La Capitale Automobile CARS 2014 - Slides del convegno

133

9° summit degli operatori della distribuzione automobilistica Venerdì 24 ottobre2014 Roma – Auditorium del Massimo

-

Upload

fleetmobility -

Category

Automotive

-

view

898 -

download

0

Transcript of La Capitale Automobile CARS 2014 - Slides del convegno

9° summit degli operatori della distribuzione automobilistica

Venerdì 24 ottobre2014Roma – Auditorium del Massimo

Associazioni

Corrado Piazzalunga,

Assilea

Fabrizio Ruggiero,

Aniasa

Gianfranco Soranna

Federauto

Romano Valente,

Unrae

Mobilità

Pierluigi Bonora

Missione Mobilità

Pier Luigi Del Viscovo

Fleet&Mobility

InsuranceGianpiero

Mosca,

Aon Re Trust Broker

Dealer

Luciano Belluzzo,

Audi Zentrum

Adolfo De Stefani

Cosentino,

De Stefani

Piero Mocarelli,

Mocauto

Plinio Vanini,

Autotorino

Case

Michele Crisci,

Volvo

Daniele Maver,

Jaguar Land Rover

Nicola Pumilia,

FCA

Outlook globale su car industry

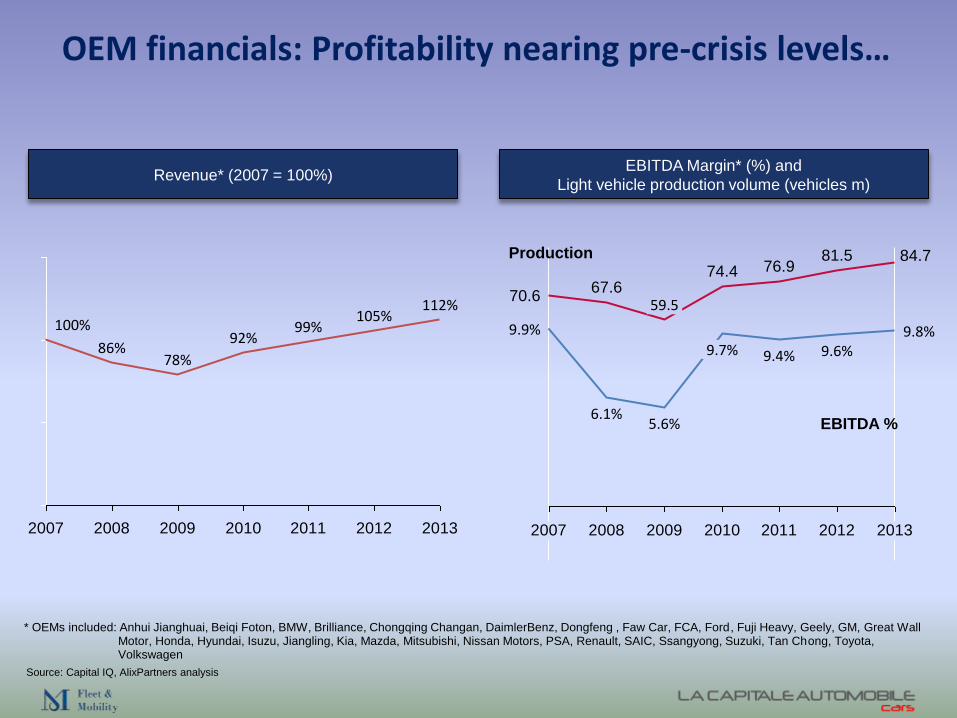

OEM financials: Profitability nearing pre-crisis levels…

2007 2008 2009 2010 2011 2012 2013

105%112%

92%99%

86%78%

100%

2007 2008 2009 2010 2011 2012 2013

84.781.5

9.8%

76.9

9.6%

74.4

9.4%

59.5

9.7%

67.6

5.6%

70.6

6.1%

9.9%

Production

EBITDA %

Source: Capital IQ, AlixPartners analysis

Revenue* (2007 = 100%)EBITDA Margin* (%) and

Light vehicle production volume (vehicles m)

* OEMs included: Anhui Jianghuai, Beiqi Foton, BMW, Brilliance, Chongqing Changan, DaimlerBenz, Dongfeng , Faw Car, FCA, Ford, Fuji Heavy, Geely, GM, Great Wall Motor, Honda, Hyundai, Isuzu, Jiangling, Kia, Mazda, Mitsubishi, Nissan Motors, PSA, Renault, SAIC, Ssangyong, Suzuki, Tan Chong, Toyota, Volkswagen

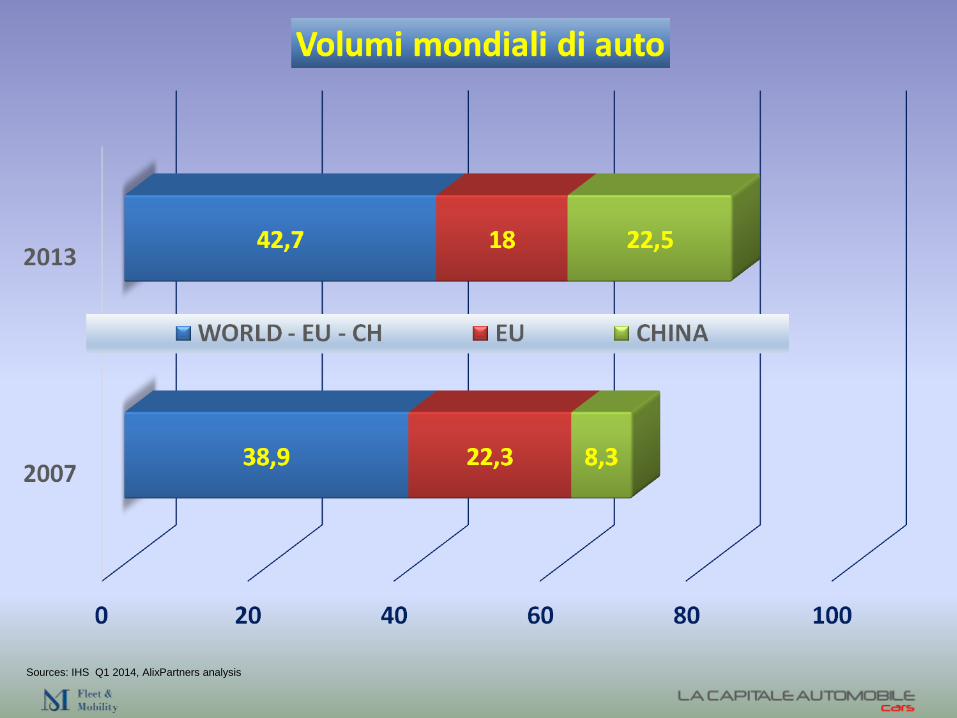

Global industry up 20% vs. pre-crisis, but Europe down 19%

Light vehicles sales volume 2007-2013 [units m]

World Europe

2012

79.4

2011

75.6

2010

72.4

+20%

2013

83.2

2009

63.8

2008

66.0

2007

69.5

16.9

5.4

15.4

5.8

15.0

3.4

14.5

19.3

2010

18.4

2009

18.4

2008

14.4

4.9

13.2

5.1

12.9

5.0

21.2

2007

22.3

2013

-19%

18.0

2012

18.3

2011

3.9

Sources: IHS Global Insight Q1 2014, AlixPartners analysis

W EuropeCE Europe

Sources: IHS Q1 2014, AlixPartners analysis

The growth continues to be unevenly spread across the globe; mature

markets saturated and mainly driven by replacement demand

Global LV volumes sold 2007-2019 [vehicles m]

Central / Eastern Europe

North America

C/S America

Vehicles sales [units m]

16.9

x.x

69.5

Greater China*

Japan / South Korea

Western Europe

Other**

Worldwide

Sources: IHS Q1 2014, AlixPartners analysis * China, Hong Kong, Taiwan ** India, ASEAN, Middle East, Africa, Oceania

103%

20192014

102%

2013

100%

2012

97%

2009

67%

2007

100%

2019

90%

2014

81%

2014

79%

2013

77%

2009

89%

2007

100%

2019

122%100%

2014

91%

2013

87%

2012

93%

2009

62%

2007

363%

20192014

305%

2013

285%

2012

262%

2009

159%

2007

100%

2019

164%

2012

139%

2009

101%

2007

100%

2014

138%

2013

135%

180%

20192014

146%

2013

137%

2012

135%

2009

124%

2007

100%

96%

20192014

99%

2013

100%

2012

104%

2009

93%

2007

100%

2009

95%

2007 2015

128%

2014

123%

2013

120%

2019

146%

100%

66.0 83.2 85.4 89.2 101.4

15.0 12.9 13.3 13.7 15.2 5.4 3.4 5.0 4.7 5.9 6.6

4.3 4.3 5.9 5.7 5.9 7.0

18.9 12.7 18.4 18.9 19.3 19.6

9.2 11.4 12.4 12.6 13.5 16.6

6.4 6.0 6.7 6.5 6.4 6.2

8.3 13.3 21.8 23.7 25.4 30.3

Ten-year outlook globally: Sales to grow 31%, to 109M units –an increase of more than 26M units

LV volumes sold 2007-2023 [vehicles m]

109107106

10310199

9793

8985

8379

7672

646669

201920182017201620152014 20212020

+31%

+20%

20232022201320122011201020082007 2009

Sources: IHS Global Insight Q1 2014, AlixPartners analysis

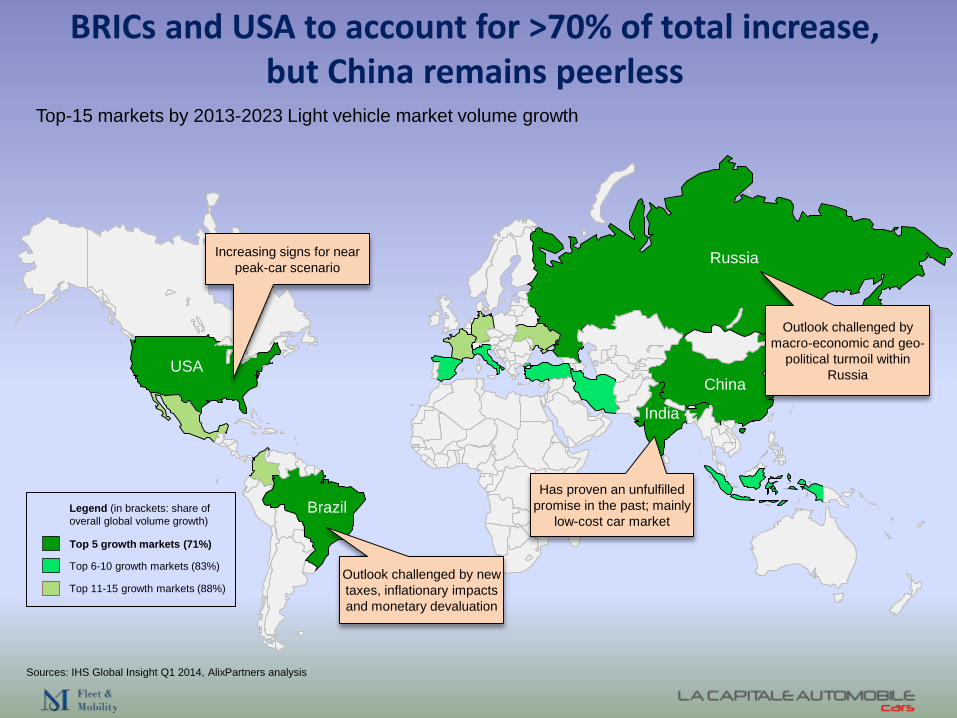

Total industry volume growth

2013-23: +26.1m vehicles

China

Russia

India

Brazil

USA

BRICs and USA to account for >70% of total increase, but China remains peerless

Sources: IHS Global Insight Q1 2014, AlixPartners analysis

Top-15 markets by 2013-2023 Light vehicle market volume growth

Top 5 growth markets (71%)

Legend (in brackets: share of

overall global volume growth)

Top 11-15 growth markets (88%)

