Istituto di Igiene Università Cattolica del Sacro Cuore, Roma

CRANEC – CENTRO DI RICERCHE IN ANALISI ECONOMICA FONDAZIONE ASTRID

Università Cattolica del Sacro Cuore

Lunedi 4 Dicembre 2017

Euro-Union Bond e il piano Juncker Prof. Alberto Quadrio Curzio Accademia Nazionale dei Lincei Università Cattolica del Sacro Cuore

Per un rilancio dell’investimento pubblico in Europa

Ruolo pubblico e Partenariato

@: non citare senza il permesso dell’autore / do not cite without author’s permission

GLI EUROBOND - rischio + crescita= + integrazione

1) La proposta Prodi e Quadrio Curzio (2011-2012)

2) Tre novità disunite: ESM, BCE-QE, Piano Juncker-EFSI

4) EuroUnionBond: EuroSyntBond; EuroInvestmentBond

5) –Rischio +Investimenti +Crescita= +Eurointegrazione

3) La proposta Quadrio Curzio e Bertini (Aprile 2017)

© CRANEC/AQC

La proposta Prodi e Quadrio Curzio 2011-12 sugli Eurounionbond (con i successivi approfondimenti di Alberto Quadrio Curzio (2017), si rimanda rif. biblio in slide 7)

Tre novità economico-istituzionali disunite: ESM, BCE-QE, Piano Juncker-EFSI

Se ci fosse una razionalità politica… che aiuterebbe anche la BCE a ricollocare i 2000 miliardi di titoli di Stato si potrebbe arrivare ad ulteriori innovazioni (la proposta di Quadrio Curzio e Bertini 2017) come…

Gli EuroUnionBond per unificare parte dei debiti pubblici degli stati della UEM;

Gli EuroInvestmentBond per finanziare gli investimenti infrastrutturali

© CRANEC/AQC

«EuroUnionBond per la Nuova Europa» in Il Sole 24 Ore del 23/08/2011 – NB i dati di questa tavola e delle due successive sono quelli del 2011

RICOSTRUZIONE CON CRESCITA INNOVATIVA EuroUnionBond (EUB) e Fondo Finanziario Europeo (FFE)

Proposta Prodi - Quadrio Curzio: 2011 e 2012

FONDO FINANZIARIO EUROPEO (FFE)

RISERVE AUREE*

AZIONI E OBBLIGAZIONI DI RETI(Enel,Eni,Poste Ecc) A VALORI DI STIMA

CAPITALE CONFERITO = 1,000 miliardi

Italia = 180 mld €

Ogni Paese conferisce in pari misura alla sua quota BCE

UEM = 550 mld

Italia = 79 mld €

UEM =450 mld € (350 milioni once)

Italia = 101 mld € (79 milioni once)

*Prezzo 1800$/oz

© C

RA

NEC

/AQ

C

Leva sul capitale conferito di 1,000 miliardi: 3

EMISSIONE OBBLIGAZIONARIA DI 3,000

Durata 10 anni (e oltre) al 3% annuo

Onere interessi 90 miliardi = 1% del PIL UEM

2,300 Titoli di Stato 25% Pil

Uem

700 Investimenti

infrastrutturali

RICOSTRUZIONE CON CRESCITA INNOVATIVA EuroUnionBond (EUB) e Fondo Finanziario Europeo (FFE)

Prodi - Quadrio Curzio: 2011 e 2012

(33% circa PIL UEM)

«EuroUnionBond per la Nuova Europa» in Il Sole 24 Ore del 23/08/2011 © CRANEC/AQC

Pil di UEM = 9,000 miliardi di euro

Debito/Pil di UEM = 85%

60 % verso il mercato

EUB FFE

RICOSTRUZIONE CON CRESCITA INNOVATIVA EuroUnionBond (EUB) e Fondo Finanziario Europeo (FFE)

Proposta Prodi - Quadrio Curzio

95% (da 120%) verso il mercato

«EuroUnionBond per la Nuova Europa» in Il Sole 24 Ore del 23/08/2011 © CRANEC/AQC

Edited by • Ivano Cardinale Goldsmiths, University of London, UK

• D'Maris Coffman University College London, UK

• Roberto Scazzieri Università degli Studi, Bologna, Italy

2017

© CRANEC/AQC

Alberto Quadrio Curzio (2017), ‘Eurobonds for EMU Stability and Structural Growth’, in The Political Economy of the Eurozone,

Cardinale I., Coffman D’Maris and Scazzieri R. eds., Cambridge: Cambridge University Press 2017

