Le lingue

Pagine

Legale

La neuroimpresa -

il contributo delle

neuroscienze

Maurizio Elia

U.O.C. di Neurologia e Neurofisiopatologia Clinica e Strumentale

IRCCS “Associazione Oasi Maria SS”

Troina (EN)

Catania, 21.03.2013

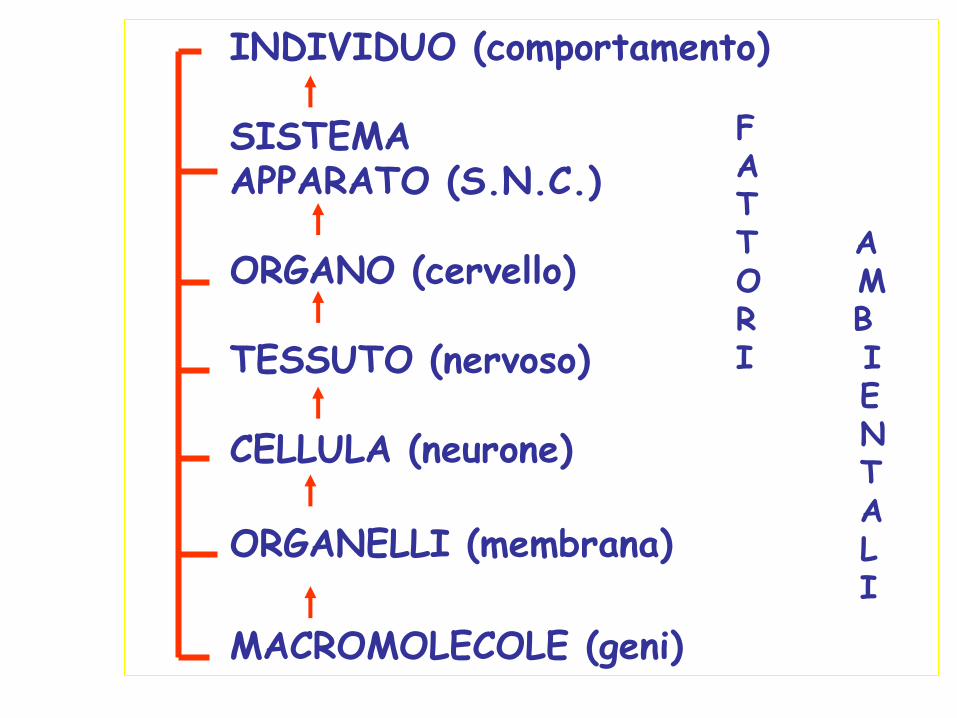

INDIVIDUO (comportamento) SISTEMA APPARATO (S.N.C.) ORGANO (cervello) TESSUTO (nervoso) CELLULA (neurone) ORGANELLI (membrana)

MACROMOLECOLE (geni)

F A T T A O M R B I I E N T A L I

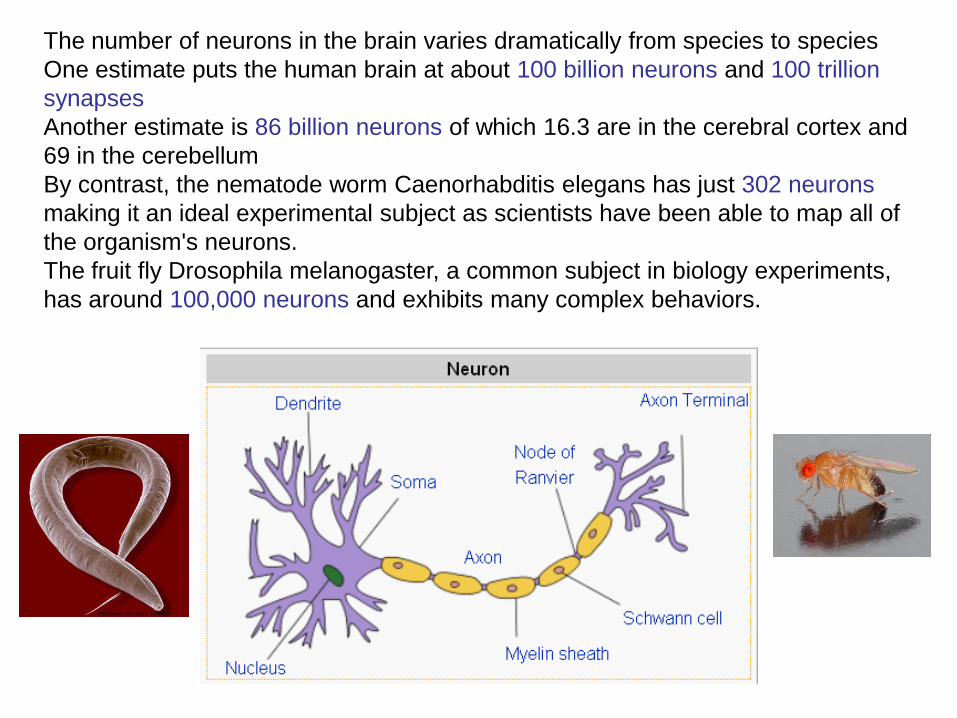

The number of neurons in the brain varies dramatically from species to species

One estimate puts the human brain at about 100 billion neurons and 100 trillion

synapses

Another estimate is 86 billion neurons of which 16.3 are in the cerebral cortex and

69 in the cerebellum

By contrast, the nematode worm Caenorhabditis elegans has just 302 neurons

making it an ideal experimental subject as scientists have been able to map all of

the organism's neurons.

The fruit fly Drosophila melanogaster, a common subject in biology experiments,

has around 100,000 neurons and exhibits many complex behaviors.