Top 6-10 growth markets (83%)Outlook challenged by new

taxes, inflationary impacts

and monetary devaluation

Outlook challenged by

macro-economic and geo-

political turmoil within

Russia

Has proven an unfulfilled

promise in the past; mainly

low-cost car market

Increasing signs for near

peak-car scenario

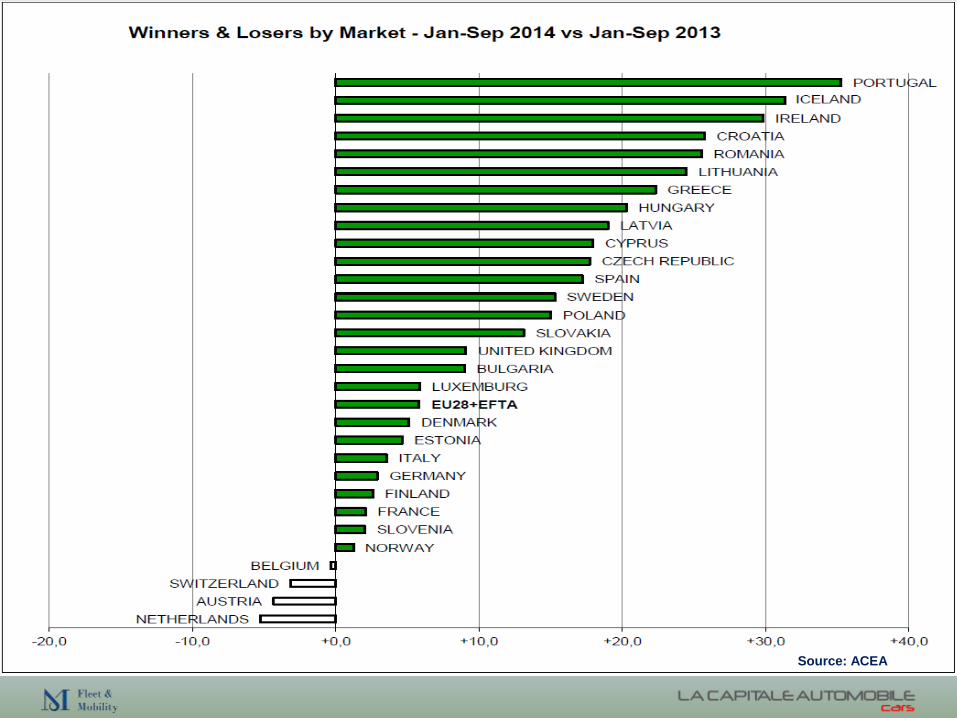

Europe industry challenges

Source: ACEA

But many markets still below pre-crisis levels in 2013

Sources: IHS Global Insight Q1 2014, AlixPartners analysis

Light vehicle sales volume comparison 2013 vs 2007

>25%

% change

15-25%

5-15%

5% - -5%

-5% - -15%

-15% - -25%

-25% - -35%

>-35%

Germany

Russia

UK

France

Italy Turkey

Spain

Belgium

Netherlands

Austria

The top-10 markets

called out in writing

account for 83% of

the total European

sales volume in

2013

WESTERN EUROPE

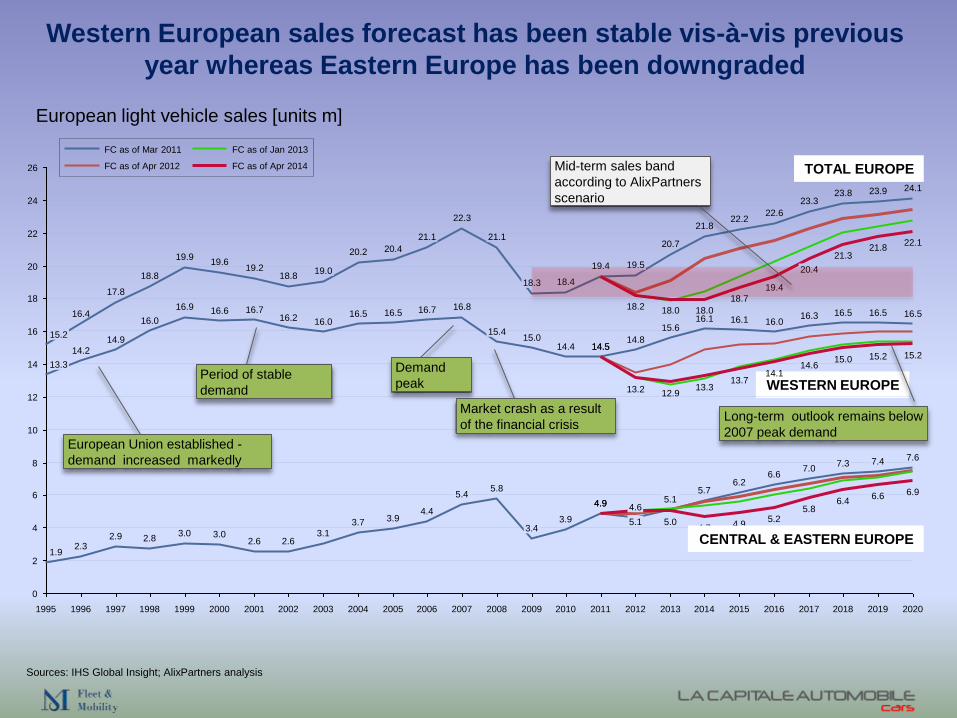

Western European sales forecast has been stable vis-à-vis previous

year whereas Eastern Europe has been downgraded

16

14

12

2007200620052004200320022001200019991998199719961995

10

8

6

26

24

22

4

20

18

2

0

2020201920182017201620152014201320122011201020092008

18.7

4.9

13.7

22.2

6.2

16.118.0

4.7

13.3

21.8

5.7

16.118.0

22.1

6.9

15.2

24.1

7.6

16.5

6.6

15.2

23.9

7.4

16.5

21.3

6.4

15.0

21.8

23.8

7.3

16.5

20.4

5.8

14.6

23.3

7.0

16.3

19.4

5.2

14.1

22.6

6.6

16.0

5.0

12.9

20.7

5.1

15.6

18.2

5.1

13.2

19.5

4.6

14.8

19.4

4.9

14.5

19.4

4.9

14.5

18.4

3.9

14.4

18.3

3.4

15.0

21.1

5.8

15.4

22.3

5.4

16.8

21.1

4.4

16.7

20.4

3.9

16.5

20.2

3.7

16.5

19.0

3.1

16.0

18.8

2.6

16.2

19.2

2.6

16.7

19.6

3.0

16.6

19.9

3.0

16.9

18.8

2.8

16.0

17.8

2.9

14.9

16.4

2.3

14.2

15.2

1.9

13.3

TOTAL EUROPE

CENTRAL & EASTERN EUROPE

Period of stable

demand

Demand

peak

European Union established -

demand increased markedly

Market crash as a result

of the financial crisisLong-term outlook remains below

2007 peak demand

Mid-term sales band

according to AlixPartners

scenario

FC as of Apr 2014

FC as of Mar 2011 FC as of Jan 2013

FC as of Apr 2012

European light vehicle sales [units m]

Sources: IHS Global Insight; AlixPartners analysis

Perché è tanto difficile azzeccare le previsioni di mercato?

E perché, comunque, si sbaglia sempre per eccesso?

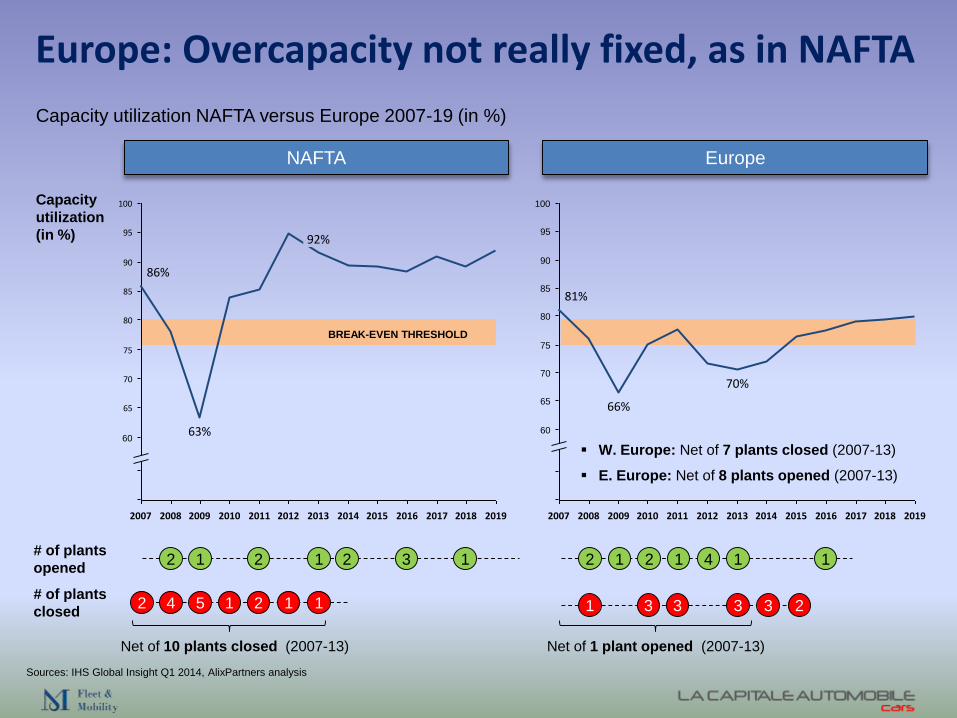

Europe: Overcapacity not really fixed, as in NAFTA

Capacity utilization NAFTA versus Europe 2007-19 (in %)

NAFTA Europe

Sources: IHS Global Insight Q1 2014, AlixPartners analysis

95

90

85

80

75

70

65

60

2019201820172016201520142013201220112010200920082007

100

70%

66%

81%

100

95

90

85

80

75

70

65

60

2010200920082007 2012 2013 2014 2015 2016 2017 2018 20192011

92%

63%

86%

Capacity

utilization

(in %)

BREAK-EVEN THRESHOLD

# of plants

opened2 1 2 1

# of plants

closed2 4 1 15 2 1

2 1 2 1

1 3 3 3

1 4

Net of 10 plants closed (2007-13)

W. Europe: Net of 7 plants closed (2007-13)

E. Europe: Net of 8 plants opened (2007-13)

2 3 1

3 2

1

Net of 1 plant opened (2007-13)

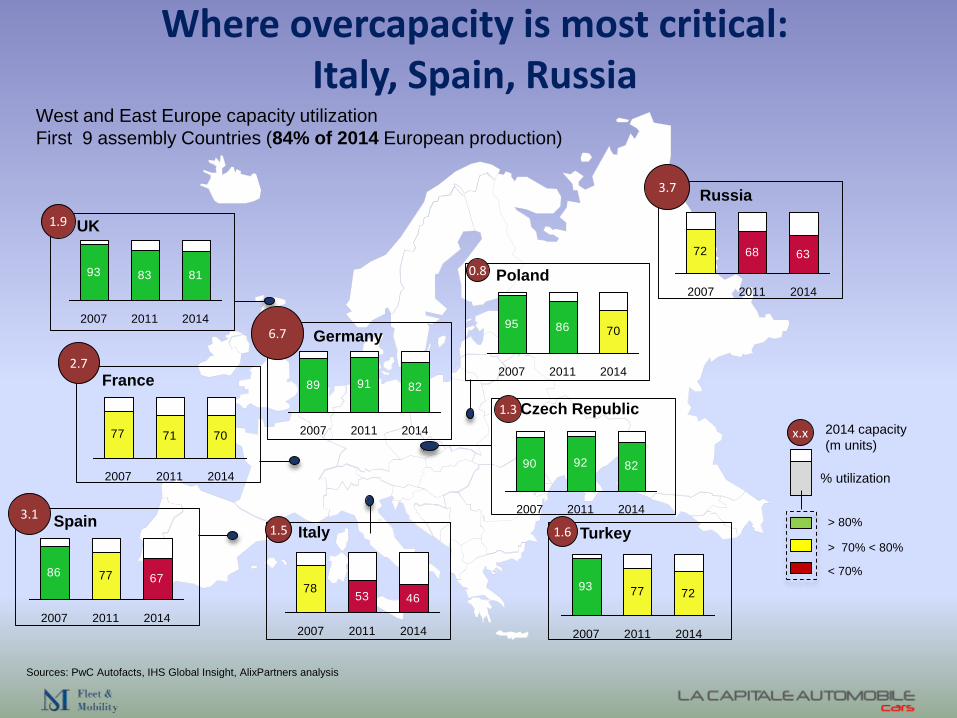

Where overcapacity is most critical: Italy, Spain, Russia

Germany

Spain

France

Russia

UK

Turkey

Poland

Sources: PwC Autofacts, IHS Global Insight, AlixPartners analysis

West and East Europe capacity utilization

First 9 assembly Countries (84% of 2014 European production)

Italy

Czech Republic

% utilization

2014 capacity

(m units)

6.7

2.7

3.1

3.7

1.9

1.61.5

0.8

1.3

x.x

> 80%

> 70% < 80%

< 70%

93 83 81

201420112007

89 91 82

201420112007

95 86 70

201420112007

68 6372

201420112007

77 7293

201420112007

53 4678

2007 20142011

677786

201420112007

77 71 70

2011 2014200790 92 82

201420112007

Il WTO ha rivisto al ribasso le previsioni di crescita del commercio.

Che impatto si prevede sulle fabbriche europee di automobili?

Che pressione sul mercato Italia?

Source: WTO

Tensioni. Incertezze. Imprevedibilità dei mercati. Crescita meno stabile.

• USA (disoccupazione <6%) e UK (PIL +3,2%) fuori dal tunnel.

• Europa in recessione

• Giappone: fine della crescita (più IVA ha frenato i consumi)

• Russia e Brasile, stagnazione se va bene.

• China (+7,5% PIL) ma rischio credit bubble e calo produttività

Source: The Economist

Parco circolante e domanda di auto nuove

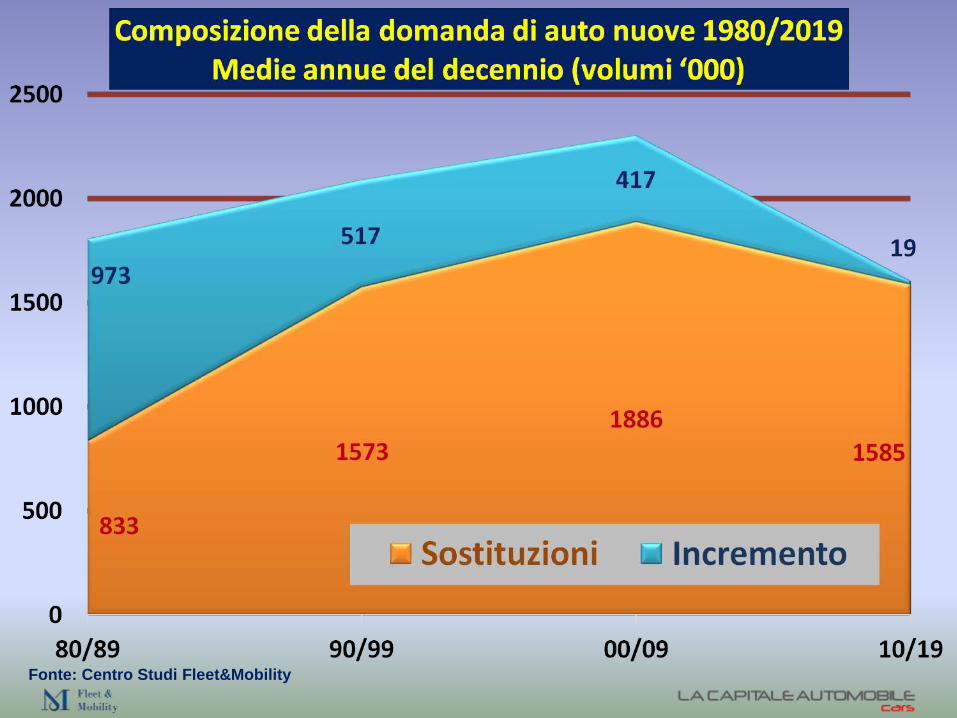

(valori '000) 80/'89 90/'99 00/'09 2010/2019

media circolante 21.905 29.806 34.593 36.972

incremento parco 9.730 5.168 4.167 194

immatricolazioni 18.064 20.894 23.024 16.040

incremento/parco 44% 17% 12% 0,5%

sostituzioni 8.334 15.726 18.857 15.846

immatr x anno 1.806 2.089 2.302 1.604

sostituz x anno 833 1.573 1.886 1.585

incremento x anno 973 517 417 19

sostituzioni/parco 38% 53% 55% 43%Fonte: Centro Studi Fleet&Mobility

Fonte: Centro Studi Fleet&Mobility

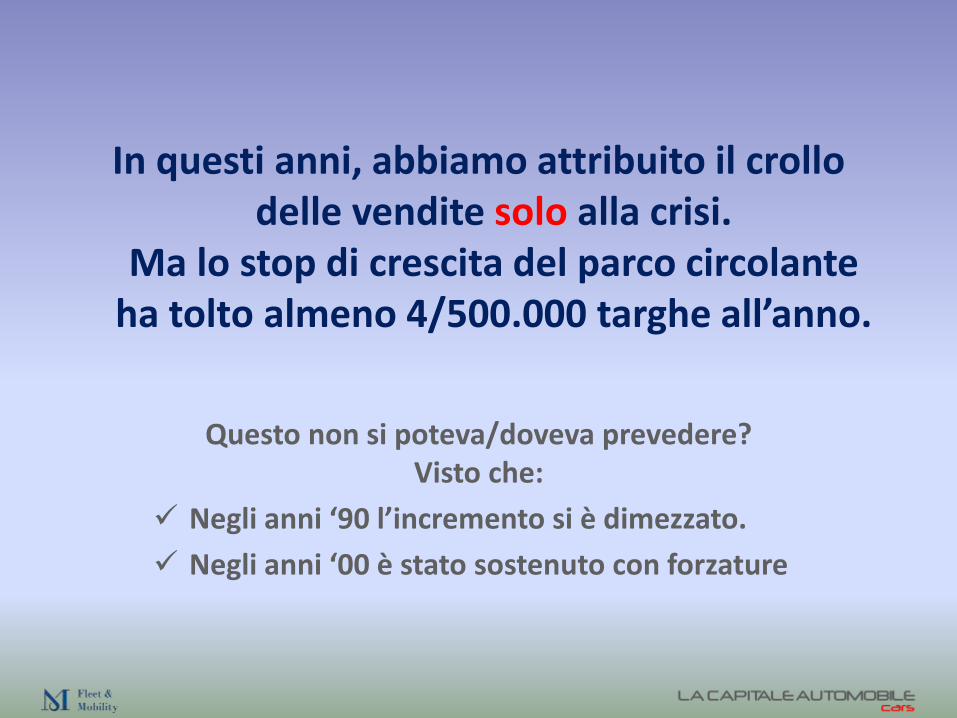

Nordio.Parco circolante. 1

In questi anni, abbiamo attribuito il crollo delle vendite solo alla crisi.

