Fabrizio Balassone Econpubblica – Università Bocconi Milano, 25 Marzo 2009 Strenghtening...

51

Fabrizio Balassone Econpubblica – Università Bocconi Milano, 25 Marzo 2009 Strenghtening Medium- Term Fiscal Frameworks

-

Upload

ross-russell -

Category

Documents

-

view

222 -

download

2

Transcript of Fabrizio Balassone Econpubblica – Università Bocconi Milano, 25 Marzo 2009 Strenghtening...

Fabrizio Balassone

Econpubblica – Università Bocconi

Milano, 25 Marzo 2009

Strenghtening Medium-Term Fiscal Frameworks

JIQ

MTFF: definition & purpose

definition: set of institutions, procedures and rules governing (constraining) the development of public finances over the medium term

purpose: ensure fiscal discipline (sustainability & stabilization) and efficient use of resources

work on MTFF combines economics, institutional knowledge and a fair dose of pragmatism

JIQ

Fiscal discipline means...

maintaining a prudent budget balance to:

ensure sustainability of public debt

allow margins to face cyclical fluctuations and e unforeseeable events taking into account the degree of debt tolerance

(Kumar & Ter-Minassian, IMF 2007)

JIQ

Why budget discipline and efficiency?

fiscal discipline and efficiency maximize public sector (PS) contribution to economic growth and welfare

fiscal discipline = prerequisite to PS functions budget constraint is nec. cond. for allocative efficiency low debt no financial fragility margins for stabilization efficiency + stability growth resources for redistribution

NB discipline does not imply efficiency: need accountability budget transparency (informed and explicit choices) measurability of results (assessment)

JIQ

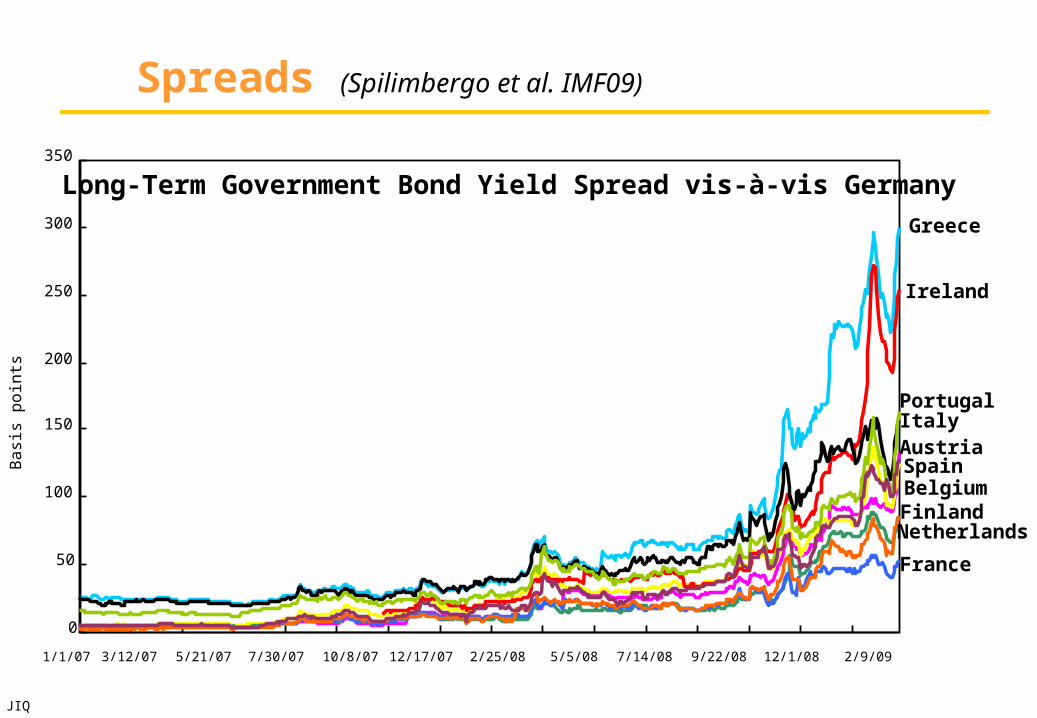

Spreads (Spilimbergo et al. IMF09)

