Corso di Ristrutturazione delle imprese - uniroma1.it cause e le tipologie di ristrutturazione...

76

Corso di Ristrutturazione delle imprese

Transcript of Corso di Ristrutturazione delle imprese - uniroma1.it cause e le tipologie di ristrutturazione...

Corso di Ristrutturazione delle imprese

Programma del corso

Le cause e le tipologie di ristrutturazione aziendale (V.libro di testo)

Modalità di gestione le ristrutturazioni

Analisi dei processi relativi alle ristrutturazioni

Strategic Redirection

Merger & Acquisition (M&A)

Major investments

Divestments

2

Le modalità di gestione delle ristrutturazioni

all’interno delle imprese

Enhanced Project Management (EPM)

EPM is a user-friendly, gated process based on best practices;

Broad goal: provide a structured process for managing mega-scale projects;

Key components for capital projects include:

o Phased system covering all vital processes, focused on front-end loading o Assurance reviews to leverage company knowledge o Development support packages to provide best information to decision

makers o End of project reviews to facilitate lessons learned o Structured performance measurement o Continual risk and stakeholder management

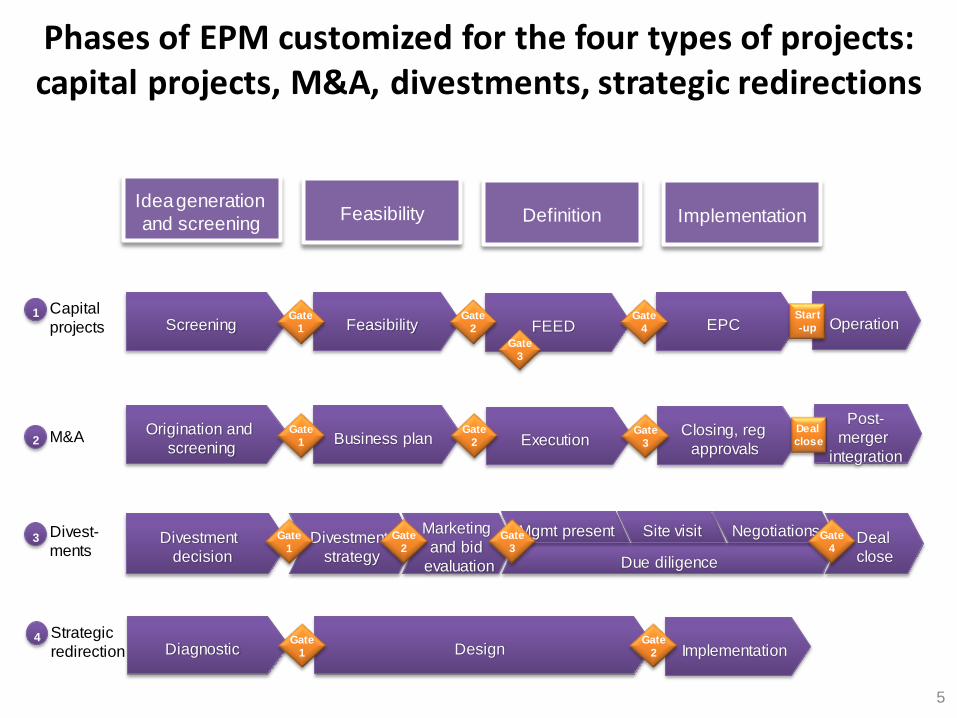

Separate processes for capital projects, M&A and divestments, Strategic redirections

4

Marketing

and bid

evaluation

Phases of EPM customized for the four types of projects: capital projects, M&A, divestments, strategic redirections

Feasibility Definition Implementation

Operation Screening Feasibility FEED EPC Start

-up

Divestment

decision

Divestment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

4

Post-

merger

integration

Origination and

screening Business plan Execution

Closing, reg

approvals

Deal

close

Capital

projects

M&A

Divest-

ments

Idea generation

and screening

1

2

3

Gate

1

Gate

2 Gate

3

Gate

1

Gate

3

Gate

2

Gate

1

Gate

2

Gate

4

Gate

3

Diagnostic Design Implementation Strategic

redirection 4 Gate

1

Gate

2

5

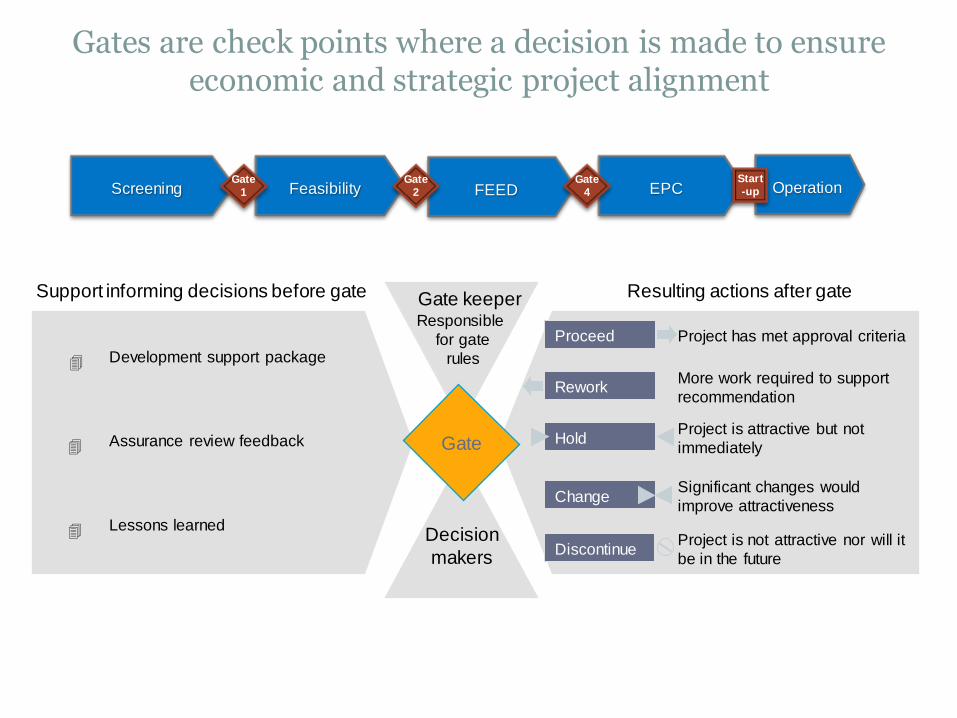

Gates are check points where a decision is made to ensure economic and strategic project alignment

Project has met approval criteria

More work required to support

recommendation

Project is attractive but not

immediately

Significant changes would

improve attractiveness

Project is not attractive nor will it

be in the future

Proceed

Rework

Hold

Change

Discontinue

Gate keeper Responsible

for gate

rules

Gate

Development support package

Assurance review feedback

Lessons learned

Support informing decisions before gate Resulting actions after gate

Decision

makers

Overview

Operation Screening Feasibility FEED EPC Start

-up Gate

1

Gate

2

Gate

4

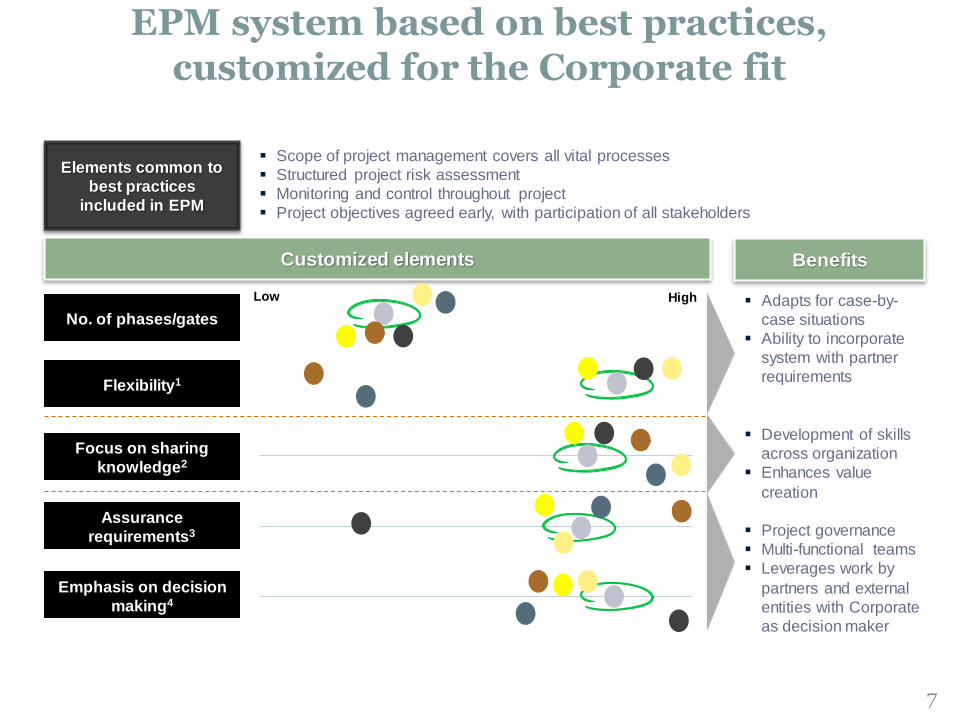

Scope of project management covers all vital processes

Structured project risk assessment

Monitoring and control throughout project

Project objectives agreed early, with participation of all stakeholders

EPM system based on best practices, customized for the Corporate fit

No. of phases/gates

Flexibility1

Focus on sharing

knowledge2

Assurance

requirements3

Emphasis on decision

making4

Elements common to

best practices

included in EPM

Customized elements Benefits

Low High Adapts for case-by-

case situations

Ability to incorporate

system with partner

requirements

Development of skills

across organization

Enhances value

creation

Project governance

Multi-functional teams

Leverages work by

partners and external

entities with Corporate

as decision maker

7

Performance Measurement

8

• Expected secured volume

• Capex

• Capex/barrel

• IRR

• Cost

– VOWD

– Estimated total costs

• Schedule

– Physical progress

– Estimated

completion date

• Grow shareholder value

through:

– Secure long term

disposal of national

hydrocarbons

– Investing in high growth

strategic markets

– Enter into economically

viable investment

opportunities in JV

– Integrate into profitable

associated downstream

activities

KPM definition: BD strategic objective and key challenges

Strategic objectives1 Key challenges

• Select few promising opportunities

which maximize national crude long

term disposal while meeting acceptable

level of strategic fit2

• Efficiently perform fit-for-purpose

feasibility analysis to support decision

making and opportunity sanction

• Progress projects through development

phases and deliver a fully operating

asset meeting time, cost and quality

targets

Proposed KPMs

Project specific

Corporate level

9

Lessons learned

10

Disseminating company

wide knowledge

through lessons learned

to

Project personnel

Corporate staff

JV staff and

partners

Formal part of DSP

Administrator regulates

access to knowledge

sharing database

Transforming raw

knowledge into a form

that can be easily shared

via lessons learned

Storing/maintaining

lessons learned in central

database

Administrator must

maintain structure/

organization of lessons

learned in system

By phase

Lessons learned are critical part of knowledge management process Knowledge management process

Codification Application

Feedback

Acquisition of

knowledge Dissemination

Translating learnings to

current context or

project

•Continual improvement

of the system

Identifying lessons

learned on current and

past projects by all levels

of staff

Within Corporate

From JVs, partners

or external

benchmarks

Administrator provides

quality check and control

for lessons learned/

documents in knowledge

sharing system

11

EPM Administration

12

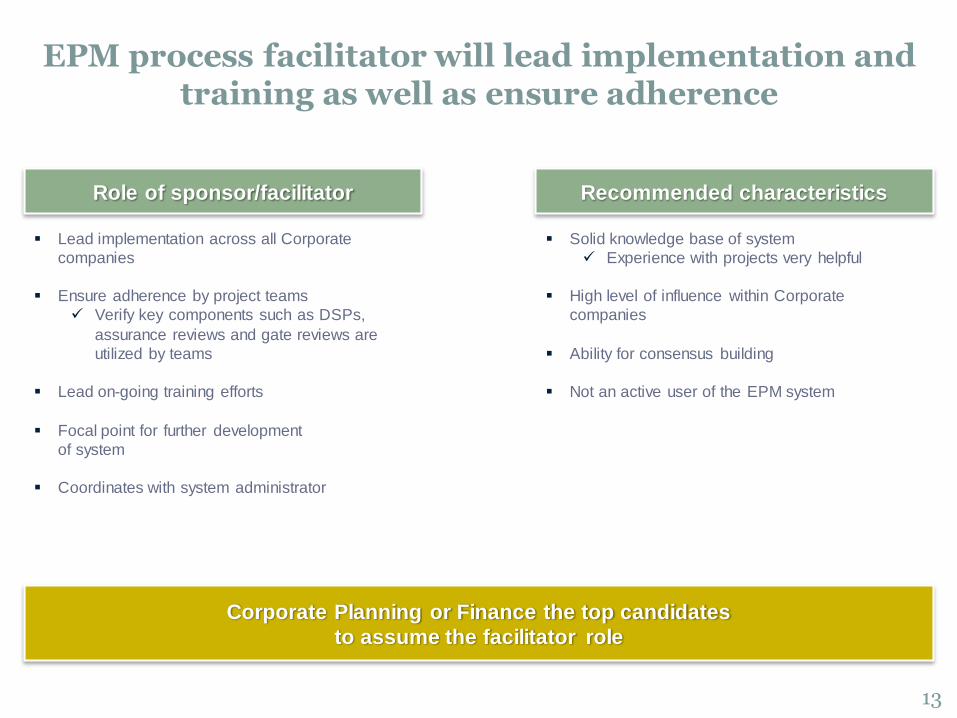

Solid knowledge base of system

Experience with projects very helpful

High level of influence within Corporate

companies

Ability for consensus building

Not an active user of the EPM system

Lead implementation across all Corporate

companies

Ensure adherence by project teams

Verify key components such as DSPs,

assurance reviews and gate reviews are

utilized by teams

Lead on-going training efforts

Focal point for further development

of system

Coordinates with system administrator

EPM process facilitator will lead implementation and training as well as ensure adherence

Role of sponsor/facilitator Recommended characteristics

Corporate Planning or Finance the top candidates

to assume the facilitator role

13

Le ristrutturazioni legate

a un nuovo assetto strategico

14

Marketing

and bid

evaluation

Feasibility Definition Implementation

Operation Screening Feasibility FEED EPC Start

-up

Divestment

decision

Divestment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

4

Post- merger

integration

Origination and

screening Business plan Execution

Closing, reg

approvals

Deal

close

Capital

projects

M&A

Divest-

ments

Idea generation

and screening

1

2

3

Gate

1

Gate

2 Gate

3

Gate

1

Gate

3

Gate

2

Gate

1

Gate

2

Gate

4

Gate 3

Diagnostic Design Implementation Strategic

redirection 4 Gate

1

Gate

2

15

Phases of EPM customized for the four types of projects: capital projects, M&A, divestments, strategic redirections

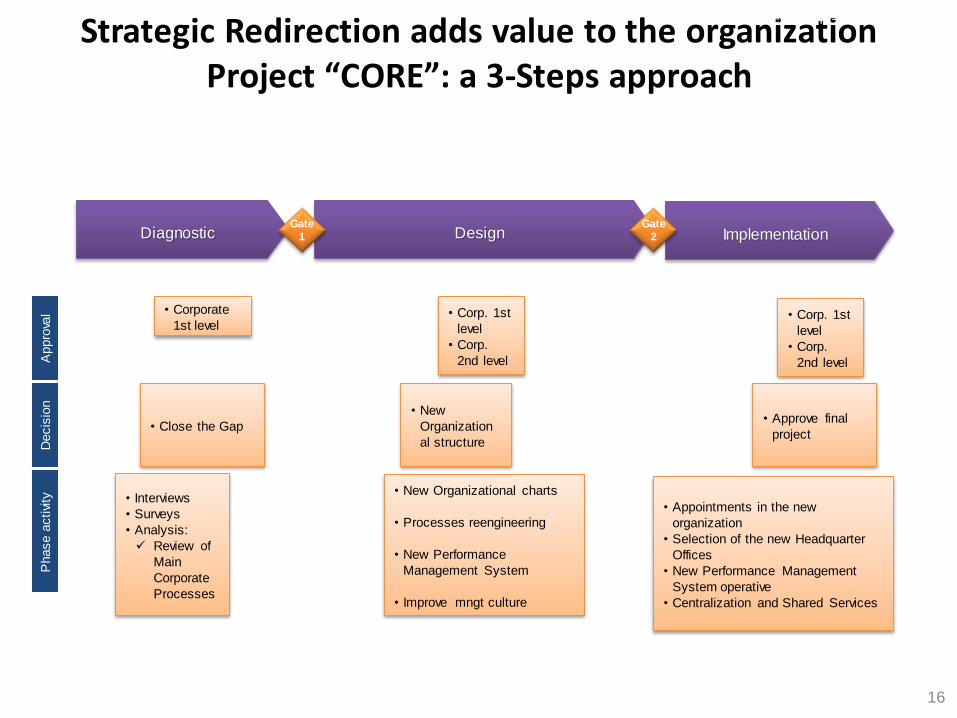

Strategic Redirection adds value to the organization Project “CORE”: a 3-Steps approach

• Interviews

• Surveys

• Analysis:

Review of

Main

Corporate

Processes

• New Organizational charts

• Processes reengineering

• New Performance

Management System

• Improve mngt culture

Phase a

ctivi

ty

Decis

ion

Appro

val • Corporate

1st level • Corp. 1st

level

• Corp.

2nd level

• Close the Gap • Approve final

project

Divestment — overview

• New

Organization

al structure

Diagnostic Design Implementation Gate

1

Gate

2

• Corp. 1st

level

• Corp.

2nd level

• Appointments in the new

organization

• Selection of the new Headquarter

Offices

• New Performance Management

System operative

• Centralization and Shared Services

16

Mergers & Acquisitions (M&A)

M&A overview M&A process usually completed in condensed timeframe with high level of confidentiality

M&A — overview

Pha

se

activi

ty

• Post

merger

integration

• Deal closing/signing

• Regulatory

approvals

• Due diligence,

final valuation

• Negotiations

• Structure

transaction

• Documentation

• Economic and

technical

evaluation

• Strategic due

diligence

• Strategic fit

• Generate ideas

• Review inbound

opportunities

• CA signed • Initial bid/non-

binding term-sheet • Bid

Ap

pro

val

• Corp. 1st

level • Corp. 1st level

• Shareholder

Board

• Corp. 2nd level

• Corp. 1st level

• Shareholder

Board

De

cis

ion

• Asset strategic;

explore options

• Approve

merger/

acquisition

• Approve final

price and

structure – as

required

Post Merger

Integration Origination and

Screening

Target

Assessment Execution Closing

Deal

close

Gate

1

Gate

2

Gate

3

Deals Opportunities

M&A — origination and screening phase

Screening phase in M&A includes origination activities and target assessment

Phase objective

To identify targets with the best strategic fit

Profile target company/asset

Complete Confidentiality Agreement

Key resource and funding decisions Commit internal and external resources for Target assessment

Decision makers

Corporate Major Project Committee

Cost/Valuation estimates

Preliminary figures based on market value or industry comparables

Phase deliverables

Checklist

Recommended timing

Origination is a continual exercise. Thorough target profiling can take over eight weeks, however actual timeframes are shorter in many cases

M&A — overview

Post Merger-

Integration Origination and

Screening

Target

Assessment Execution Closing

Deal

close

Gate

1

Gate

2

Gate

3

Key questions to answer in screening phase

Business fundamentals

What does the company do? What is the business model?

Is there a key technology or competitive edge?

Strategic rationale for acquisition

Does the company have a strong position a target industry? Which gap in our portfolio does it fill?

How does this deal generate more revenue as a combined entity than as two separate ones? How does it lower costs?

How does this deal strengthen our position against existing and new competitors?

What do you perceive as the key risks of this acquisition?

How would the acquisition impact our other businesses and/or sister k-companies?

Financials

What are the company’s revenues, EBITDA, net income? Their growth rate?

What is the company’s market cap, P/E, stock price development? (For public targets)

What is the preliminary valuation estimate (ballpark number)?

Acquisition information

How do we know this company? Who do we know, and how well?

What is the likelihood of success? Are there other bidders in the game? What is the likely timeline?

Are there any critical items which may cause delay in deal closing (eg, labor laws, local laws, regulatory requirements)?

Who should have access to deal information? How is the confidentiality of all parties and documents retained?