15.1 Introduction

15.2 Unionbonds: Investment for Growth

15.3 GoldEurobonds: Debt Safety and Investment Push

15.3.1 Gold After Bretton Woods’ Collapse

15.3.2 Euro-Gold-Development Fund and Gold-Eurobonds

15.4 Stability Bonds: The role of EU Institutions

15.4.1 The Two Ministers’ proposal

15.4.2 The European Parliament Proposal

15.4.3 The European Commission Proposal

15.5 RescueBonds: Temporary Help for the EMU?

15.5.1 The EFSF Fund

15.5.2 Assistance by EFSF to Ireland, Portugal and Greece

15.5.3. From the EFSF to the ESM

15.6 EuroUnionBonds: Stability and Growth 15.6.1 The Proposal: EUBs and the EFF 15.6.2 The European Financial Fund’s Structure 15.6.3 The EFF and the Central Bank Gold Agreements 15.6.4 The EFF and ‘In-In’ Real Capital 15.6.5 The Issue of EUBs 15.6.6 EFF Governance 15.6.7 EFF and EUBs for EMU-MS Sovereign Debt 15.6.8 The EFF and EUBs for Structural Investment 15.6.9 The EFF and EUBs in the Very Long Run: Some Open Issues 15.7 Conclusions 15.7.1 German Worries 15.7.2 European Necessities

© CRANEC/AQC Un dibattito che dura da più di 20 anni

Il futuro della UEM passa dal coordinamento delle innovazioni che ci sono ma che vanno completate e connesse

1) Eurobond del MES: sono concreti e di successo. Limitate emissioni. Finalità di soccorso a Stati

in difficoltà Spagna, Grecia, Portogallo

2) Eurobond della BCE: sono sintetici o compositi dai titoli di stato acquistati con il QE nelle

proporzioni delle quote di capitale sottoscritte dagli Stati membri presso la BCE

3) Eurobond dell’EFSI (Fondo Europeo per gli Investimenti Strategici del Piano Juncker): sono

immaginari perché non c’è raccolta ma solo prestiti Bei con garanzie

© CRANEC/AQC

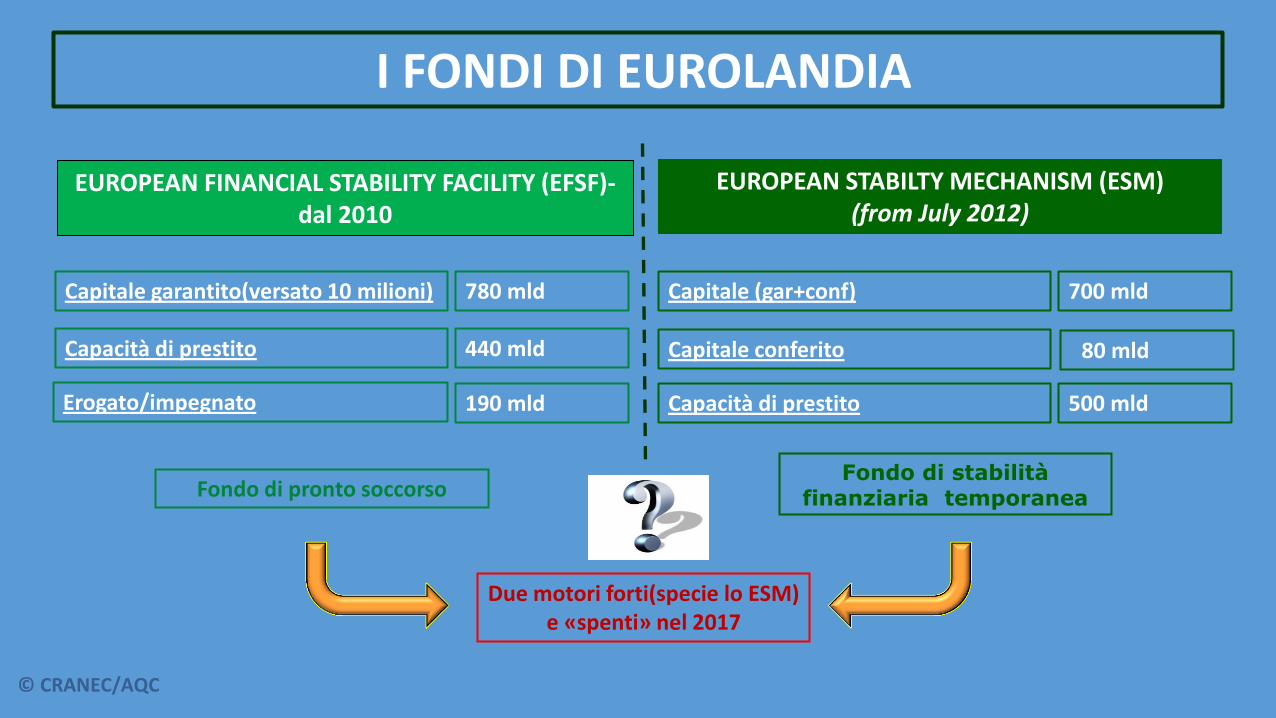

I FONDI DI EUROLANDIA

EUROPEAN FINANCIAL STABILITY FACILITY (EFSF)-dal 2010

EUROPEAN STABILTY MECHANISM (ESM) (from July 2012)