Ma lo stop di crescita del parco circolante ha tolto almeno 4/500.000 targhe all’anno.

Questo non si poteva/doveva prevedere? Visto che:

Negli anni ‘90 l’incremento si è dimezzato.

Negli anni ‘00 è stato sostenuto con forzature

Ficili. Parco circolante. 18

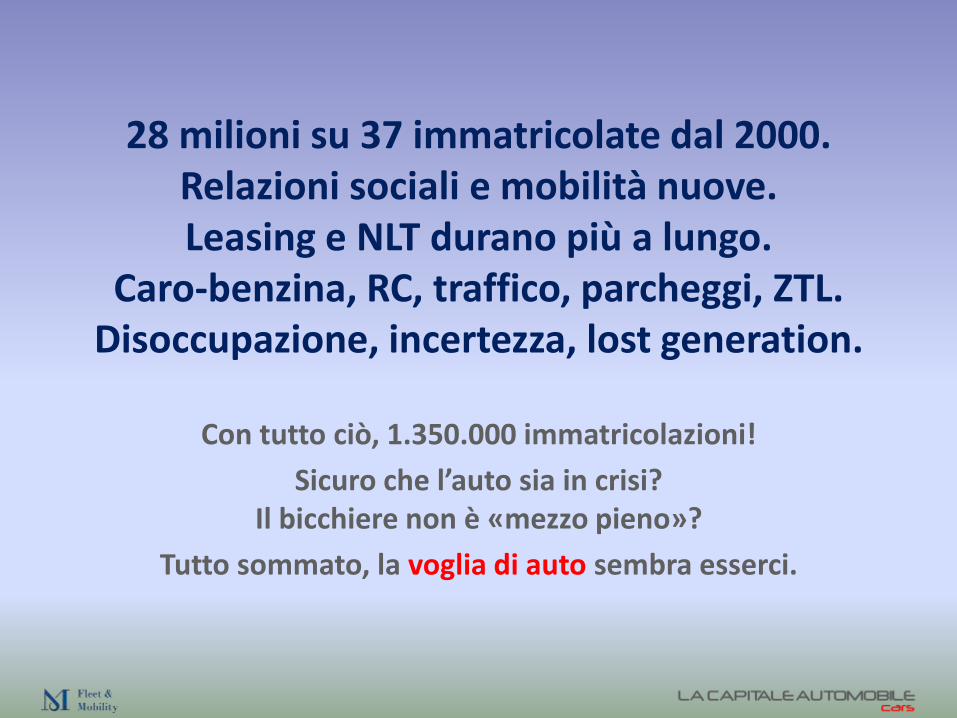

28 milioni su 37 immatricolate dal 2000.Relazioni sociali e mobilità nuove.Leasing e NLT durano più a lungo.

Caro-benzina, RC, traffico, parcheggi, ZTL.Disoccupazione, incertezza, lost generation.

Con tutto ciò, 1.350.000 immatricolazioni!

Sicuro che l’auto sia in crisi? Il bicchiere non è «mezzo pieno»?

Tutto sommato, la voglia di auto sembra esserci.

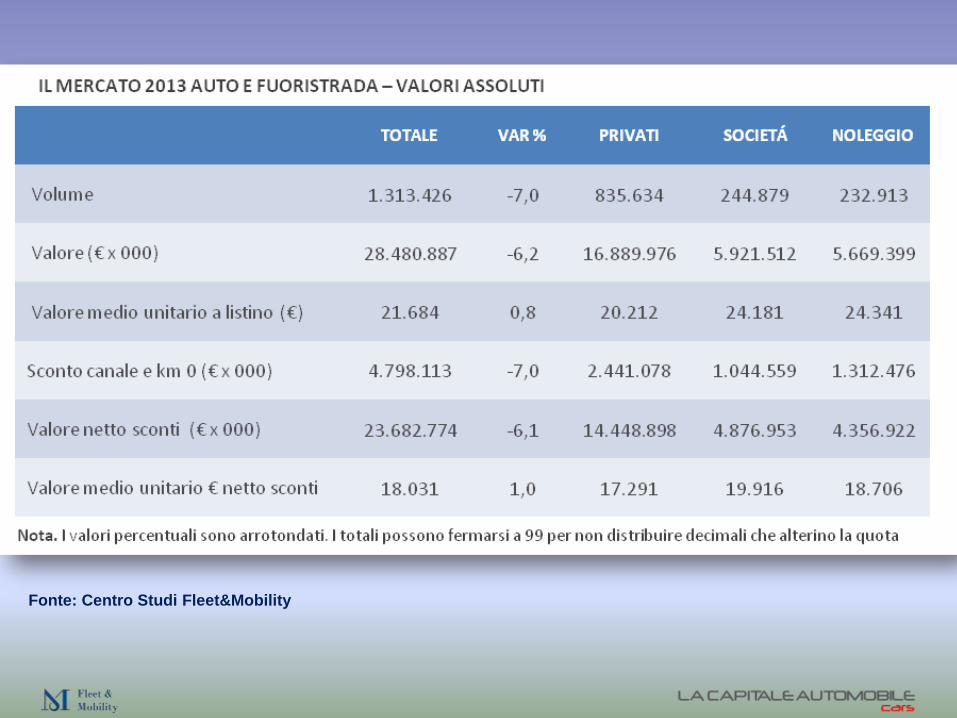

Mercato Italia.

Fonte: Centro Studi Fleet&Mobility

Fonte: Centro Studi Fleet&Mobility – UNRAE

Fo

nte

: C

en

tro

Stu

di

Fle

et&

Mo

bilit

y

Fo

nte

: C

en

tro

Stu

di

Fle

et&

Mo

bilit

y

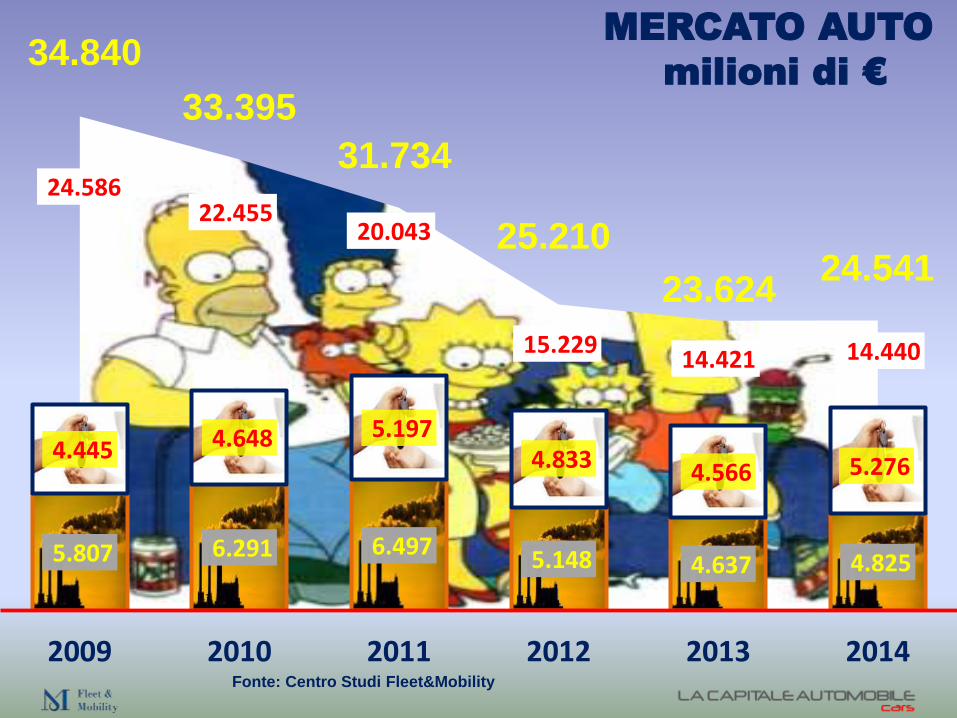

24.586 22.455

20.043

15.229 14.421 14.440

5.807 6.291 6.497 5.148 4.637 4.825

4.445 4.648 5.197 4.833 4.566 5.276

2009 2010 2011 2012 2013 2014

24.541

34.840

33.395

31.734

MERCATO AUTO

milioni di €

23.624

25.210

Fonte: Centro Studi Fleet&Mobility

Fonte: UNRAE

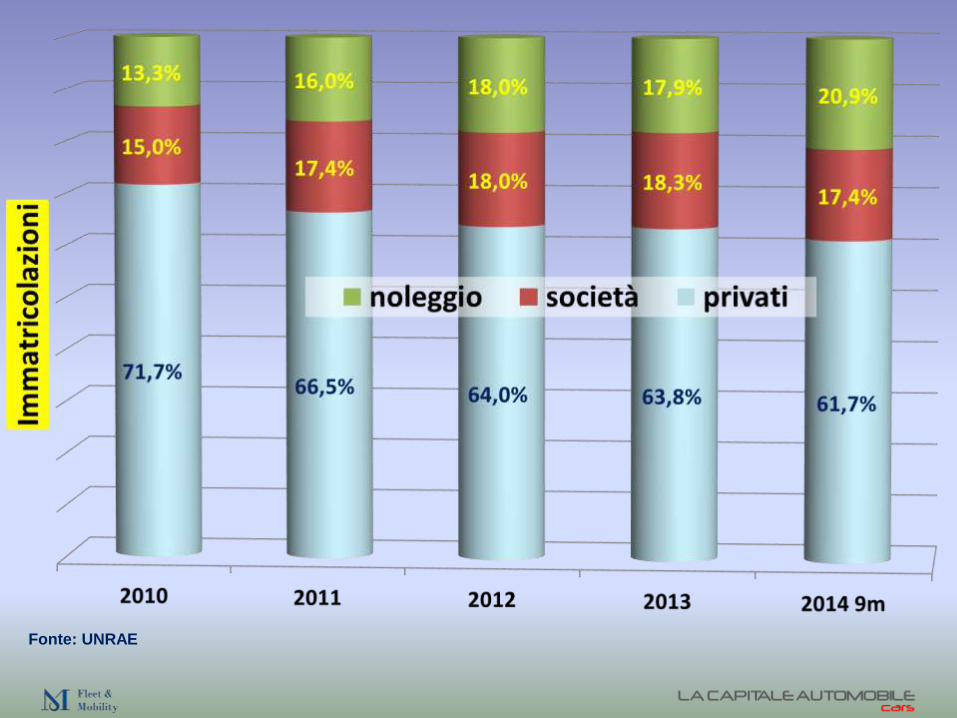

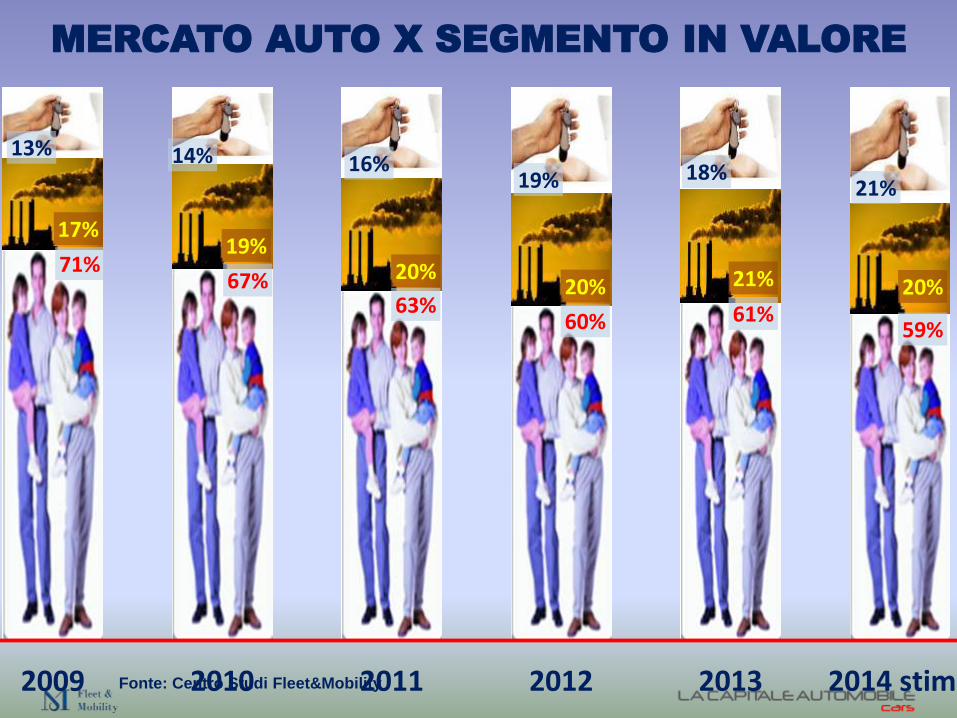

71%67%

63%60% 61%

59%

17%19%

20%20% 21% 20%

13% 14% 16%19% 18%

21%

2009 2010 2011 2012 2013 2014 stima

MERCATO AUTO X SEGMENTO IN VALORE

Fonte: Centro Studi Fleet&Mobility

Invece di abbassare le tasse sulle company car hanno

alzato quelle sulle famiglie. Il risultato è lo stesso, no?