M&A — overview

Strategic fit key criteria during screening phase

Profile of target provides basis of knowledge to team and decision makers

Executive summary Acquisition pros and cons

Fact sheet

Location of facilities, history, ownership structure, organizational structure and breakdown of business units by geography

Products

Market position, sales, historical growth and projections Combined portfolio matrix Key customer segments, competitors and degree of industry rivalry Financial performance

Asset size, market capitalization, stock price performance, revenue, profit, cash flow and growth projections

Core capabilities and potential value of patents/technologies/R&D Profile of management team Potential risks

Lawsuits, pension plans, changing market trends, etc

M&A — overview

High-level profiles also allow acquirer to rank top candidates on key dimensions

= Unattractive = Highly attractive

After high-level profiles are developed, acquirer’s top management must

decide which targets to investigate further

Candidate 1

Candidate 2

Candidate 3

Candidate 4

Candidate 5

Mgmt

Financial

performance Products

Combined

portfolio

Customers

and competition

Core

capabilities Potential

liabilities

= Moderately attractive

M&A — overview

M&A - Target Assessment

Target Assessment phase focuses on financial valuation and market assessment

Phase objective

Financial evaluation from multiple valuation techniques

Start strategic diligence/market assessment

To establish sound and robust set of assumptions for financial valuation

Initial bid/non-binding term sheet

Key resource and funding decisions

Approve the entire deal (in concept)

Fund internal and external resources for next phase

Decision makers

Major Project Committee

Cost/Valuation estimates

Range based on triangulation of different valuation techniques (DCF, recent transaction multiples, publicly traded comparables)

Phase deliverables

Checklist

M&A — overview

Post Merger-

Integration Origination and

Screening Target

Assessment Execution Closing

Deal

close

Gate

1

Gate

2

Gate

3

• Result depends on quality of assumptions – Cash flows – Discount rate – Terminal value

• Lack of company specific data for inputs

• Complexity

• No company completely comparable to another

• Transaction prices not often applicable – Prices reflect value-creation through synergies – Acquisition price is company specific

• Usually provides wide range of values

• No company completely comparable to another – Different business mixes, capabilities,

performance and growth prospects – Different accounting methods

• Usually provides wide range of values

• Compare ratios of recent transactions to target – Earnings multiples – Cash-flow multiples – Asset multiples – Sales multiples – Other multiples

• Compare financial ratios of public firms to target – Earnings multiples – Cash-flow multiples – Asset multiples – Sales multiples – Other multiples

Method Description Advantage Disadvantage

Valuation range should be determined by multiple methods

• Publicly

traded

comparables

• Simple, transparent

Cash flow

Investment

Residual value

• Recent

transaction

comparables

• Simple, transparent

• Discounted

cash flow

(DCF)

• Usually more

accurate than

comparables

analysis

1

2

3

M&A — overview

Target assessment process determines valuation range Process performed in four distinct steps

Stand Alone

Evaluation

• Market and

competition

• Products and pricing

• Cost structure

• Capabilities and

processes in R&D,

distribution, marketing,

sales, operations

• Resources

• Key success factors

• Culture and

management

strengths

• Finance, legal and tax

issues

• IT systems

Independent growth

prospects

• Market growth

• Competitive shifts

• Organic growth plans

• New product and

pricing strategies

• Technological and

regulatory trends

• Risk factors

• Business model

stability

Combined

prospects (Synergies)

• Potential along

merged value chain

• Revenue synergies

• Cost synergies

• Financing synergies

• Managerial synergies

• Market synergies

• Future options

provided

• Integration needed to

achieve synergies

• Costs of integrating

the companies

Feasibility

• Internal resources

• Investments required

• Financing capability

• Culture and

organizational issues

• People retention

• Management team

• Integration needs

• Other bidders

• Competitive response

1 2 3 4

Initial data input into financial model from available

sources; to be clarified/updated during due diligence

M&A — overview

Stand alone evaluation covers all relevant areas of target (I) Target assessment step 1

Market

• Market size and development

• Profitability

• Sales and pricing structure

• Market cycles

• Growth trends

• Barriers to entry

• Customer mix and behavior

• Buying patterns

• Historical and future trends

• Analysis by

regions/geographies

Products

• Product portfolio

• Sales volumes and trends

• Cost position

• Price position

• Level of differentiation

• Quality

• Branding, image

Marketing, sales

• Marketing capabilities

• Sales organization

• Channel access and

development

• Advertising and

promotion strategies

Competition

• Analysis of major players

• Strengths and weaknesses

• Sources of advantage

• Profitability

• Market share trends

• Relative price levels

• Likely responses to acquisition

• Competitive forces

• Possible new entrants or new

business models

Operations

• Production facilities and

equipment

• Maintenance and investments

• Supply contracts, partnerships

• Cost structures

• Capacity

Distribution, logistics

• Distribution system and

capabilities

• Logistics

• Trends in distribution and

logistics

• Speed, flexibility and quality

M&A — overview

Align internal and external assumptions and forecasts

Independent growth assessment reviews plan of target Target assessment step 2

Identify and evaluate

internal growth plans and

assumptions

• Future plans

• Internal strengths and

weaknesses

• Internal processes

• Human resources

• Investments and financial

resources

• Operational capacities

Define and verify

assumptions on market and competition

• Market structure and trends

• Cyclicality

• Strategy and positioning

• Change in customer needs

• New entries or exits

• Competitor reactions

Define and verify

assumptions on market and competition

Rev

Realistic range of growth assumptions to be included in

financial valuation

M&A — overview

Value creation depends on

ability to realize synergies

Combined prospects values potential synergies Target assessment step 3

Operating synergies

• Potential synergies exist in all

steps of the value chain from

R&D to after-market service

Financial synergies

• Acquisitions may provide tax

shields, improved credit rating,

access to capital, etc

Managerial synergies

• Acquisitions can improve

management practices

• Can provide additional talented

managers

Market-evaluation

reassessment

• Market may view the acquirer

as a survivor in a consolidating

industry

Realistic expectations of synergies should be included in

financial valuation

M&A — Overview

Source: BCG experience; adaptation of Chakravarty in Business Today, March 1998

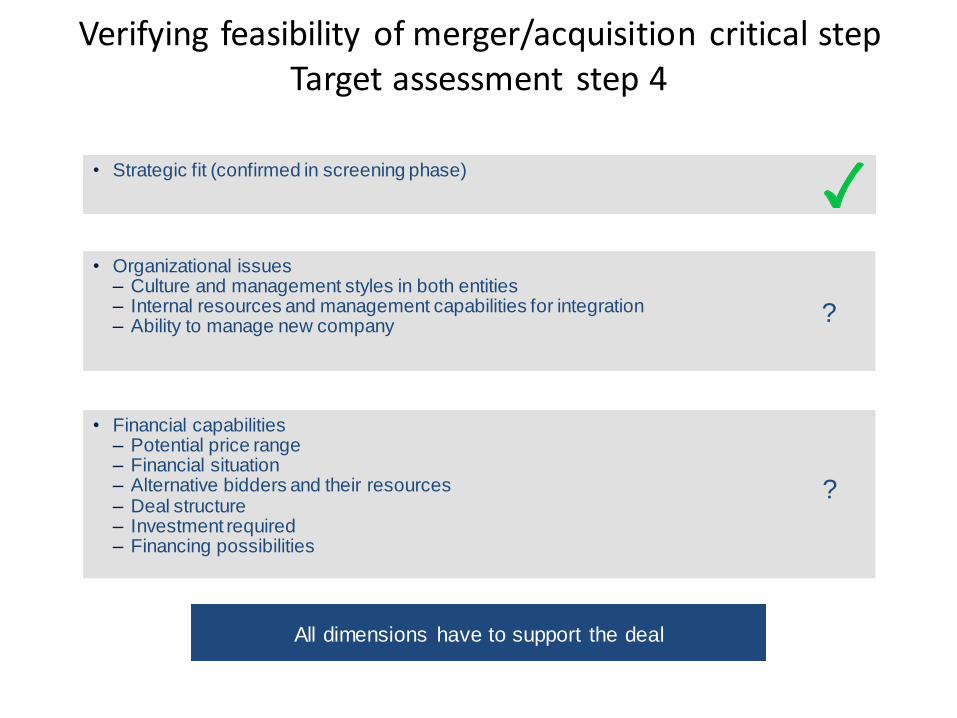

• Financial capabilities – Potential price range – Financial situation – Alternative bidders and their resources – Deal structure – Investment required – Financing possibilities

• Organizational issues – Culture and management styles in both entities – Internal resources and management capabilities for integration – Ability to manage new company

• Strategic fit (confirmed in screening phase)

?

?

M&A — overview

All dimensions have to support the deal

Verifying feasibility of merger/acquisition critical step Target assessment step 4

M&A — Execution

• Phase objective

– Determine final range of valuations for bidding

– Finalize due diligence efforts on all aspects of target

– Structure transaction

– Determine deal terms through negotiations

• Key resource and funding decisions

– Final investment Decision

• Decision makers

– KPI Major Project Committee, Aruba, KPC (as necessary)

• Cost/Valuation estimates

– Range based on triangulation of different valuation techniques (DCF, recent transaction multiples, publicly

traded comparables)

• Phase deliverables

– Checklist

Execution in M&A performs due diligence effort, provides range of valuations for FID and negotiates terms