Fondo di pronto soccorso Fondo di stabilità

finanziaria temporanea

Due motori forti(specie lo ESM) e «spenti» nel 2017

Erogato/impegnato

Capacità di prestito

780 mld

190 mld

Capitale garantito(versato 10 milioni)

440 mld Capitale conferito

Capacità di prestito

700 mld

80 mld

Capitale (gar+conf)

500 mld

© CRANEC/AQC

© CRANEC/AQC

* Figures do mention the net disbursed amount for PT & IE, being the net loan amount minus the upfront fees and issuance costs paid by the beneficiary MS to the EFSF

at inception of the loan. Both are conventions for these countries. The net loan amount lent to IE and PT set in total €2bn higher. Contrarily the facility refers to the net

loan amount for GR.

** The initial programme amount for Greece was €144.6bn. This final amount is derived by excluding the undisbursed amount of €0.95bn of the PSI facility as well as

€10.93bn "Bank Recapitalisation Installment" and €1.81bn installment of the MFFA, whose availability periods have ended and are therefore no longer available.

Fonte: sito ESM, presentazione «European Financial Stability Facility & European Stability Mechanism», December 2017

EFSF lending programme

[as of November 2nd, 2017]

* Disbursements were made in-kind. All notes have now been exchanged for cash.

** Currently the entire €86bn programme for Greece is shown as funded by ESM; however, the initial programme buffer of €19.6bn is no longer expected to be disbursed and

the final ESM participation is also expected to be lower due to lower financing needs and alternative sources of financing (in particular IMF). ESM lending figures will be

adjusted when IMF participation becomes clearer.

** Initial programme amount for SP was €100 bn out of which €41,3 was disbursed during Availability Period. Availability period has ended on 31/12/13.

*** Spain has voluntarily prepaid €1.3bn on 08/07/14, €1.5bn on 17/03/15, €2.5bn on 14/07/15, €1bn on 11/11/2016 and €1bn on 14/06/2017, €2bn on 16/11/17 and made a

scheduled repayment of €0.3bn on 23/07/14.

**** Following expiration of Availability Period on 31 March 2016, remaining €2.67bn installment is no longer available for disbursement.

***** Greece early repaid €2.029bn on 20/02/2017

Fonte: sito ESM, presentazione «European Financial Stability Facility & European Stability Mechanism», December 2017

ESM lending programme

[as of November 2nd, 2017]

[as of November 2nd, 2017]

Fonte: sito ESM, presentazione «European Financial Stability Facility & European Stability Mechanism», December 2017

