FACOLTÀ DI SCIENZE POLITICHE, ECONOMICHE E SOCIALI...

16

FACOLTÀ DI SCIENZE POLITICHE, ECONOMICHE E SOCIALI The Reforms Effects on Consumer Prices in Fixed Telecommunication Sector in the Netherlands (From 1998 until 2008) Christian Francesco Pompilio March 2015

Transcript of FACOLTÀ DI SCIENZE POLITICHE, ECONOMICHE E SOCIALI...

FACOLTÀ DI SCIENZE POLITICHE,

ECONOMICHE E SOCIALI

The Reforms Effects on Consumer Prices in Fixed Telecommunication Sector in the Netherlands

(From 1998 until 2008)

Christian Francesco Pompilio

March 2015

1. Introduction

The Netherlands is the main constituent country of the Kingdom of the Netherlands. It is made up of

Aruba, Curaçao, the Netherlands, and Sint Maarten. These countries are separated and participate on a

basis of equality as partners in the Kingdom. The countries of Aruba, Curaçao, and Sint Maarten are

dependent on the Netherlands for matters like foreign policy and defence, although they are autonomous

to a certain degree with their own parliaments. The Netherlands' name literally means "Low Country",

inspired by its low and flat geography, with only about 50% of its land exceeding one metre above sea level.

It is geographically a very low and flat country, with about 26% of its area and 21% of its population located

below sea level, and only about 50% of its land exceeding one metre above sea level. The Netherlands is a

small populated country, lying mainly in Western Europe, but also including three islands in the Caribbean.

With a population density of 406 people per km² – 497 if water is excluded – the Netherlands is a very

densely populated country for its size.

According to the European statistical office Eurostat, in 2013, the Netherlands recorded the second highest

level of Gross Domestic Product per capita in the EU-28 (€ 38.300.00), at 31 % above the EU average, with

only Luxembourg at a higher level. The Netherlands has a long history of openness to global commerce and

economic freedom, and its prosperous economy depends mostly on foreign trade. According to research

carried out by the Netherlands Bureau for Economic Policy Analysis, the Netherlands earns almost 30% of

its income from the export of goods and services, this can mainly be attributed to transit exports to other

European countries. Main exports are: machinery and transport equipment, mineral fuels, food, clothing,

footwear and pharmaceuticals. The country also imports large quantities of goods. According to Statista,

one of the world’s largest statistics portals, the Netherlands gained 589,77 billion US dollars in 2013. As far

as the quality of life is concerned, according to the OECD Better Life Index, nearly 75% of people aged 15 to

64 in the Netherlands have a paid job, above the OECD employment average of 65%; in terms of education

system, it is one of the strongest OECD countries in students’ skills. Concerning the public sphere, there is a

strong sense of community and high levels of civic participation and in general, 82% of people in the

Netherlands say they have more positive experiences on an average day than negative ones, more than the

OECD average of 76%.

In this paper, we will examine how the development of network industries (i.e. electricity, gas, water,

transport and telecommunications) played and continually play a crucial role in the Dutch society, both

from an economic and a social perspective as "they offer society the opportunity to coordinate, over time

and space, large and complex flows of essential goods"1.

We will focus our attention on the telecommunications sector in the Netherlands, and in particular on the

fixed-line telephony. This sector had a great impact on the economy of the country, above all after the

European directives, when the telecom market was opened to competition. In 2010, the

telecommunications market in the Netherlands brought in a total revenue of around € 18 billion with a

contribution of 1.5% to the Dutch GDP, according to the figures of Netherlands ICT2. More generally, 25% of

economic growth in the past 40 years is attributed to telecom industry.

1 Florio Massimo, Network Industries and Social Welfare. The experiment that Reshuffled European Utilities, Oxford University Press, 2013, p.3. 2 http://www.nederlandict.nl/Files/TER/Factsheet%20telecom%20webversie%20november%202013%20EN.pdf

We will see whether the liberalisation of the telecommunications market in the Netherlands has been

successful. We will verify how the increased competition, in combination with pro-competitive regulatory

measures has resulted in important benefits for consumers and significant price reductions.

2. Regulatory Structures and Reforms in the Telecommunications Sector:

We will take into consideration the sector of fixed telephony in the Netherlands, starting from 1998, when

the European Directives led to the removal of legal barriers to market entry and to the liberalization of the

whole telecommunications market, until 2008.

Graphic 1

These ETCR indicators take into considerations 3 variables. The first is the entry regulation, which is a

weighted average of legal conditions of entry in a market and is coded from 0 (free entry) to 6 (franchised to

one firm). The second is variable public ownership, which measures the degree of public ownership and is

coded from 0 (i.e. private ownership) to 6 (i.e. public ownership). The third is the variable market structure,

which is an indicator of the market share of new entrants and is coded from 0 to 6 (6 being the smallest

market share and 0 being the largest).

From the graphic 1, it is clear that starting from 1990, the trend has been towards a marked reduction of

public ownership, a less integrated industry structure and a less regulated access to the market.