M&A — overview

Post-merger

integration Origination and

screening

Target

assessment Execution Closing

Deal

close Gate

1

Gate

2 Gate

3

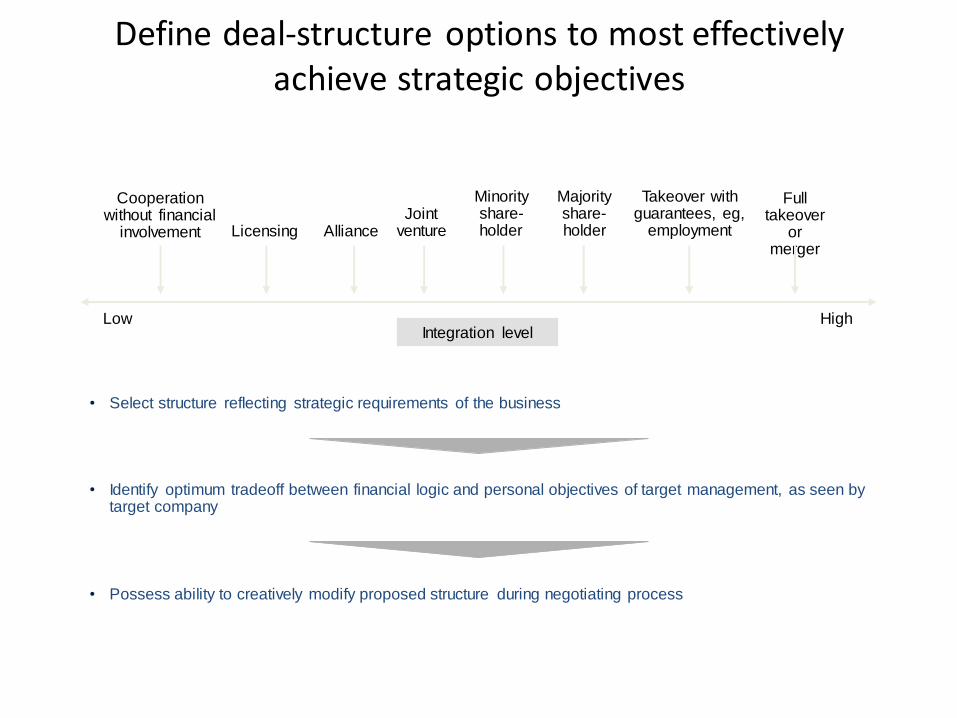

Minority share-holder

• Select structure reflecting strategic requirements of the business

High

Full takeover

or merger

Takeover with guarantees, eg,

employment

Majority share-holder

Joint venture Licensing

Cooperation without financial

involvement

Integration level Low

Alliance

Define deal-structure options to most effectively achieve strategic objectives

• Identify optimum tradeoff between financial logic and personal objectives of target management, as seen by target company

• Possess ability to creatively modify proposed structure during negotiating process

M&A — overview

• Management structure – Board structure – Individual manager and board

member roles

• Organizational details – Name, logo, branding – Location of headquarters – Organization of businesses

• Post-merger integration planning

• Confirm strategic and operational logic – Gather additional data and insight

• Refine synergy estimates and financial evaluation

• Assess management, culture and organizational capabilities and fit

• Monitor and respond to other bidders and key stakeholders

3. Determining key aspects

of the new entity

4. Drafting the contract

Represe

n-tations

Indemnities

Conditions

Covenants

Price

Friendly Hostile

1. Make the approach

2. Refine and understand

Manage

the human

context and

balance of

power

issues

Strategic focus should be kept during deal negotiations Deal negotiation components

M&A — overview

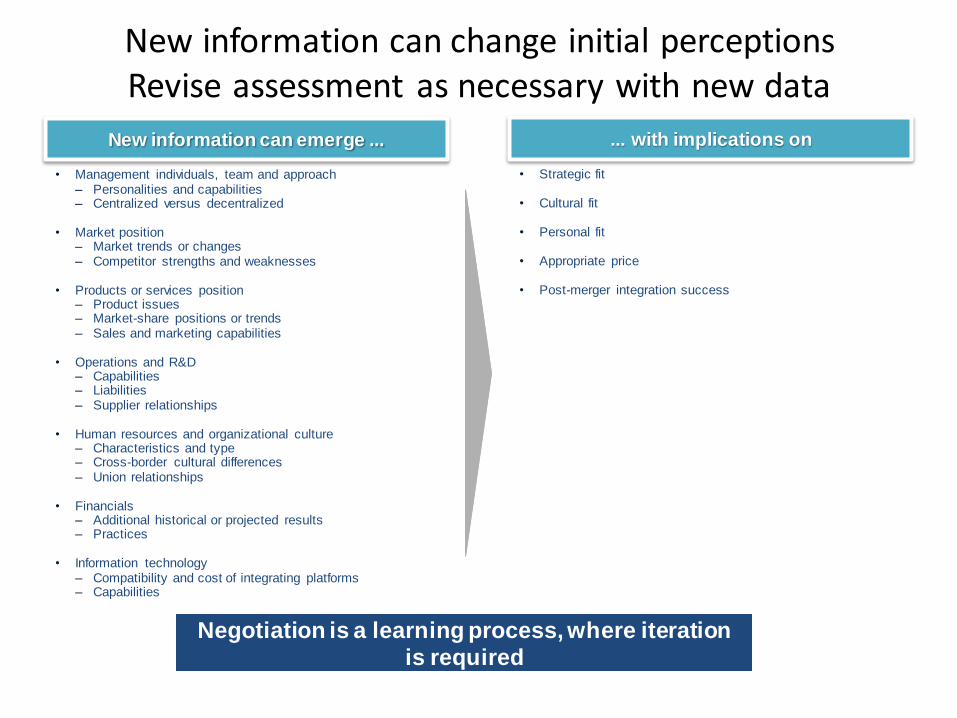

• Management individuals, team and approach – Personalities and capabilities – Centralized versus decentralized

• Market position – Market trends or changes – Competitor strengths and weaknesses

• Products or services position – Product issues – Market-share positions or trends – Sales and marketing capabilities

• Operations and R&D – Capabilities – Liabilities – Supplier relationships

• Human resources and organizational culture – Characteristics and type – Cross-border cultural differences – Union relationships

• Financials – Additional historical or projected results – Practices

• Information technology

– Compatibility and cost of integrating platforms – Capabilities

New information can emerge ... ... with implications on

• Strategic fit • Cultural fit • Personal fit • Appropriate price • Post-merger integration success

Negotiation is a learning process, where iteration

is required

New information can change initial perceptions Revise assessment as necessary with new data

M&A — overview

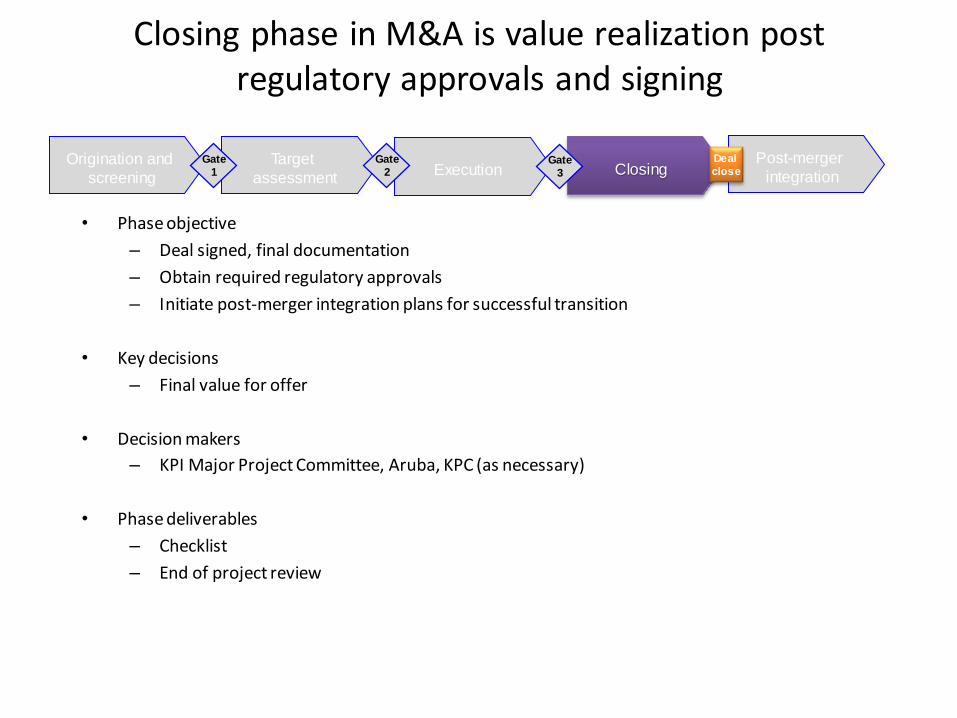

M&A — Closing phase

Closing phase in M&A is value realization post regulatory approvals and signing

• Phase objective

– Deal signed, final documentation

– Obtain required regulatory approvals

– Initiate post-merger integration plans for successful transition

• Key decisions

– Final value for offer

• Decision makers

– KPI Major Project Committee, Aruba, KPC (as necessary)

• Phase deliverables

– Checklist

– End of project review

M&A — overview

Post-merger

integration Origination and

screening

Target

assessment Execution Closing

Deal

close Gate

1

Gate

2 Gate

3

• Start actual implementation – Transfer responsibilities

to the line organization (BUs)

• Already involved as sponsors in phase 1

• Integration teams continue to push cross-BU topics

– Line organizations set up own integration teams

• Define detailed integration

performance and control measures – Break down integration

concept into detailed measures

• Setup tracking processes

– Eg, enter measures in tracking tool

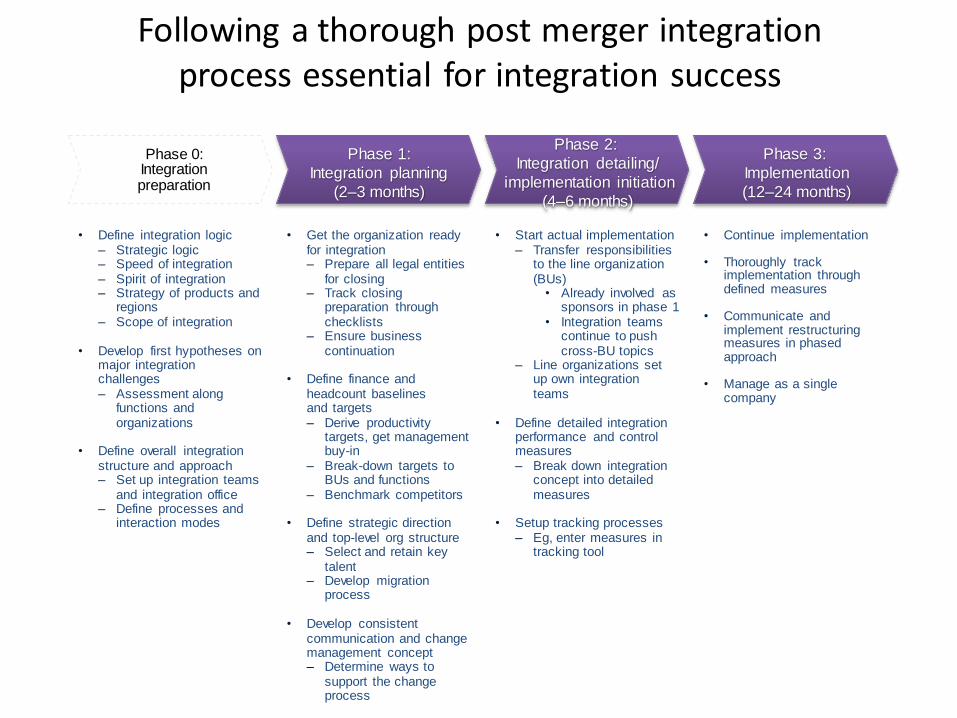

Following a thorough post merger integration process essential for integration success