Long-Term Government Bond Yield Spread vis-à-vis Germany

BelgiumFinland

France

Greece

Ireland

Italy

Netherlands

Spain

0

50

100

150

200

250

300

350

1/1/07 3/12/07 5/21/07 7/30/07 10/8/07 12/17/07 2/25/08 5/5/08 7/14/08 9/22/08 12/1/08 2/9/09

Basi

s po

ints

Austria

Portugal

JIQ

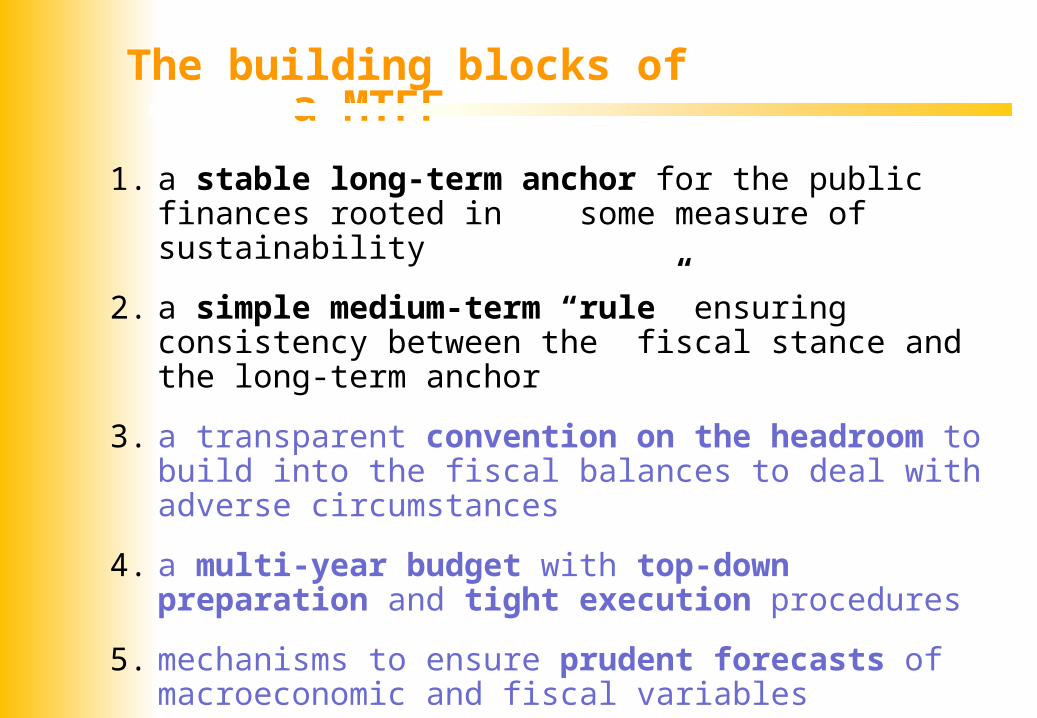

The building blocks of a MTFF

1. a stable long-term anchor for the public finances rooted in some measure of sustainability

2. a simple medium-term “rule” ensuring consistency between the fiscal stance and the long-term anchor

3. a transparent convention on the headroom to build into the fiscal balances to deal with adverse circumstances