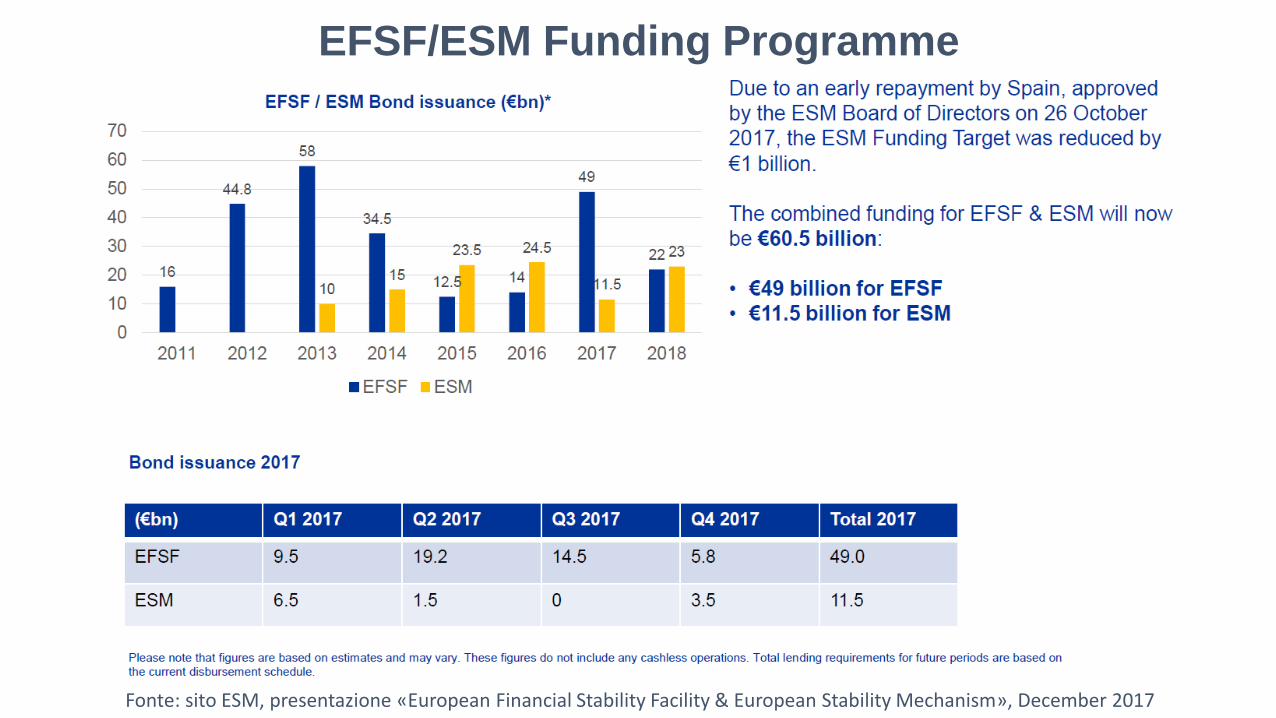

EFSF/ESM Funding Programme

Fonte: sito ESM, presentazione «European Financial Stability Facility & European Stability Mechanism», December 2017

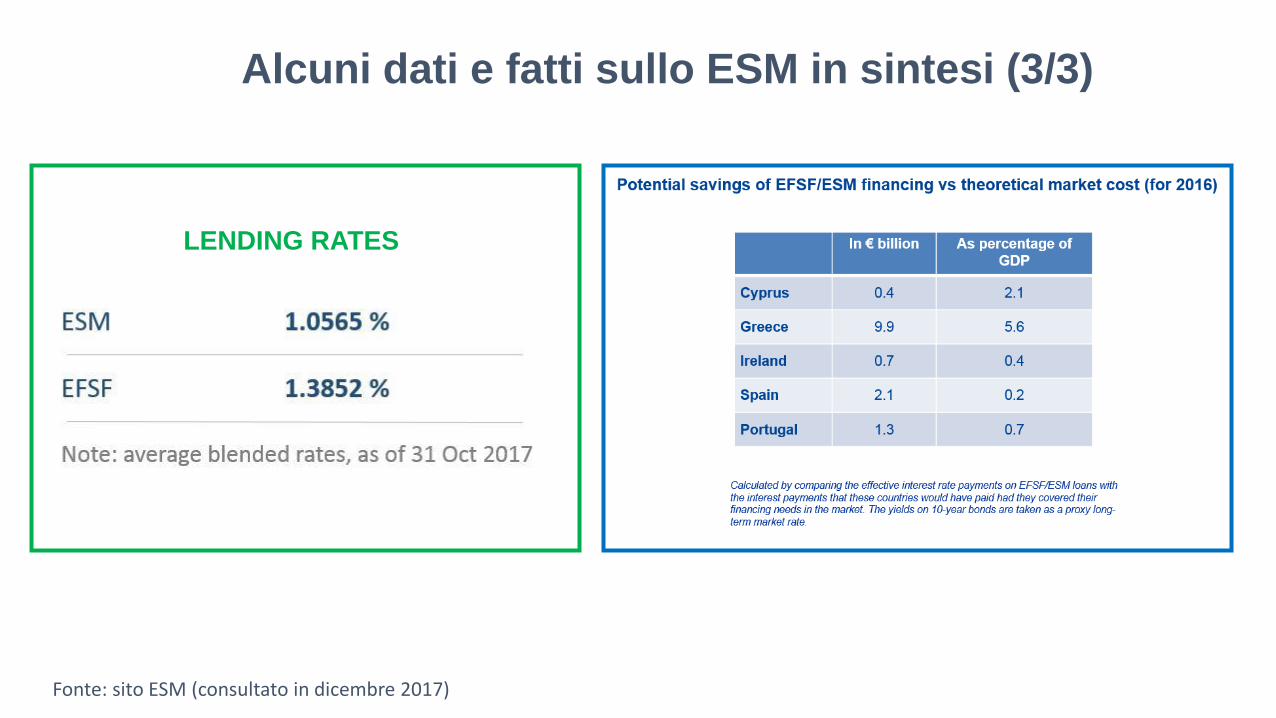

Alcuni dati e fatti sullo ESM in sintesi (1/3)

Fonte: sito ESM (consultato in dicembre 2017)

Fonte: sito ESM (consultato in dicembre 2017)

Alcuni dati e fatti sullo ESM in sintesi (2/3)

Fonte: sito ESM (consultato in dicembre 2017)

Alcuni dati e fatti sullo ESM in sintesi (3/3)