Since 1987 the Dutch telecommunications regime has been radically transformed. In a relatively short time,

the Dutch telecom policy community was amply restructured and the rules of the game were rewritten.

Until 1990, the Royal Dutch PTT (KPN) held a monopoly on all aspects of the installation of

telecommunications networks and on the provision of all telecommunications services. Things started

changing in 1989 when the state administered telecommunications services (PTT Telecom and PPT Post)

were incorporated into KPN and the European directives started to promote liberalisation initiatives over

the network industries. The reform of telecommunications markets in Europe has essentially been driven by

the European Union policies. Since the release of the 1987 “Green Paper on the Development of the

Common Market for Telecommunications and Services”, the European Commission has played an important

role in promoting the liberalisation of the EU telecommunication market. In 1990 the EU Directives 387 and

388 opened the door to market opening for private networks and leased line; competition was allowed for

circuit and packet switched data transport services, and simple resale of leased line capacity. Four years

later, in 1994, voice telephony service in closed user groups was permitted as well. During that period, the

Dutch government progressively privatised KPN beginning in 1994 with a sale of 30 per cent of the

government’s shares and finally completed the process in 2006, giving up its golden share veto rights. In

1996, the Netherlands introduced the “interim legislation”3, which allowed competition (except for voice

telephony) for satellite networks and communications services. It also enabled the use of cable television

infrastructure for telecommunications purposes, other alternative fixed infrastructure (e.g., networks of

electricity companies and the railway company) for telecommunications purposes and the installation and

exploitation of new fixed telecommunications infrastructures. In July 1997, six months earlier than

scheduled by EU legislation, competition for voice telephony service was introduced in the Netherlands. In

1996, on the basis of the interim legislation, two new national infrastructure licences were granted, to

EnerTel (an association of regional utility companies, acquired by Worldport Communication Inc. in June

1998), and to Telfort (a joint venture of NS Telecom, which is a subsidiary of Dutch Railways and BT). It is

interesting to note that the state has a significant stake in two national telecommunication infrastructure

licensees. In addition to the direct 43.8 per cent state ownership in KPN, the state owns 100 per cent of the

Dutch Railways (a major shareholder in Telfort). Moreover, prior to 1997, KPN owned Casema, the largest

shareholder of EnerTel. This gave rise to concerns over the extent to which competition would arise

between KPN and EnerTel. To address these concerns and stimulate the development of alternate

infrastructure, in 1997 the Dutch Government required KPN to divest its ownership in Casema.

In October 1998, the interim legislation was replaced by the Act which aims at ensuring full competition in

all telecommunications activities and completing implementation with the Full Competition Directive

(1996/19/EC). The Act includes a number of new regulatory provisions and safeguards to prevent the

incumbent from leveraging its dominant market position. The Act foresees the government (including the

independent regulatory body) remaining as a key player in the market until it can be shown that the market

or specific segments of the market are sufficiently competitive to allow the government to forebear from

regulation. The Act covers practically all areas of telecommunications regulation, including registration,

spectrum frequency policy and management, numbering policy, rights of way, interconnection and special

access, open network provision (ONP), universal service, type approval of terminal equipment, protection

of personal data and privacy, and disputes and appeal processes among telecommunication service

providers.

From 1 January 1998, European Union telecommunications legislation requires the establishment of

national regulatory authorities (NRAs) in the member states of the Union. The regulatory body must be

legally distinct and functionally independent from all telecommunications organisations. A new

independent regulatory body called OPTA (Onafhankelijke post en telecommunicatie autoriteit) was

therefore established in the Netherlands in August 1997. OPTA is charged with promoting competition and

3 OECD, "Regulatory Reform in the Netherlands. Regulatory Reform in the Telecommunications Industry", 1999, p. 7.

the interests of consumers, and with regulating the telecommunications and postal sectors. OPTA’s

responsibilities include dispute settlement, approving interconnection and retail tariffs, and supervising the

postal concession. However, its power is limited since it cannot take action on its own initiative and has to

wait for an official complaint from market participants4.

Others important Directives which were adopted during the 2000s were Directives 2002/22 EC and

2002/27/EC which “further extended consumer protection and abolished some exclusive rights”. In that

regard, OPTA has taken significant action in order to ensure competitive access to KPN’s local loop in terms

of regulation of prices, cost orientation, monthly tariffs and connection charges. Moreover,

telecommunication operators are no longer required to obtain a license to operate and only have to

register.

In 2002, the 1998 framework was reviewed in the light of convergence of telecommunications, the

Internet, and broadcasting. With the 2002 “Second Telecoms Package”, which came into effect in 2003, the

regulators in the member states of the EU have to define the relevant markets while taking into account

national circumstances. To do so, they carry out market analyses and assess whether effective competition

exists in these markets. In case there is insufficient competition in a certain market, the national regulator

has to draft regulatory measures and submit them for approval to the Commission. The 2009 "Third

Telecoms Package" amended the 2002 one towards enhanced regulatory coordination at the EU level,

aimed to further harmonise national regulations under stronger competition principles with respect to the

previous rules. In fact, a Body of European Regulators for Electronic Communications (BEREC) was created,

and NRAs' competences were broadened by including functional separation (i.e. separation of wholesale

and retail lines of business management under a same ownership in case of enduring access problems to

the incumbent operators' network) among possible remedies to ensure better competition in the relevant

markets, reduced to 7 in December 2007 due to advances in competition. It is worth noting that, before

adopting remedies, NRAs must submit them to the Commission under the so-called Article 7 procedure,

and take into utmost account subsequent remarks5.