4. a multi-year budget with top-down preparation and tight execution procedures

5. mechanisms to ensure prudent forecasts of macroeconomic and fiscal variables

6. reporting, monitoring, auditing tools to ensure accountability

JIQ

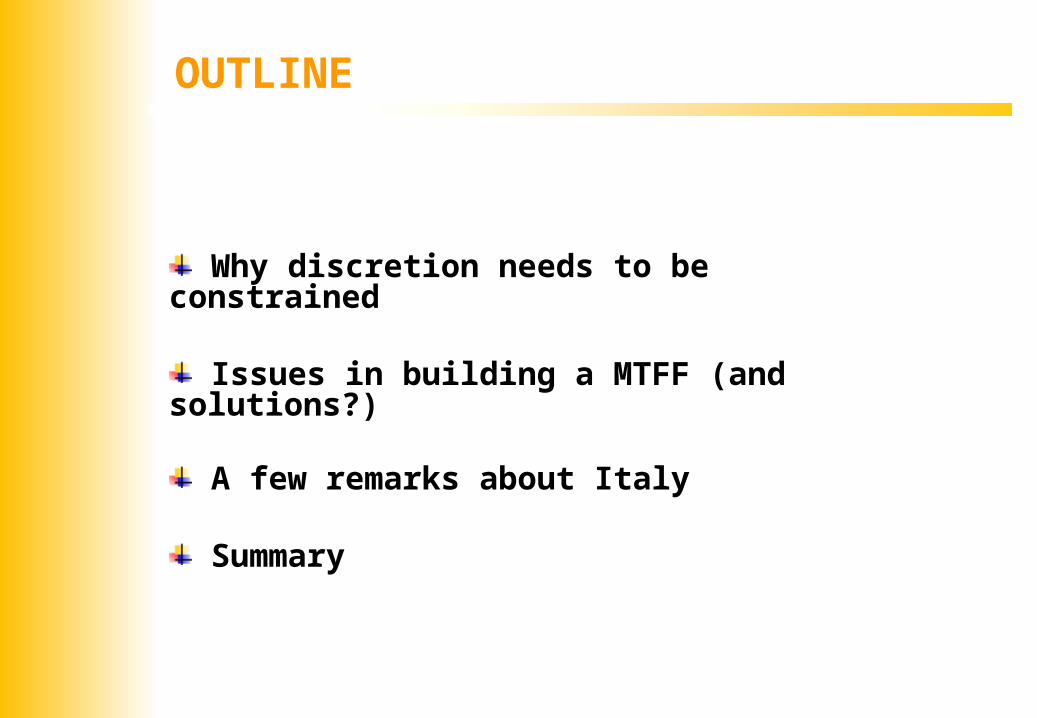

OUTLINE

Why discretion needs to be constrained

Issues in building a MTFF (and solutions?)

A few remarks about Italy

Summary

JIQ

I. Why Does Discretion Need to Be Constrained?

JIQ

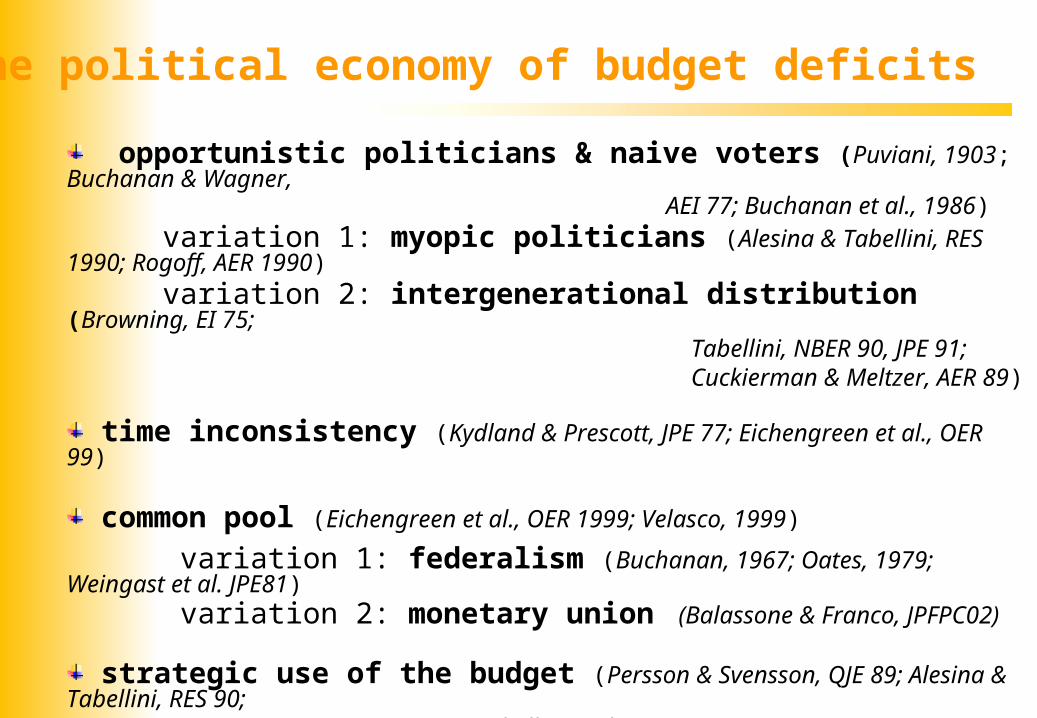

opportunistic politicians & naive voters (Puviani, 1903; Buchanan & Wagner, AEI 77; Buchanan et al., 1986) variation 1: myopic politicians (Alesina & Tabellini, RES 1990; Rogoff, AER 1990) variation 2: intergenerational distribution (Browning, EI 75;