Fonte: Centro Studi Fleet&Mobility

Atanasio. Flotte di prossimità. 19

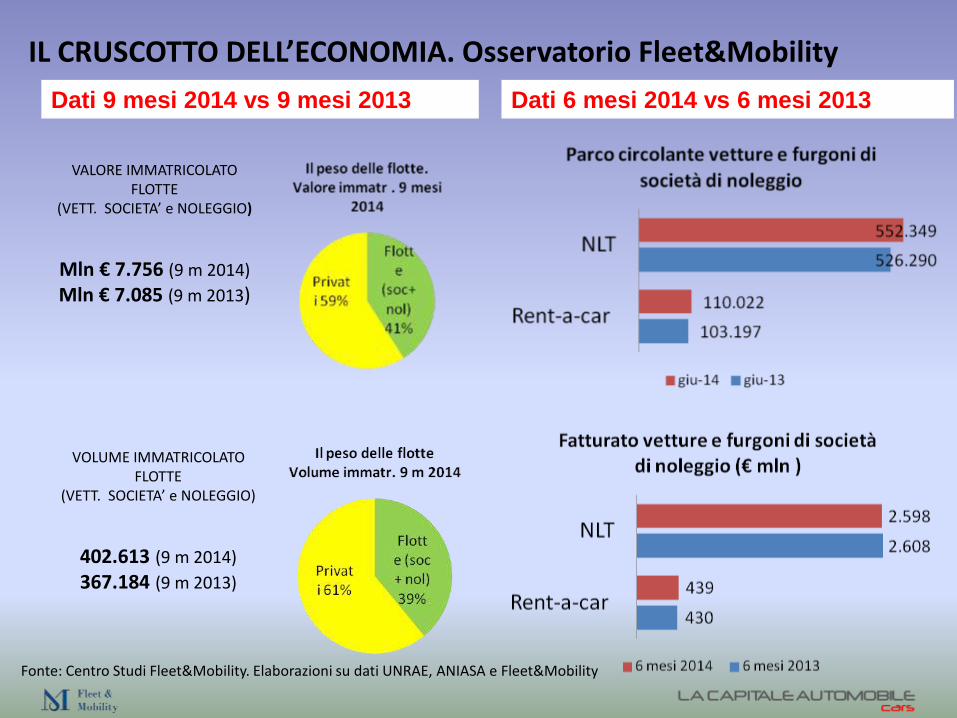

Fonte: Centro Studi Fleet&Mobility

VALORE IMMATRICOLATO FLOTTE

(VETT. SOCIETA’ e NOLEGGIO)

Mln € 7.756 (9 m 2014)

Mln € 7.085 (9 m 2013)

Fonte: Centro Studi Fleet&Mobility. Elaborazioni su dati UNRAE, ANIASA e Fleet&Mobility

IL CRUSCOTTO DELL’ECONOMIA. Osservatorio Fleet&Mobility

VOLUME IMMATRICOLATO FLOTTE

(VETT. SOCIETA’ e NOLEGGIO)

402.613 (9 m 2014)

367.184 (9 m 2013)

Dati 9 mesi 2014 vs 9 mesi 2013 Dati 6 mesi 2014 vs 6 mesi 2013

Leasing. 2014 v 2013

Fonte: Assilea

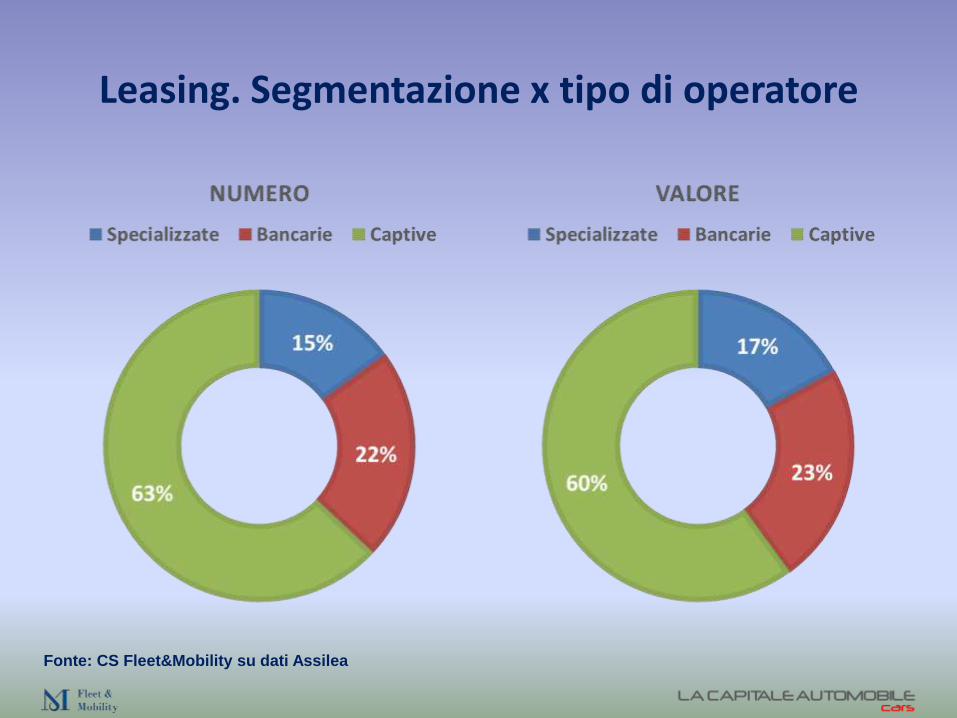

Leasing. Segmentazione x tipo di operatore

Fonte: CS Fleet&Mobility su dati Assilea

Leasing. Composizione del business

Fonte: CS Fleet&Mobility su dati Assilea

2015 = ? ______

9 mesi G-set ‘14 Var % G-set ‘13

Privati 641 = 640

Noleggio 217 +15% 189

Società 186 +4% 179

Mercato 1.044 +4% 1.007

Ipotesi STD 2014 Var % 2013

9 mesi 1.044 +3,7 1.007

Ott-dic 319 +4,9 304

Tot anno 1.363 +4,0 1.311

Ipotesi FCA 2014 Var % 2013

9 mesi 1.044 +3,7 1.007

Ott-dic 293 -3,6 304

Tot anno 1.337 +2,0 1.311

Fonte: Centro Studi Fleet&Mobility – UNRAE

Sistema Italia

Sta funzionando. Perchè?

Nordio.Mobilità privata. 7

Nordio.Missione Italia. 8

Bilanci dei dealer.

Courtesy of Italia Bilanci

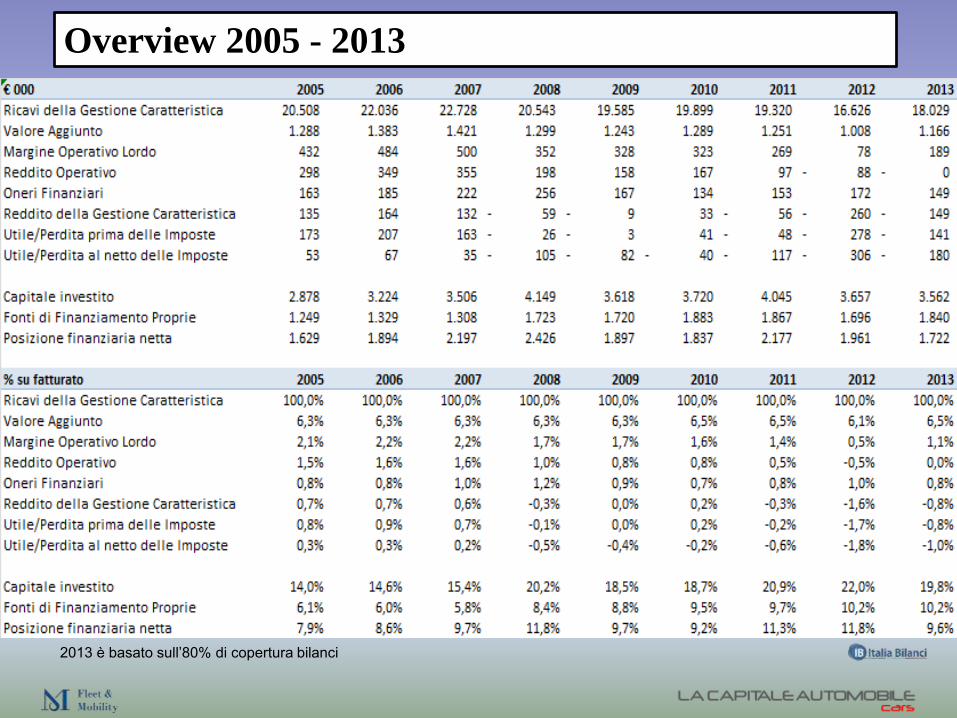

Overview 2005 - 2013

2013 è basato sull’80% di copertura bilanci

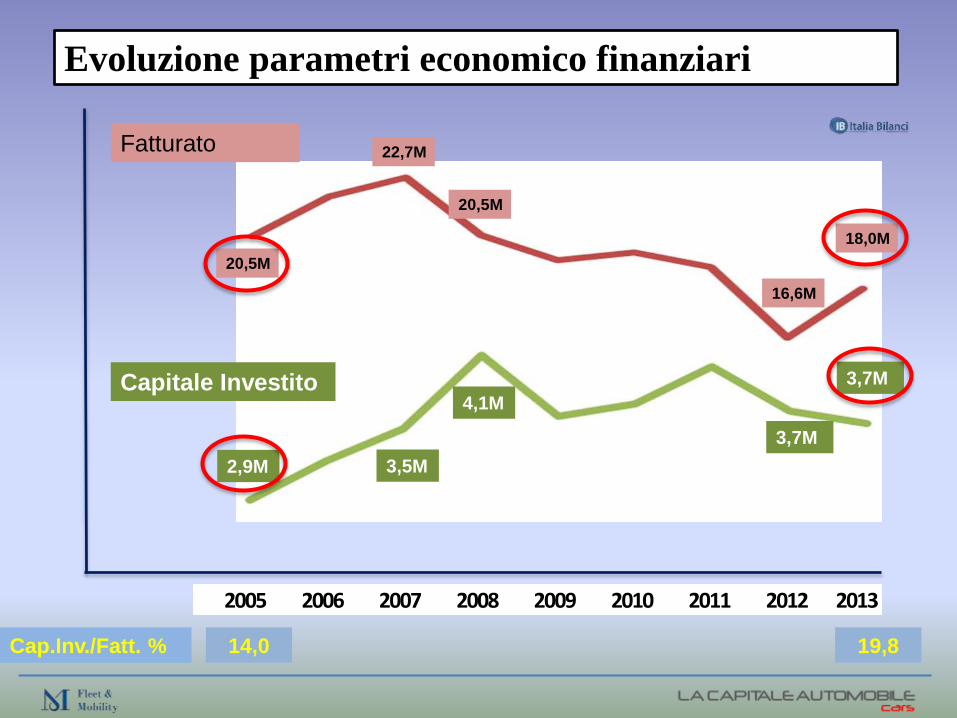

Evoluzione parametri economico finanziari

Dealer in perdita

Perdita cumulata : (830.000)

26% 25% 28% 47% 38% 38% 48% 60% 52%

3,5M

3,7M

2005 2006 2007 2008 2009 2010 2011 2012 2013

22,7M

16,6M

20,5M

Fatturato

Capitale Investito

Cap.Inv./Fatt. % 19,8

Evoluzione parametri economico finanziari

4,1M

2,9M

20,5M

18,0M

3,7M

14,0

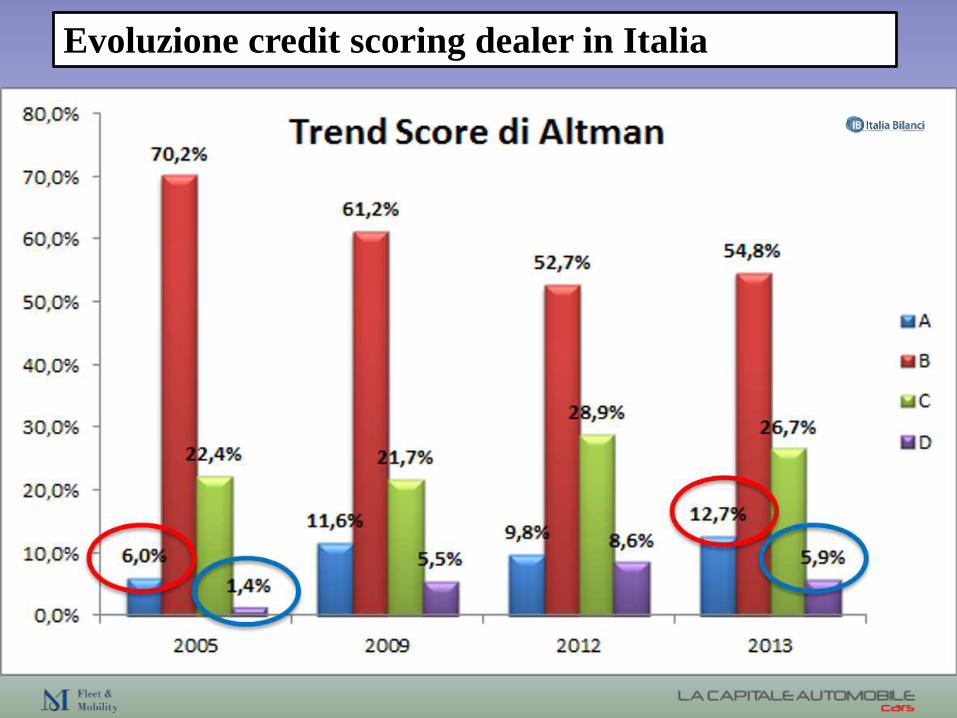

Evoluzione credit scoring dealer in Italia

Assicurazione.Gioie e dolori.