It is important to note that KPN has been privatised with the fixed network included. Since 2000, a

discussion has taken place about whether privatising KPN as an integrated company. The crucial question

was if privatising KPN as an integrated company may have delayed competition in some market segments.

KPN, the former monopolist, was exposed to competition and new regulations, and transformed itself into

a commercial enterprise because it was obliged to unbundle the local loop. Newcomers, who did not have

their own networks, was initially allowed to use regulated access to KPN‘s existing infrastructure. Clearly,

the fact that KPN was and continues to be both service provider and network owner gave an incentive to

raise rivals’ costs and this created difficulties for the regulator, OPTA. Since several key terms in the law and

powers of OPTA have been unclear, there have been many legal disputes in this area. Nevertheless, OPTA

has taken a tough stance imposing several measures as price squeeze tests on KPN, that forced the

company to leave some margin between its retail and wholesale tariffs and that allowed CPS-operators

(carrier select) to compete; access obligations and tariff regulation (partly by safety caps based on the 2011

tariff levels).

4 Cfr, OECD, "Regulatory Reform in the Netherlands. Regulatory Reform in the Telecommunications Industry", 1999, pp. 7-13 5 Cfr, Occasional Papers 12, Market Functioning in Network Industries - Electronic Communications, Energy and Transport, 2013, pp. 83-90