Tabellini, NBER 90, JPE 91; Cuckierman & Meltzer, AER 89)

time inconsistency (Kydland & Prescott, JPE 77; Eichengreen et al., OER 99)

common pool (Eichengreen et al., OER 1999; Velasco, 1999)

variation 1: federalism (Buchanan, 1967; Oates, 1979; Weingast et al. JPE81) variation 2: monetary union (Balassone & Franco, JPFPC02)

strategic use of the budget (Persson & Svensson, QJE 89; Alesina & Tabellini, RES 90; Tabellini & Alesina, AER 1990)

coalitions & wars of attrition (Roubini-Sachs, EP89; Alesina-Drazen, AER91; Balassone-Giordano, PC01)

The political economy of budget deficits

JIQ

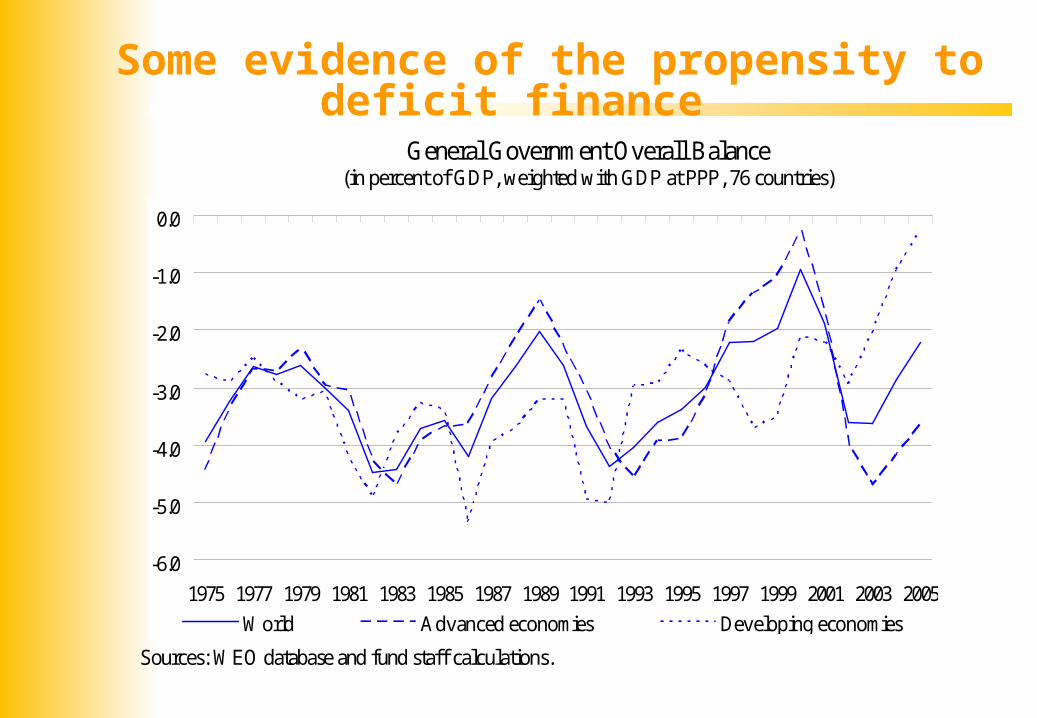

General Government Overall Balance (in percent of GDP, weighted with GDP at PPP, 76 countries)

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

World Advanced economies Developing economies

Sources: WEO database and fund staff calculations.