Courtesy of AON

438.48

718.79

241.98

2,250.55

453.36

715.59

246.55

2,226.73

C

L

M

B

2013 2012

Italy – portfolio avg premium by type of vehicle

AB analysis on Market data representing 91% of Mkt share

Total Average Premium

511.33

500.63

-2.1%

Y 2012

Y 2013

Italian Market –Number of vehicles

“not insured” and frauds

Source: ANIA – ASSICURAZIONE ITALIANA 2013/14

AreaInsured

vehicles

Not insured

vehicles

Tot.

circulating

vehicles

% of not

insured

vehicles

North 20,9 1,2 22,1 5,3%

Center 9,4 0,8 10,2 8,1%

South 10,1 1,5 11,6 13,1%

Total 40,4 3,5 43,9 8,0%

Not insured vehicles - 2013 estimated values (in million)

Country

% of frauds

on N° of

losses

% of

undetected

frauds

Italy -2% 7%-10%

France -1% 3%-5%

Germany n.d. 3%-5%

Spain -2% 3%-5%

UK -1,2% 3%-5%

MTPL frauds – European comparison

In Italy, according tothe Decree of January24th 2012«Disposizioni urgentiper la concorrenza, losviluppo delleinfrastrutture e lacompetitività», eachyear Italian insurancecompanies will have tosend to IVASS astandard report onfrauds (in case of non-submission of theannual report therewill be a penalty ofEuro 10.000-50.000)

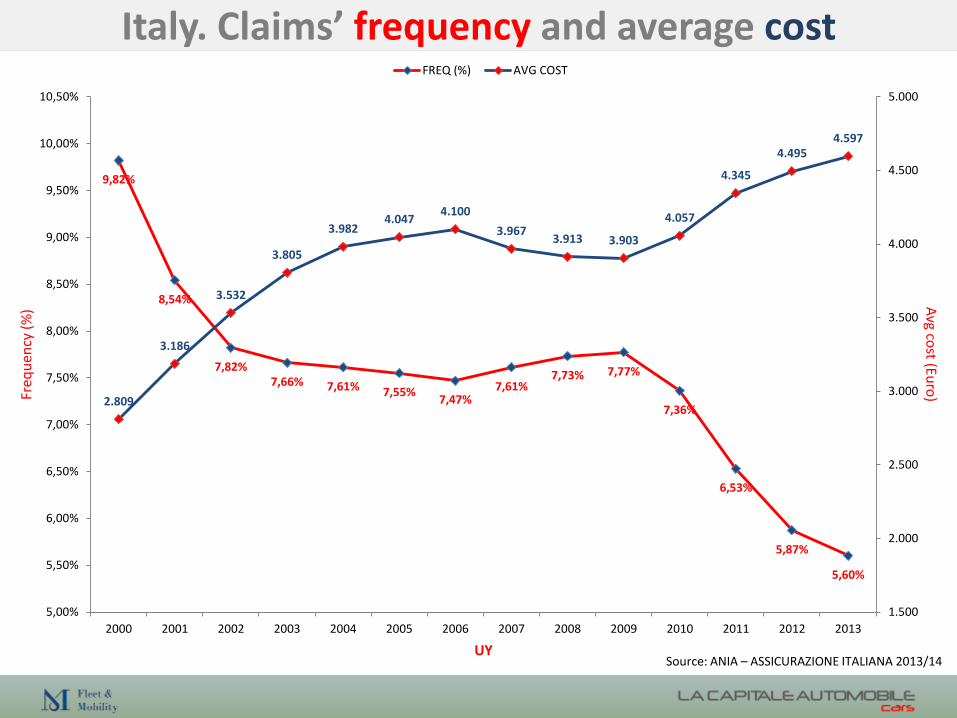

Italy. Claims’ frequency and average cost

9,82%

8,54%

7,82%7,66% 7,61% 7,55%

7,47%7,61%

7,73% 7,77%

7,36%

6,53%

5,87%

5,60%

2.809

3.186

3.532

3.805

3.9824.047

4.100

3.9673.913 3.903

4.057

4.345

4.4954.597

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

5,00%

5,50%

6,00%

6,50%

7,00%

7,50%

8,00%

8,50%

9,00%

9,50%

10,00%

10,50%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Avg co

st (Euro

)Freq

uen

cy (

%)

UY

FREQ (%) AVG COST

Source: ANIA – ASSICURAZIONE ITALIANA 2013/14

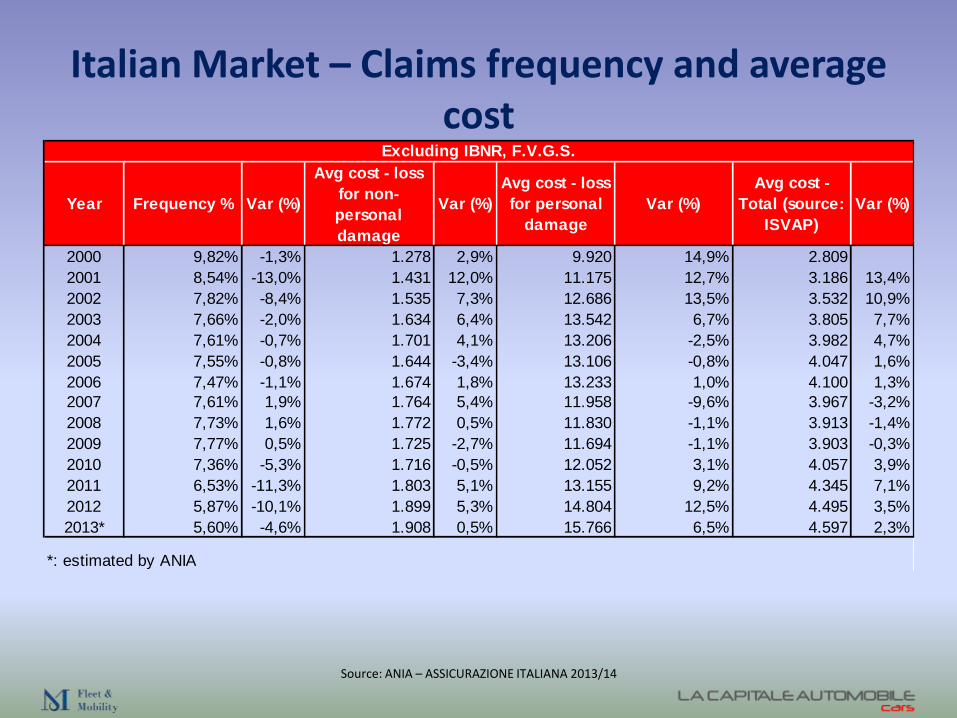

Italian Market – Claims frequency and average cost

Source: ANIA – ASSICURAZIONE ITALIANA 2013/14

Year Frequency % Var (%)

Avg cost - loss

for non-

personal

damage

Var (%)

Avg cost - loss

for personal

damage

Var (%)

Avg cost -

Total (source:

ISVAP)

Var (%)

2000 9,82% -1,3% 1.278 2,9% 9.920 14,9% 2.809

2001 8,54% -13,0% 1.431 12,0% 11.175 12,7% 3.186 13,4%

2002 7,82% -8,4% 1.535 7,3% 12.686 13,5% 3.532 10,9%

2003 7,66% -2,0% 1.634 6,4% 13.542 6,7% 3.805 7,7%

2004 7,61% -0,7% 1.701 4,1% 13.206 -2,5% 3.982 4,7%

2005 7,55% -0,8% 1.644 -3,4% 13.106 -0,8% 4.047 1,6%

2006 7,47% -1,1% 1.674 1,8% 13.233 1,0% 4.100 1,3%

2007 7,61% 1,9% 1.764 5,4% 11.958 -9,6% 3.967 -3,2%

2008 7,73% 1,6% 1.772 0,5% 11.830 -1,1% 3.913 -1,4%

2009 7,77% 0,5% 1.725 -2,7% 11.694 -1,1% 3.903 -0,3%

2010 7,36% -5,3% 1.716 -0,5% 12.052 3,1% 4.057 3,9%

2011 6,53% -11,3% 1.803 5,1% 13.155 9,2% 4.345 7,1%

2012 5,87% -10,1% 1.899 5,3% 14.804 12,5% 4.495 3,5%

2013* 5,60% -4,6% 1.908 0,5% 15.766 6,5% 4.597 2,3%

*: estimated by ANIA

Excluding IBNR, F.V.G.S.

Source: ANIA – ASSICURAZIONE ITALIANA 2013/14

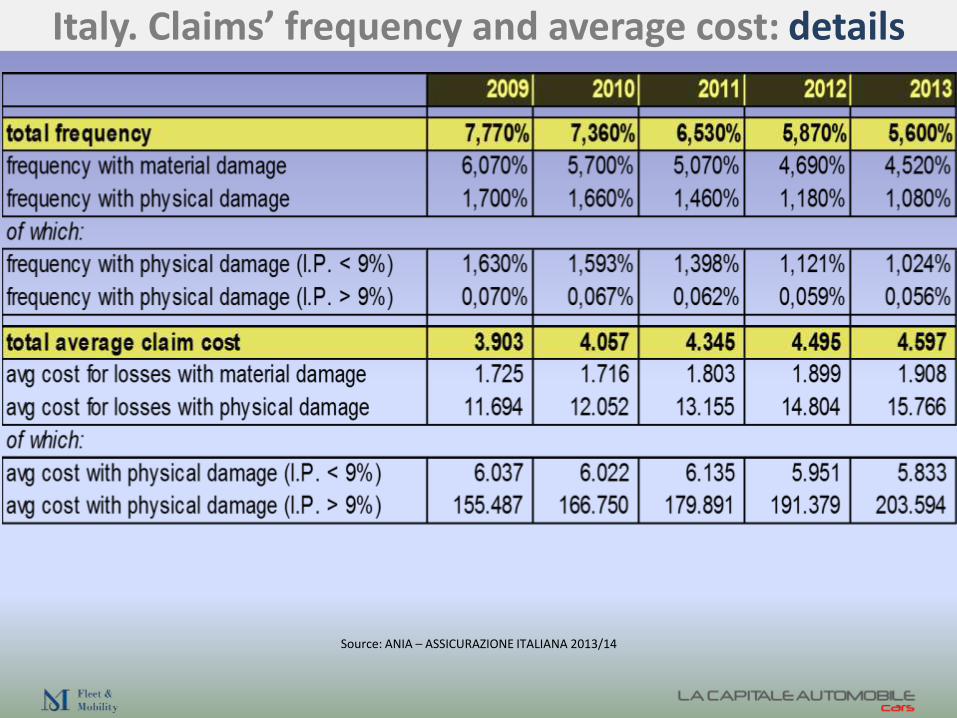

Italy. Claims’ frequency and average cost: details

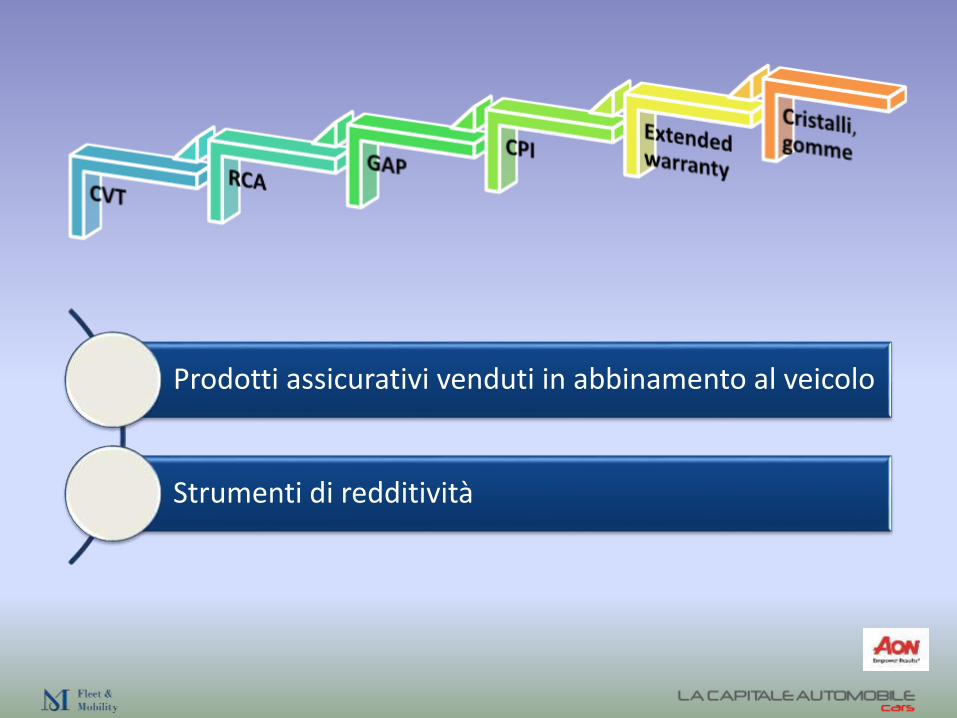

Prodotti assicurativi venduti in abbinamento al veicolo

Strumenti di redditività

Credit Protection Insurance

• Venduti insieme al veicolo

• Commissioni elevatissime

• Indagine IVASS ottobre 2013

• Netto calo delle vendite

1. Trasparenza verso il cliente. 2. Contenuti assicurativi adeguati.3. Redditività dealers.

Dealer, reti e saloni.

Ficili. Reti.