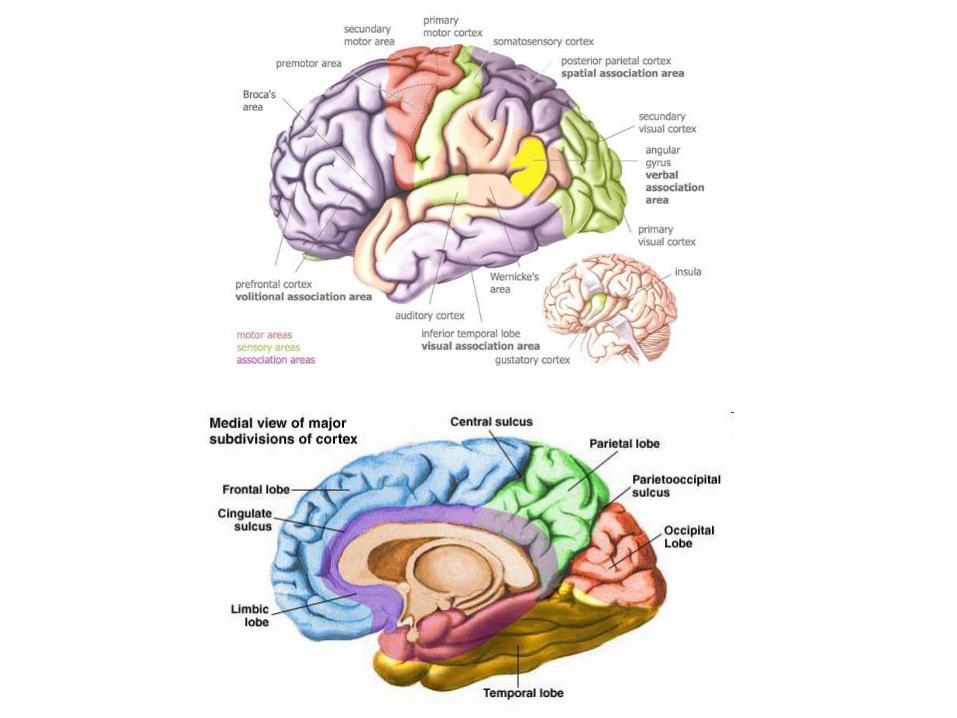

Pierre Paul Broca

(1824-1880)

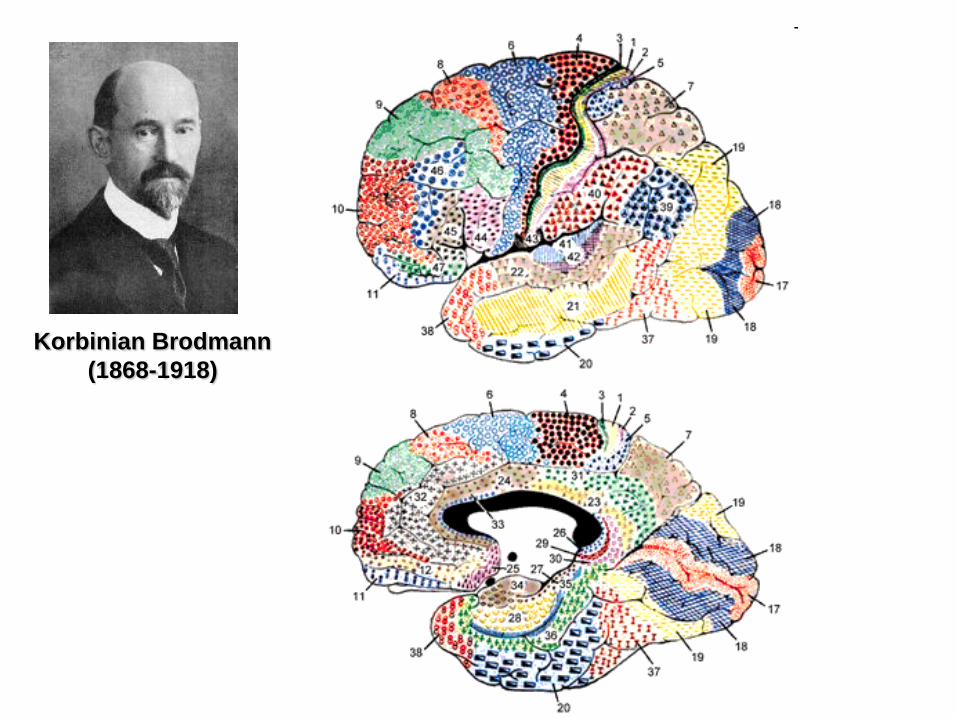

Korbinian Brodmann

(1868-1918)