LENDING RATES

La BCE e lo ESM: un «connubio» virtuoso possibile

© CRANEC/AQC

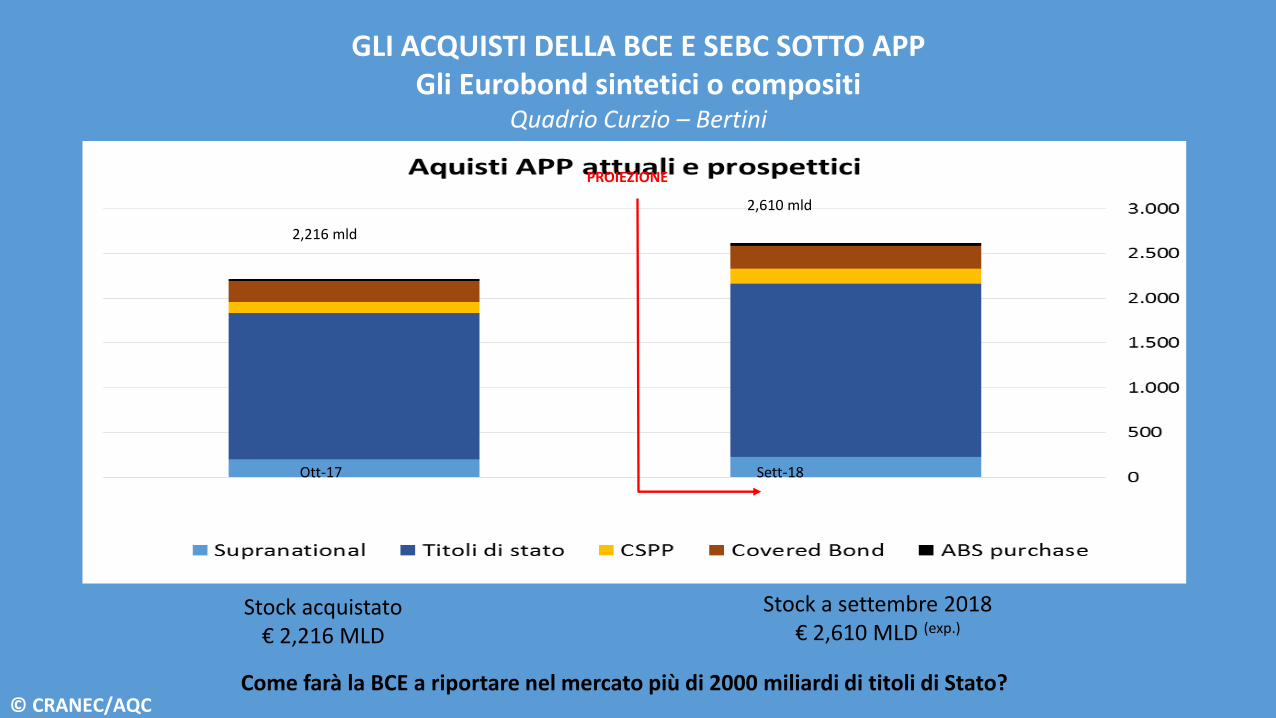

GLI ACQUISTI DELLA BCE E SEBC SOTTO APP Gli Eurobond sintetici o compositi

Quadrio Curzio – Bertini

PROIEZIONE

Stock acquistato € 2,216 MLD

Ott-17

2,216 mld

2,610 mld

Sett-18

Stock a settembre 2018 € 2,610 MLD (exp.)

Come farà la BCE a riportare nel mercato più di 2000 miliardi di titoli di Stato? © CRANEC/AQC

ESM = FFE+FES BCE RIENTRA DALLA POLITICA MONETARIA

ESPANSIVA QE (APP DI CUI PSPP E CSPP +

TLTRO ) MARZO 2015

IMPULSO ALLA COESIONE EUROPEA E 2° PILASTRO ALLA IRREVERSIBITA’ DEL PROGETTO UEM

MODIFICA ESM MARZO 2018

CREAZIONE di due SPV MARZO 2018

STRUTTURAZIONE PORTAFOGLI DI

GARANZIA OTTOBRE 2018

EMISSIONE di EueoUnionBond = a EURO(SAFE)BOND più EUROINVESTMENT BOND

MARZO 2019

IMPULSO ALLA CRESCITA di € MLD da 675 a 3,350

secondo la leva (da 3 a 15)

DALL’ESM ALL’EURO-MEF:

fine mandato Draghi alla BCE OTTOBRE 2019

3° Pilastro BANKING UNION

European Deposit Insurance

© CRANEC/AQC

IL FFE(fondo Finanziario europeo) E GLI EUROSAFEBOND Ipotesi Quadrio Curzio - Bertini

SPV = Special Purpuse Vehicle

The European Stability Mechanism (ESM) is an important component of the comprehensive EU strategy designed to safeguard financial stability within the euro area. ESM should create a S.P.V.=FFE that brings together national securities purchased under PSPP program and then cc issues Eurobonds

ESM

Nuovo ESM S.P.V.=FFE (Fondo Finaziario Europeo

Rating AAA

Paid-in Capital € 80.5 MLD

Capitale sottoscritto € 704.8 MLD

Azionariato ripartito secondo le proporzioni della Capital Key come BCE € 80.5 MLD Paid-in Capital

CAPITALE SUPPLEMENTARE

€ 845 MLD (o € 1,350 MLD a marzo 2017) Titoli di Stato PSPP

Capitale di garanzia aggiuntivo SPV : 120 MLD richiamati da C. sottoscritto e/o 180 MLD di riserve auree SEBC