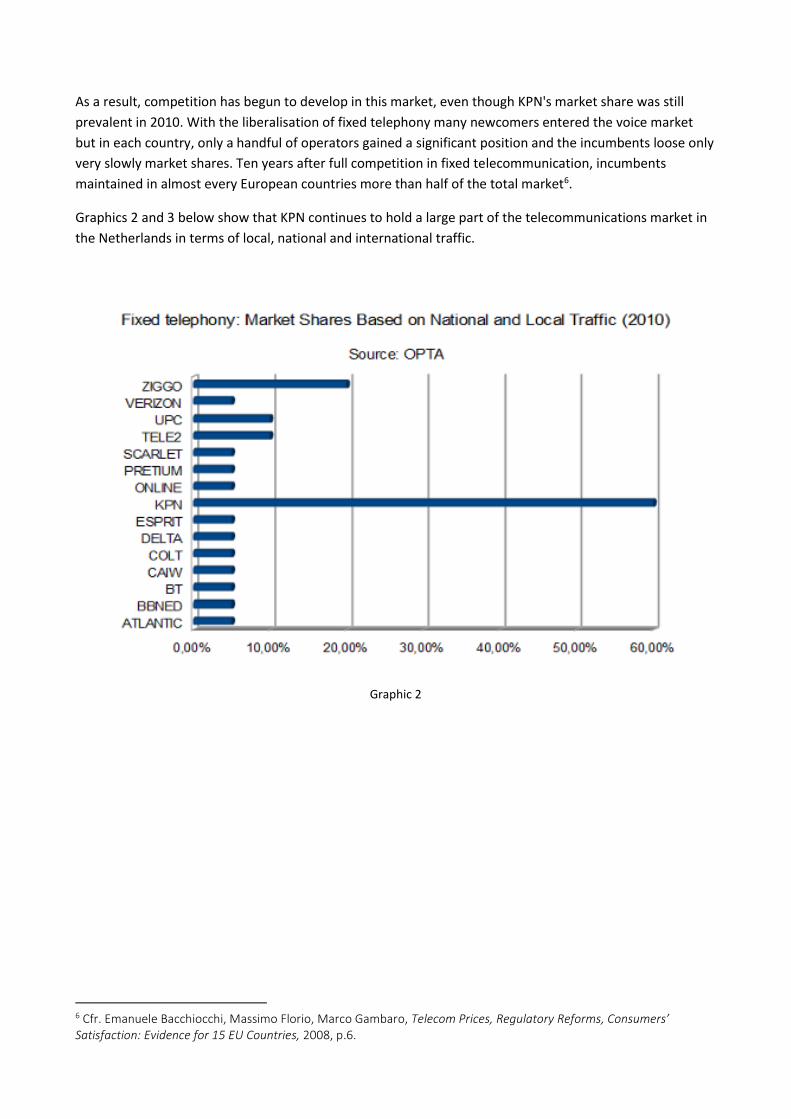

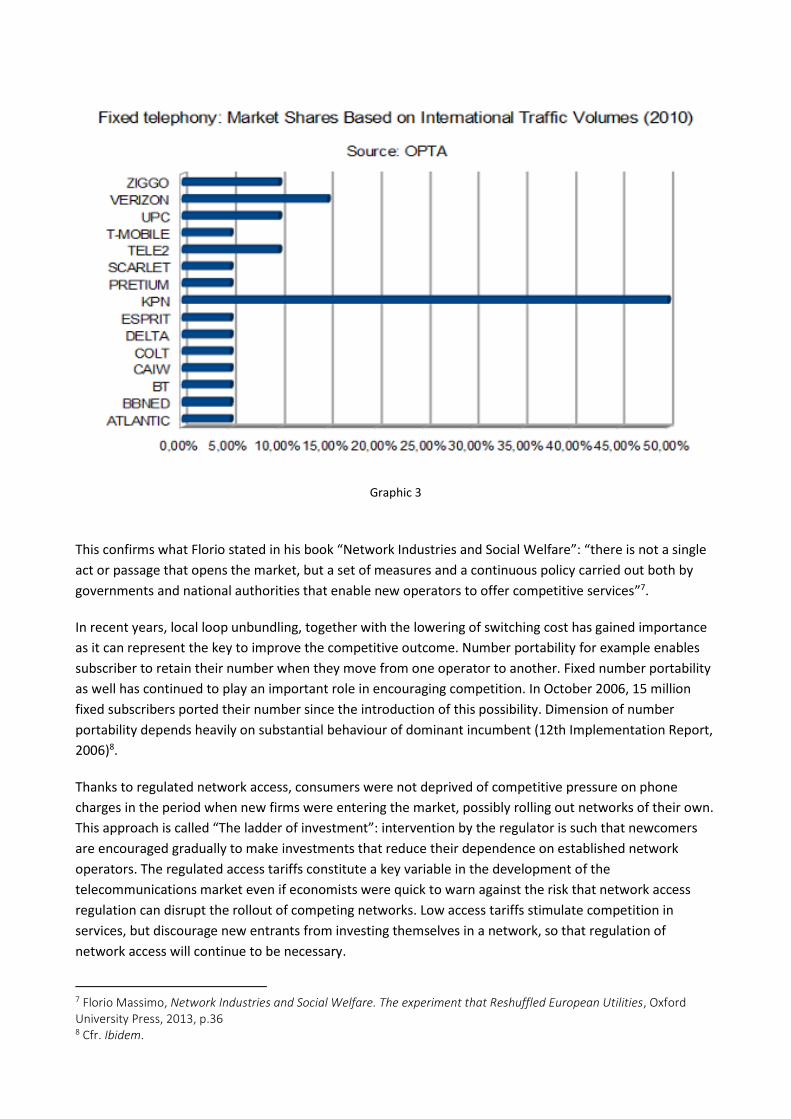

As a result, competition has begun to develop in this market, even though KPN's market share was still

prevalent in 2010. With the liberalisation of fixed telephony many newcomers entered the voice market

but in each country, only a handful of operators gained a significant position and the incumbents loose only

very slowly market shares. Ten years after full competition in fixed telecommunication, incumbents

maintained in almost every European countries more than half of the total market6.

Graphics 2 and 3 below show that KPN continues to hold a large part of the telecommunications market in

the Netherlands in terms of local, national and international traffic.

Graphic 2

6 Cfr. Emanuele Bacchiocchi, Massimo Florio, Marco Gambaro, Telecom Prices, Regulatory Reforms, Consumers’ Satisfaction: Evidence for 15 EU Countries, 2008, p.6.

Graphic 3

This confirms what Florio stated in his book “Network Industries and Social Welfare”: “there is not a single

act or passage that opens the market, but a set of measures and a continuous policy carried out both by

governments and national authorities that enable new operators to offer competitive services”7.

In recent years, local loop unbundling, together with the lowering of switching cost has gained importance

as it can represent the key to improve the competitive outcome. Number portability for example enables

subscriber to retain their number when they move from one operator to another. Fixed number portability

as well has continued to play an important role in encouraging competition. In October 2006, 15 million

fixed subscribers ported their number since the introduction of this possibility. Dimension of number

portability depends heavily on substantial behaviour of dominant incumbent (12th Implementation Report,

2006)8.

Thanks to regulated network access, consumers were not deprived of competitive pressure on phone

charges in the period when new firms were entering the market, possibly rolling out networks of their own.

This approach is called “The ladder of investment”: intervention by the regulator is such that newcomers

are encouraged gradually to make investments that reduce their dependence on established network

operators. The regulated access tariffs constitute a key variable in the development of the

telecommunications market even if economists were quick to warn against the risk that network access

regulation can disrupt the rollout of competing networks. Low access tariffs stimulate competition in

services, but discourage new entrants from investing themselves in a network, so that regulation of

network access will continue to be necessary.

7 Florio Massimo, Network Industries and Social Welfare. The experiment that Reshuffled European Utilities, Oxford University Press, 2013, p.36 8 Cfr. Ibidem.