Some evidence of the propensity to deficit finance

JIQ

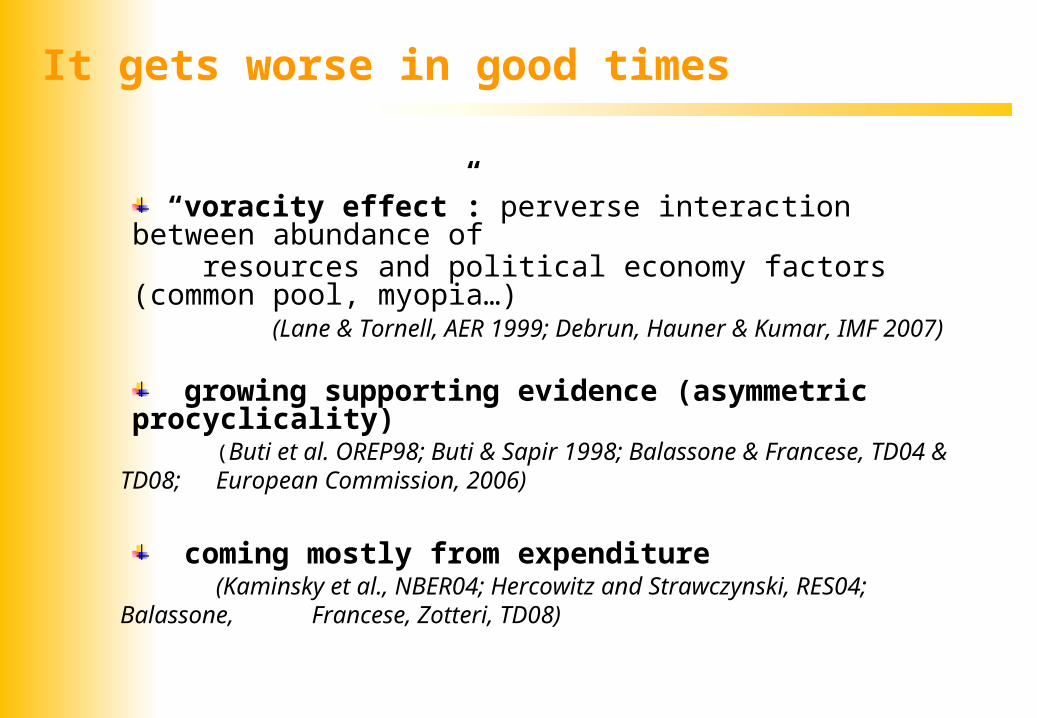

“voracity effect”: perverse interaction between abundance of resources and political economy factors (common pool, myopia…) (Lane & Tornell, AER 1999; Debrun, Hauner & Kumar, IMF 2007)

growing supporting evidence (asymmetric procyclicality)(Buti et al. OREP98; Buti & Sapir 1998; Balassone & Francese, TD04 &

TD08; European Commission, 2006)

coming mostly from expenditure(Kaminsky et al., NBER04; Hercowitz and Strawczynski, RES04; Balassone, Francese, Zotteri, TD08)