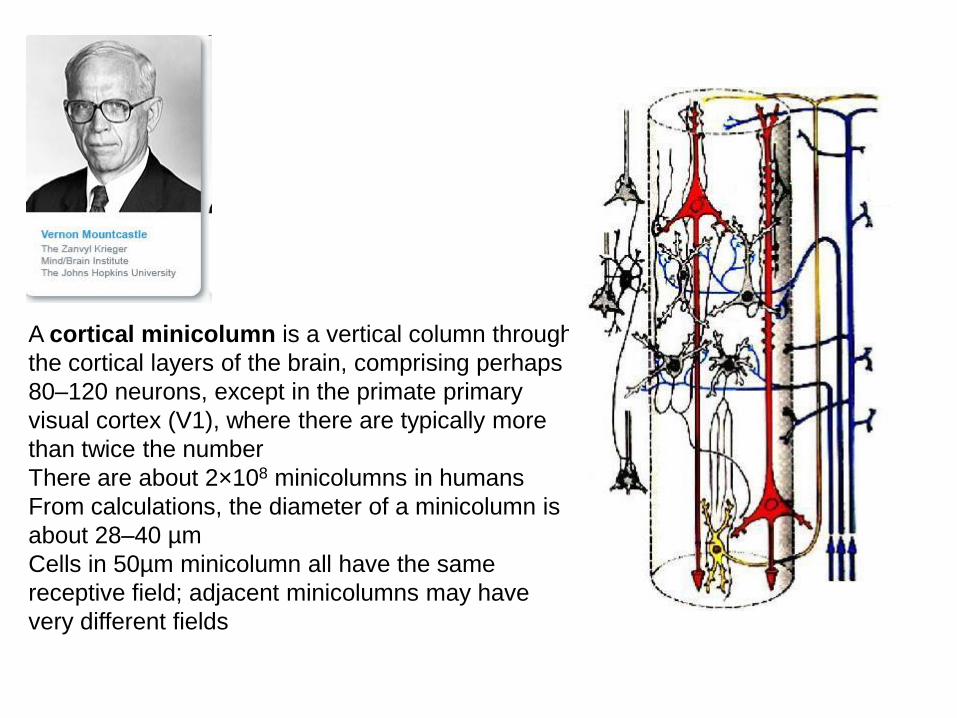

A cortical minicolumn is a vertical column through

the cortical layers of the brain, comprising perhaps

80–120 neurons, except in the primate primary

visual cortex (V1), where there are typically more

than twice the number

There are about 2×108 minicolumns in humans

From calculations, the diameter of a minicolumn is

about 28–40 µm

Cells in 50µm minicolumn all have the same

receptive field; adjacent minicolumns may have

very different fields

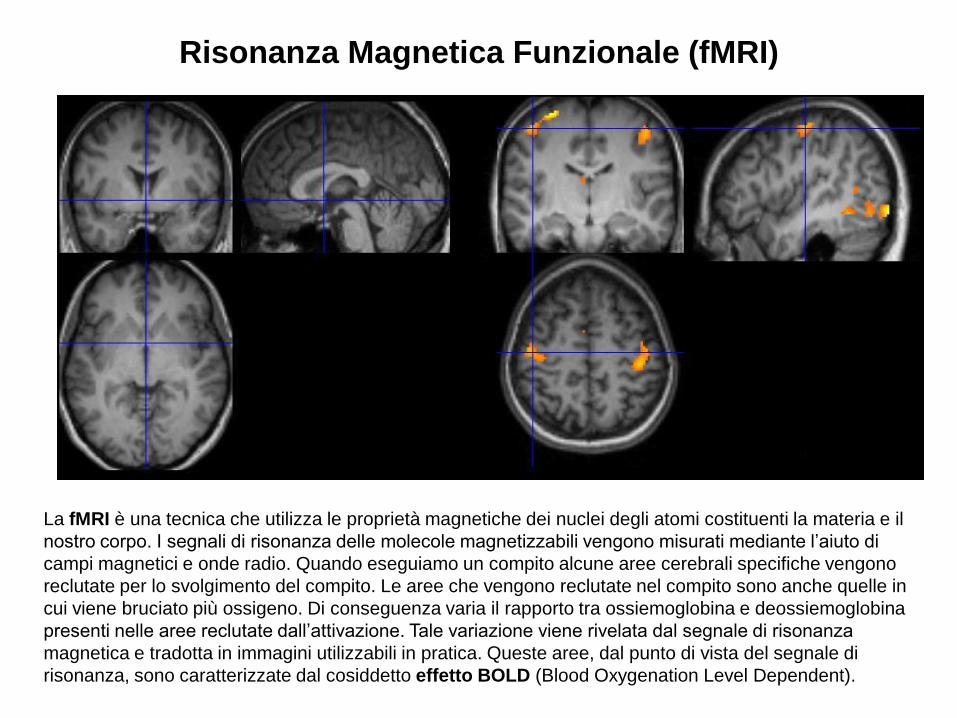

Risonanza Magnetica Funzionale (fMRI)

La fMRI è una tecnica che utilizza le proprietà magnetiche dei nuclei degli atomi costituenti la materia e il

nostro corpo. I segnali di risonanza delle molecole magnetizzabili vengono misurati mediante l’aiuto di

campi magnetici e onde radio. Quando eseguiamo un compito alcune aree cerebrali specifiche vengono

reclutate per lo svolgimento del compito. Le aree che vengono reclutate nel compito sono anche quelle in

cui viene bruciato più ossigeno. Di conseguenza varia il rapporto tra ossiemoglobina e deossiemoglobina

presenti nelle aree reclutate dall’attivazione. Tale variazione viene rivelata dal segnale di risonanza

magnetica e tradotta in immagini utilizzabili in pratica. Queste aree, dal punto di vista del segnale di

risonanza, sono caratterizzate dal cosiddetto effetto BOLD (Blood Oxygenation Level Dependent).