3. Price Trend

In this section, we will have a look at the development of the prices of fixed telephone calls actually paid by

the consumers. We will take 1998, a largely pre-reform year, as the starting point and 2008 as the final

year.

The goal of First Telecoms Package, issued in 1998, was to foster sustainable competitive conditions in the

national markets by means of heavy regulation, such as access through the "open network provisions", and

National Regulatory Authority's (NRA) remedies to be imposed in case of incumbent operators' significant

market power, defined as the ability to act independently of competitors, customers, and consumers.

These direct intervention powers by the national regulators in implementing the EU Framework within

insufficiently competitive markets, namely protecting entrants and final users against dominant operators

through adequate regulatory obligations9.

The data are presented with the following parameters:

Taken from Teligen, 2010

Using EURO exchange rates

VAT excluded

Call charges refer to calls within the operator’s own network

Incumbent's Call Price (KPN) 1998-2008

10 Minute Call *3 km 10 Minute Call *200 km 10 Minute Call to USA

1998 2008 1998 2008 1998 2008

€ 0,26 € 0,37 €0,58 € 0,37 € 2,29 € 0,57

* at weekdays 11:00

Note: all prices are in current Euro excluding VAT

Source: Teligen 2010

9 Cfr. Occasional Papers 12, Market Functioning in Network Industries - Electronic Communications, Energy and

Transport, 2013, p.17.

Competitor's Call Price (Tele2) 2002 - 2008

10 Minute Call *3 km 10 Minute Call *200 km 10 Minute Call to USA

2002 2008 2002 2008 2003 2008

€ 0,24 € 0,24 € 0,36 € 0,33 € 0,45 € 0,37

* at weekdays 11:00

Note: all prices are in current Euro excluding VAT

Source: Teligen 2010

Call price comparison between the incumbent KPN and the first competitor Tele2

Graphic 4

Prices are in current Euro, excluding VAT

Source: Teligen 2010

€0,00

€0,05

€0,10

€0,15

€0,20

€0,25

€0,30

€0,35

€0,40

2002 2003 2004 2005 2006 2007 2008

10 Minute Call Charges for a 3km Call at Weekdays h: 11:00

KPN Tele 2

Graphic 5

Prices are in current Euro, excluding VAT

Source: Teligen 2010

Graphic 6

Prices are in current Euro, excluding VAT

Call duration is 10 minutes, and any call setup is included

Source: Teligen 2010

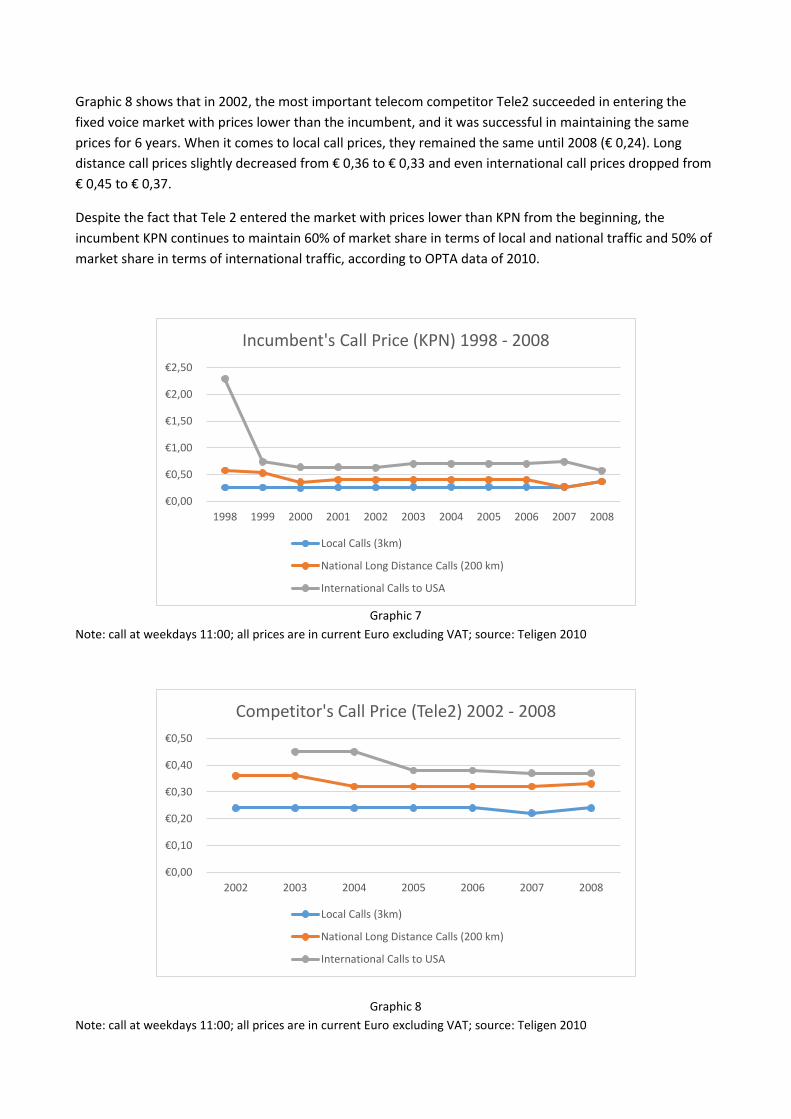

As graphic 7 shows, KPN in the relatively short time span of 10 years lowered dramatically international call

prices from € 2,29 to € 0,57. Long distance call prices decreased as well from € 0,58 to € 0,37. On the

contrary, local call prices increased from € 0,26 to € 0,37.

