as one of the possible drivers1 for achieving internal savings, we

1 Refer to paragraph 6.2.1 “Net Assets”, point 4.

CERN/FC/5740 7CERN/3064

therefore recommend to monitor closely the increase of these expenses and to keep

the Council informed through a periodic and detailed report, also specifying the

potential effect of this increase in remuneration resulting from career advancement

on the Pension Scheme.

4.1.2 Total revenue

Total actual revenue amounted to 1.186,5 MCHF showing a decrease of 2,1% as

compared with the previous year end (1.211,7 MCHF in 2011). As in previous

years, actual revenue consisted mostly of contributions from Member States

(1.082,2 MCHF, weighting 91,2% of the total revenues). Details of revenues are

given in the Financial Statements, Part I, page 5.

4.2 Net Accounting Deficit

Total revenue minus total expenses led to a budget surplus of 108,0 MCHF. After

deduction of 24,3 MCHF for capital repayment and of 60 MCHF for the

recapitalization of the Pension Fund, 23,7 MCHF (131,7 MCHF in 2011) were

allocated to the Budget Balance to reduce the accumulated budget deficit.

2012 was the fifth year in which CERN had a budget surplus after a number of years

of deficit. This confirms a continuous positive trend reversion as compared to the past

as shown in the table below:

Years Budget (MCHF) Budget surplus/deficit (MCHF)

2005 -332,0 -323,6

2006 -183,9 -184,3

2007 105,1 130,6

2008 229,4 265,9

2009 276,8 306,4

2010 178,3 288,0

2011 123,4 215,3

2012 8,8 108,0

The “Accounting Reconciliation” table in page 3 follows the table on page 2

8 CERN/FC/5740 CERN/3064

"Statement of Comparison of Budget and Actual Amounts" and shows the

transition from the Budget Surplus (108,0 MCHF) to the Net Accounting Deficit

for the year 2012 (-252,9 MCHF), by integrating in the first item those amounts, in

surplus or deficit, not present in the Budget but recorded in the Financial Year 2012.

The accounting reconciliation is mainly given by fixed assets' depreciation and

expenses transferred to the same item minus variations of provisions and the

recapitalization of Pension Fund.

CERN/FC/5740 9CERN/3064 5. STRUCTURE OF THE ACCOUNTING STATEMENTS

The Financial Statements of CERN prepared and presented in compliance with IPSAS 1

included the following elements:

A Statement of Financial Position, showing Assets (divided into Current and Non-

current assets), Net assets and Liabilities (split into Current and Non-current

liabilities);

A Statement of net surplus/deficit and gains/losses recognized directly in Net Assets,

showing the Net surplus or deficit for the Financial Year including gains and losses

directly recognized in Net Assets without being transferred to the Statement of

Financial Performance;

A Statement of Changes in Net Assets, showing the Net surplus or Deficit for the

Financial Year including losses directly recorded in Net assets without being

transferred to the Statement of Financial Performance;

A Statement of Financial Performance, showing the Surplus/Deficit for the

financial year;

A Cash Flow Statement, showing the inflow and outflow of cash and cash

equivalents, purposely regarding the operational, investments and financing

transactions and the treasury totals at the end of the Financial Year;

Notes on the accounting statements providing information about accounting policies and

additional information necessary for a fair presentation.

10 CERN/FC/5740 CERN/3064

6. STATEMENT OF FINANCIAL POSITION 2012

6.1 Assets

Assets - mostly consisting of Non-current assets (96,0%) - totalled to 7.650,4 MCHF

at the end of 2012, showing a decrease of 110,3 MCHF (- 1,4%) as compared to

2011 (7.760,7 MCHF).

6.1.1 Non-current Assets

Non-current assets as at 31 December 2012 totalled to 7.347,9 MCHF, recording a

reduction of 152,3 MCHF (- 2,0%) as compared to 2011 figures (7.500,1 MCHF), this

was mainly due to the depreciation of the LHC”2.

They consist of a) Fixed Assets, equal to 7.200,2 MCHF (98,0% of the total Non-

current Assets) b) Financial assets, only related to the CERN Health Insurance

Scheme (CHIS), equal to 146,8 MCHF (1,99% of the total Non-current Assets) and c)

Intangible assets3, inserted in this heading for the first year, equal to 0,9 MCHF

(0,01% of the total Non-current Assets).

a) Fixed Assets

The total amount of Fixed Assets as at 31 December 2012 was 7.200,2 MCHF,

compared to 2011 (7.373,4 MCHF) it showed a decrease of 173,2 MCHF (- 2,3%).

Fixed Assets consisted of i) infrastructure and services buildings ( 2,3% of the Fixed

Assets), ii) LHC, which amounted to 6.287,4 MCHF (87,3% of the Fixed Assets),

iii) PS consolidation (0,8% of the Fixed Assets), iv) SPS consolidation (0,5% of the

Fixed Assets) and CNGS (0,4% of the Fixed Assets) plus fixed assets in progress,

which amounted to 622,9 MCHF (8,7% of the Fixed Assets).

LHC

As far as the LHC machine is concerned, it was recorded for 6.287,4 MCHF under Fixed

Assets, and it was 87,3% of the whole heading. In order to understand the relevance

of the LHC, it is important to highlight that it weights around 82% of the CERN’s

2 Refer to Note 3, Part II of the Financial Statements, paragraph 3.1. 3 Refer to Note 4, Part II of the Financial Statements.

CERN/FC/5740 11CERN/3064

assets.

The reduction of the value recorded in 2012 (6.287,4 MCHF), as compared to the

2011 value (6.682,4 MCHF), was due to the depreciation of the machine, using a

linear method at the rate of 5% of the gross value of the various component, except

for computing component. The LHC will be depreciated in a 20 year-period and it

has been recorded into the account as a Fixed Asset at the end of 2008 when it started

its activity. Implementation and upgrading of the LHC are after 2008 recorded in the

accounts under the sub-heading fixed asset in progress which is examined in the

paragraph below.

CNGS

As far as the CNGS asset programme is concerned, it was recorded at net book value

for 29,8 MCHF under Fixed Assets, and it was 0,4% of the whole heading. Having

been depreciated at a rate of 10% for half of its gross value, and in the Medium

Term Plan4 not having been reported any decision of closing, we have requested the

Management, as in the last year, to provide us with further elements, and we

understood that Management is discussing over CNGS’ future and the decision of a

depreciation rate of 10% is consistent with the information received.

We therefore renew our recommendation to the Accounting Service to monitor

closely the decision that will be taken on the future of CNGS, in order to assure that

this decision of the Management will be correctly reflected in the accounts.

Fixed Assets in Progress

This sub-heading, which recorded all the Assets that are still in the process of

being built at the 31st of December, amounted to 622,9 MCHF and it increased by

219,1 MCHF (+54,3%) comparing to the previous year (403,8 MCHF).

The overall increase of 219,1 MCHF, recorded into the 2012 accounts, is due to the

net effect of, from one side, the additions (+263,0 MCHF) and, on the other side, of

the disposals and transfers (-43,9 MCHF).

Under the 2012 additions5, the most relevant activities are the LHC improvement

(52,1 MCHF, representing around the 20% of the all Additions), the LINAC 4 (28,4

MCHF), the accelerator consolidation (26,2 MCHF), the CLIC Test Facility (25,4

MCHF) and the LCG Phase 2 (20,8 MCHF).

4 CERN/3069. 5 Refer to Note 3.2, Part II of the Financial Statements.

12 CERN/FC/5740 CERN/3064

We audited a sample of transactions recorded in the accounts as additions in the year

2012 without detecting any material error.