GARANZIA AL 22% SULLE NUOVE EMISSIONI

Il portafoglio di titoli conferito da BCE e SEBC che chiamiamo Eurobond Sintetici genera altrettanti EuroUnionBond

20%* DEI BOND EUROPEI CON

GARANZIA SPV DEL 22%

* Bond europei considerati eligible BCE (aggregato inferiore al debito pubblico totale)

CON UN CAPITALE

© CRANEC/AQC

3

Nuove emissioni € 3375 MLD

IL FES (fondo europeo sviluppo)E EUROINVESTMENTBOND Ipotesi Quadrio Curzio - Bertini

€ 8 MLD Paid-in Capital + 8MLD impegnati € 5 MLD dalla BEI

CON UN CAPITALE

Elevare in chiave pro-ciclica l’attività attualmente svolta da FEIS e BEI in complementarietà con il Piano Juncker

Dal FEIS del Piano Juncker al FES

FEIS Attuale

Effetto moltiplicatore stimato P-Juncker 1 : 15 = € 315 MLD (exp.)

Ipotesi Rating : AAA

CAPITALE GARAZIA TOT. € 250 MLD

SPV FES EUROINVESTMENTBOND

FEIS Cap. Upgrade

+ Riserve Auree SEBC PER € 107 MLD+120 da ESM

Trasferimento all’SPV-FES dei Titolo Supranational e sotto CSPP € 122 MLD (o € 225 MLD a marzo 2017)

EMISSIONE DI EUROINVESTMENTBOND

Nuove emissioni € 1125 MLD

1

Leva fin. 1 : 3 Garanzia SPV 37%

Nuove emissioni € 675 MLD

base* 2

Leva fin. 1 : 5

Garanzia SPV 22%

accelerata*

Leva fin. 1 : 15

Garanzia SPV 7,5%

P.Juncker*

* La leva finanziaria deve esse dipendente dai tassi BCE per favorire collegamento e pro-ciclicità della politica monetaria

Ipotesi Ipotesi Ipotesi

© CRANEC/AQC

Il Piano Juncker è un buon inizio per gli investimenti

© CRANEC/AQC

Fonte: European Commission, Un piano di investimenti per l’Europa. Sito Commissione Europea. © CRANEC/AQC

Fonte: European Commission, Un piano di investimenti per l’Europa. Sito Commissione Europea.

Troppe buone intenzioni

© CRANEC/AQC

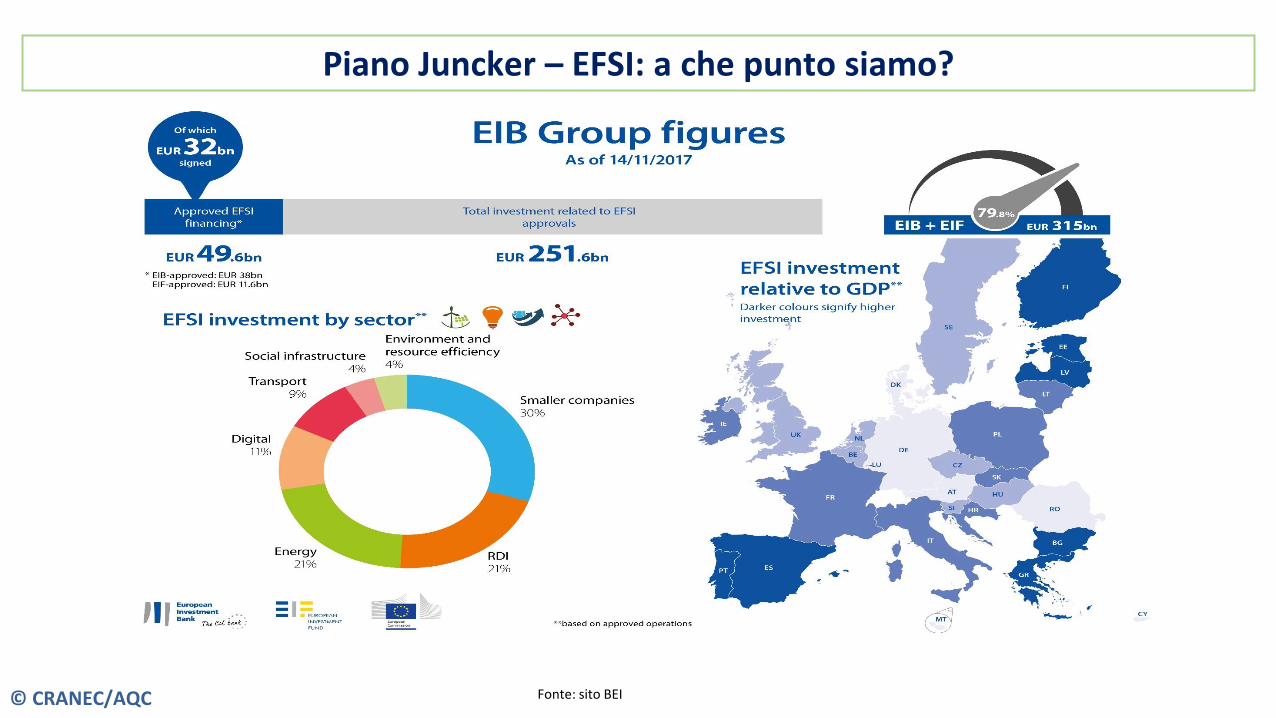

Piano Juncker – EFSI: a che punto siamo?