It gets worse in good times

JIQ

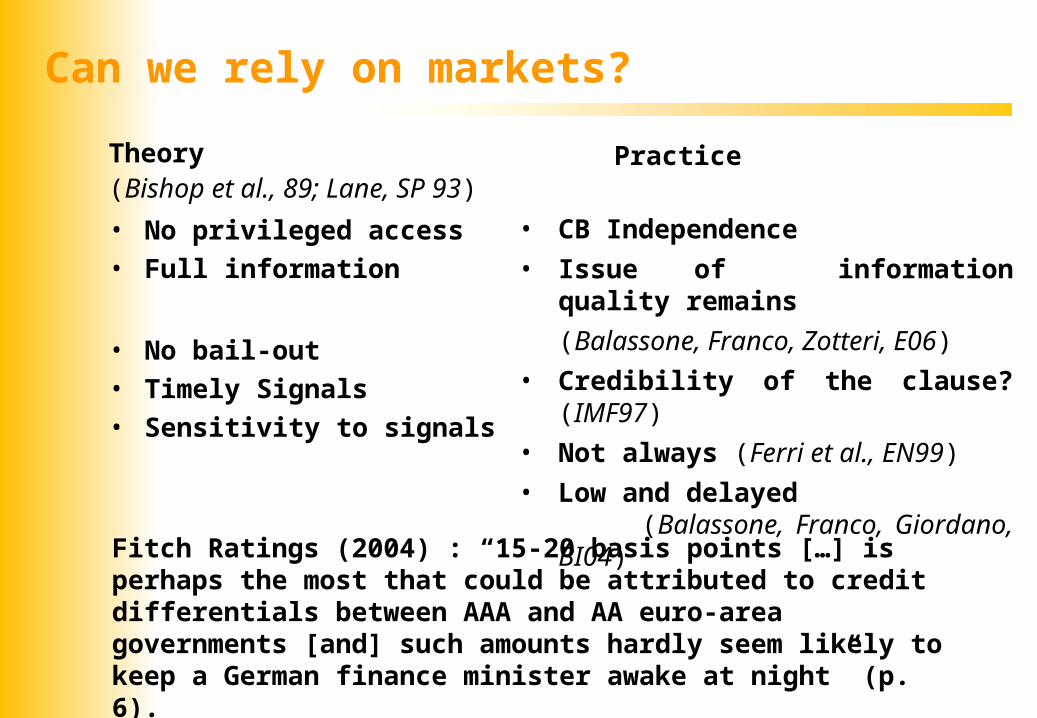

Theory(Bishop et al., 89; Lane, SP 93)

• No privileged access

• Full information

• No bail-out

• Timely Signals

• Sensitivity to signals

Practice

• CB Independence

• Issue of information quality remains

(Balassone, Franco, Zotteri, E06)

• Credibility of the clause? (IMF97)

• Not always (Ferri et al., EN99)

• Low and delayed (Balassone, Franco, Giordano, BI04)

Fitch Ratings (2004) : “15-20 basis points […] is perhaps the most that could be attributed to credit differentials between AAA and AA euro-area governments [and] such amounts hardly seem likely to keep a German finance minister awake at night” (p. 6).

Can we rely on markets?

JIQ

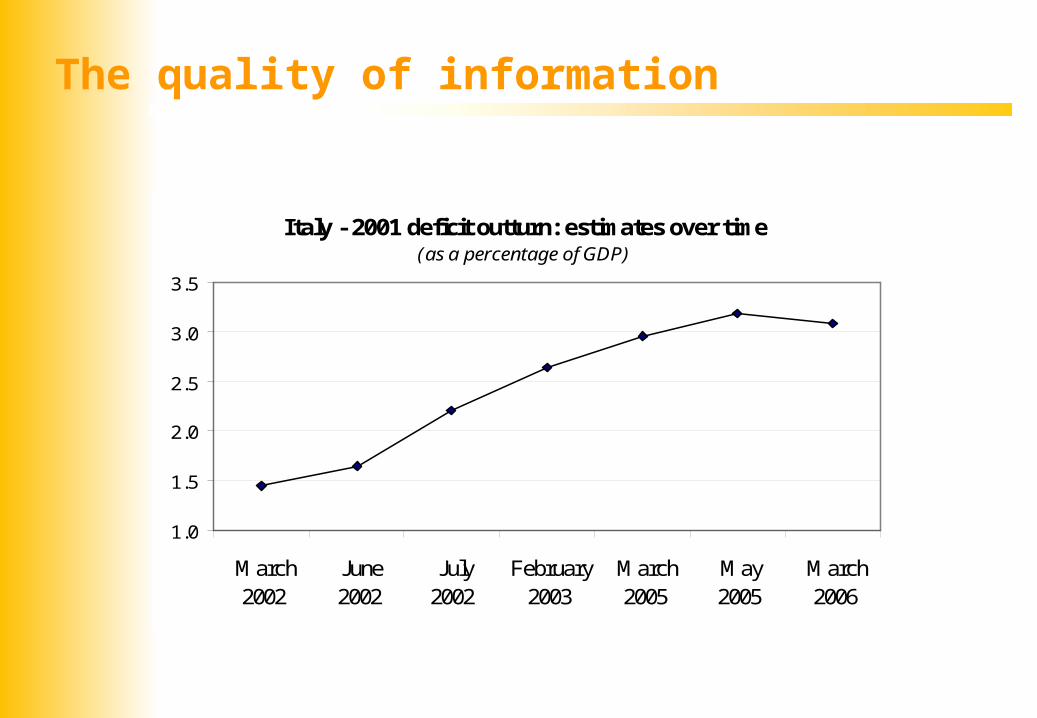

Italy - 2001 deficit outturn: estimates over time(as a percentage of GDP)