- o-o-o -

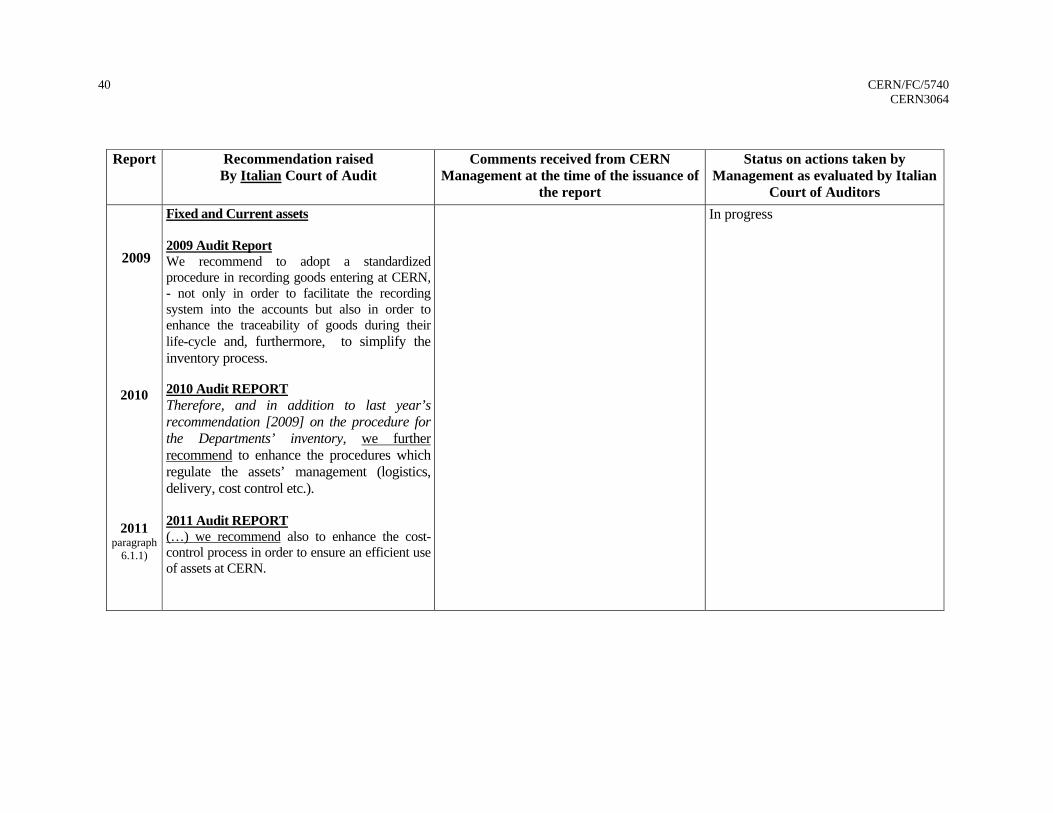

Management has started to develop common procedures for the Inventory process

As in the past years, during our audit activity related to the Assets, we focused on

asset management such us inventory procedures set up by the Management, the

logistics and procedures which regulate the safekeeping, the attribution of property

and the recording of the fixed assets into the accounts.

Since the beginning of our audit mandate in 2008, we observed that the assets’

management is weak, especially considering the volume and the value of such assets

and that the inventory procedures, although existing, were too broad, leaving

flexibility for their implementation according to the specific requirements of each

department, ending up in creating discrepancies in the categories of goods recorded

under the inventory procedure in different Departments.

According to our past recommendations and to our findings, in 2011 Management

gave them priority and a “Working Group Inventory” was set up with a first meeting

held on September 2011. Progress has been made in achieving the objectives of

establishing a standard procedure (using a defined list of inventoriable items) and in

designing and putting in place a new inventory application having links with other

software (EDH, CET, others), enhancing internal controls and standardizing the way

of working for all Departments.

We followed-up the implementation in 2012 of such process, and we acknowledge

the efforts of the Management in bringing solutions to the problems we identified.

We therefore recommend, as in the past year, to continue to enforce the inventory

rules, to extend the list of inventoriable items, registering them in a single point-of-

entry, and following them through their life-cycle. As part of this work, we

encourage CERN to put an emphasis on identifying and implementing measures to

ensure the accuracy and controls over all fixed assets. We view this as important

given the significance of the fixed assets to CERN’s operations and financial

statements. Furthermore, given no fixed asset register exists, we suggest

Management to take account of cost-benefit issues before deciding to implement our

recommendation.

CERN/FC/5740 13CERN/3064

We also renew our recommendation to enhance the cost-control process in order to

ensure an efficient use of assets at CERN.

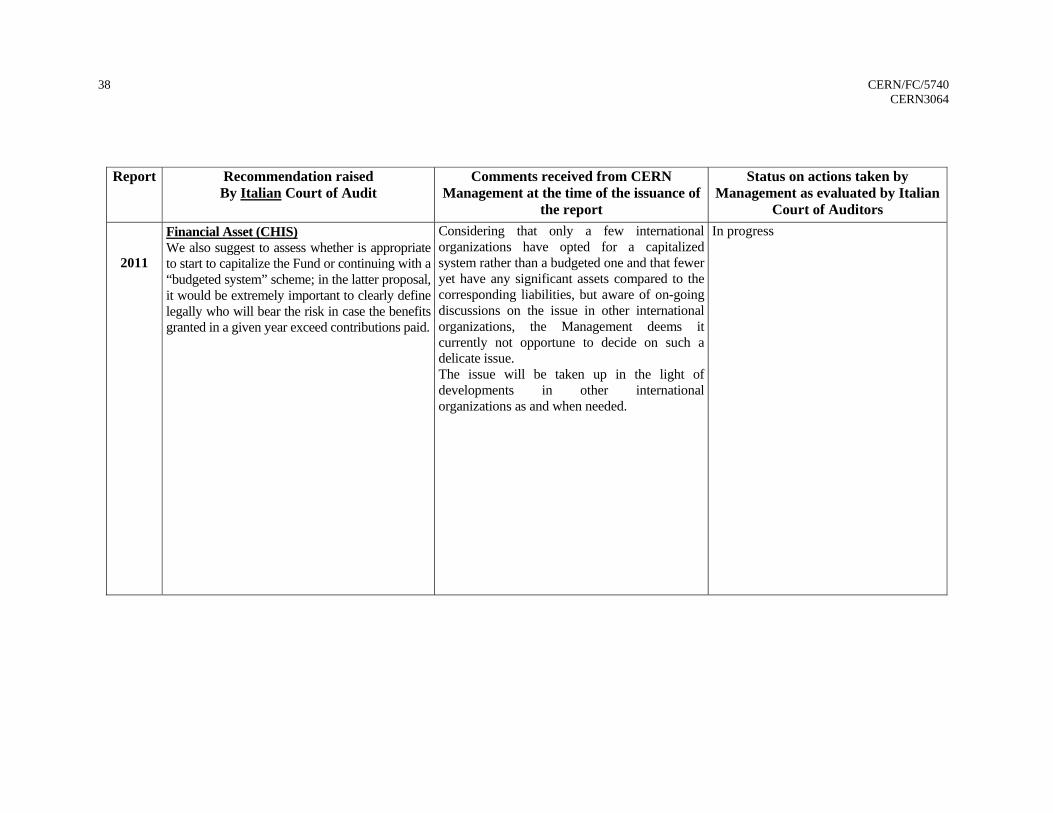

b) Financial Asset – CHIS Fund

The CHIS financial assets amounted to 146,8 MCHF in 2012, increasing by 15,9%

(20,1 MCHF) in comparison to 2011 (126,7 MCHF).

The CHIS financial assets in 2012 consisted of equities and bonds (136,1 MCHF,

equivalent to 92,6% of the amount shown in the heading Financial Asset - CHIS

fund), deposits in bank accounts (8,1 MCHF), UNIQA receivable (1,8 MCHF) and

credits stemming from taxation at source through anticipated deductions to be

reimbursed (0,9 MCHF). The CHIS assets have their exact counterpart in the liabilities.

In December 2007, as requested by IPSAS, the reserves previously set aside for the

CHIS were transformed into a capitalized fund for the CHIS. At the same time, this

was done to contribute to facing the issue of the aging of the insured population as

this fund was expected to increase with capital return together with payment into the

fund of any contributions in excess of benefits paid.

In December 2007, reserves accumulated for Health Insurance and Long Term Care from

past contributions were transferred to the capitalized fund. The full amount of the fund

fluctuated depending on the performance of investments as well as on the ratio

contributions/benefits and on the overheads expenses.

We defined in broad term as “technical performance” the ratio between contributions

and benefits paid (including the Contractor fees and overheads) and as “financial

performance” the financial gain or loss on financial assets.

The performance of the Fund for years 2008, 2009, 2010, 2011 and 2012 is listed

below:

CHIS FUND (in MCHF) 2012 2011 2010 2009 2008

Technical Performance 13,4 15,9 6,8 -0,8 4,9 Financial Performance 6,6 -1,0 2,2 9,4 -7,0 Total 20,0 14,9 9,0 8,6 -2,1

14 CERN/FC/5740 CERN/3064

Analytical review of the CHIS Fund from 2008 till 2012

In 2008 we observed a decrease of 2,1 MCHF in the CHIS assets; in fact, the

financial performance suffered directly from the financial crisis that took place in

2008. On the contrary, the total performance of the Fund from 2009 till 2012 was,

on total, positive and it appears as steadily increasing (respectively, from 8.6 MCHF

in 2009, to 9.0 MCHF in 2010, to 14,9 MCHF in 2011 till 20,0 MCHF in 2012), but

with different contribution from the technical and financial performance.

More specifically, results were affected in 2009 by a negative technical performance,

mainly due to the negative ratio of contributions/benefits, however compensated by a

positive financial performance (around 9% if compared with the CHIS assets).

Meanwhile, in 2010, both performance’s components were positive but with a

reduced contribution of the financial performance (around 2% if compared with the

CHIS assets).

In 2011 the ratio contributions/benefits was positive with an increase of 9,1 MCHF

(+133,8%) comparing to 2010 but with a negative financial performance (-1 MCHF).

In 2012 the ratio contributions/benefits is positive with a slight decrease of 2,5 CHF

(-15,7%) comparing to 2011 and with a positive financial performance (6,6 MCHF).