€0,00

€0,05

€0,10

€0,15

€0,20

€0,25

€0,30

€0,35

€0,40

€0,45

2002 2003 2004 2005 2006 2007 2008

10 Minute Call Charges for a 200 km Call at Weekdays h: 11:00

KPN Tele 2

€0,00

€0,10

€0,20

€0,30

€0,40

€0,50

€0,60

€0,70

€0,80

2003 2004 2005 2006 2007 2008

10 Minute International Call Charges (to USA)

KPN Tele 2

Graphic 8 shows that in 2002, the most important telecom competitor Tele2 succeeded in entering the

fixed voice market with prices lower than the incumbent, and it was successful in maintaining the same

prices for 6 years. When it comes to local call prices, they remained the same until 2008 (€ 0,24). Long

distance call prices slightly decreased from € 0,36 to € 0,33 and even international call prices dropped from

€ 0,45 to € 0,37.

Despite the fact that Tele 2 entered the market with prices lower than KPN from the beginning, the

incumbent KPN continues to maintain 60% of market share in terms of local and national traffic and 50% of

market share in terms of international traffic, according to OPTA data of 2010.

Graphic 7

Note: call at weekdays 11:00; all prices are in current Euro excluding VAT; source: Teligen 2010

Graphic 8 Note: call at weekdays 11:00; all prices are in current Euro excluding VAT; source: Teligen 2010

€0,00

€0,50

€1,00

€1,50

€2,00

€2,50

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Incumbent's Call Price (KPN) 1998 - 2008

Local Calls (3km)

National Long Distance Calls (200 km)

International Calls to USA

€0,00

€0,10

€0,20

€0,30

€0,40

€0,50

2002 2003 2004 2005 2006 2007 2008

Competitor's Call Price (Tele2) 2002 - 2008

Local Calls (3km)

National Long Distance Calls (200 km)

International Calls to USA

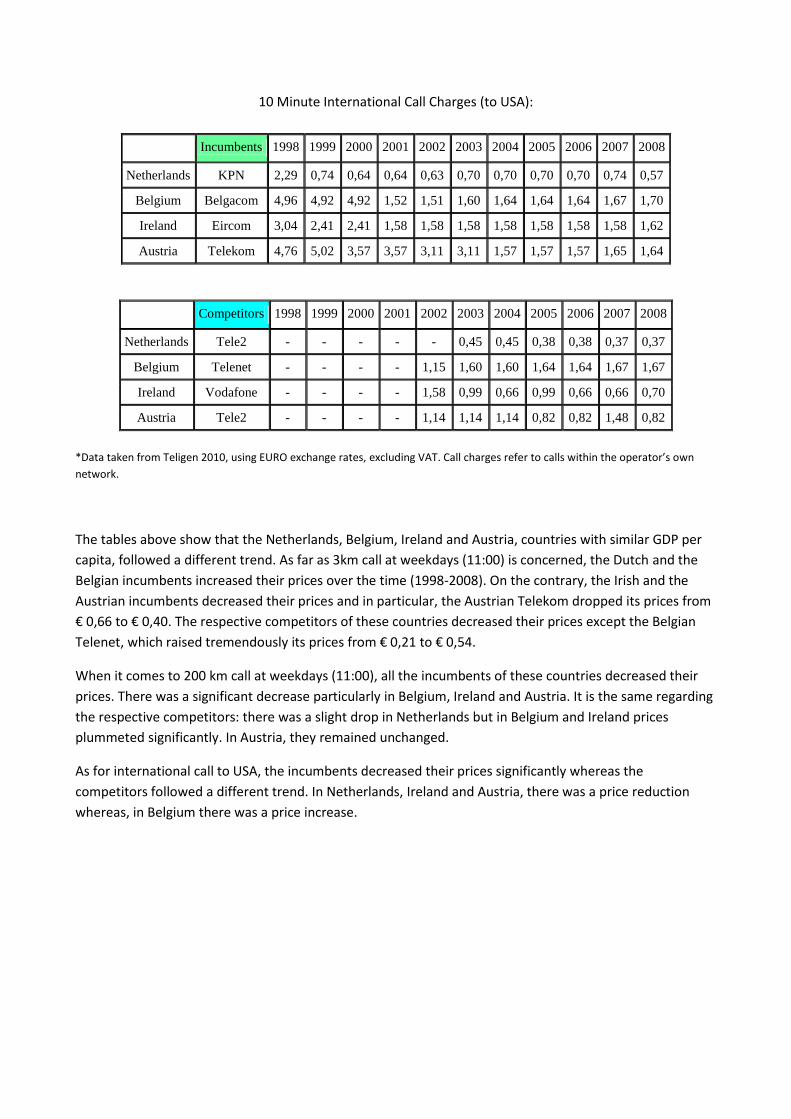

Call price comparison with countries having similar GDP per capita

10 Minute Call Charges for a 3km Call at Weekdays h: 11:00

Incumbents 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Netherlands KPN 0,26 0,26 0,25 0,26 0,26 0,27 0,27 0,27 0,27 0,27 0,37