1.0

1.5

2.0

2.5

3.0

3.5

March2002

June2002

July2002

February2003

March2005

May2005

March2006

The quality of information

JIQ

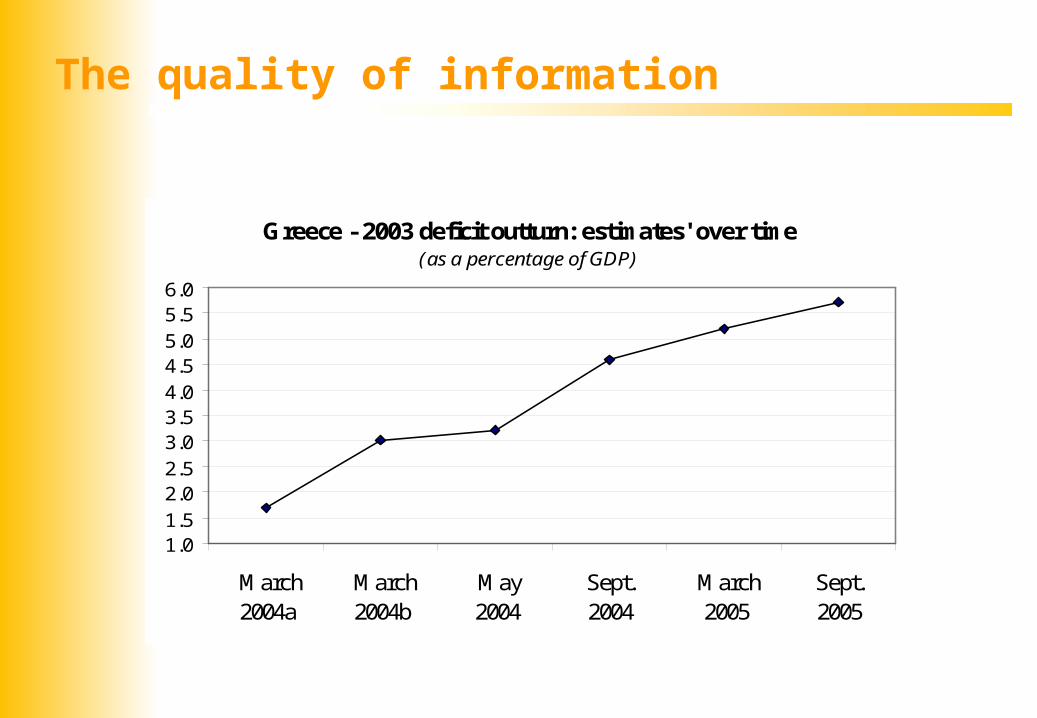

Greece - 2003 deficit outturn: estimates' over time(as a percentage of GDP)