14

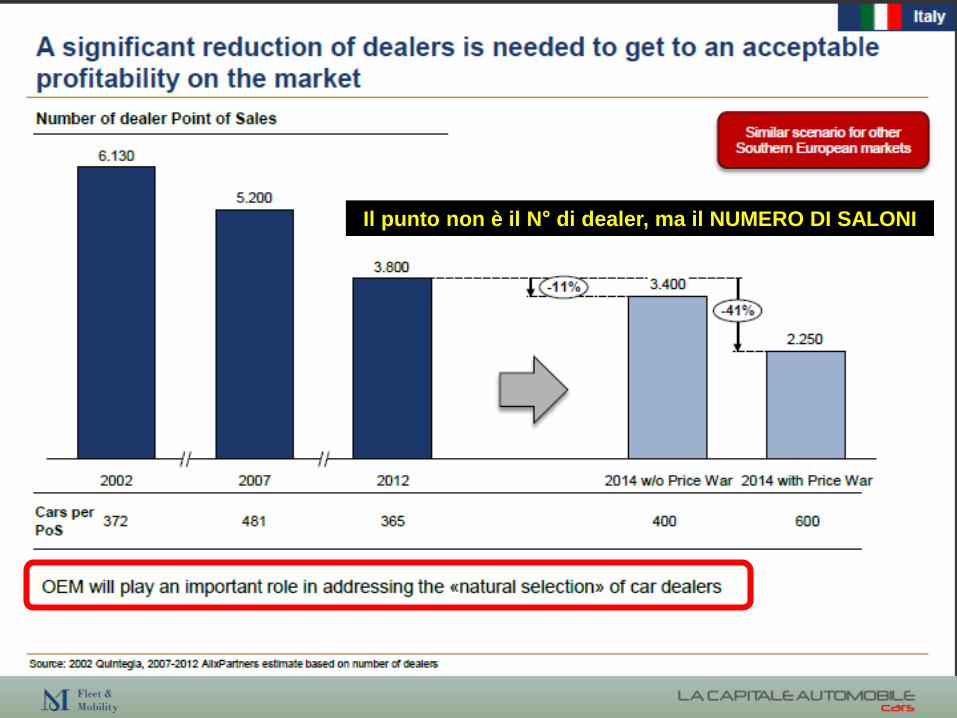

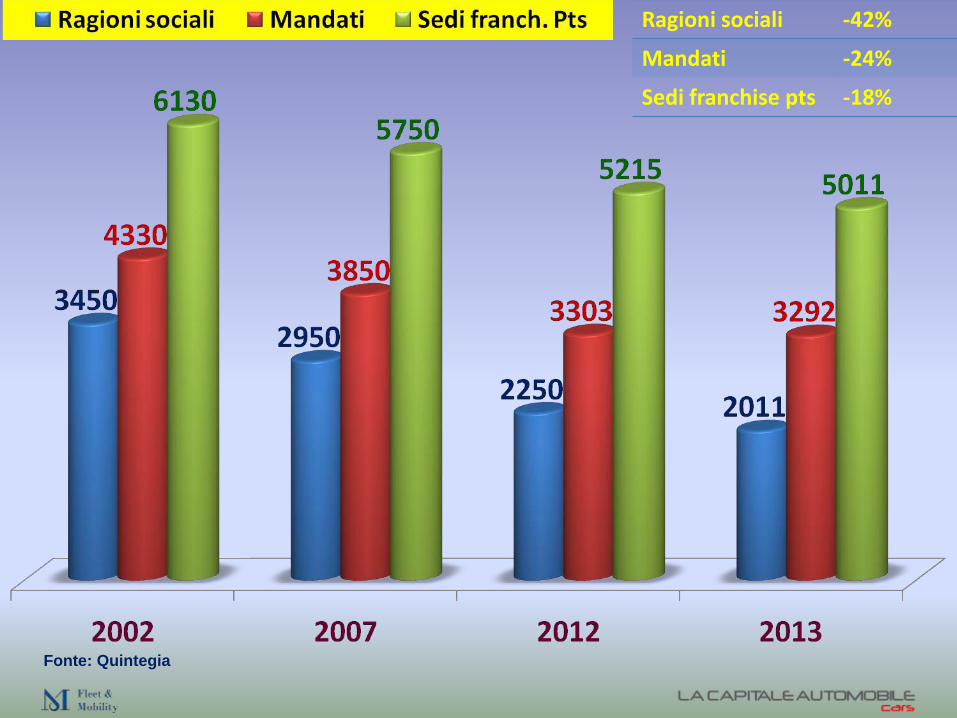

Il punto non è il N° di dealer, ma il NUMERO DI SALONI

Ragioni sociali -42%

Mandati -24%

Sedi franchise pts -18%

Fonte: Quintegia

Targhe x rag.soc. +2%

Targhe x salone -30%

Fonte: Centro Studi Fleet&Mobility – Quintegia

Meno vendite. Meno punti vendita.Sulla carta, non fa una piega.

Ma sulla strada?

Come si fa a garantire la copertura (reach) del brand su un territorio che non è rimpicciolito?

Oltre una certa distanza il cliente rinuncia.

Fiaschetti.Brand del dealer. 12

Ficili. Fuori salone.

16

Atanasio. Supporto ai dealer. 20

Atanasio. Marginare sul cliente. 21

Atanasio. La venditaè l’inizio. 22

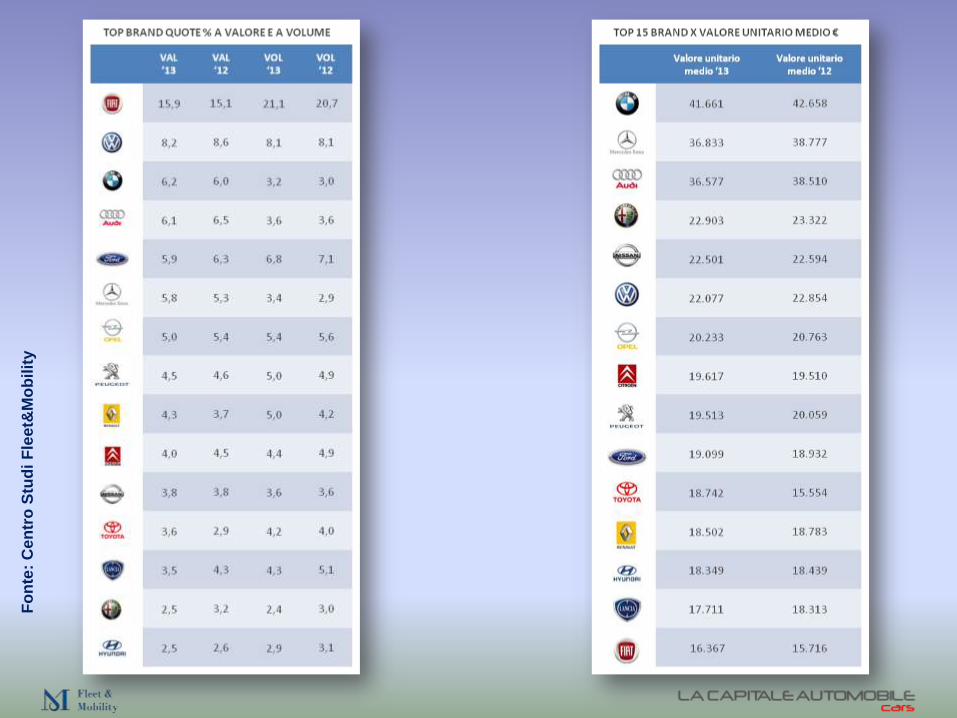

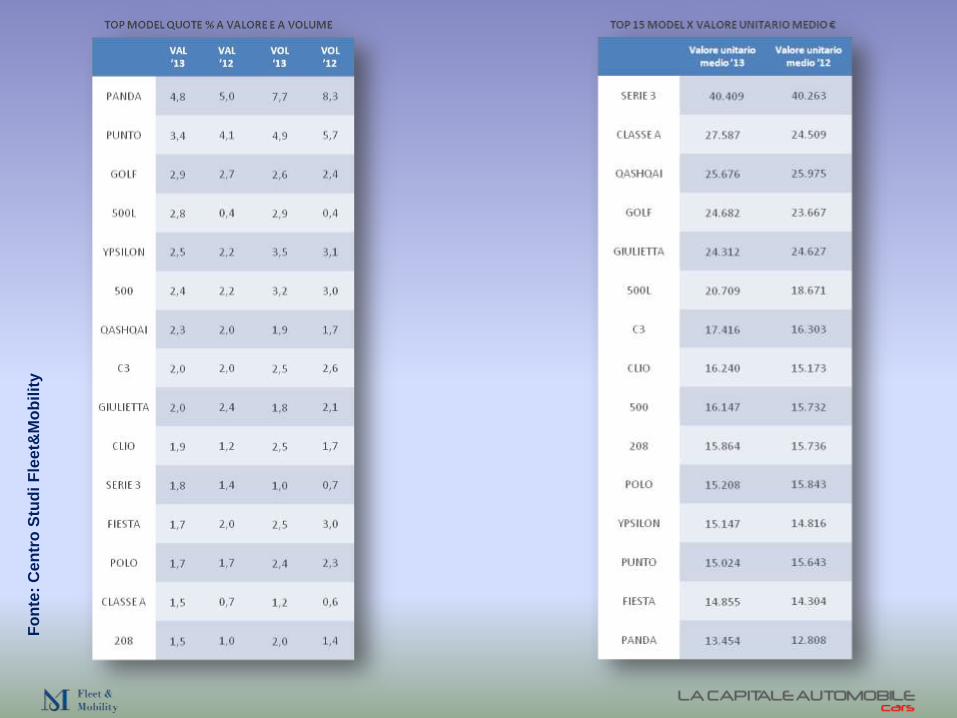

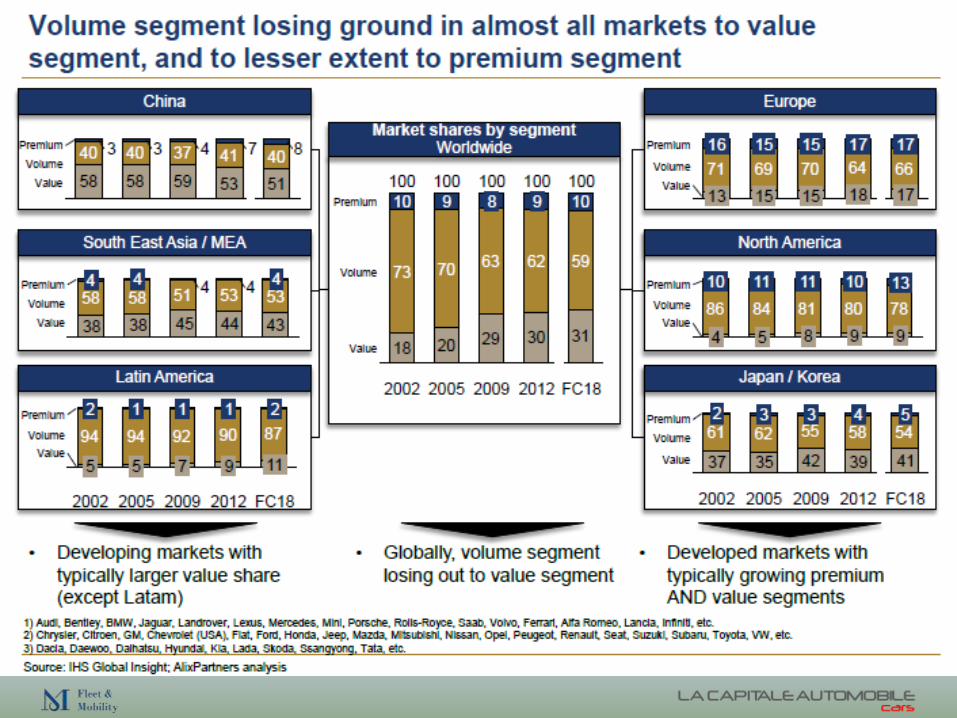

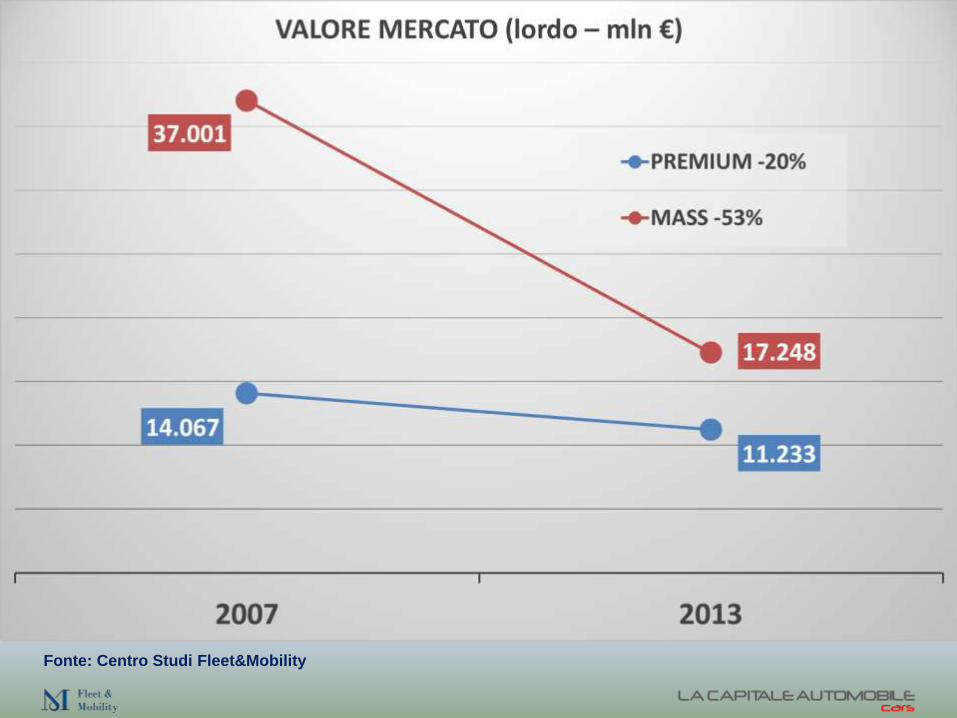

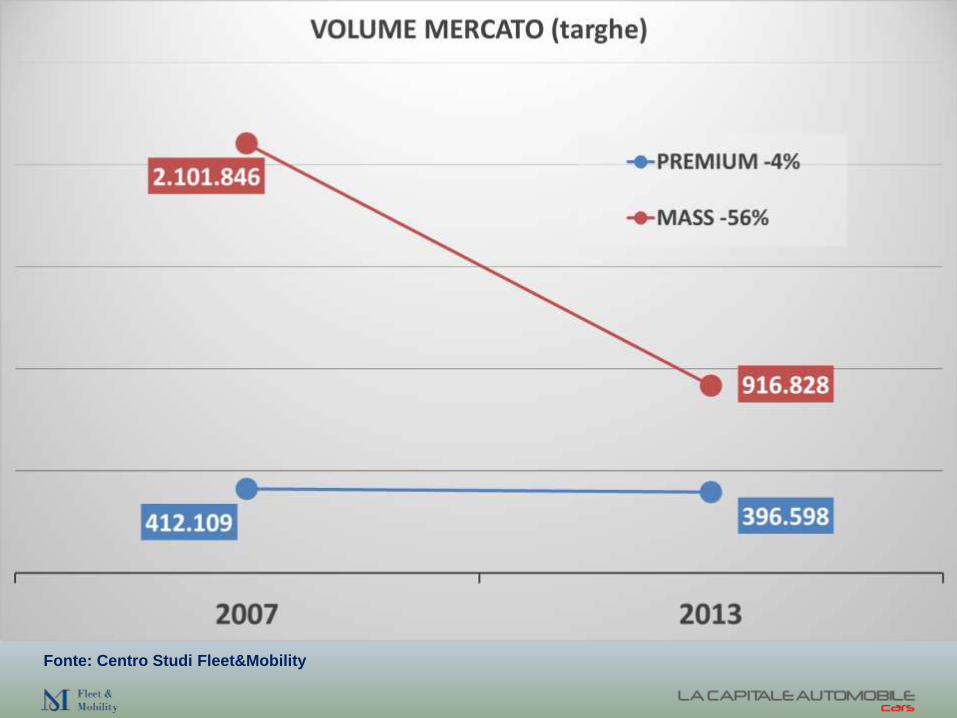

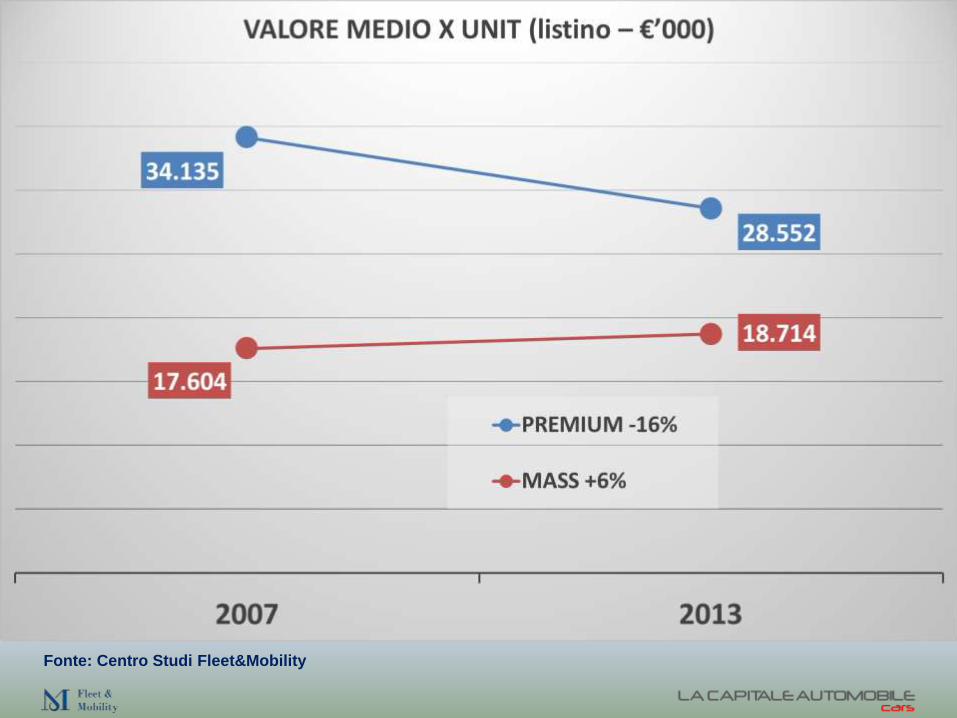

Premium e mass market

Fonte: Centro Studi Fleet&Mobility

AUTO PREMIUM: Audi, BMW, Mini, Mercedes, Smart, Lexus, Jeep, Jaguar, Land

Rover, Abarth, Aston Martin, Bentley, Cadillac, Hummer, Lamborghini, Infiniti, Lotus, Maserati, Porsche, Rolls Royce, Saab, Tesla, Volvo, Martin Motors, McLaren e Ferrari

+ Fiat 500, Opel Adam, Nissan Juke e Lancia Y.