Belgium Belgacom 0,41 0,41 0,41 0,45 0,45 0,46 0,47 0,47 0,47 0,48 0,50

Ireland Eircom 0,48 0,40 0,42 0,42 0,42 0,42 0,40 0,40 0,40 0,43 0,43

Austria Telekom 0,66 0,66 0,57 0,57 0,46 0,46 0,40 0,40 0,40 0,40 0,40

Competitors 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Netherlands Tele2 - - - - 0,24 0,24 0,24 0,24 0,24 0,22 0,24

Belgium Telenet - - - - 0,21 0,21 0,38 0,47 0,47 0,48 0,54

Ireland Vodafone - - - - 0,45 0,40 0,31 0,31 0,31 0,31 0,31

Austria Tele2 - - - - 0,46 0,46 0,45 0,40 0,40 0,38 0,38

10 Minute Call Charges for a 200 km Call at Weekdays h: 11:00

Incumbents 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Netherlands KPN 0,58 0,53 0,36 0,40 0,40 0,40 0,40 0,40 0,40 0,27 0,37

Belgium Belgacom 1,43 1,43 1,43 0,45 0,45 0,46 0,47 0,47 0,47 0,48 0,50

Ireland Eircom 1,69 1,05 0,78 0,78 0,78 0,68 0,68 0,68 0,68 0,71 0,71

Austria Telekom 1,90 1,90 1,90 0,64 0,55 0,55 0,49 0,49 0,49 0,49 0,49

Competitors 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Netherlands Tele2 - - - - 0,36 0,36 0,32 0,32 0,32 0,32 0,33

Belgium Telenet - - - - 0,21 0,21 0,38 0,47 0,47 0,48 0,54

Ireland Vodafone - - - - 0,70 0,40 0,31 0,31 0,31 0,31 0,31

Austria Tele2 - - - - 0,46 0,46 0,45 0,40 0,40 0,46 0,46

10 Minute International Call Charges (to USA):

Incumbents 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Netherlands KPN 2,29 0,74 0,64 0,64 0,63 0,70 0,70 0,70 0,70 0,74 0,57

Belgium Belgacom 4,96 4,92 4,92 1,52 1,51 1,60 1,64 1,64 1,64 1,67 1,70

Ireland Eircom 3,04 2,41 2,41 1,58 1,58 1,58 1,58 1,58 1,58 1,58 1,62

Austria Telekom 4,76 5,02 3,57 3,57 3,11 3,11 1,57 1,57 1,57 1,65 1,64

Competitors 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Netherlands Tele2 - - - - - 0,45 0,45 0,38 0,38 0,37 0,37

Belgium Telenet - - - - 1,15 1,60 1,60 1,64 1,64 1,67 1,67

Ireland Vodafone - - - - 1,58 0,99 0,66 0,99 0,66 0,66 0,70

Austria Tele2 - - - - 1,14 1,14 1,14 0,82 0,82 1,48 0,82

*Data taken from Teligen 2010, using EURO exchange rates, excluding VAT. Call charges refer to calls within the operator’s own

network.

The tables above show that the Netherlands, Belgium, Ireland and Austria, countries with similar GDP per

capita, followed a different trend. As far as 3km call at weekdays (11:00) is concerned, the Dutch and the

Belgian incumbents increased their prices over the time (1998-2008). On the contrary, the Irish and the

Austrian incumbents decreased their prices and in particular, the Austrian Telekom dropped its prices from

€ 0,66 to € 0,40. The respective competitors of these countries decreased their prices except the Belgian

Telenet, which raised tremendously its prices from € 0,21 to € 0,54.

When it comes to 200 km call at weekdays (11:00), all the incumbents of these countries decreased their

prices. There was a significant decrease particularly in Belgium, Ireland and Austria. It is the same regarding

the respective competitors: there was a slight drop in Netherlands but in Belgium and Ireland prices

plummeted significantly. In Austria, they remained unchanged.

As for international call to USA, the incumbents decreased their prices significantly whereas the

competitors followed a different trend. In Netherlands, Ireland and Austria, there was a price reduction

whereas, in Belgium there was a price increase.

4. Consumer Satisfaction

According to “Consumer Satisfaction Survey10” carried out by Ipsos Inra in 2006, the percentage of satisfied

customers with their fixed telephone supplier in the Netherlands is 39.7 and the percentage of dissatisfied

customers is 3.3.