Phase 3:

Implementation

(12–24 months)

Phase 0: Integration preparation

Phase 2:

Integration detailing/

implementation initiation

(4–6 months)

Phase 1:

Integration planning

(2–3 months)

• Continue implementation

• Thoroughly track implementation through defined measures

• Communicate and implement restructuring measures in phased approach

• Manage as a single company

M&A — overview

• Define integration logic – Strategic logic – Speed of integration – Spirit of integration – Strategy of products and

regions – Scope of integration

• Develop first hypotheses on major integration challenges – Assessment along

functions and organizations

• Define overall integration

structure and approach – Set up integration teams

and integration office – Define processes and

interaction modes

• Get the organization ready for integration – Prepare all legal entities

for closing – Track closing

preparation through checklists

– Ensure business continuation

• Define finance and

headcount baselines and targets – Derive productivity

targets, get management buy-in

– Break-down targets to BUs and functions

– Benchmark competitors

• Define strategic direction and top-level org structure – Select and retain key

talent – Develop migration

process

• Develop consistent communication and change management concept – Determine ways to

support the change process

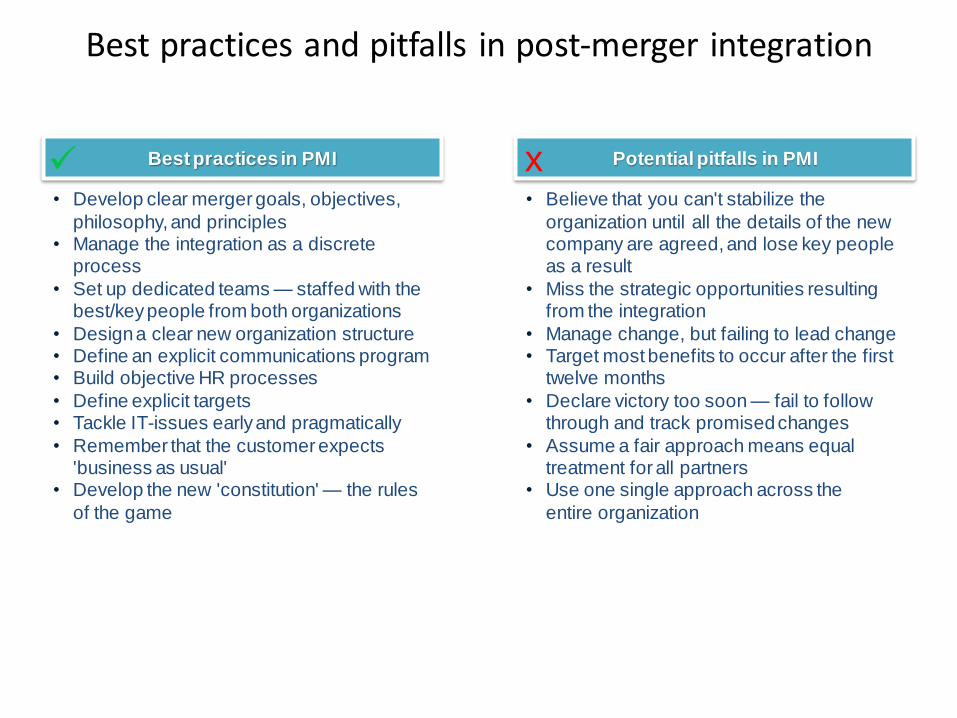

Best practices and pitfalls in post-merger integration

• Believe that you can't stabilize the

organization until all the details of the new company are agreed, and lose key people as a result

• Miss the strategic opportunities resulting from the integration

• Manage change, but failing to lead change • Target most benefits to occur after the first

twelve months

• Declare victory too soon — fail to follow through and track promised changes

• Assume a fair approach means equal treatment for all partners

• Use one single approach across the

entire organization

Best practices in PMI Potential pitfalls in PMI x • Develop clear merger goals, objectives,

philosophy, and principles • Manage the integration as a discrete

process

• Set up dedicated teams — staffed with the best/key people from both organizations

• Design a clear new organization structure • Define an explicit communications program • Build objective HR processes

• Define explicit targets • Tackle IT-issues early and pragmatically

• Remember that the customer expects 'business as usual'

• Develop the new 'constitution' — the rules

of the game

M&A — overview

• Project review is mandatory requirement

– Focus on lessons learned

– Increases opportunity for knowledge transfer and skill development

– Generates continual improvements to project management solutions

• Participants from all phases of project

– BD organizes and leads effort

– Representatives from assurance reviews, support functions, project team and operations

• Continual learning

– BD records and maintains all lessons learned

– Future projects should have open access to database/files

End of project review critical link for knowledge sharing Focus on lessons learned

End of

project

review

M&A — overview

Post-merger

integration Origination and

screening

Target

assessment Execution Closing

Deal

close Gate

1

Gate

2 Gate

3

Project review to occur for all projects

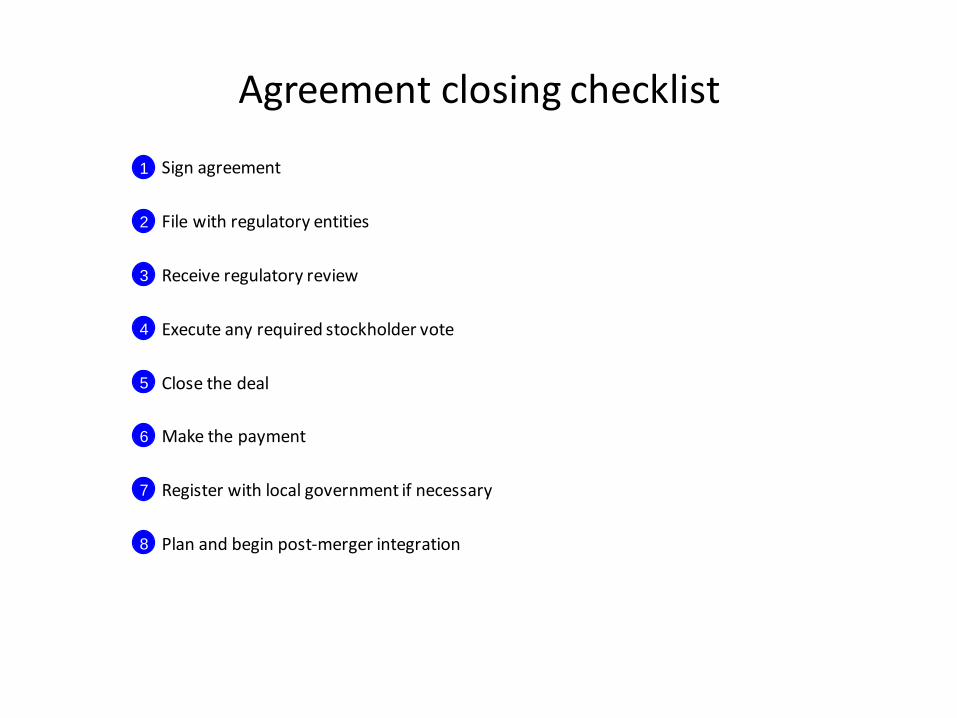

Agreement closing checklist

• Sign agreement

• File with regulatory entities

• Receive regulatory review

• Execute any required stockholder vote

• Close the deal

• Make the payment

• Register with local government if necessary

• Plan and begin post-merger integration

M&A — checklist

1

2

3

4

5

6

7

8

Capital projects

Operation

Capital Projects overview

Screening Feasibility FEED EPC

Projects

• Strategic fit

• Confirm national

crude status

• Basis of

design, FEED

• Engineering

procurement

construction

Phase a

ctivi

ty

Decis

ion

• Allocate

resources for

feasibility

• Approve

project;

• fund next

phase

• Final Investment

Decision (FID);

fund project

• Internal

check after

BOD

Start

-up Gate

1

Gate

2

Gate

3

Rew ork, Change,

Hold, Discontinue Proceed Rew ork, Change,

Hold, Discontinue Proceed

Rew ork, Change,

Hold, Discontinue Proceed

Appro

val

• Project originator/sponsor leads • Project team leads

• Project team assembled

• Operations

Role

Hand

over

JV1

• MOU signed • Major commercial

/Technical items finalized • JV agreements

finalized

Start

-up

• Corporate

1st level • Corporate 1st level

• Corporate 2nd level

• Economic and

technical evaluation

• On-going

operations

Opportunities

• Corporate

1st level

• Corporate 1st level

• Corporate 2nd level

• Identify risks and sort by

– Category

– Impact area

• Category

– Technical

– Commercial/market

– External (political, Fx, etc)

– Legal

– Resource/organizational

• Impact area

– People

– Environment

– Project objectives (Cost,

schedule, commercial)

– Company reputation

• Evaluate risk level

(qualitative and quantitative)

– Likelihood of occurrence

– Severity of impact

• Prioritize risk based on level

– High, Medium, Low

• Assess manageability

– High — within complete

control of project

– Medium — project

can influence

– Low — out of project’s

control or influence

• Define risk control strategy

– Avoid

– Mitigate

– Transfer or share

– Accept

• Develop action plan for managing

risks

– All data on risks

– Resources required

to manage

– Schedule of risk

mgmt activities

• Allocate tasks and responsibilities

– Risk tracking

– Reporting

– Closure

Risk assessment should be a structured, core activity throughout the process

Identify Evaluate Plan and control

Risk register Risk management plan

Screening Feasibility FEED EPC Gate

1

Gate

2

Gate

3

Risk assessment

Screening phase

Screening phase is critical to ensure correct projects selected for evaluation

• Phase objective – To establish opportunity can support economically attractive development

– Confirm alignment with strategic direction; – Agree main principles of agreement and/or sign MOU with partners

• Key resource and funding decisions – Commit internal and external resources for feasibility phase

• Decision makers – Corporate major project committee1

• Cost estimates – Preliminary figures based on industry comparables

• Phase deliverables – Development support package – Initiation of project performance measurement

• Recommended timing – Up to four months; however, it is critical unattractive projects are discontinued as soon as possible to free up

valuable resources

Overview

Operation Screening Feasibility FEED EPC Start

-up Gate

1

Gate

2

Gate

3

• Country or market fundamentals (Score from 0–4)