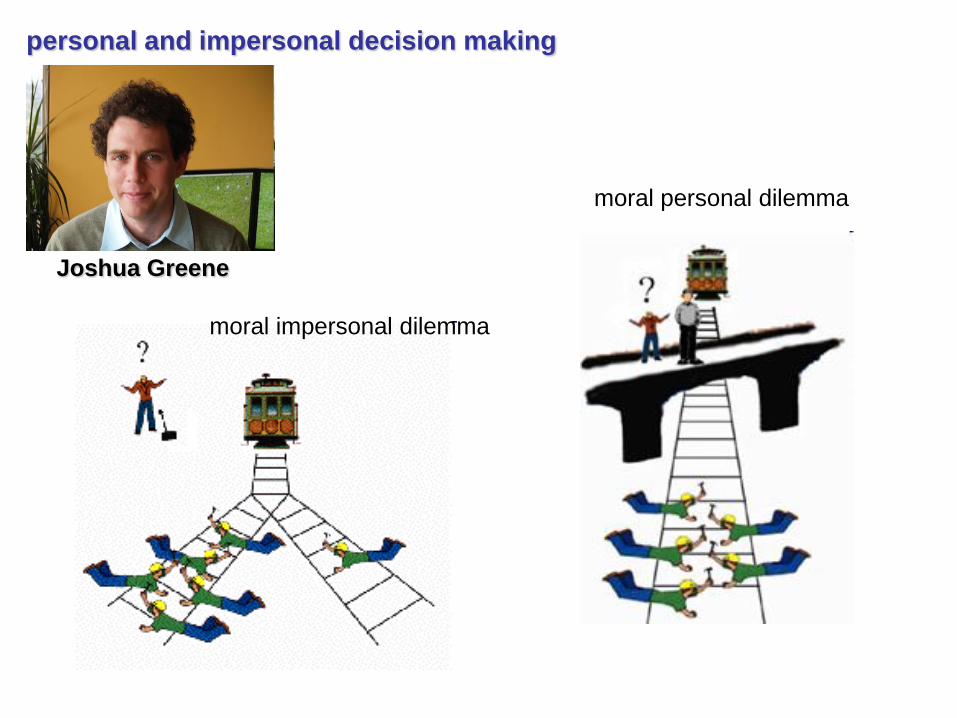

personal and impersonal decision making

Joshua Greene

moral personal dilemma

moral impersonal dilemma

(DLPFC)

La teoria dell’economia normativa nel prendere decisioni sotto rischio assume

che i decisori combinino probabilità e valutazione (utilità) di possibili esiti in un

certo modo, per lo più tipicamente con un’attesa probabilità-pesata su possibili

utilità.

Le nostre esperienze quotidiane ed evidenze empiriche, però, ci dicono che

sistematicamente violiamo la teoria normativa.

Un tipo di sistematica violazione della teoria normativa è che le persone tendono

a pesare le probabilità obiettive in maniera non lineare.

I decisori spesso sovrastimano basse probabilità (ad es., lotterie) e sottostimano

alte probabilità.

L’alternativa principale alla teoria normativa (dell’utilità attesa) è la teoria della

prospettiva (Tversky e Kahneman, 1992).

Una delle componenti importanti della teoria della prospettiva è la pesatura non

lineare della probabilità nella quale le probabilità obiettive (p) sono trasformate in

maniera non lineare in pesi di decisione w(p) attraverso una funzione di pesatura.

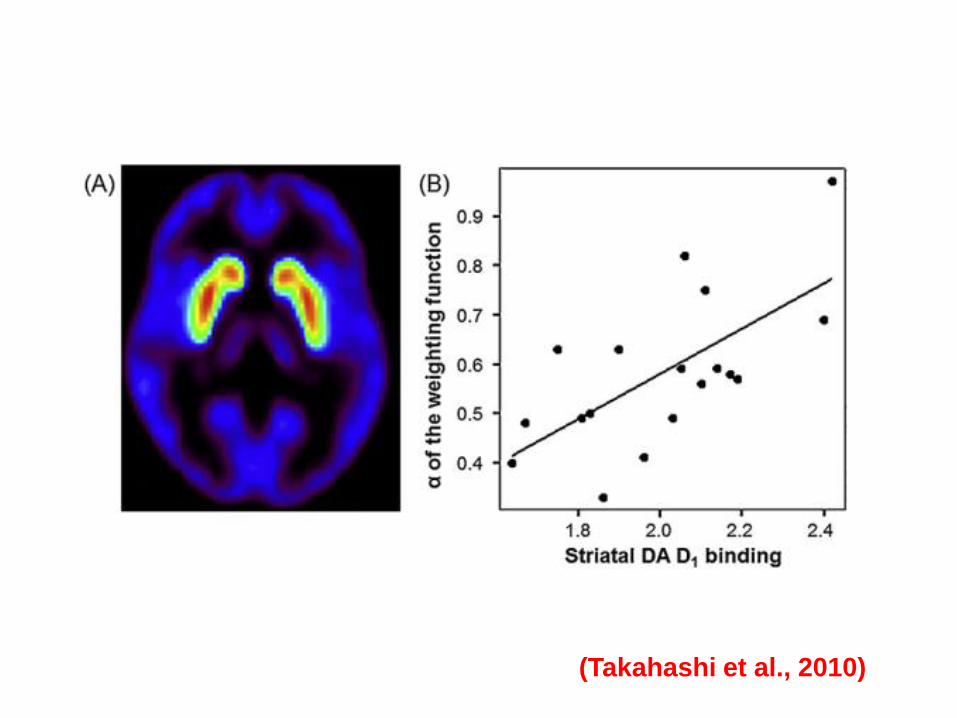

(Takahashi et al., 2010)

Il senso di avversione derivato dal perdere una certa quantità di denaro

sembra essere maggiore del piacere derivato dal guadagnare una quantità

equivalente.

Immaginiamo di partecipare al gioco della lancio della monetina: se uscirà

testa vincerò 100 euro, se uscirà croce perderò 100 euro. Vogliamo giocare?

La maggior parte della gente dirà di no.

Se, però, il premio per la vincita viene aumentato a 200 euro e la potenziale

perdita rimane 100 euro, qualcuno accetterà di giocare.

Questo significa che, tipicamente, le perdite hanno 2 volte l’impatto di

equivalenti guadagni, una proprietà detta “avversione per la perdita”.

decision making under uncertainty

(a) Aversive stimuli, whether

decision options that involve

increased risk or punishments

themselves, have frequently been

shown to activate insular cortex

(INS) and ventrolateral prefrontal

cortex (vlPFC)

(b) Unexpected rewards modulate

activation of the striatum (STR),

particularly its ventral aspect, as

well as the medial prefrontal cortex

(mPFC)

(c) Executive control processes

required for evaluation of uncertain

choice options are supported by

dorsolateral prefrontal cortex

(dlPFC) and posterior parietal

cortex (PPC)