2007 2013

Fonte: Centro Studi Fleet&Mobility

Fonte: Centro Studi Fleet&Mobility

Fonte: Centro Studi Fleet&Mobility

Fonte: Centro Studi Fleet&Mobility

Nordio.Brand premium. 3

Negli anni la strategia delle Case è stata: se hai un brand premium, puoi prenderne un altro di massa, e viceversa. Così completi

l’offerta e non li metti in concorrenza.

Ma se sono due segmenti tanto diversi, non sarebbe meglio gestire insieme premium con

premium e generalista con generalista?

Fiaschetti.Multi-brand orizzontali. 11

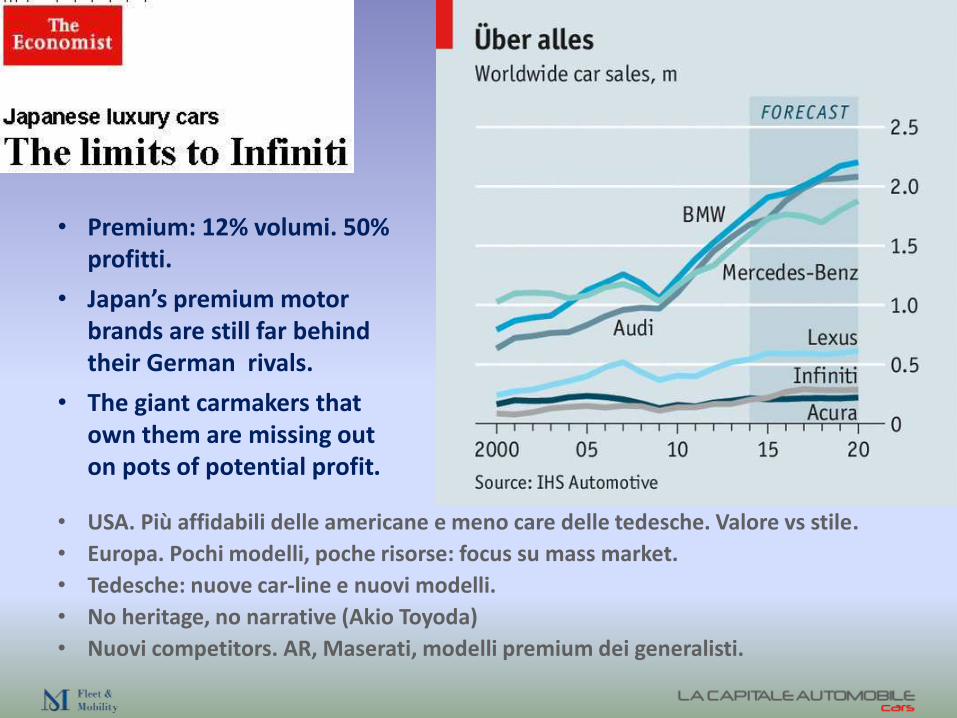

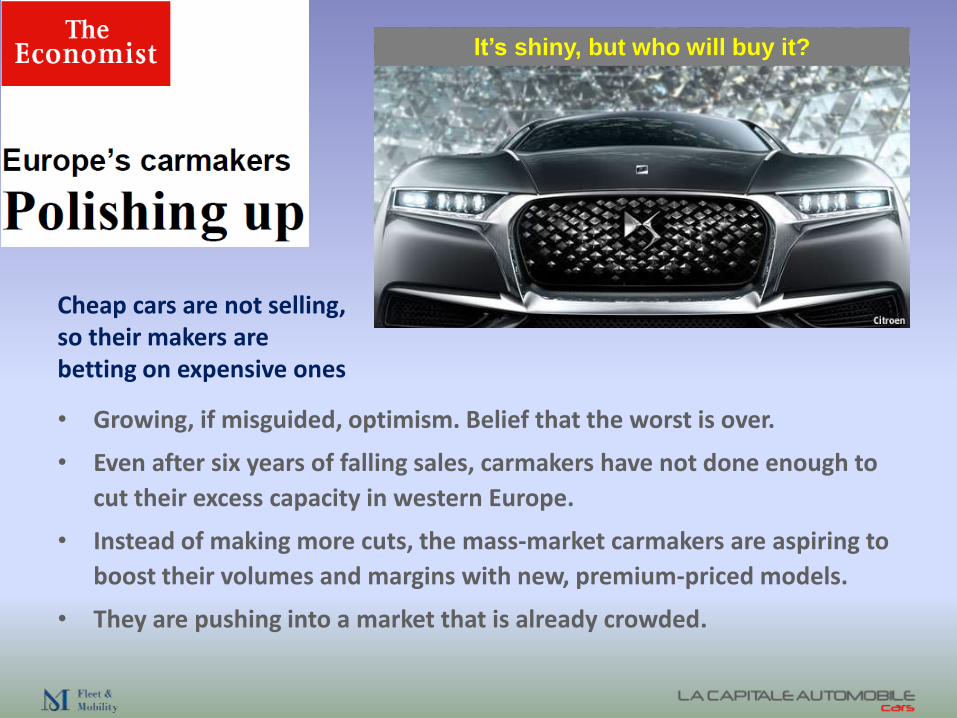

• USA. Più affidabili delle americane e meno care delle tedesche. Valore vs stile.

• Europa. Pochi modelli, poche risorse: focus su mass market.

• Tedesche: nuove car-line e nuovi modelli.

• No heritage, no narrative (Akio Toyoda)

• Nuovi competitors. AR, Maserati, modelli premium dei generalisti.

• Premium: 12% volumi. 50% profitti.

• Japan’s premium motor brands are still far behind their German rivals.

• The giant carmakers that own them are missing out on pots of potential profit.

Cheap cars are not selling, so their makers are betting on expensive ones

• Growing, if misguided, optimism. Belief that the worst is over.

• Even after six years of falling sales, carmakers have not done enough to

cut their excess capacity in western Europe.

• Instead of making more cuts, the mass-market carmakers are aspiring to

boost their volumes and margins with new, premium-priced models.

• They are pushing into a market that is already crowded.

It’s shiny, but who will buy it?

Dealer e usato

Io vorrei … non vorrei … ma se vuoi …

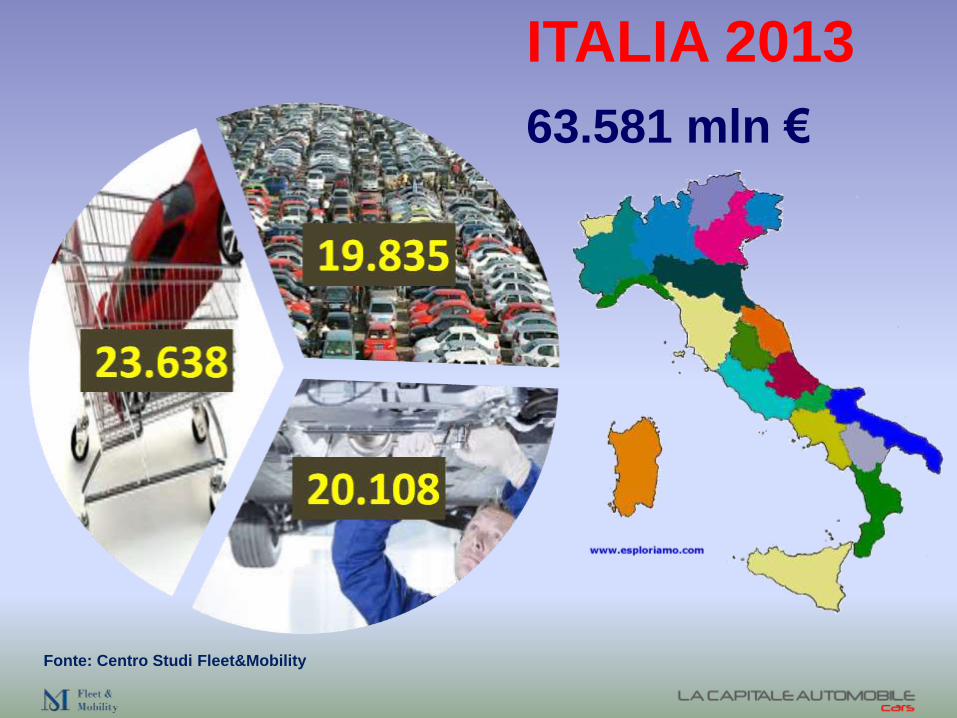

63.581 mln €

ITALIA 2013

Fonte: Centro Studi Fleet&Mobility

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

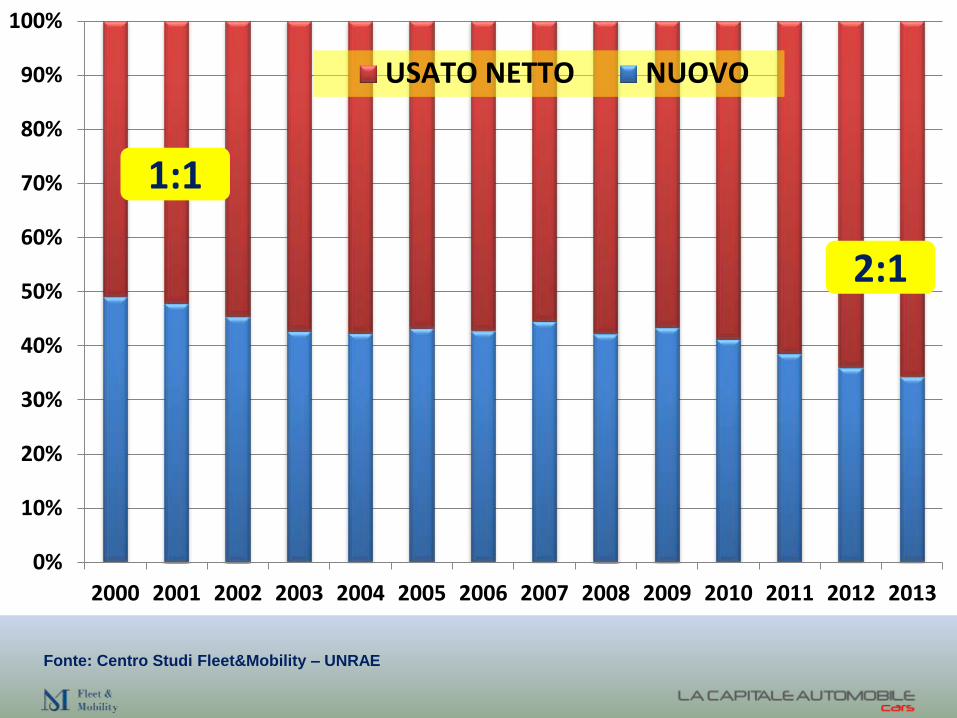

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

USATO NETTO NUOVO

2:1

1:1

Fonte: Centro Studi Fleet&Mobility – UNRAE

Fonte: Fleet&Mobility su dati ACI

Ficili.Usato.

13

Cosa è successo?

3.111.593 2.967.723 2.824.381 2.802.829 2.792.216 2.561.487 2.512.212 2.487.000

Memo: usato netto Fonte: Fleet&Mobility su dati InterAutoNews

Mercato – 20%Vendite dealer – 64%

3.111.593 2.967.723 2.824.381 2.802.829 2.792.216 2.561.487 2.512.212 2.487.000

Memo: usato netto Fonte: Fleet&Mobility su dati InterAutoNews

Secondo il mercato – 29%Fatturato reale dealer – 68%

Alcuni punti del … … Nuovo … Usato

Numero fornitori La CasaDecine/

centinaia

Concorrenti Altri dealer Commercianti

Cliente si fida di … … Casa e Dealer … il Dealer è solo

Prodotti Tutti uguali Tutti diversi

Condizioni d’acquisto Trattare una tantum Auto x auto

Vendere macchine v gestire una concessionaria

Shopping experience. Standard hard vs soft.

Ficili. Brand experience. 15

Nordio.Saloni.