– Forecasted crude product deficit, netback

– Country risk, margins, competitive landscape

• Product volume (Score from 0–3)

• Opportunities along value chain for Corporate (Score

from 0–2)

• Calculate Corporate share of project

NPV

• Determine probability of success

– Review of risk register

– Review of stakeholder plan

– Assessment of partner relations

– Type (brownfield, grassroots)

– Business judgment

• Multiply NPV x probability

Prioritize projects by attractiveness and strategic importance Resources to be allocated against highest priority projects

Attractiveness:

probabilistic value per product

Strategic importance

Low

Score of 0

High

Score of 10

Low

High Highest priority

Fully allocate

internal

and external

resources (Full

feasibility)

Medium priority

Allocate internal

resources and

limited external

resources (Pre-

feasibility)

Lower priority

Allocate internal

resources only

when available

(Pre-feasibility

with internal

resources only)

Medium priority

Allocate internal

resources and

limited external

resources (Pre-

feasibility)

1

2

3

1

2

3

Prioritization process is a key management decision tool Priorities likely to change as projects are further developed

Low High Strategic importance

Low

High

Attractiveness

probabilistic value of product

($)

Total Corporate NPV

represented

as size of bubble

Project C

Project B

Project A

$200MM

Project D

Project E

Project prioritization helps allocate resources to the most

valuable projects

Corporate cross-functional team requirements vary by phase of work - Screening

Org and skills — 100% ownership

Skills

• Planning/strategy

• Commercial

• Finance and tax

• Project Controls

• Legal

• Process engineer

• Project engineer

• HSE

• Operations

Technic

al

Functio

na

l

Active involvement Little to no involvement

Screening Feasibility FEED EPC

Feasibility phase

52

Feasibility phase sets the course for project approval

• Phase objective

– To establish project is technically feasible and economically attractive

– Confirm alignment with strategic direction and all stakeholders

– Finalize majority of terms and agreements with JV partners

• Key resource and funding decisions

– Approve the entire project (in concept)

– Fund internal and external resources for FEED phase

– Fund initial procurement costs of critical long-lead items

• Decision makers

– Corporate Investment Committee, Shareholders Board

• Cost estimates

– +/- 30–40%

• Phase deliverables

– Development Support Package with Feasibility study

– Assurance review

• Recommended cumulative timing

– Up to 14 months for screening and feasibility phases

Overview

Operation Screening Feasibility FEED EPC Start

-up Gate

1

Gate 2

Gate

3

53

• Request formal confirmation1 from internal

stakeholders that

– No known factors make the project

completely unworkable for Corporate

• Confirmation of no potential showstoppers2

– Unacceptable country risk

– Unacceptable partners (local or IOC)

– Availability of product (quality,

timing, quantity)

– Beyond limits of current technology

• Note: This process is not to gain approval,

but to confirm the project basis is not

fundamentally flawed with current information

Formalized kick-off meeting with internal stakeholders helps to agree objectives and identify any showstoppers

Identify any showstoppers

Corp.

1st lvl

Corp.

2nd lvl

Other

• Project should

incorporate any

new information

into assessment

• If showstoppers

identified,

development

efforts put on hold

or discontinued

until issue

resolved

Other gate requirements

Operation Screening Feasibility FEED EPC Gate

1

Gate 2

Gate

3

Kick-off meeting introduces project scope,

objectives, and context to internal stakeholders

Start

-up

Potential stakeholders

FEED Phase

55

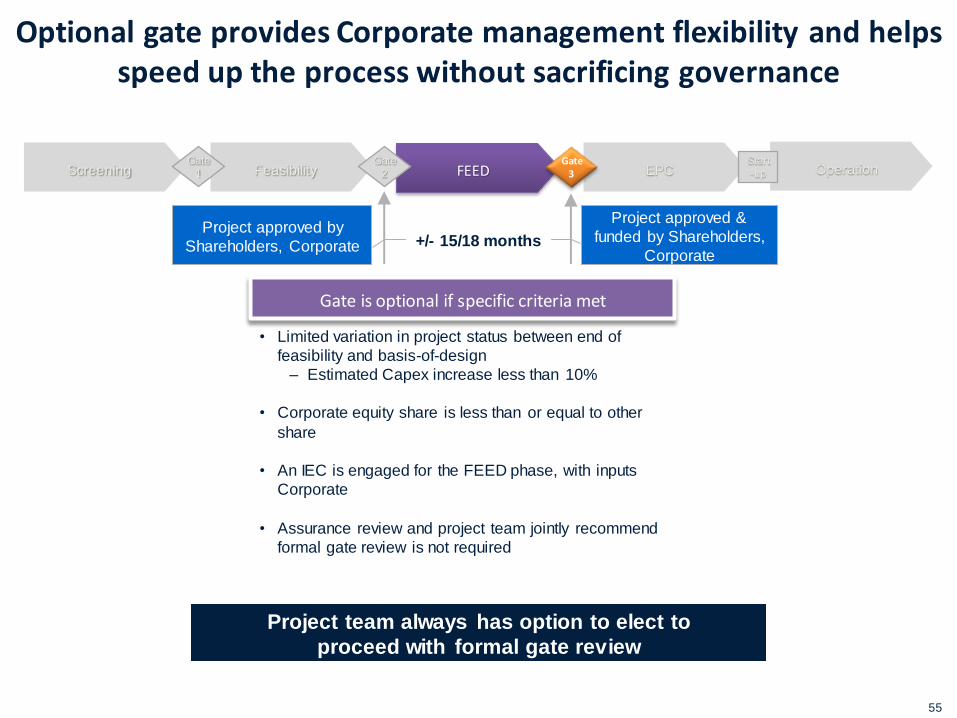

Optional gate provides Corporate management flexibility and helps speed up the process without sacrificing governance

Project team always has option to elect to

proceed with formal gate review

Gate is optional if specific criteria met

Operation Screening Feasibility FEED EPC Start

-up

Gate

1

Gate

2

Gate 3

Project approved by

Shareholders, Corporate

Project approved &

funded by Shareholders,

Corporate +/- 15/18 months

• Limited variation in project status between end of

feasibility and basis-of-design

– Estimated Capex increase less than 10%

• Corporate equity share is less than or equal to other

share

• An IEC is engaged for the FEED phase, with inputs

Corporate

• Assurance review and project team jointly recommend

formal gate review is not required

56

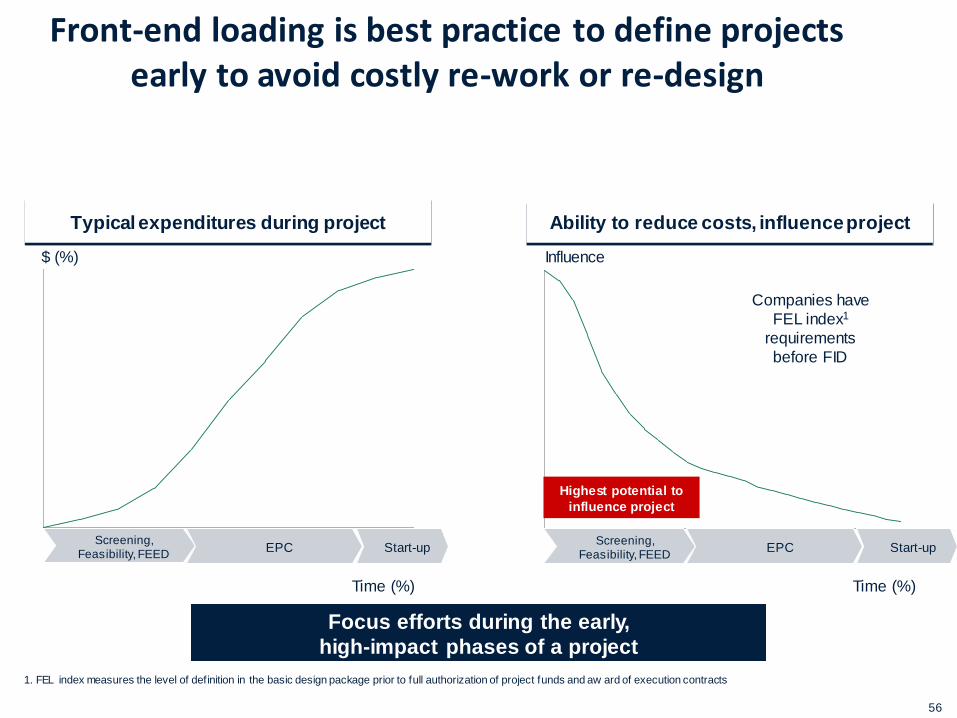

Front-end loading is best practice to define projects early to avoid costly re-work or re-design

$ (%)

Time (%)

Influence

Time (%)

Typical expenditures during project Ability to reduce costs, influence project

Highest potential to

influence project

Screening, Feasibility, FEED

EPC Start-up Screening,

Feasibility, FEED EPC Start-up

Companies have

FEL index1

requirements

before FID

Overview

Focus efforts during the early,

high-impact phases of a project

1. FEL index measures the level of definition in the basic design package prior to full authorization of project funds and aw ard of execution contracts

EPC phase

58

Value realization in the EPC phase

• Phase objective

– To deliver a world-class facility on schedule, under budget and without HSE incident

– Realization of product placement

• Key resources and funding decisions

– Approve and fund any significant variations from final cost estimates

• Decision makers

– Project steering committee and directorate for routine project management decisions

– If cost and/or schedule overrun occurs above thresholds outlined in Corporate guidelines, please refer to applicable Corporate policies

• Phase deliverables

– Hand-over commissioned facility to operating group

– End of project review

• Recommended cumulative timing

– Up to 68 months for screening, feasibility, FEED, and EPC phases

Overview

Operation Screening Feasibility FEED EPC Start -up

Gate 1

Gate 2

Gate 3

59

• Project review is mandatory requirement

– Focus on lessons learned

– Increases opportunity for knowledge transfer and

skill development

– Generates continual improvements to project

management solutions

• Participants from all phases of project

– BD organizes and leads effort

– Representatives from assurance reviews, support

functions, project team, and operations

• Continual learning

– BD records and maintains all lessons learned

– Future projects should have open access to

database/files

End of project review critical link for knowledge sharing Focus on lessons learned