Fonte: sito BEI © CRANEC/AQC

Fonte: European Commission, The Investment Plan for Europe: Two years on, 2016

© CRANEC/AQC

Che non basta per recuperare gli investimenti europei nella crisi: ci vogliono gli Euroinvestmentbond

© CRANEC/AQC

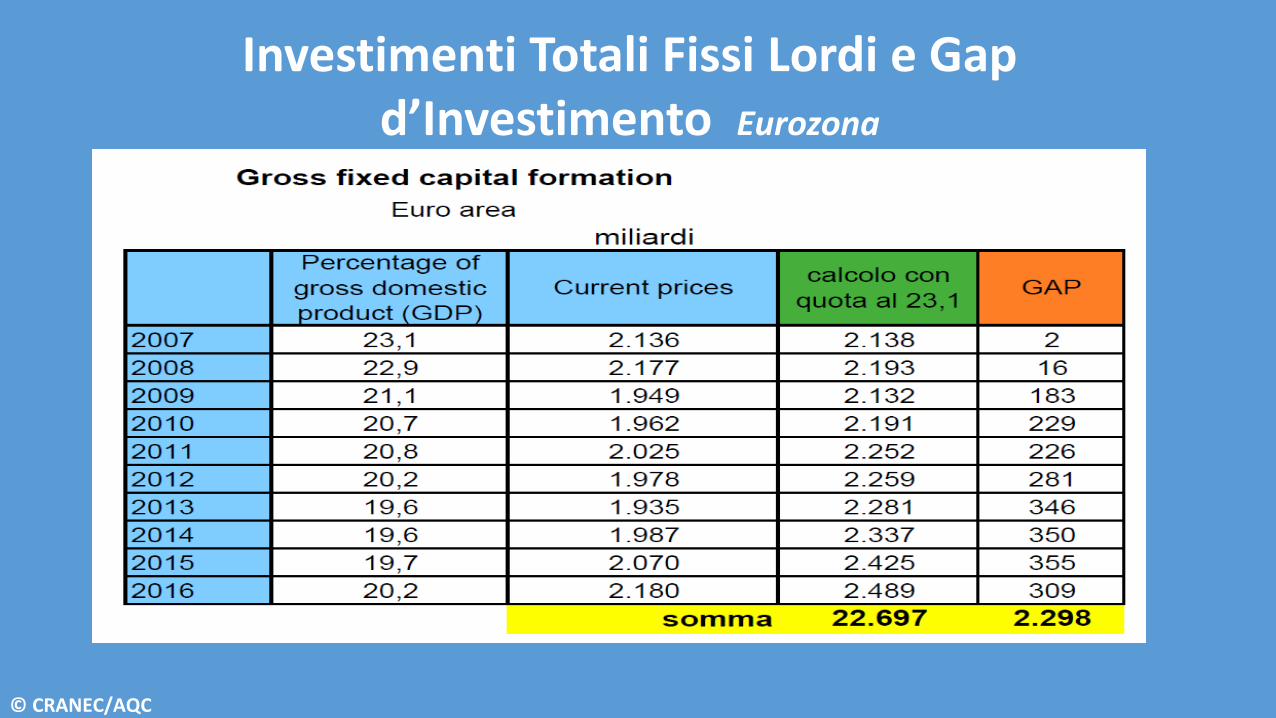

Fonte: DG ECFIN, AMECO Database, 2016 © CRANEC/AQC

Investimenti Totali Fissi Lordi e Gap d’Investimento Eurozona

© CRANEC/AQC

How big are Europe’s investment gaps?