Source: IPSOS INRA, Consumer Satisfaction Survey, 2007

This survey shows that 47% of citizens in the Netherlands think that their fixed telephone provider offers a

quality service overall. In terms of competition, more than 85% of Dutch consumers believe that it is

possible to get what they want from any fixed telephone supplier without a reduction in quality.

The survey also demonstrates that most of the 15 UE consumers (85%) think that fixed telephone services

are available for everybody in their country. In the Netherlands this is true for more than 90% of users.

When we deal with prices, their level for fixed telephone services is one of the main sources of

dissatisfaction for fifteen European Union consumers. As it is stated in the survey, in the last few years,

several factors among which liberalisation of the telecoms industry and competition between information

technologies (e.g. Voice over Internet Protocol) have put the spotlight on the different tariffs charged by

different operators in different countries. These factors make fixed telephony a basic service that

consumers are not ready to pay much for any more.

Moreover, in many countries, the penetration of mobile telephony has recently become higher than that of

fixed telephony. This explains why, in spite of considerable price reductions since 2000, “ the pricing of

fixed phone services is still a point of dissatisfaction for EU consumers. Commercial offers from fixed

telephone operators (the lack of special prices for specific target groups or specific usage) are also a source

of dissatisfaction for consumers”.

10 Ipsos Inra, Consumer Satisfaction Survey, 2007. pp. 60-67

5. Conclusion

The Dutch citizens did not benefit extremely from privatisation and liberalisation of the fixed telephony

sector in the Netherlands. The Netherlands has made steady progress in telecommunications market

liberalisation in the 1990s in conformance with the EU Directives, and it has always been one of the leading

performers in terms of implementing the principles of the EU Directives11. However, reforms in the fixed

telephony sector impacted the market creating better and worse effects. Obviously, they are changing the

telecommunication market but the mission cannot be declared a success yet. Some paradoxical questions

still remain.

As far as competition in concerned, it seems that the reforms worked enough as, from 2002, competition

on the Dutch market for fixed telecommunications started to increase, however slightly. In addition, over

the last few years, competitors as Ziggo, Verizon, UPC and Tele2 have been increasing their market share

maintaining their prices lower than the incumbent KPN. Nevertheless, KPN continues to hold a large part of

the fixed telephony market. It is possible that the OPTA efforts aimed at encouraging competition will be

visible in the next few years given that we have seen that the most important competitors succeeded in

gaining 10/20% of market share in eight years.

In the matter of prices, we can state that over the period that we have taken into account (1998-2008),

there has not been a drop in prices for all the types of calls that we have considered. Reforms had a healthy

impact on Dutch citizens for national and international calls. For these kinds of calls, prices dropped

significantly in the Netherlands, while there was a paradoxical increase in local (3 km) call price. This drop in

price for national and international calls can be attributed to technology development (e.g. Voice over

Internet Protocol) or to the rise of new social networks which allow to make free calls or at an extremely

low price. Thus, this price reduction can be attributed to a demand decrease for national and international

calls. For this reason, it is likely possible that telecommunication companies put pressure mostly on local

calls as there is more demand for them compared to the national and international from fixed line.

When it comes to the degree of satisfaction of consumers, according to Ipsos Inra, analysis carried out in

2006, only 47% of citizens in the Netherlands think that their fixed telephone provider offers a quality

service overall. The pricing of fixed phone services remains, however, a point of dissatisfaction for Dutch

customers. It is possible that the penetration of mobile telephony, the competition between information

technologies and the lack of special prices for specific target groups or specific usage make fixed telephony

a basic service for which consumers are not ready to pay much anymore.

11 Oecd, Reveiws of Regulatory Reform: Regulatory Reform in the Netherlands 1999.

References:

Monograph:

OECD, "Regulatory Reform in the Netherlands. Regulatory Reform in the Telecommunications Industry",

1999. Available on: http://www.oecd.org/regreform/2507100.pdf

Florio Massimo, Network Industries and Social Welfare. The experiment that Reshuffled European Utilities,

Oxford University Press, 2013, p.3.

Occasional Papers 12, Market Functioning in Network Industries - Electronic Communications, Energy and

Transport, 2013. Available on:

http://ec.europa.eu/economy_finance/publications/occasional_paper/2013/pdf/ocp129_en.pdf

Emanuele Bacchiocchi, Massimo Florio, Marco Gambaro, Telecom Prices, Regulatory Reforms, Consumers’

Satisfaction: Evidence for 15 EU Countries, 2008. Available on: http://www.side-

isle.it/ocs/viewpaper.php?id=215&cf=2

Ipsos Inra, Consumer Satisfaction Survey, 2007. Available on:

http://ec.europa.eu/consumers/archive/cons_int/serv_gen/cons_satisf/consumer_service_finrep_en.pdf

Websites:

http://www.oecdbetterlifeindex.org/

http://www.itu.int/en/ITU-D/Statistics/Pages/stat/default.aspx

http://www.strategyanalytics.com/default.aspx?mod=saservice&a0=25&m=5#0

http://www.oecd.org/

https://www.acm.nl/en/