However, it is worthwhile mentioning that, in 2011, in order to stabilize it by

“counter[acting] revenue shortfall stemming from deviations from the actuarial

assumptions”6, the Fund received 5,0 MCHF of additional contribution from CERN,

then if we deduct it from the total performance of 2011 (9,9 MCHF net of the

additional contribution), the increase from 2011 to 2012 is equivalent to 10,1 MCHF

(+102,0%).

Management reacted rapidly to the negative financial performance in 2011

With reference to the paragraph above related to the “analytical review”,

Management explained in Note 11 of the Annual Accounts (ref. pages 32 and 33),

that the “financial performance of the funds invested with (...) banks amounted to 6.6

MCHF (-1 MCHF in 2011)” and that the “performance is based on a valuation of the

portfolio at market prices at 31.12.2012. The gross yield is 5,68% in 2012 compared

to -0,6% in 2011”.

Although performance is also linked to unforeseeable circumstances and to market

6 Refer to FC/5497.

CERN/FC/5740 15CERN/3064

trend, Management reacted and invited the banks’ executives, responsible of the

negative performance of 2011, providing them written instructions, to limit risks and

to protect capital from future losses. Management then reported on this initiative for

information to the CERN Health Insurance Supervisory Board meetings, held on 14th

February 2012 and on 14th March 2013.

We acknowledge and welcome the Management’s reactivity and, as last year, we

recommend to perform a continuous monitoring of the investment’s performance and

to issue clear and formal instructions to the banks as a result.

The 2012 technical performance: ratio contributions/benefits improved again

positively this year although the long term sustainability is not yet assured

In the past years, from our audit and our analysis performed over the scheme, we

observed some risks and critical points in relation with: i) the capacity of the CHIS to

fulfil its obligations in the long term, ii) the internal controls, delegation of duties and

compliance with rules.

We have followed up in the following paragraph (paragraph i) and in our follow-up

table (See Annex 1) whether the remedial actions that have been approved by

Council ensure that the CHIS will have the capacity to fulfil its long term obligations.

The additional contribution from CERN of 5 MCHF in 2011 should remain

exceptional

This year, no additional contribution from CERN has been made available to the

Fund. However, as above mentioned7, we are aware that the additional contribution

was granted only in year 2011.

Considering that this saving, although to a lesser extent, will benefit directly the

CERN’s activities and research, we recommend to exclude additional contribution to

the CHIS Fund in the future, in particular when its performance is positive.

i) CHIS’s capacity to fulfil its obligation in the long term

Under the non-current liabilities shown in the Statement of Financial Position, and

7 Refer to FC/5497.

16 CERN/FC/5740 CERN/3064

more specifically under the heading concerning the post-employment benefits8, there

are reported provisions that cover future obligations due to present commitments and,

in particular, the one related to the Health Insurance Scheme that represents the

estimated actuarial liability. The trend of this provision is listed in the table below,

which is an extract of the table presented in paragraph 6.2.2.

in MCHF

Post-employment benefits (Liabilities) 2008 2009 2010 2011 2012

CHIS Benefits 1.438,7 1.597,4 2.515,0 3.348,2 3.457,3

As reported in the Note 13 of the Financial statements, the increase in the CHIS

liability (109,1 MCHF) is mainly due to the reduction of the discount rate (69

MCHF), mitigated (+51 MCHF) by other changes such as the rate of contributions

and related population.

As last year, we highlight that liabilities are steadily increasing and, in the long term,

the CHIS might face underfunding issue.

Although the 2010 Five-yearly review, and the proposals by the Management

summarized in 4.2.2 of the document CERN/2946 resulted in overall terms, into a

positive ratio contributions/benefits, the capacity of the CHIS to fulfil its long term

obligations is not yet assured in the long term.

Moreover, it is worth mentioning that the remedial actions approved in the 2010

Five-yearly review, did not change “the overall envelope of benefits”9 – which

remains substantially unchanged since year 2001-; the fact that the benefits have

been maintained unchanged, may partly explain the increase of around 4,1% in the

benefits paid in 2012 (71,7 MCHF) comparing to year 2011 (68,9 MCHF: increase of

around 5% comparing to 2010) and to year 2010 (65,4 MCHF).

We are not in the position to evaluate, at the issuance of the Report, the effect of the

increase in the covered population of 2%, which cannot be considered directly

correlated to the increase of 4,1% of the benefits paid because, usually, new members

8 Refer to paragraph 6.2.2 below. 9 Annex 1 CERN/2946 particularly § 4.2.2.

CERN/FC/5740 17CERN/3064

usually have a positive impact in the level of contributions paid to the Scheme.

We are aware of the fact that in the context of the 2010 five-yearly review,

Management proposed and Council agreed that the Director General may “take

timely measures to limit the increase of CHIS expenses, by encouraging the use of

health care providers and treatments which provide the best quality-to-cost ratio10”.

On this basis, Management, as it is also stated in our follow-up table, declared

elaborated changes in the benefits in 2011 with effect on 1 January 2012, inviting

“CHIS members to make increase use of medical treatment and products in and from

low health care cost Member States”. However, looking at the above mentioned

increase in the benefits paid in 2012 (+4,1%), this measure, which is not structural

and is based only on the sense of responsibility of the CHIS Members, has not yet

proven to be effective.

In this sense, we suggest that possible structural remedial measures in order to reduce

the level of benefits paid would be adopted, after a careful review and analysis of

every specific medical treatment and drugs, to put a threshold which is based “on use

of medical treatment and products (…) from low health care cost Member States”.

Furthermore, if we combine the CHIS liabilities (3.457,3 MCHF) with the CERN

Pension liabilities (equal to 5.318,7 MCHF), the future obligations for the two

schemes (8.776,1 MCHF), as also highlighted last year, have a critical impact on the

CERN’s Member States obligation (see paragraph related to Net Assets).

The continuous increase of the CHIS and Pension Fund liabilities, confirmed also in

2012 (+0.9 %), that weights around 86% of the total liabilities, although they are

actuarial provisions, in case that the benefits granted to staff are maintained at the

same level in the future for the two schemes, we express, this year again, our concern

that the part of the Member States contributions which actually fund research

activities and projects will be de facto reduced, year after year more significantly, by

the funds allocated to the long term balance of the social schemes.

In addition, we highlight, this year again, that the long-term risk of affecting the

sustainability of the CHIS has, so far, not yet been fully addressed by the bodies

responsible for managing the CHIS and, in the hypothetical scenario of dissolution of

CERN, there are, today, no remedial actions or agreements with external bodies for

maintaining the health insurance level as, for example, Council’s resolution in 1996

10 Refer to Annex 1.

18 CERN/FC/5740 CERN/3064

to establish, prior to the dissolution of the Organization, a Foundation intended to

succeed to the CERN Pension Fund11.

Therefore, we renew our recommendation that, in the future, the financial long-term

equilibrium of the scheme is periodically monitored in order to (a) confirm that the

corrective measures are giving the expected results, (b) if needed - that appropriate

actions or measures are introduced as soon as possible in order to prevent any further

deterioration.

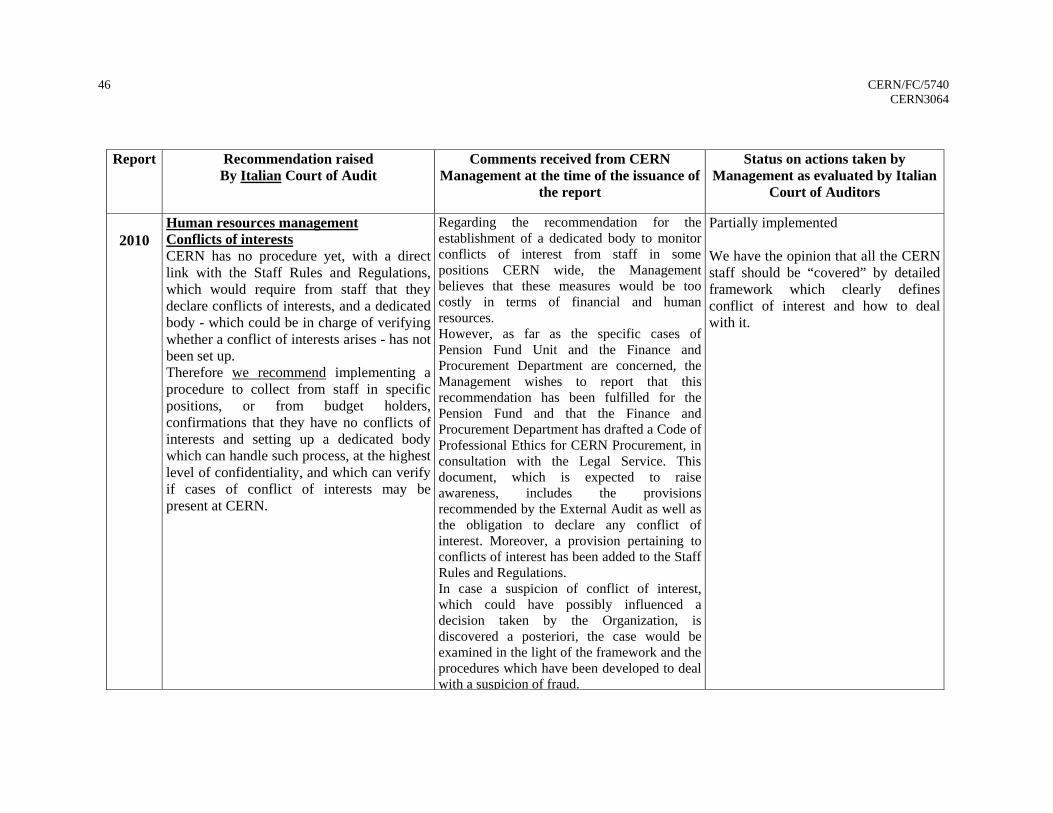

ii) the internal controls, delegation of duties and compliance with rules

Management, in line with our recommendations issued in previous years, nominated

in 2011 a Manager (Head of Health Insurance and Social Services), in charge of

addressing issues related to internal controls and reporting, conducting a benchmark