Fonte: EIB, Restoring EU Competitiveness, 2016 © CRANEC/AQC

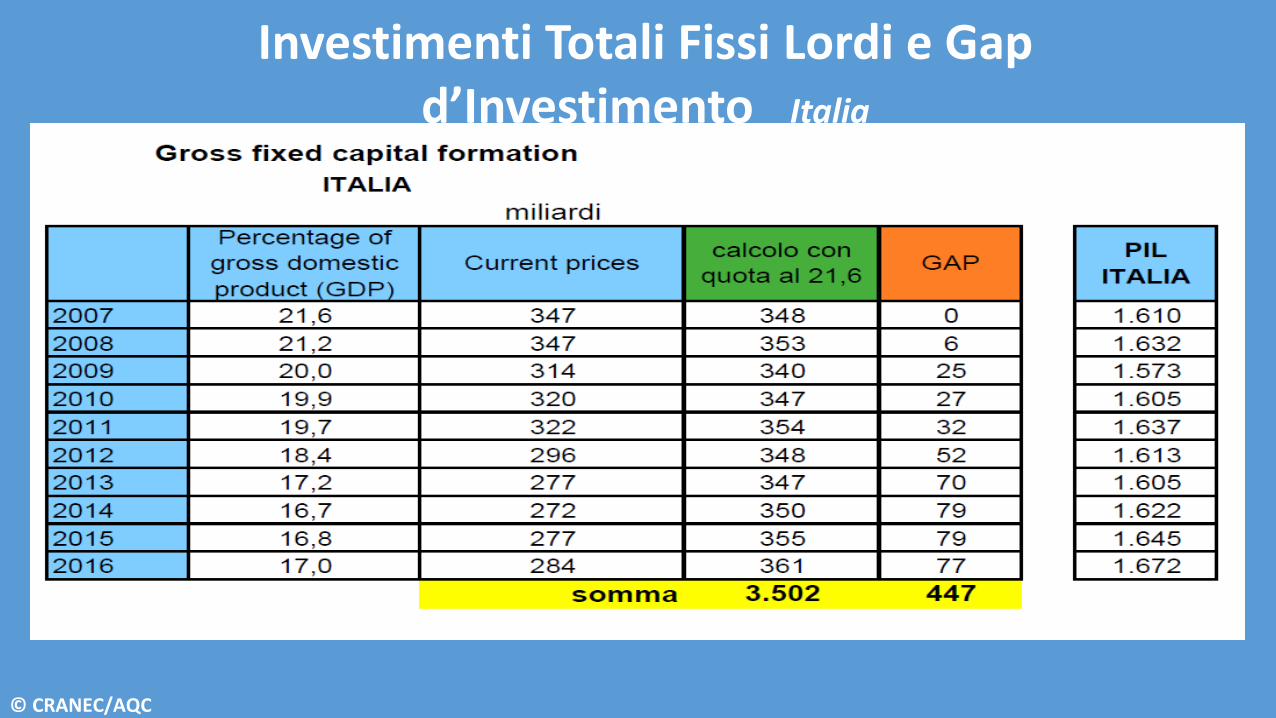

Investimenti Totali Fissi Lordi e Gap d’Investimento Italia

© CRANEC/AQC

Investimenti settore trasporti (porti, aeroporti, strade, ferrovie)

Investimenti totali (trasporti, sistemi idraulici, telecomunicazioni)

Fonte: elaborazione su dati GiHub 2017 – Global Infrastructure Outlook – a G20 initiative

2017 2018 2019 2020 2021 2022 2023 2024 Tot

Trend Investimento 21,6 mld/$ 21,8 mld/$ 22,2 mld/$ 22,3 mld/$ 22,5 mld/$ 22,6 mld/$ 22,8 mld/$ 22,9 mld/$ 178,7 mld/$

Fabbisogno effettivo 30,6 mld/$ 31,2 mld/$ 32 mld/$ 32,5 mld/$ 33 mld/$ 33,6 mld/$ 34,1 mld/$ 34,7 mld/$ 261,7 mld/$

Δ (Gap) 9 mld/$ 9,4 mld/$ 9,8 mld/$ 10,2 mld/$ 10,5 mld/$ 11 mld/$ 11,3 mld/$ 11,8 mld/$ 83 mld/$

2017 2018 2019 2020 2021 2022 2023 2024 Tot.

Trend Investimento 44,7 mld/$ 46,5 mld/$ 46,9 mld/$ 47,2 mld/$ 47,2 mld/$ 47,2 mld/$ 47,5 mld/$ 47,5 mld/$ 374,7 mld/$

Fabbisogno effettivo 54,7 mld/$ 56,9 mld/$ 57,8 mld/$ 58,5 mld/$ 58,8 mld/$ 59,4 mld/$ 60,2 mld/$ 60,6 mld/$ 466,9 mld/$

Δ (Gap) 10 mld/$ 10,4 mld/$ 10,9 mld/$ 11,3 mld/$ 11,6 mld/$ 12,2 mld/$ 12,7 mld/$ 13,1 mld/$ 92,2 mld/$

© CRANEC/AQC

CRANEC – CENTRO DI RICERCHE IN ANALISI ECONOMICA FONDAZIONE ASTRID

Università Cattolica del Sacro Cuore

Lunedi 4 Dicembre 2017

Prof. Alberto Quadrio Curzio Accademia Nazionale dei Lincei Università Cattolica del Sacro Cuore

@: non citare senza il permesso dell’autore / do not cite without author’s permission

Gli Euro-Union Bond= Euro-Safe Bond+Euro-InvestmentBond

il traguardo