6

Fiaschetti.Saloni multimediali. 10

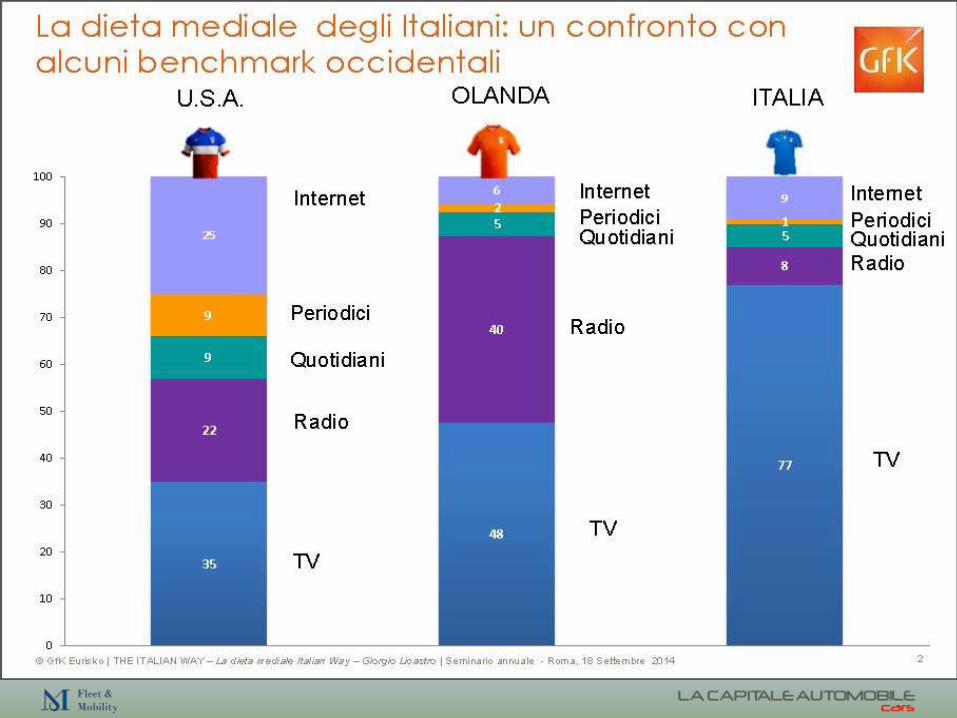

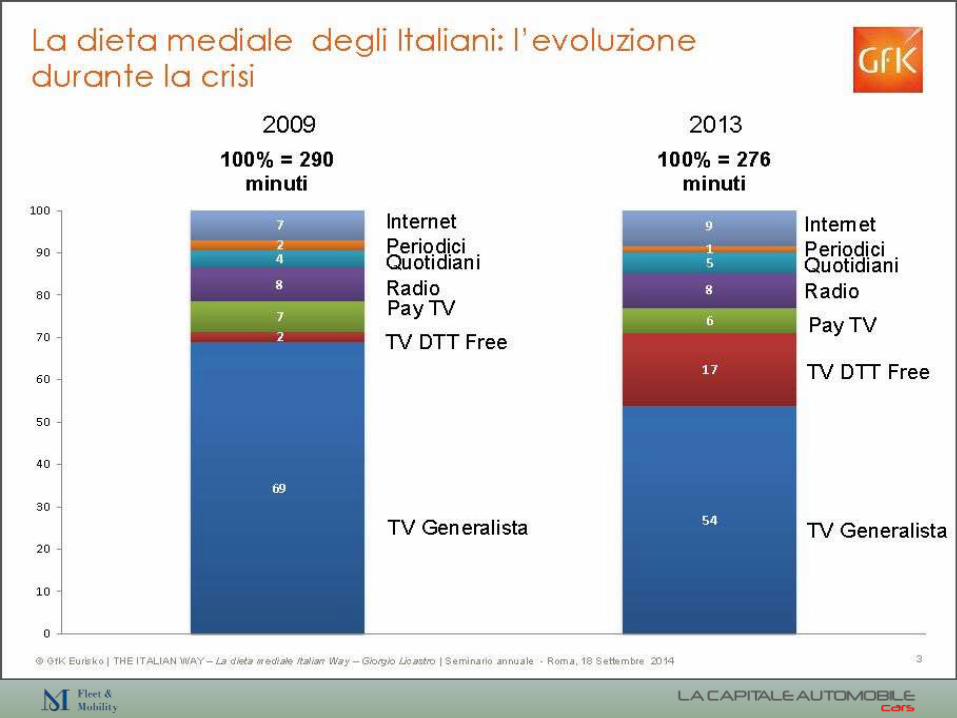

Nordio.Italiani informati. 4

Shopping experience.On/off-line.

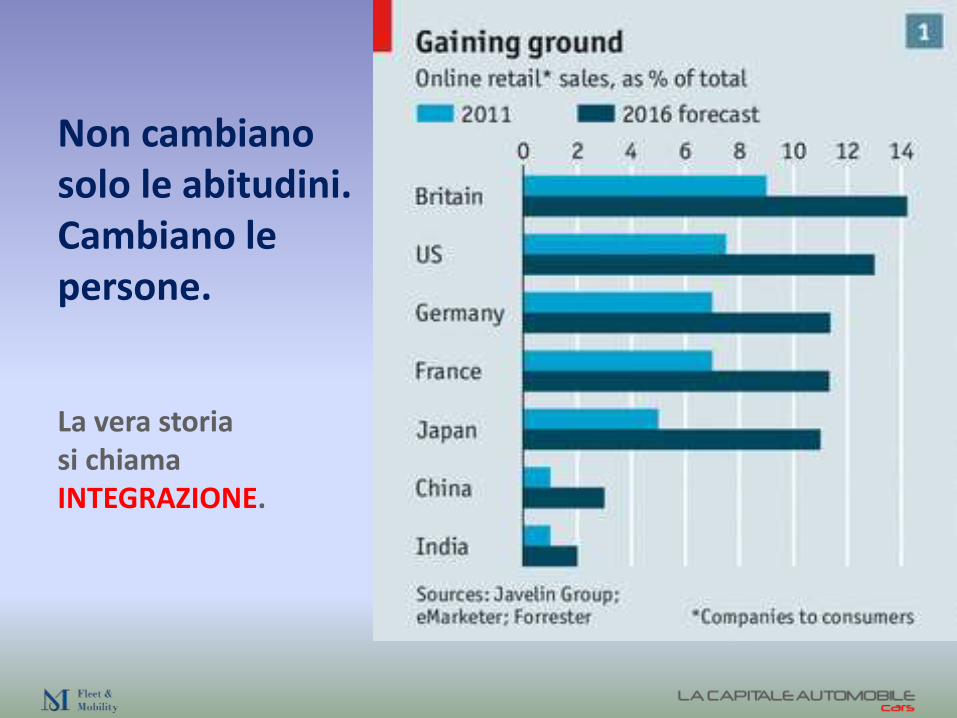

Non cambiano solo le abitudini. Cambiano le persone.

La vera storia si chiama INTEGRAZIONE.

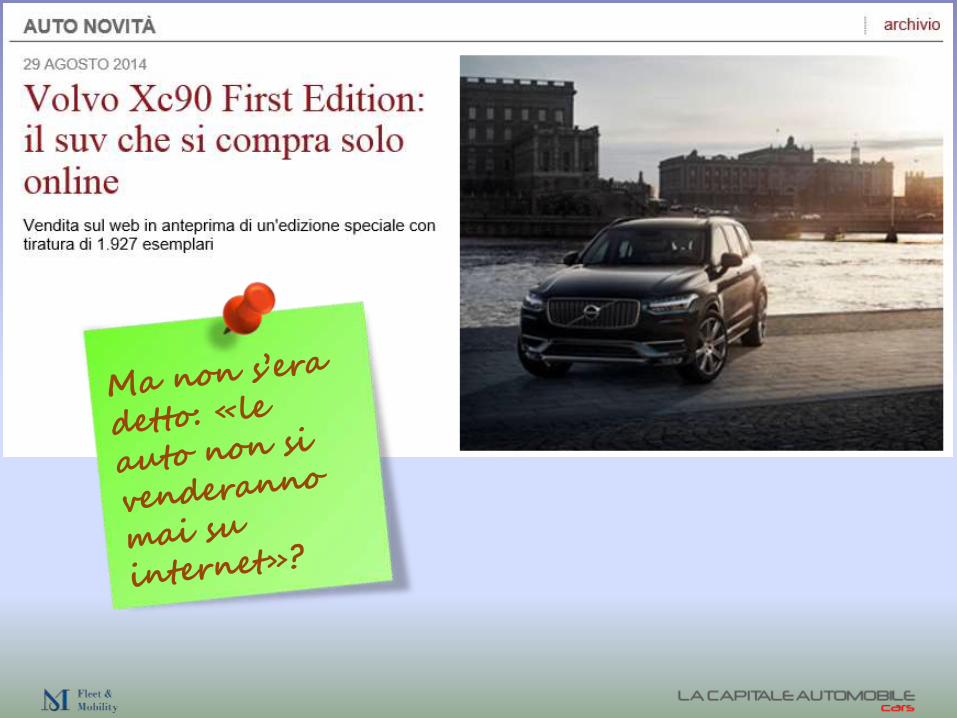

Nessuno usa internet come canale di vendita diretta. Chi è che non si fida?

• L’industria. Il pubblico, fosse per lui, le macchine su internet le comprerebbe da anni come compera biglietti aerei, libri e qualunque altro prodotto o servizio.

• Il 32% degli automobilisti europei si dice pronto a ordinare – e pagare –la sua prossima auto sul web.

• D’altra parte, che quello dell’auto sia l’unico settore merceologico privo di e-commerce, e che quel poco che c’è sia appannaggio di società private che vendono usati, è un indizio della difficoltà che ha il mondo dell’auto ad adeguarsi al nuovo.

Flavien Neuvy, resp. Osservatorio Findomestic di BNP-Paribas, 17 giugno.

InterautoNews 7/’13

Nordio.Web.

5

Ficili. Web.

17

Nordio.Pubblicità.

9

Car sharing

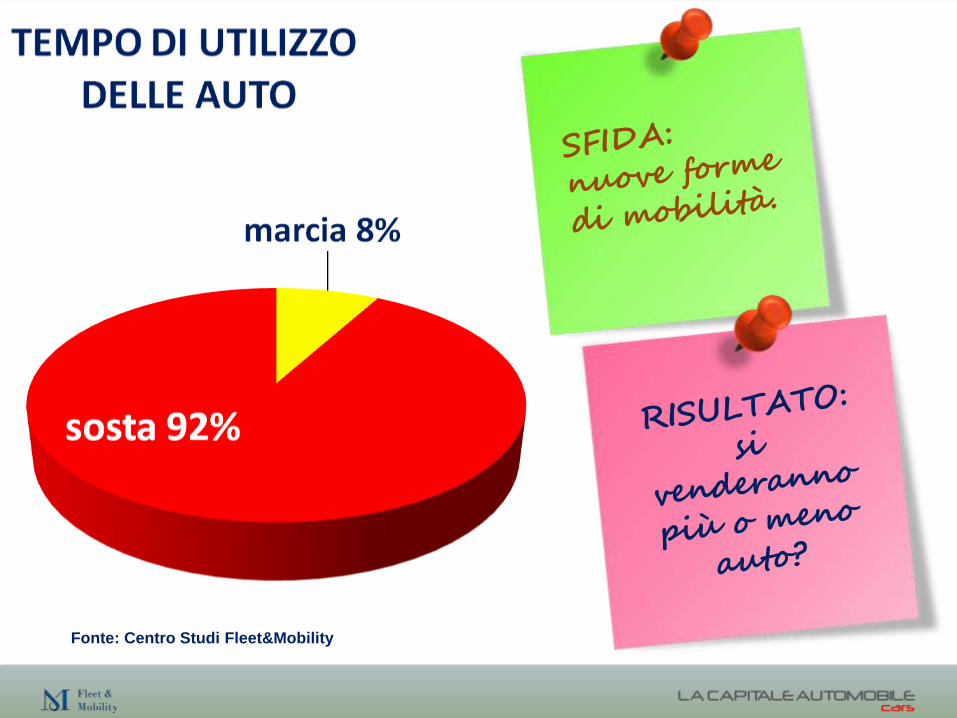

Fonte: Centro Studi Fleet&Mobility

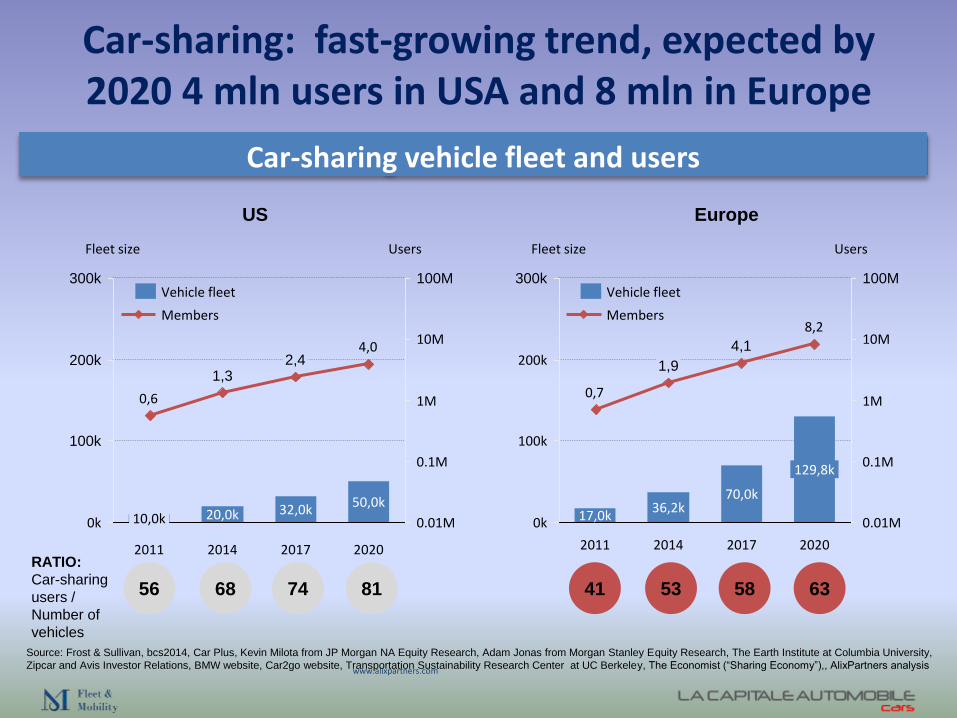

Car-sharing: fast-growing trend, expected by 2020 4 mln users in USA and 8 mln in Europe

www.alixpartners.com

Car-sharing vehicle fleet and users

56 68 74 81 53 58 6341

RATIO:

Car-sharing

users /

Number of

vehicles

0k

10M

100k

300k

200k

1M

100M

0.1M

0.01M10,0k

4,0

32,0k

2014

1,3

20,0k

2011

50,0k

20202017

2,4

0,6

UsersFleet size

Vehicle fleet

Members

0.1M

0.01M

300k 100M

1M

10M

200k

100k

0k

Fleet size Users

20202017

129,8k

70,0k

8,2

1,9

4,1

20142011

17,0k36,2k

0,7

Vehicle fleet

Members

US Europe

Source: Frost & Sullivan, bcs2014, Car Plus, Kevin Milota from JP Morgan NA Equity Research, Adam Jonas from Morgan Stanley Equity Research, The Earth Institute at Columbia University,

Zipcar and Avis Investor Relations, BMW website, Car2go website, Transportation Sustainability Research Center at UC Berkeley, The Economist (“Sharing Economy”),, AlixPartners analysis

Nordio.Car sharing.

2

23 ottobre 2014

6 febbraio 2015

5 giugno 2015