and an analysis of the pros and cons of in-sourcing the CHIS administration,

preparing consistent proposals for a new tender, and preparing Management’s

response to Internal and External Audit recommendations.

In March 2013 the Manager presented both to us and to the CERN Internal Audit the

response to our recommendations, listed in a report signed by the Director General.

We welcome the timely presentation of this report and we recognize the important

effort of the Management to provide us detailed information. We have followed–up

the Management’s reply to our recommendations in Annex 1.

It is worthwhile mentioning that, although we classified as “closed” our

recommendation issued in 2009 related to the assessment of “the economy, the

efficiency and effectiveness of using an external service provider instead of a direct

in-house management”, we consider as a good practice in the public sector not to

outsource – even through a tender process- indefinitely and repeatedly and, more, to

the same external provider, a service that can be equally in-sourced. Therefore, we

recommend to apply the principle of competitive re-tendering and rotation12 between

the present company and other service providers.

-o-o-o-

11 CERN/2165. 12 Refer to the following paragraph “Principle of rotation and conflict of interest”.

CERN/FC/5740 19CERN/3064

Principle of rotation and conflict of interest

With reference to the contract above mentioned and, furthermore, considering that

last year, we observed another case of a contract which was systematically renewed

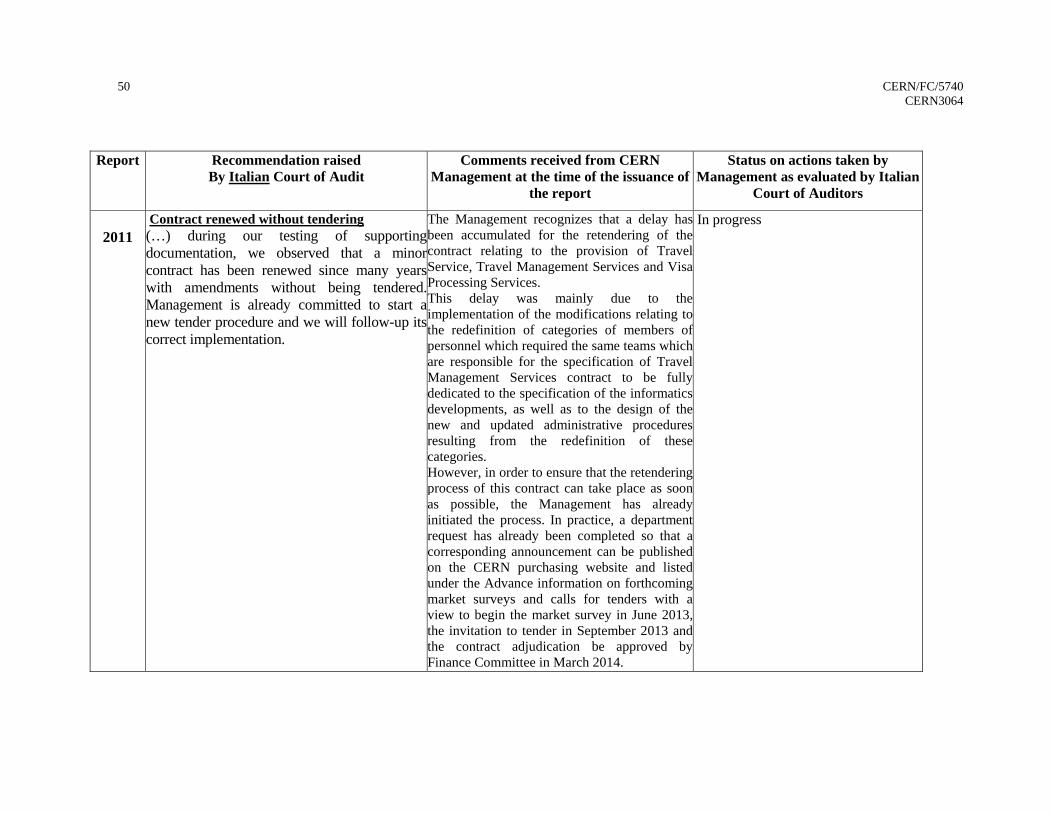

since 23 years without being tendered13, this year, following our analysis of the

Purchasing report at 31.12.2012 presented by the Management to the Finance

Committee14, we asked the Procurement services to provide a detailed list of all the

categories of contracts (i.e. B, C, E, K, KE, KM, S, X), assigned to the same supplier

for a period exceeding 7 years duration. We obtained a list of 44 such contracts.

Of the 44 contracts, 33 had been with the same supplier for more than 10 years

(global value 181,5 MCHF), and 6 had a duration of more than 20 years (global value

39,1 MCHF).

We understand that, for each of these contracts with a long duration, Management

has a reasonable explanation, therefore we are not pointing out any single contract.

Moreover, we acknowledge that the Procurement service regularly provides to the

Finance Committee updated information on all the contracts.

However, whereas the principle of re-tendering has a sound legal basis at CERN, in

particular in the procurement rules, there is no legal basis for a “principle of

rotation”, which means that a supplier cannot be awarded a contract beyond a pre-

define period. Actually, we consider that, in such cases of continued renewal of

contract, a public organization, with a view to cost effectiveness, should reflect on

the opportunity to in-source this specific service (as we stated also in the above

paragraph related to delegations of duties at the CHIS Fund). This principle of

rotation is applied at CERN for the External Audit mandate, or for the appointment

of the Pension Fund Actuary. More generally the principle of rotation is applied

outside CERN, to prevent potential risks of conflicts of interest.

In our view, re-tendering and “rotation” should both be possible at CERN and

covered by a sound legal basis, therefore we recommend Management to start to

prepare an analytical study about the appropriateness as well as the pros and cons of

inserting the principle of rotation in the CERN procurement rules with the objective

to mitigate the risks of cost ineffectiveness and conflicts of interest.

13 In Annex 1 we have followed-up the related recommendation. 14 Refer to CERN/FC/5722/RA.

20 CERN/FC/5740 CERN/3064

c) Intangible Asset

This heading, has been inserted for the very first time at CERN in 2012, in line

with our recommendation, and, therefore, at 31 December 2012, intangible assets

were recorded for 0,9 MCHF.

Although the amount is not relevant in weight on the total Non-current Assets

(0,01%), we strongly believe that capitalising intangible assets, in particular

patents and internally developed software, is important for CERN. We have not

noted any issues with the initial implementation of CERN’s intangible assets

policy or the measurement of intangible assets as at 31 December 2012, however

we recommend that Management monitors both the policy and its implementation

in future years.

We retraced the corresponding entries and transition procedures for Non-current Assets

accounts and we examined the bookkeeping entries of expenses accounts and fixed

assets accounts, including depreciations. We did not observe material errors and the

amounts recorded in the Financial Statements are thus verified and confirmed.

6.1.2 Current Assets

The total of inventories, receivables, cash and cash equivalents, other financial

assets, was 302,5 MCHF in 2012 (260,6 MCHF in 2011) resulting in an increase

of 41,9 MCHF (+16,1%). Current assets weighted 4,0% of the total assets, increasing

the weight they had in the 2011 Accounts (3,4%).

A breakdown of Current Assets is shown in the Financial Statements, Part II, Notes 5

to 8; the basis for the evaluation of Current Assets is given in the Accounting

Principles (Accounting Statements, Note 1).

The sub-heading "cash and cash equivalent" - totalling to 42,7 MCHF15 (146,7

MCHF in 2011; 37,3 MCHF in 2010; 26,7 MCHF in 2009 and 61,8 MCHF in 2008)

- included all the balances of CERN banks current accounts as at 31 December

2012.