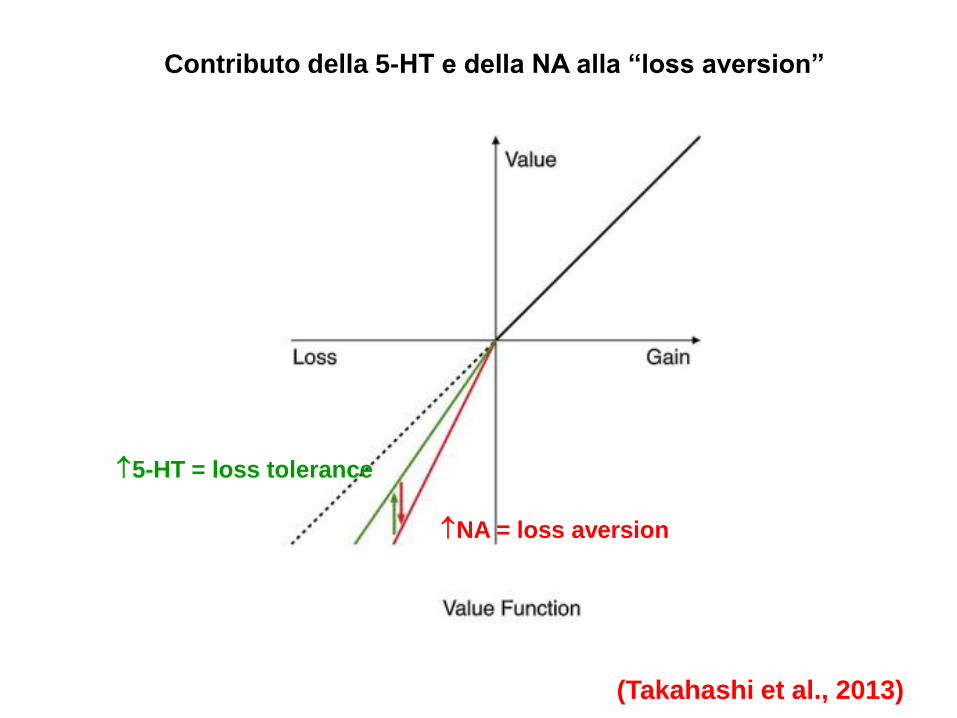

Contributo della 5-HT e della NA alla “loss aversion”

NA = loss aversion

5-HT = loss tolerance

(Takahashi et al., 2013)

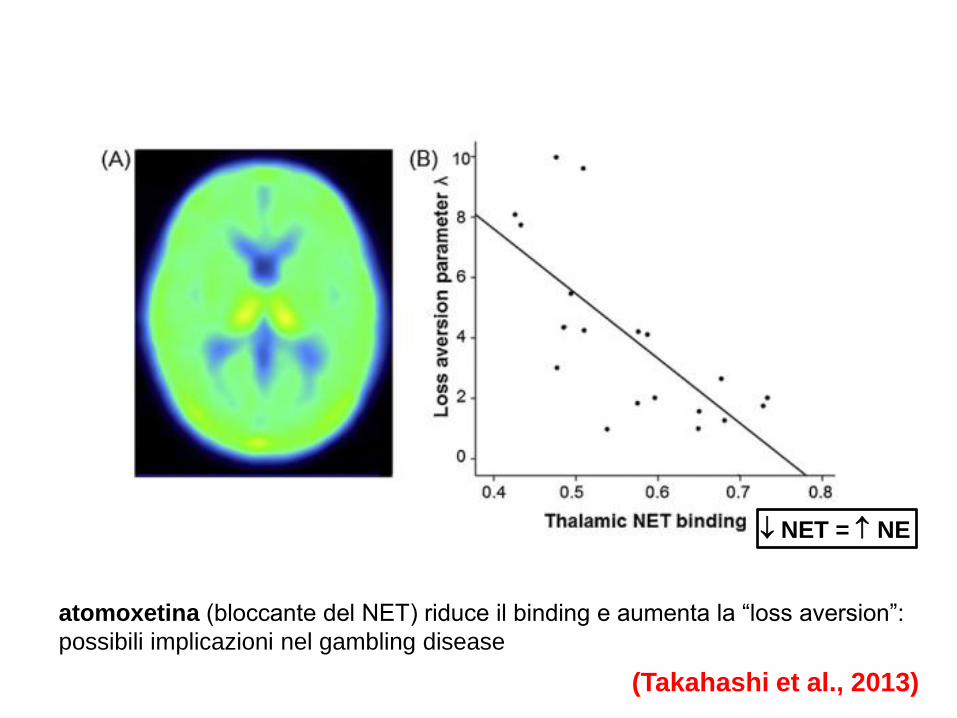

(Takahashi et al., 2013)

NET = NE

atomoxetina (bloccante del NET) riduce il binding e aumenta la “loss aversion”:

possibili implicazioni nel gambling disease

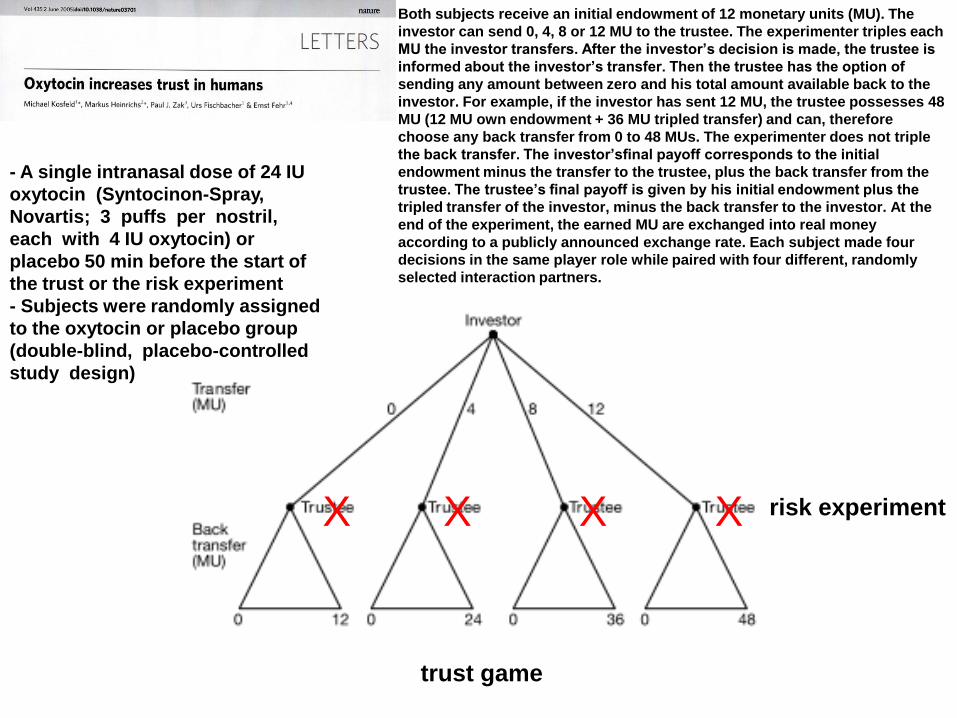

trust game

X X X X risk experiment

- A single intranasal dose of 24 IU

oxytocin (Syntocinon-Spray,

Novartis; 3 puffs per nostril,

each with 4 IU oxytocin) or

placebo 50 min before the start of

the trust or the risk experiment

- Subjects were randomly assigned

to the oxytocin or placebo group

(double-blind, placebo-controlled

study design)

Both subjects receive an initial endowment of 12 monetary units (MU). The

investor can send 0, 4, 8 or 12 MU to the trustee. The experimenter triples each

MU the investor transfers. After the investor’s decision is made, the trustee is

informed about the investor’s transfer. Then the trustee has the option of

sending any amount between zero and his total amount available back to the

investor. For example, if the investor has sent 12 MU, the trustee possesses 48

MU (12 MU own endowment + 36 MU tripled transfer) and can, therefore

choose any back transfer from 0 to 48 MUs. The experimenter does not triple

the back transfer. The investor’sfinal payoff corresponds to the initial

endowment minus the transfer to the trustee, plus the back transfer from the

trustee. The trustee’s final payoff is given by his initial endowment plus the

tripled transfer of the investor, minus the back transfer to the investor. At the

end of the experiment, the earned MU are exchanged into real money

according to a publicly announced exchange rate. Each subject made four

decisions in the same player role while paired with four different, randomly

selected interaction partners.

The investors’ average

transfer is 17% higher in the oxytocin

group (Mann-Whitney U-test;

z = -1.897, P = 0.029, one-sided)

The average transfer is 7.5 MU in

both groups (Mann-Whitney U-

test; z = 0.022, P = 0.983; two-

sided test)