Overview of project review

Other gate requirement

Operation Screening Feasibility FEED EPC Start -up

Gate 1

Gate 2

Gate 3

End of

project

review

Project review to occur for all projects, even those

that do not proceed to Operational phase

60

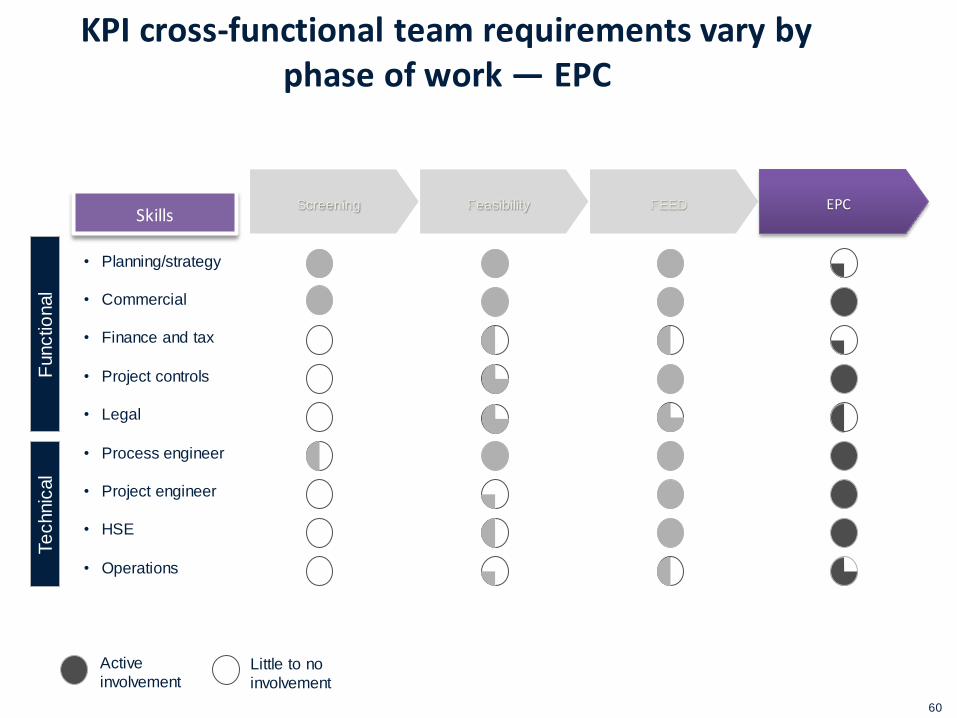

KPI cross-functional team requirements vary by phase of work — EPC

Skills

• Planning/strategy

• Commercial

• Finance and tax

• Project controls

• Legal

• Process engineer

• Project engineer

• HSE

• Operations

Te

chnic

al

Functio

nal

Active

involvement Little to no

involvement

Screening Feasibility FEED EPC

Divestments

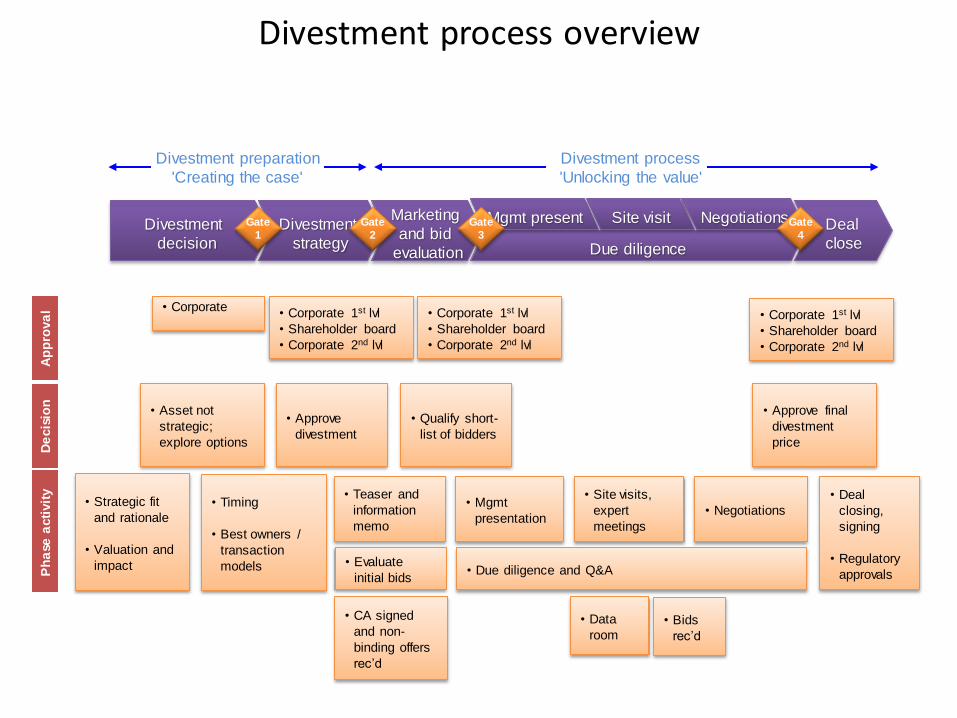

Divestment process overview

• Due diligence and Q&A

• Teaser and

information

memo

• Deal

closing,

signing

• Regulatory

approvals

• Strategic fit

and rationale

• Valuation and

impact

• Timing

• Best owners /

transaction

models

• Mgmt

presentation

• Site visits,

expert

meetings

• Negotiations

Ph

ase

acti

vit

y

De

cis

ion

A

pp

rova

l • Corporate

• Corporate 1st lvl

• Shareholder board

• Corporate 2nd lvl

• Asset not

strategic;

explore options

• Approve

divestment

• Approve final

divestment

price

Divestment — overview

• Evaluate

initial bids

• Qualify short-

list of bidders

• CA signed

and non-

binding offers

rec’d

• Bids

rec’d

• Data

room

Divestment process

'Unlocking the value'

Divestment preparation

'Creating the case'

Marketing

and bid

evaluation

Divestment

decision

Divestment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

1

Gate

4

Gate

3

Gate

2

• Corporate 1st lvl

• Shareholder board

• Corporate 2nd lvl

• Corporate 1st lvl

• Shareholder board

• Corporate 2nd lvl

Divestments — Exit decision

• Phase objective

– Robust rationale for divestment, focusing on lack of strategic fit

– Quantify valuation range

– Assess impact to current operations

• Key decisions

– Explore options for divestment

• Decision makers

– Corporate major project committee

• Phase deliverables

– Checklist

Lack of strategic fit initiates decision on divesting asset

Marketing and bid

evaluation

Divestment

decision

Divest- ment

strategy

Deal close

Due diligence

Mgmt present Site visit Negotiations Gate

1

Gate

4

Gate

3

Gate

2

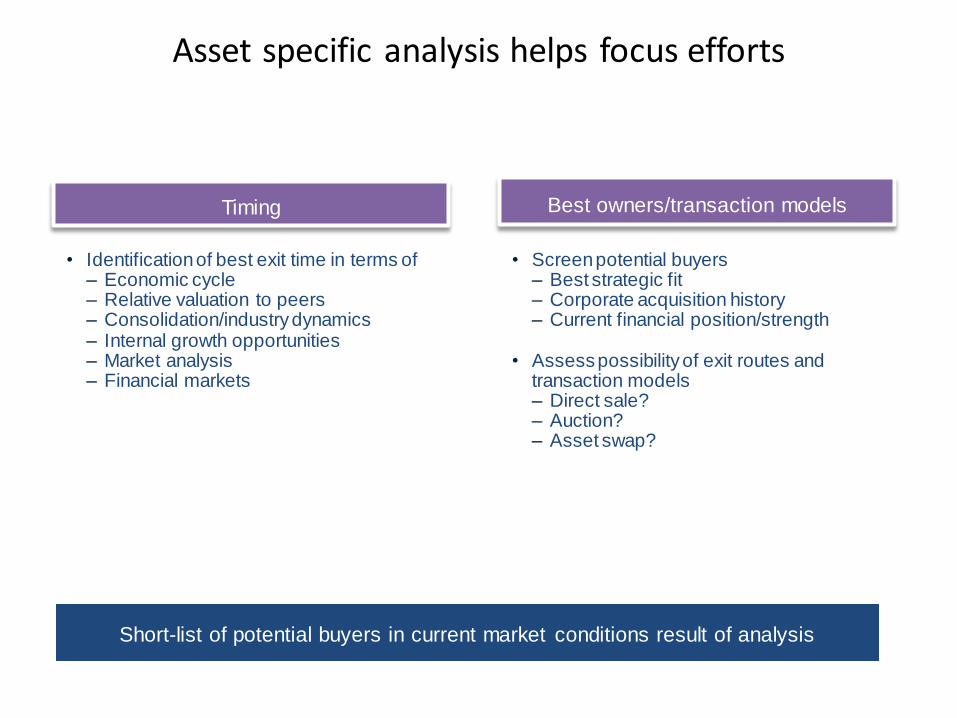

Divestment — overview

• Assess valuation of remaining Corporate assets

• Impact to current operations – Product placement – Brand/awareness – Logistics – Purchasing power – Overhead

• Strategic portfolio evaluation – Strategic fit – Value creation

• Assessment of portfolio health before and after divestiture

Asset specific analysis during exit preparation phase helps focus efforts during divestment

Rationale/feasibility Valuation/impact

Va

lue

cre

atio

n

Strategic fit

Divestment — overview

Divestments — Divestment strategy

• Phase objective

– Robust rationale for divestment, focusing on lack of strategic fit

– Determine best timing for divestment

– Short-list potential buyers; estimate values potential buyers willing to pay

• Key decisions

– Approve divestment

• Decision makers

– Corporate Major Project Committee, Shareholders, Corporate 2nd level

• Phase deliverables

– Checklist

Divestment strategy formulates best timing and potential buyers

Divestment — overview

Marketing and bid

evaluation

Divestment decision

Divest-

ment

strategy

Deal close

Due diligence

Mgmt present Site visit Negotiations Gate

1

Gate

4

Gate

3

Gate

2

• Screen potential buyers – Best strategic fit – Corporate acquisition history – Current financial position/strength

• Assess possibility of exit routes and

transaction models – Direct sale? – Auction? – Asset swap?