We asked all the banks having a business relation with CERN to confirm the current

accounts' balances as at 31 December 2012 and we verified that they were properly

15 See paragraph 9 “Cash-flow Statement 2012” .

CERN/FC/5740 21CERN/3064

recorded into the accounts. All variances detected have been explained and justified.

Current Assets also comprised inventories amounting to a net value of 6,4 MCHF

(gross value as at 31.12.2012 equal to 8,2 MCHF minus a depreciation of 1,8

MCHF); they represent around 2,1% of the Current Assets.

The low stock values were mainly due to the Stores Management commitment to a

policy of minimization of items in the stores through direct delivery to users. We

carried out, as past years, a physical stock checking of a sample of items randomly

selected by us. No major problems were identified, which may have an impact on the

accounts at the closing date (31.12.2012). We traced that all the tested items were

properly recorded into the Stores' accounts.

Receivables, totalling 128,5 MCHF (108,1 MCHF in 2011), which weight 42,5%

of the Current Assets value, resulted in an increase of around 18.9 % comparing

to 2011, mostly corresponded to the sums which Member States owed to CERN as

contributions. During the last five years this sub-heading showed a considerable

noteworthy increase — from 8,9 MCHF in 2008 to 43,6 MCHF in 2009, to 51,2

MCHF in 2010, to 79,6 MCHF in 2011 and to 88,5 MCHF in 2012 — resulting in

29,3% of all Current Assets.

In addition, the heading included taxes paid by CERN (total amount in 2012 10,5

MCHF; 10,9 MCHF in 2011), to be refunded as a consequence of CERN’s

exemptions regime (3,5% of Current assets), plus the amounts owed by teams and

collaborations (6,7 MCHF in 2012; 6,5 MCHF in 2011) plus other receivables and

prepayments (22,7 MCHF in 2012 and 11,0 MCHF in 2011; +11,7 MCHF comparing

to 2011).

As for the above-mentioned receivables (amounts owed by sundry debtors) we asked,

on a sample basis, direct confirmation from third parties of the amounts declared by

CERN as due at the year-end. According to our suggestion, the accounting unit is in

the process of carrying out a careful review of any discrepancies which emerged.

Some clients did not answer to our confirmation letters' request. In these cases, yet

again on a sample basis, and also in relation to the other subheadings, we checked

the subsequent payments after the year-end closing and no major problems have

been identified.

22 CERN/FC/5740 CERN/3064 6.2 Liabilities and Net Assets

6.2.1 Net Assets

This heading corresponded to the difference between liabilities and assets and it

included contributed capital, accumulated gains and losses from defined benefits

plans, accumulated surpluses - or deficits - and reserves, as shown in the Statement

of Changes in Net Assets16.

The Statement of Financial Position shows a negative net assets (-2.554,4 MCHF) due

to the impact of the net deficit for 2012 and the gains and losses recognized directly in

net assets of -219,5 MCHF, mainly originated by provisions for actuarial liability for

post-employment benefits totalling 8.776,1 MCHF (5.318,7 MCHF for Pension Scheme

and 3.457,3 MCHF for Health Insurance Scheme).

Management is monitoring the effectiveness of the measures that it submitted to the

Council and which were approved in December 2010 and Management has assured us

that it will continue to monitor these and will adapt them should a change in situation

arise. We would like to point out that remedial measures also depend on unforeseeable

events, for instance, developments on the investment markets.

As already stated last year, remedial measures are urgent and necessary and we continue

to observe that there are mainly five “drivers” in order to offset negative Net assets:

1. increase the level of Member States’ Contributions

2. increase the level of Staff contributions to the Pension Fund and Health Insurance

Scheme

3. decrease the level of benefits guaranteed by the Health Insurance Scheme

4. increase the level of internal savings, through a reduction of specific expenses

related to personnel and operations

5. increase the level of revenues, for example charging researchers and users from the

Member and Non-Member States when being hosted at CERN.

We were told by the Management that it is best practice in the research environment

to allow free access for researchers and users, which concerns the fifth driver.

As remedial measures are urgent, these drivers have to be considered by the

16 Financial Statements, Part II, page 15.

CERN/FC/5740 23CERN/3064

Council: whereas the first two drivers are not within the Managements’ remit, we

recommend Management to address the third and fourth drivers, having noted that

these drivers have not been significantly tackled during 2012.

6.2.2 Non-current liabilities

This heading comprised long-term debts, ppbar contributions from Member States,

liabilities against a fund for the CERN Health Insurance Scheme (CHIS) and

provisions covering obligations of uncertain amount and timing mainly related to

post-employment benefits and radioactive waste management.

The Non-current liabilities totally amounted to 9.830,9 MCHF at the end of 2012

(9.719,3 MCHF at the end of 2011, after the reclassification as explained in the Note

to the Statement of Financial Position) with a slight increase of 111,7 MCHF, +1,1 %,

mainly due to the post-employment benefits.

Total long-term debts weighted 4,2% of the total non-current liabilities (4,5% in

2011, 6.6 % in 2010 and 9% in 2009) and they decreased by 25,3 MCHF (-5,7%),

from 465,3 MCHF in 2010, to 441,5 in 2011 and, finally, to 416,2 MCHF in 2012,

and included loans with FORTIS BANK, FIPOI and SIG (Services Industriels de

Genève).

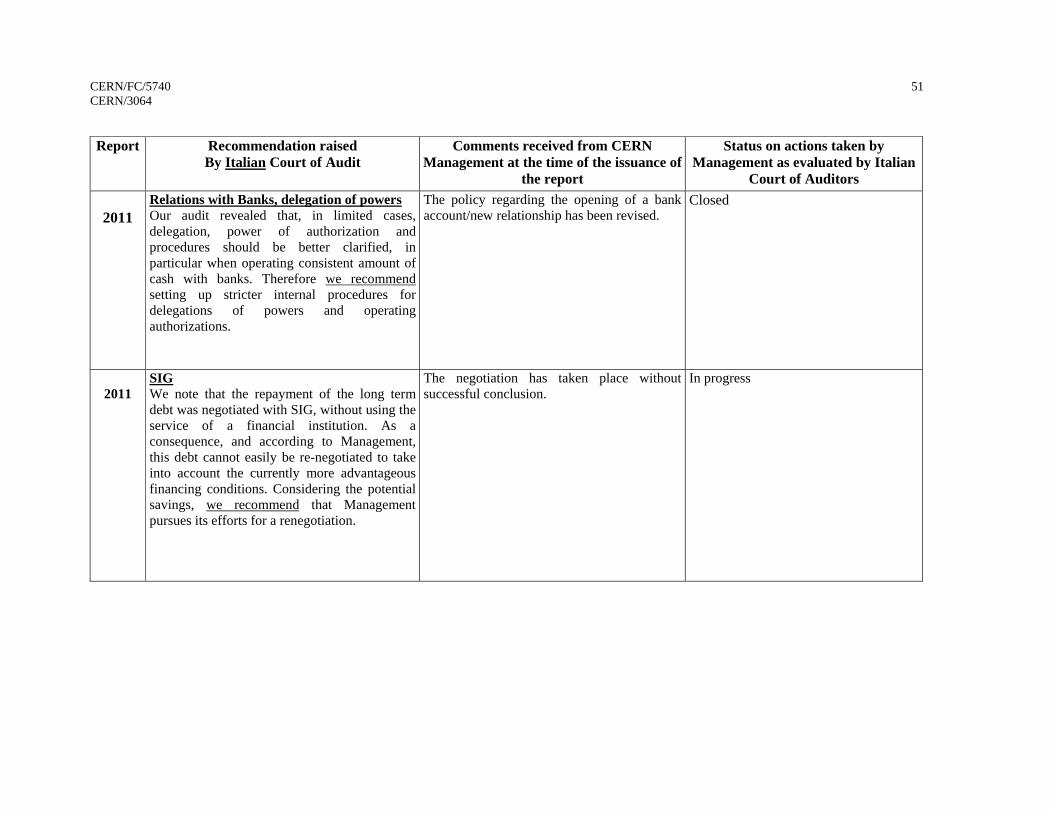

The outstanding debt of 37,9 MCHF with SIG at 31.12.2012 is being repaid with

annual payments of 4 MCHF, and will be entirely repaid in 2024.

Liabilities against Member States - related to ppbar contributions from 5 of the

Member States - amounted to 20,7 MCHF as at 31 December 2012, same amount as in

the past years due to the fact that no indexation rate has been applied.

The recommendation made by our predecessors, the Austrian Court of Audit, to write

off this debt, is still pending (see Annex 1), however we are aware that for the first

time after years, following our recommendation, Management has sent a letter to the

Member States concerned; therefore, we recommend to find with them a mutually

agreed solution that can lead to write off or to pay back the debt.