N= 128

N= 66

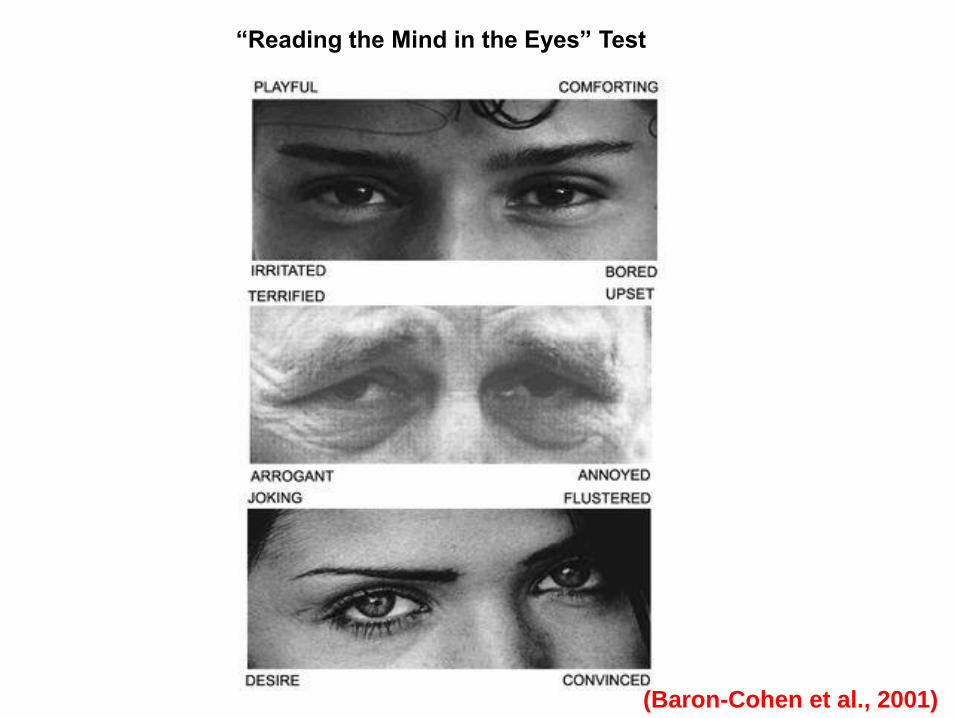

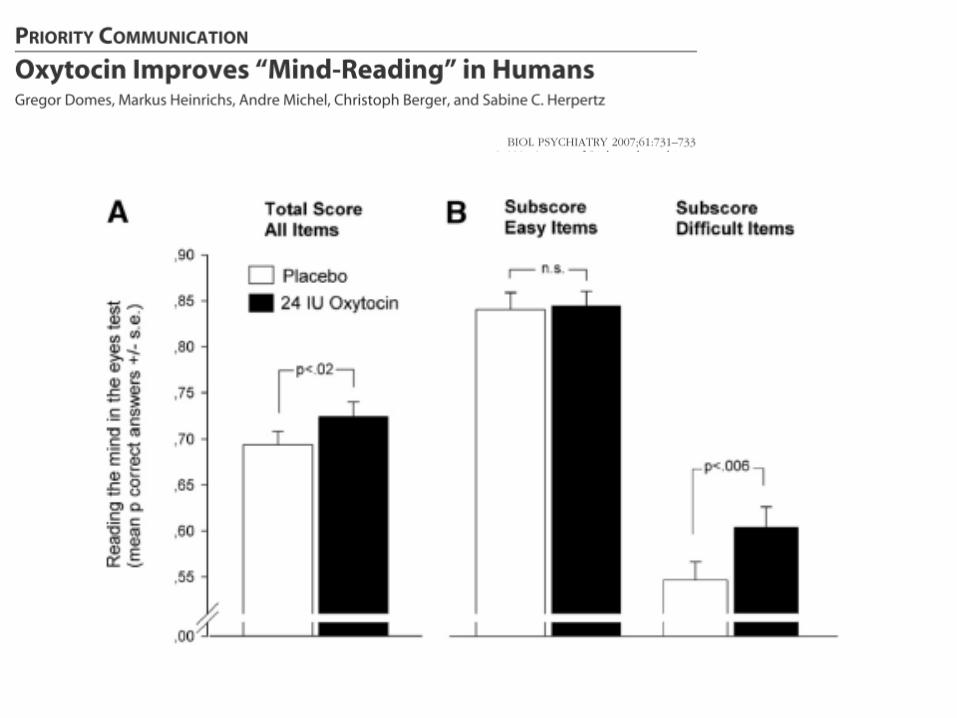

(Baron-Cohen et al., 2001)

“Reading the Mind in the Eyes” Test

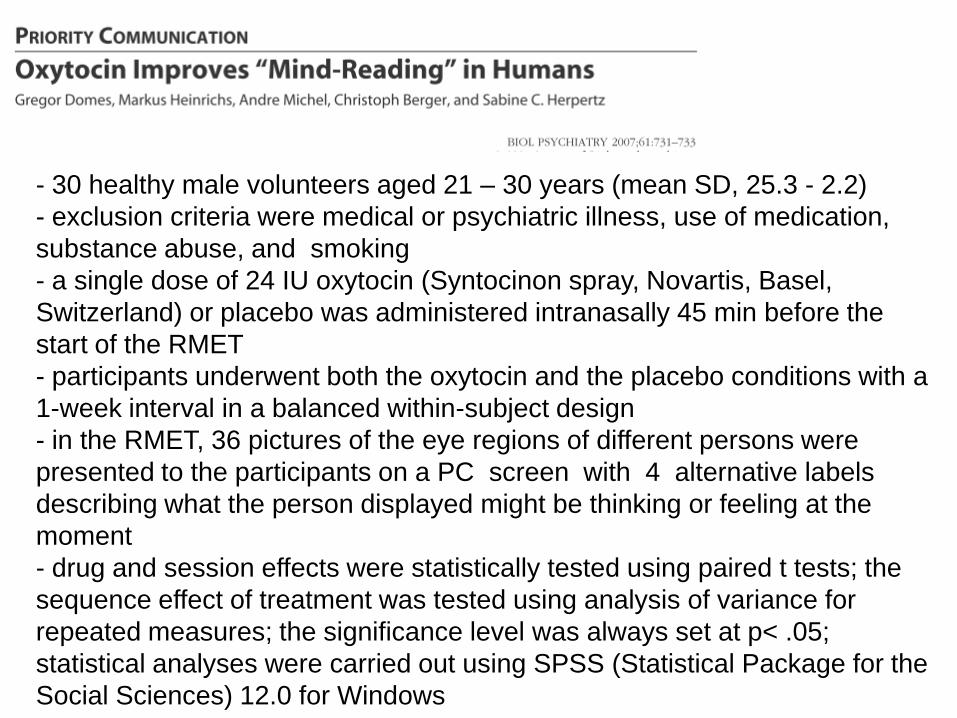

- 30 healthy male volunteers aged 21 – 30 years (mean SD, 25.3 - 2.2)

- exclusion criteria were medical or psychiatric illness, use of medication,

substance abuse, and smoking

- a single dose of 24 IU oxytocin (Syntocinon spray, Novartis, Basel,

Switzerland) or placebo was administered intranasally 45 min before the

start of the RMET

- participants underwent both the oxytocin and the placebo conditions with a

1-week interval in a balanced within-subject design

- in the RMET, 36 pictures of the eye regions of different persons were

presented to the participants on a PC screen with 4 alternative labels

describing what the person displayed might be thinking or feeling at the

moment

- drug and session effects were statistically tested using paired t tests; the

sequence effect of treatment was tested using analysis of variance for

repeated measures; the significance level was always set at p< .05;

statistical analyses were carried out using SPSS (Statistical Package for the

Social Sciences) 12.0 for Windows

- 68 males participated in the experiment with 34 of them

receiving OT and 34 receiving placebo

- mean age was 21.8 (SD 3.8)