• Identification of best exit time in terms of – Economic cycle – Relative valuation to peers – Consolidation/industry dynamics – Internal growth opportunities – Market analysis – Financial markets

Asset specific analysis helps focus efforts

Timing Best owners/transaction models

Short-list of potential buyers in current market conditions result of analysis

Divestments — Marketing and bid evaluation

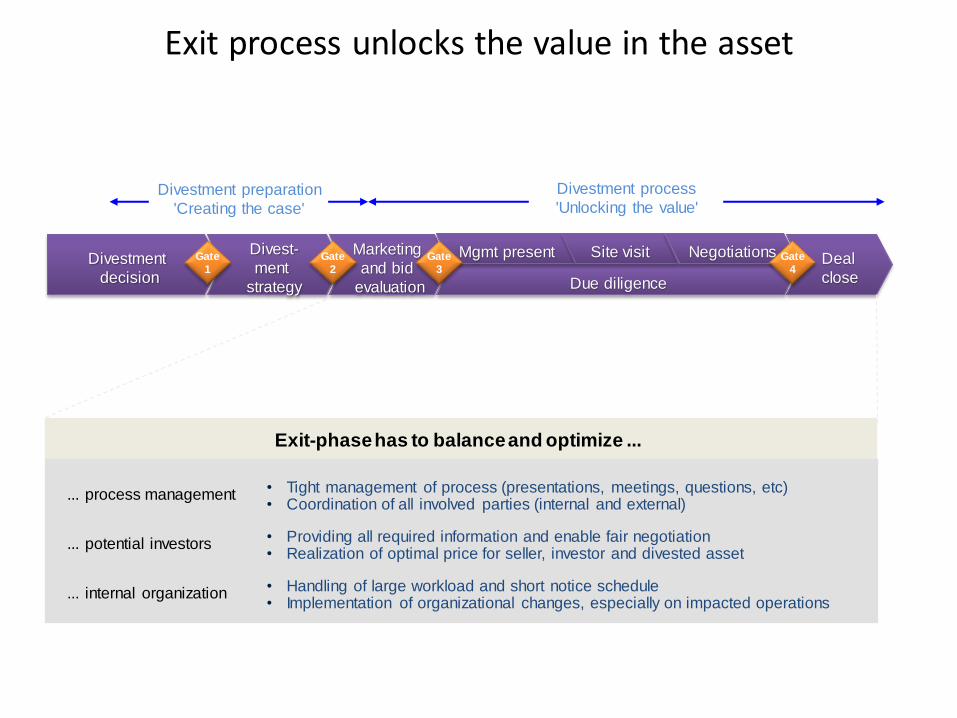

Exit process unlocks the value in the asset

Exit-phase has to balance and optimize ...

... process management • Tight management of process (presentations, meetings, questions, etc) • Coordination of all involved parties (internal and external)

... potential investors • Providing all required information and enable fair negotiation • Realization of optimal price for seller, investor and divested asset

... internal organization • Handling of large workload and short notice schedule • Implementation of organizational changes, especially on impacted operations

Divestment preparation

'Creating the case'

Divestment process

'Unlocking the value'

Marketing

and bid

evaluation

Divestment

decision

Divest-

ment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

1

Gate

4

Gate

3

Gate

2

• Phase objective

– Distribute initial information to potential bidders to gauge interest

– Receive and evaluate non-binding bids

– Qualify short-list of bidders, based on price and strategic fit

• Key decisions

– Approve short-list of potential buyers and price range of divestment

• Decision makers

– Corporate Major Project Committee, Shareholders , Corporate 2nd level

• Phase deliverables

– Checklist

Marketing and bid evaluation phase qualifies bidders for execution phase

Divestment — overview

Marketing

and bid

evaluation

Divestment decision

Divest- ment

strategy

Deal close

Due diligence

Mgmt present Site visit Negotiations Gate

4

Gate

3

Gate

2

Gate

1

• Confidentiality and indemnity agreements between

– Client and potential buyers – External advisors and potential buyers

• Describes the 'opportunity' (does not include reserved information)

– Business summary – Divestiture background – Key financials

Investor marketing material must clearly articulate strategic rationale for investment case

Information teaser

Information

Memorandum (IM)

Non-disclosure

agreements

Divestment — overview

• Comprehensive document providing

– Overview of market – Detailed business description, detailed financials including forecasts – Future outlook and business strategy

– Transaction process • Only numbered hard copies of Information Memorandum to be released

for confidentiality purposes

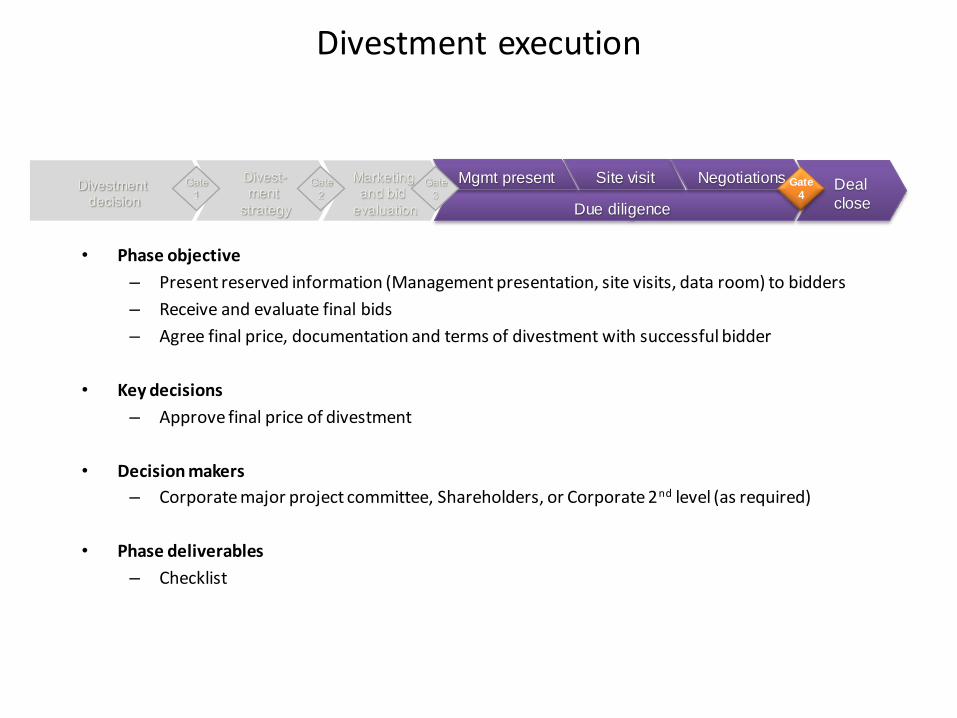

Divestments — Exit process

Divestment execution

• Phase objective

– Present reserved information (Management presentation, site visits, data room) to bidders

– Receive and evaluate final bids

– Agree final price, documentation and terms of divestment with successful bidder

• Key decisions

– Approve final price of divestment

• Decision makers

– Corporate major project committee, Shareholders, or Corporate 2nd level (as required)

• Phase deliverables

– Checklist

Divestment — overview

Marketing and bid

evaluation

Divestment decision

Divest- ment

strategy

Deal

close Due diligence

Mgmt present Site visit Negotiations Gate

4

Gate

3

Gate

2

Gate

1

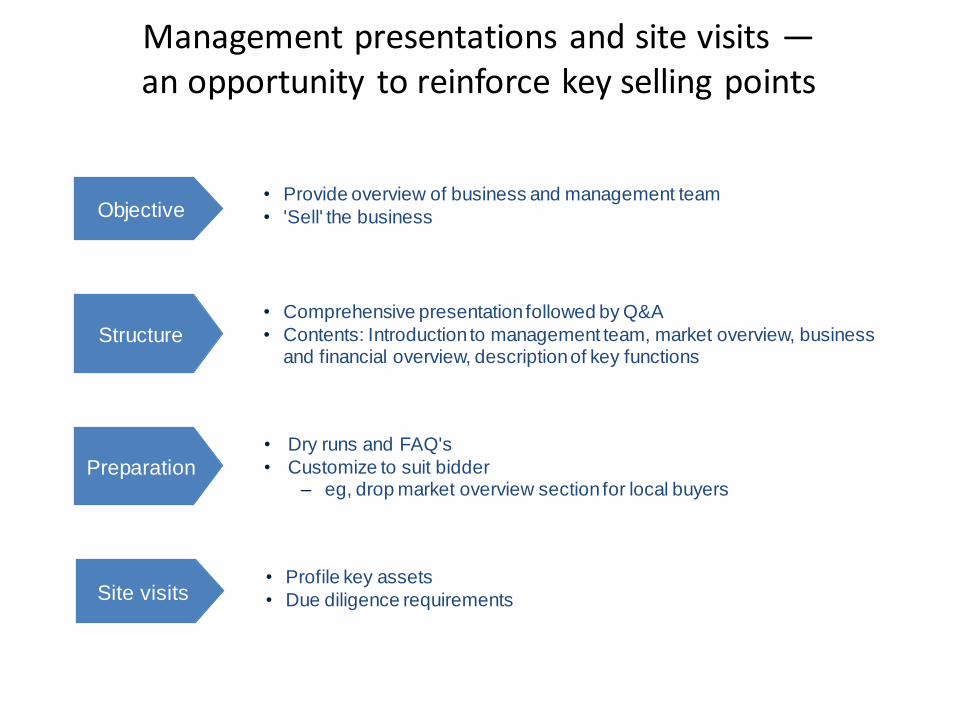

Management presentations and site visits — an opportunity to reinforce key selling points

• Provide overview of business and management team

• 'Sell' the business Objective

Structure • Comprehensive presentation followed by Q&A

• Contents: Introduction to management team, market overview, business and financial overview, description of key functions

Preparation

Site visits • Profile key assets

• Due diligence requirements

• Dry runs and FAQ's

• Customize to suit bidder – eg, drop market overview section for local buyers

• Information classified into fund profile, distribution, financials, legal/regulatory, etc

• Circulated to shortlisted bidders prior to due diligence – Ensures appropriate team for due diligence – Additional information needs raised upfront

• Content to be approved by management and legal

Setting up a data room for due diligence Data room typically run by outside contractor

Define data

room protocols

• Rules for entry, exit, number of people allowed, responding to queries, copying

documents, data room timing, etc

Prepare data

room index

Collect data • Manage process with client, accounting firm, lawyers

• Consistency with information memorandum and management presentation

Data room

logistics

• Define location

• Assign responsibility for control of documents and entry/exit • Ordering of bidders in data room important — best/most likely bids to get

second/third slot, first one used as a ‘pilot’