24 CERN/FC/5740 CERN/3064

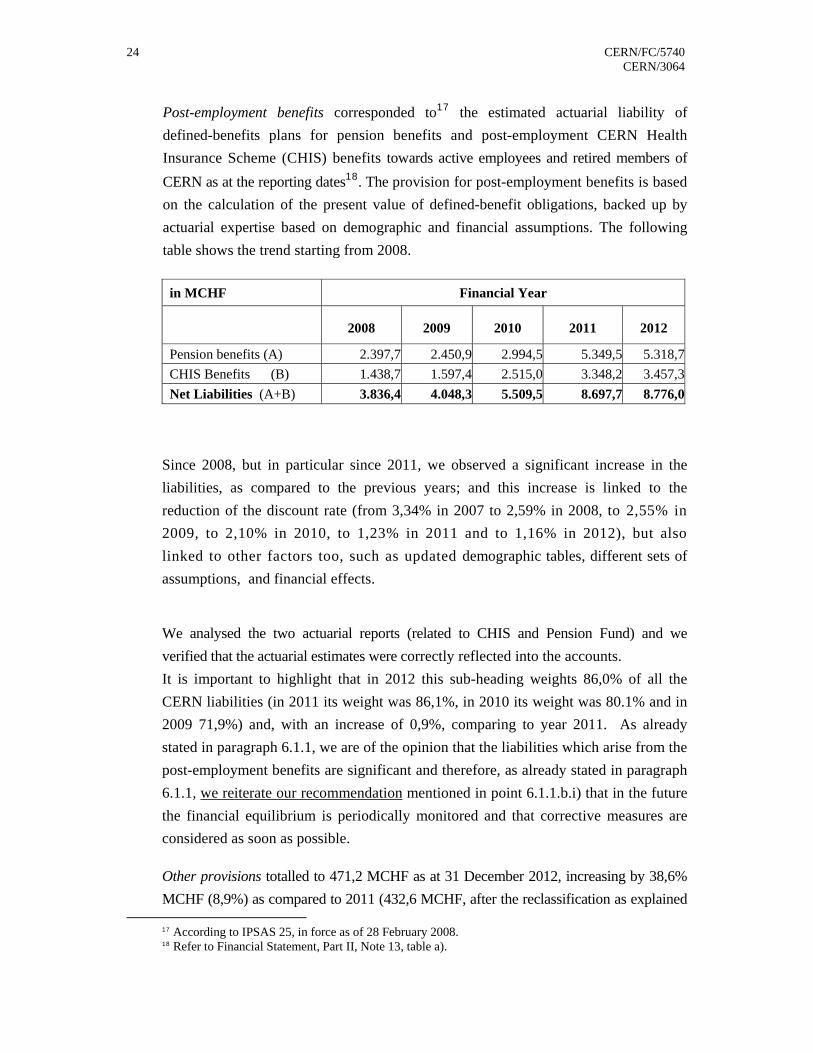

Post-employment benefits corresponded to17 the estimated actuarial liability of

defined-benefits plans for pension benefits and post-employment CERN Health

Insurance Scheme (CHIS) benefits towards active employees and retired members of

CERN as at the reporting dates18. The provision for post-employment benefits is based

on the calculation of the present value of defined-benefit obligations, backed up by

actuarial expertise based on demographic and financial assumptions. The following

table shows the trend starting from 2008.

in MCHF Financial Year

2008 2009 2010 2011 2012

Pension benefits (A) 2.397,7 2.450,9 2.994,5 5.349,5 5.318,7

CHIS Benefits (B) 1.438,7 1.597,4 2.515,0 3.348,2 3.457,3

Net Liabilities (A+B) 3.836,4 4.048,3 5.509,5 8.697,7 8.776,0

Since 2008, but in particular since 2011, we observed a significant increase in the

liabilities, as compared to the previous years; and this increase is linked to the

reduction of the discount rate (from 3,34% in 2007 to 2,59% in 2008, to 2,55% in

2009, to 2,10% in 2010, to 1,23% in 2011 and to 1,16% in 2012), but also

linked to other factors too, such as updated demographic tables, different sets of

assumptions, and financial effects.

We analysed the two actuarial reports (related to CHIS and Pension Fund) and we

verified that the actuarial estimates were correctly reflected into the accounts.

It is important to highlight that in 2012 this sub-heading weights 86,0% of all the

CERN liabilities (in 2011 its weight was 86,1%, in 2010 its weight was 80.1% and in

2009 71,9%) and, with an increase of 0,9%, comparing to year 2011. As already

stated in paragraph 6.1.1, we are of the opinion that the liabilities which arise from the

post-employment benefits are significant and therefore, as already stated in paragraph

6.1.1, we reiterate our recommendation mentioned in point 6.1.1.b.i) that in the future

the financial equilibrium is periodically monitored and that corrective measures are

considered as soon as possible.

Other provisions totalled to 471,2 MCHF as at 31 December 2012, increasing by 38,6%

MCHF (8,9%) as compared to 2011 (432,6 MCHF, after the reclassification as explained

17 According to IPSAS 25, in force as of 28 February 2008. 18 Refer to Financial Statement, Part II, Note 13, table a).

CERN/FC/5740 25CERN/3064

in Note to Statement of Financial Position). The increase is mainly due to the

reassessment of the estimated costs for the disposal of radioactive waste stored at CERN

at the year-end (392,0 MCHF, which represents around 83,2% of the sub-headings).

Other Items not recognized in the Financial Statement

The Management dedicated a paragraph to disclose the “other Items not recognized in the

Financial Statement”19 but for which the Management itself does not consider appropriate

to create a dedicated provision into the accounts or i) because they consider not having a

legal or constructive obligation, or ii) because they do not consider probable that an

outflow of resources will be required to settle the obligation or iii) because a reliable

estimate of the amount of the obligation cannot be made.

Dismantling

For the above-mentioned reasons, and as in the past year, no provision for dismantling is

recognized. Although neither a legal obligation for dismantling any installation (LHC

CNGS etc.) nor commitments to do so exist, it cannot be excluded that the closer towards

the end of operation, the more a future obligation for CERN to dismantle the installations

may be contracted.

Furthermore, it is not possible to foresee the sites' final destination and their physical state

by the end of their operational periods.

For these reasons, the assumption that, from a financial and accounting point of view, no

estimates of expenses for the dismantling should be included in the 2012 CERN Financial

Statements is basically correct according to the IPSAS, although, with the passing of

time, it might be appropriate to start giving some thoughts to the issue.

While current reporting is in conformity with IPSAS at the date of issuance of this

report, we recommend it would be prudent for Management in the coming years to

continue to assess the financial and operational effects of an eventual dismantlement,

and to inform Council on the results of such reflections in due course.

6.2.3 Current liabilities

The total amount of this item is 373,8 MCHF, presenting a decrease of 2,6 MCHF

19 Refer to Financial Statement, Part II, Note 13, part C. page 39.

26 CERN/FC/5740 CERN/3064

(-0,7%) as compared to 2011.

a) The total of short-term debt and bank overdrafts is referring to the amounts of

long-term debts falling in 2012 and to the short term borrowings from banks, and in

2012 it was 25,4 MCHF. It increased by 0,8 MCHF (+3,3%) as compared to the

previous year.

In 2012 CERN Management did not incur any short term borrowings from banks; in

the past, these operations were carried out to face temporary cash-shortage, mainly

due to delay in Member States contributions.

b) Other liabilities referred to suppliers (61,7 MCHF in 2012, decreased of 1,3% in

respect of 62,5 MCHF in 2011), advances received from teams and

collaborations (168,8 MCHF in 2012, decreased of 8,0% in respect of 183,4

MCHF in 2011).

We asked to a selected sample of suppliers having a business relation with CERN to

confirm the balances at 31 December 2012; around half of them answered and the

Accounting department reconciled the balances.

In other liabilities there are also included the compensations for shift work and accruals

of employee benefits from paid leaves and termination allowances in 2012, equal to

76,7 MCHF with an increase of 2,6 MCHF comparing to 2011 (74,1 MCHF, +3,6%),

after the reclassification as explained in Note to Statement of Financial Position; the

latter stood for the estimates concerning the accumulated present value of CERN’s

liability towards its staff.

c) Deferred revenues (37,1 MCHF in 2012; increased by 8,9 MCHF (+31,4%)

comparing to 28,2 MCHF in 2011) it referred mainly to EU and other projects to

be further recognized as revenue.

d) Other current liabilities amounted to 4,2 MCHF in 2012 with an increase of 0,5

MCHF (+13,3%) as compared to 2011 (3,7 MCHF).

The statement of liabilities and the corresponding notes were examined on the basis of

supporting documentation concerning the underlying transactions. We did not observe

errors and the amounts recorded are thus verified and confirmed.