- only male subjects because of the possibility of an

unintended miscarriage in females as well as the varying

effects of OT over the menstrual cycle

- exclusion criteria included significant medical or

psychiatric illness, medications that interact with OT, and

drug or alcohol abuse

- participants were infused by nasal inhaler with either 40 IU

of OT or normal saline of the same amount

- OT was allowed to load for 60 minutes prior to the UG and

DG choices

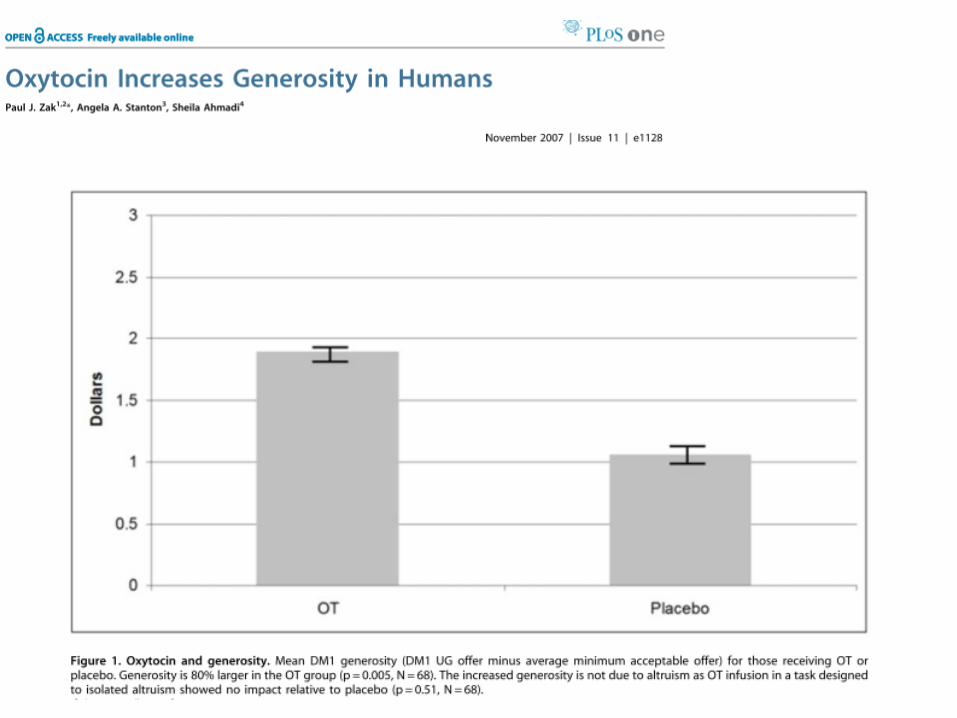

In the ultimatum game (UG), decision-maker 1(DM1) was endowed

with $10 and was asked to offer a split of this money to DM2. DM2

has no endowment.

If DM2 accepted the split, the money was paid. But, if DM2 rejected

the split, both DMs earned nothing.

Participants were asked to make decisions as both DM1 and DM2,

with subsequent random assignment of roles. As DM2s, they

were asked to state the minimum amount they would accept from a

DM1. The rejection threshold was not reported to the other DMs.

By asking subjects for the minimum acceptable offer, the UG task

was designed to have participants consider how the DM2 in the

dyad would react to an offer (perspective taking).

A rejection of DM1’s offer in the UG allowed DM2 to punish DM1 for

stingy offers, but at a cost.

We define a generous transfer in the UG as a DM1 offer that

exceeds the average minimum acceptable offer.

The dictator game (DG) is similar to the UG in that

DM1 has a $10 endowment and DM2 has nothing. The

difference in the DG is that DM2 has no choice— he or

she must accept whatever DM1offers.

As a result, the DG does not compel DM1 to consider

how DM2 will feel about the split of benefits (reduced

perspective taking).

The consensus view in experimental economics is that

the transfer in the DG is a measure of altruism.

The inclusion of both the UG and DG allows us to

dissociate generosity from altruism within subjects.

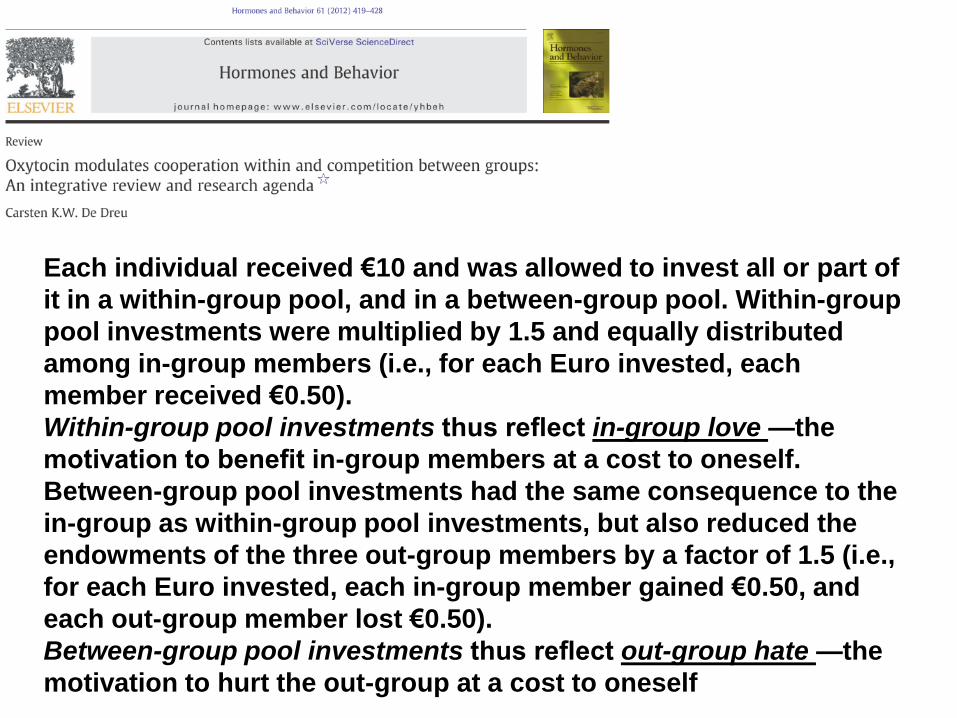

Each individual received €10 and was allowed to invest all or part of

it in a within-group pool, and in a between-group pool. Within-group

pool investments were multiplied by 1.5 and equally distributed

among in-group members (i.e., for each Euro invested, each

member received €0.50).

Within-group pool investments thus reflect in-group love —the

motivation to benefit in-group members at a cost to oneself.

Between-group pool investments had the same consequence to the

in-group as within-group pool investments, but also reduced the

endowments of the three out-group members by a factor of 1.5 (i.e.,

for each Euro invested, each in-group member gained €0.50, and

each out-group member lost €0.50).

Between-group pool investments thus reflect out-group hate —the

motivation to hurt the out-group at a cost to oneself

24 IU

Top Related