CERN/FC/5740 27CERN/3064

7. STATEMENT OF FINANCIAL PERFORMANCE 2012

This Statement showed the Organization's operating and financial revenue and

expenses classified, disclosed and presented on a consistent basis in order to explain

the year's net deficit or surplus20.

a) Total operating revenue amounted to 1.442,9 MCHF with an increase of 48,6

MCHF (+3,5%) as compared to 2011 (1394.2 MCHF), chiefly owing to the increase of

the Transfers to the fixed assets amounting to 264,2 MCHF (183,9 MCHF in 2011)

which were increased by 80,2 MCHF (+43,6%) and to the contribution from EU

(+2,7 MCHF), from Romania, as candidate for accession (+0,8 MCHF), from Israel

and Serbia as associate Member States (+3,8 MCHF). The additional contributions

from Host-States (1,4 MCHF) decreased by -21,6 MCHF (-94,1%).

It is worthwhile mentioning that the Member States’ contributions decreased by 15

MCHF in 2012, as in 2011, and, according to the revised Medium Term Plan

approved in September 201021, that assumed a reduction of contributions by an

overall cumulative amount of 135 MCHF over the years 2011 to 2015 (in 2010

prices).

b) Total operating expenses increased compared to 2011 and they amounted to 1.686,4

MCHF and, in comparison with last year's (1.480,8 MCHF), showed an increase

of 205,6 MCHF (+13,9%). They are subdivided into three main items: Materials,

Personnel and Recapitalization Pension Fund.

Materials decreased from 877,6 MCHF in 2010 to 853,7 MCHF in 2011 (-23,9

MCHF, equivalent to -3%), mainly due to the effect of the assets depreciation.

Materials increased from 853,7 MCHF in 2011 to 937,4 MCHF in 2012 (+83,6

MCHF, equivalent to +9,8%), mainly due to the increase of the costs for service

contracts (+23,6 MCHF), for repair and maintenance (+10,4 MCHF) and due to the

effect of the variation of provision for elimination of radioactive waste (+ 27,0

MCHF).

Personnel22 increased by 122,1 MCHF (+21,5 %) from 567,0 MCHF in 2011 to 689,1

20 IPSAS 1: "As a minimum, the face of the statement of financial performance should include line items which present the following amounts: revenue, surplus or deficit from operating activities, financial costs and extraordinary surplus or deficit for the period." 21 Refer to CERN/2915/Rev. page 2, approved in the restricted 156th Session of the Council, held on 16th September 2010. 22 Refer also to sub paragraph 4.1.1 “Personnel expenses”.

28 CERN/FC/5740 CERN/3064

MCHF in 2012, in particular due to the growth of “Remuneration” (+11,2 MCHF,

+3,4%), to the increase of paid leave (+6,9 MCHF), and to the changes in provision

for post-employment benefits related to Pension and Health scheme (+101.8 MCHF,

+277.9,1%).

Recapitalization Pension Fund is a sub-heading, introduced last year for the first time,

that, following the Five-Yearly Review 2010 and the approval of the Council in

December 2010 (CERN/2947), shows the CERN contribution to the recapitalization of

the Pension Fund related to year 2012 (+60 MCHF). It is one of the most important

reasons of the increase of all the heading “Total operating expenses”.

We highlight, as last year, that this amount of 60 MCHF, to be transferred annually to

the Pension Fund for its recapitalization until full funding is reached, will have an

impact on the net surplus/deficit of every year onwards.

c) The Net deficit from operating activities amounted to 243,6 MCHF - as in previous

year, i.e. last year in 2011 was registered a deficit of 86,6 MCHF, in 2010 it was

around 50 MCHF- compared to the surplus registered in 2009 (5,7 MCHF) and in

2008 (1.624,0 MCHF).

d) Financial activities showed a deficit of 9,4 MCHF. Details of financial revenue and

expenses are provided in the Financial Statements, Part II, Note 24.

e) The net deficit for the year 2012 amounted to 252,9 MCHF which, when comparing

it with the 2011 net deficit of 101,4 MCHF (in 2010 the net deficit was of 68.9 MCHF),

illustrated a noteworthy increase of deficit of 151,5 MCHF (+149,4%).

We examined the composition of the Statement of Financial Performance based on the

balance and consolidation of corresponding annual accounts, we carried out interviews

within the Accounting service and we did not detect any material extraordinary

operations. We thus certify the amounts recorded in the Financial Statements and the

relevant net deficit for the period 2012.

8. STATEMENT OF CHANGES IN NET ASSETS 2012

In 2012 changes in the Net Assets (- 219,5 MCHF as opposed to -3.278,3 MCHF in

2011, and -1.511,1 MCHF in 2010), resulted from the recognition of gains directly

recorded in the Net Assets (+33,5 MCHF) related to variations due to actuarial

CERN/FC/5740 29CERN/3064

estimates regarding health care and pensions, plus 252,9 MCHF as net deficit for

the period.

As far as the accounting reconciliation is concerned, we found that the entries were

properly backed-up by supporting documentation and correctly settled into the

corresponding accounts.

9. STATEMENT OF NET DEFICIT & LOSSES RECOGNIZED DIRECTLY IN NET ASSETS

The Statement has been introduced in 2010 and discloses the net deficit for the year

2012 (-252,9 MCHF) (in 2011 it was -101,4 MCHF) and the other valuations

adjustments which, under IPSAS, are not recorded in the Statement of Financial

Performance but directly reported in the Statement of Financial Position, which in

2012 are the actuarial gains from defined benefits plans (equal to +33,5 MCHF,

composed by -17,8 MCHF for actuarial losses related to Health Care and by +51,3

MCHF for actuarial gains related to Pensions).

The total of the three above-mentioned figures (- 219,5 MCHF which is the result of

adding up the values of -252,9 MCHF and the value of +33,5 MCHF) is recognized

directly in Net Assets23. Thus the values are reconciled with both the Statement of

Financial Position and Changes in Net Assets24.

As last year, we draw the attention of the Council to the fact that, lacking sufficient

capital, special reserves and accumulated surpluses, the consequence of the net deficit

of the period (-252,9 MCHF) and of the actuarial gains (+ 33,5 MCHF) results on a

negative value of the Net Assets (-2.554,4 MCHF), which might require timely

reaction and corrective measures from the Council25.

10. CASH FLOW STATEMENT 2012

The Cash Flow Statement26 identifies the sources of cash inflows, the items on which

cash was spent during the reporting period, and the cash balance as at the reporting

date.

23 Refer to § 8. 24 Refer to Part II, page 15 of the 2012 Annual Accounts. 25 See paragraph 6.2.1. 26 Refer to Part II, page 17 of the 2012 Annual Accounts.

30 CERN/FC/5740 CERN/3064

In 2012 the Organization reported cash flows from operating activities using the direct

method, i.e. whereby major classes of gross cash receipts and gross cash payments cash-

flows from operating activities showed a surplus from receipts and payments

amounting to 410,5 MCHF. Net cash flows from investing activities, which included

personnel and materials expenses and the CHIS Fund capitalization (see paragraph

6.1.1), added to -412,8 MCHF and cash flows from financing activities accounted

for -101,7 MCHF. As a consequence, the net decrease in cash and cash equivalents

was 104,0 MCHF; by adding cash and cash equivalents at the beginning of period

(146,7 MCHF), it led to cash and cash equivalents amounting to 42,7 MCHF as at 31

December 201227 .

We checked the underlying entries by selecting samples from some accounts. The

result was that all transactions chosen were properly backed-up by supporting

documentation. The Cash Flow Statement is thus verified and confirmed.

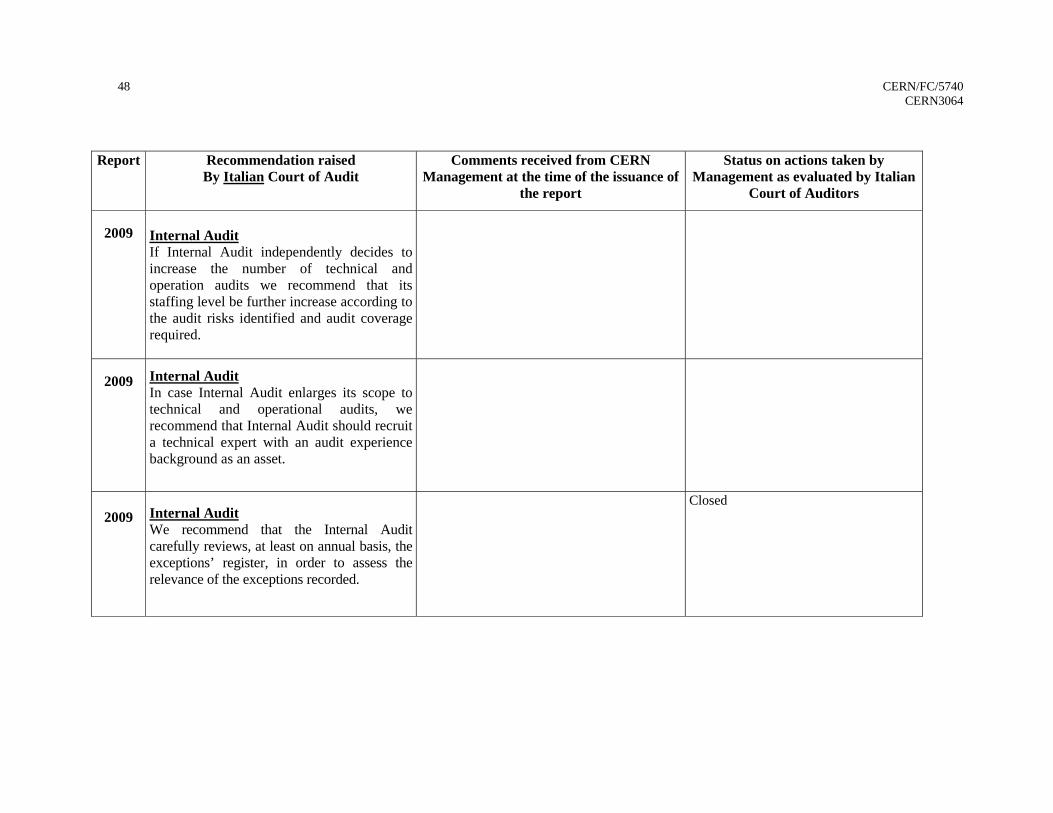

11. INTERNAL AUDIT SERVICE

In May 2013, at the time of our reporting, as last year, the Internal Audit Service (IA)

was composed of 3 auditors with a staffing level equivalent to 3 FTEs. In addition,

the IA was assigned a part-time (20%) secretarial resource.

We can confirm that, throughout our mandate, the IA provided the necessary

support to the External Auditors for the conduct of their mission, providing

technical help with CERN specific systems and tools and acting as a primary

contact with the Organization.

Internal Audit's main role is to provide an independent assurance to the Director-

General and Management and, indirectly so, to the Council, on the risk

management, control and governance processes of the Organization. Beyond the

support and technical help that IA provides to them, IA's full and free access to the

External Auditors and the CERN Standing Advisory Committee on Audits is an

additional guarantee of Internal Audit's independence.

27 Refer to paragraph 6.1.2 Current Assets.

CERN/FC/5740 31CERN/3064

12. FOLLOW-UP OF RECOMMENDATIONS 2006 - 2011

Following the request of the Council regarding the examination and adoption of the

External Auditors' past recommendations, we have reviewed the External Auditors

reports of the Austrian Court of Audit for the period of time from 2004 to 200728 and

the corresponding comments by the Management29.

Annex 1 collects all the audit recommendations issued by the Austrian Court of

Audit and/or by us in our 2008, 2009, 2010 and 2011 Reports that are still considered

as “not implemented” or “in progress”. When needed for clarity, similar

recommendations have been grouped with the indication in the first column of the

table of the years concerned.

In addition, Annex 1 also includes the comments received from CERN Management

at the time of the issuance of the corresponding Report and the latest status on

actions taken by Management.

It appears that most of our predecessors' recommendations, as well as the

recommendations we issued, have been implemented; therefore we appreciate the

willingness and attention of the Management to improve the effectiveness and

efficiency on financial and administrative matters.

28 See CERN/2559 - CERN/FC/4810, CERN/2609 - CERN/FC/4923, CERN/2668 - CERN/FC/5043, CERN/2721 - CERN/FC/5140, CERN/2788 - CERN/FC/5246. 29 See CERN/2560 - CERN/FC/4811, CERN/2610 - CERN/FC/4924, CERN/2669 - CERN/FC/5044, CERN/2722 - CERN/FC/5141, CERN/FC/5529 -CERN/2965.

32 CERN/FC/5740 CERN3064

ANNEX 1

Report Recommendation raised

By Austrian Court of Audit Comments received from

CERN Management at the time of the issuance of

the report

Status on actions taken byManagement as reported

by Austrian Court of Audit

Status on actions taken by Management as evaluated by

Italian Court of Auditors

2006

2007

2008

2009

2010

2011

Long-term debts a) Ppbar contributions: the External Auditors recommended entering into negotiations with the Member States concerned to write-off the outstanding amounts.

The Management accepted the recommendation and will take the necessary steps.

The Management has sent a letter in April 2013 to the Member States concerned in order to find a mutually acceptable solution to settle the outstanding amounts.

In progress

2006

Funds and Reserves Other Reserves (CHIS):

b) The External Auditors recommended to consider the assignment of the Health Insurance Scheme to the insurance company in full.

a) The Management will issue a new market survey to evaluate the possibility of a complete outsourcing of the insurance risk.(2006)

a) Ongoing - A market survey have been performed.

In progress Refer also to our recommendation in paragraph 6.1.1 b). Moreover, the fact to out-source the risk in full should be considered at legal level.

CERN/FC/5740 33 CERN/3064 Report Recommendation raised

By Italian Court of Audit Comments received from CERN

Management at the time of the issuance ofthe report

Status on actions taken by Management as evaluated by Italian

Court of Auditors

2009

2010

2011

“Statement of Comparison of Budget and Actual amounts” in part 1 of the Annual accounts …even though we are aware that the Management produces the Annual Progress Report (APR) - a document where such deviations are explained by “project or activity” and not by “nature” - we renew our recommendation to make more extensive use of the descriptive notes in the Annual Accounts, in order to explain all major variations between the budgeted and actual amount figures. Considering that detailed explanations concerning variations and deviations by “project or activity” are already enclosed in the APR, we recommend to the Management to enhance the level of descriptions in Part 1 of the Annual Accounts of variations by “nature”, providing more details on the reason why variations and deviations occurred.

Significant efforts have been made in order to improve and enhance the explanations on deviations in the APR as well as the references between the Annual Accounts and the APR. Furthermore, tables in the APR and Annual Accounts have been harmonized and provide now a clear and direct link between the APR and the Annual Accounts. Additional explanations on variations and deviations have been added in Part I (budget out-turn) of the 2012 Annual Accounts.

Closed

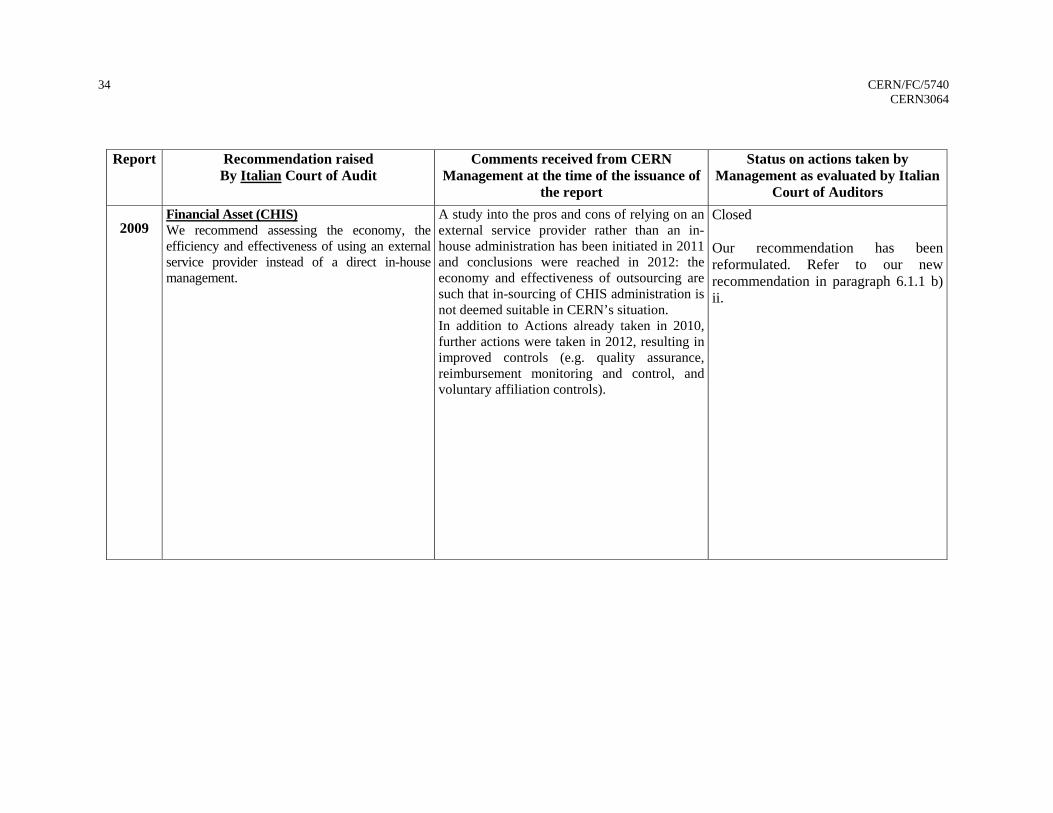

34 CERN/FC/5740 CERN3064

Report Recommendation raised By Italian Court of Audit

Comments received from CERN Management at the time of the issuance of

the report

Status on actions taken by Management as evaluated by Italian

Court of Auditors

2009

Financial Asset (CHIS) We recommend assessing the economy, the efficiency and effectiveness of using an external service provider instead of a direct in-house management.