1.01.52.02.53.03.54.04.55.05.56.0

March2004a

March2004b

May 2004

Sept. 2004

March2005

Sept. 2005

The quality of information

JIQ

II. Issues in Building a MTFF

JIQ

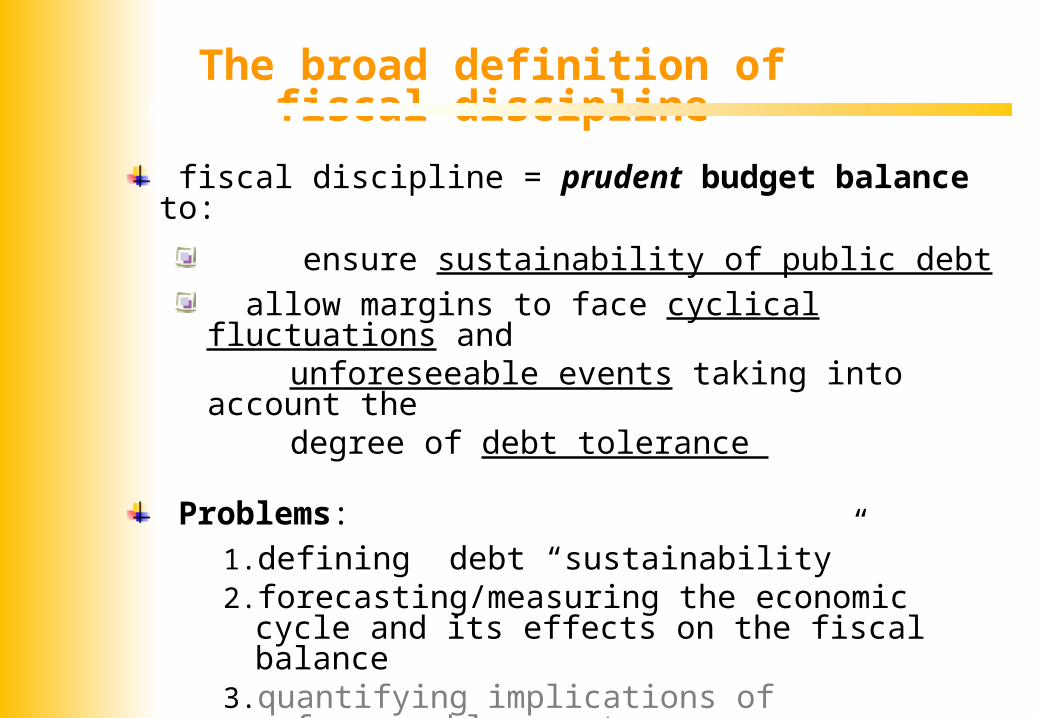

The broad definition of fiscal discipline

fiscal discipline = prudent budget balance to:

ensure sustainability of public debt

allow margins to face cyclical fluctuations and unforeseeable events taking into account the degree of debt tolerance

Problems:

1. defining debt “sustainability” 2. forecasting/measuring the economic cycle and its effects

on the fiscal balance3. quantifying implications of unforeseeable events

(e.g. contingent liabilities - IMF 2007)

4. estimating the degree of “debt tolerance” (history? Reinhart, Rogoff & Savastano, NBER 2003)

JIQ

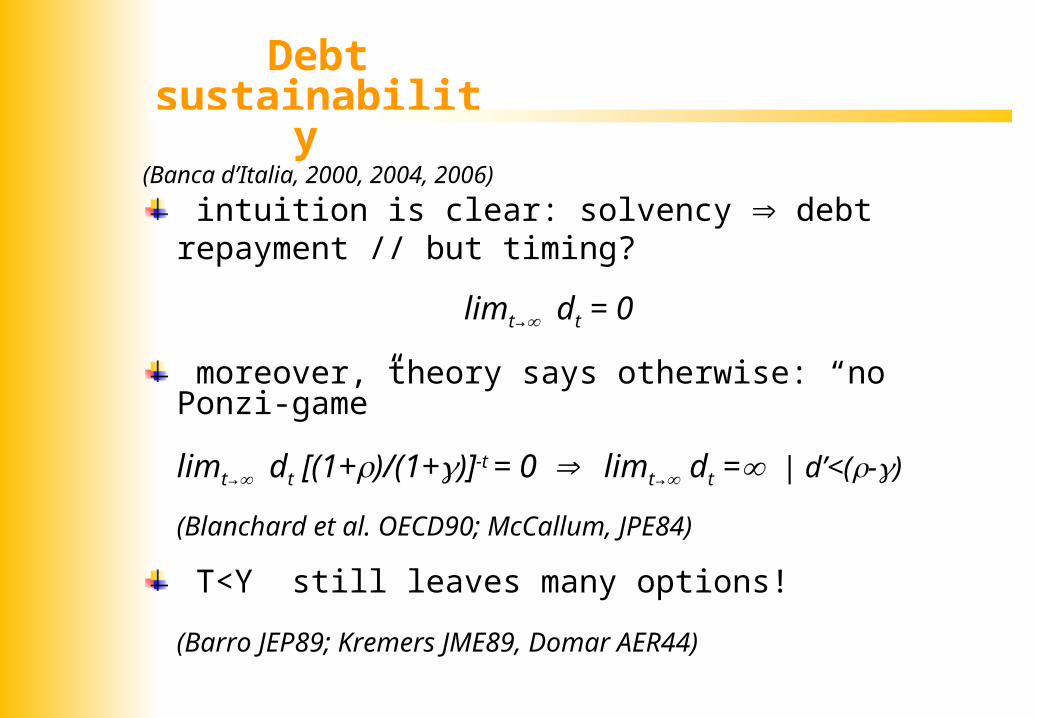

Debt sustainability (Banca d’Italia, 2000, 2004, 2006)

intuition is clear: solvency debt repayment // but timing?

limt→ dt = 0

moreover, theory says otherwise: “no Ponzi-game”

limt→ dt [(1+)/(1+)]-t = 0 limt→ dt = | d’<(-)

(Blanchard et al. OECD90; McCallum, JPE84)

T<Y still leaves many options!

(Barro JEP89; Kremers JME89, Domar AER44)

JIQ

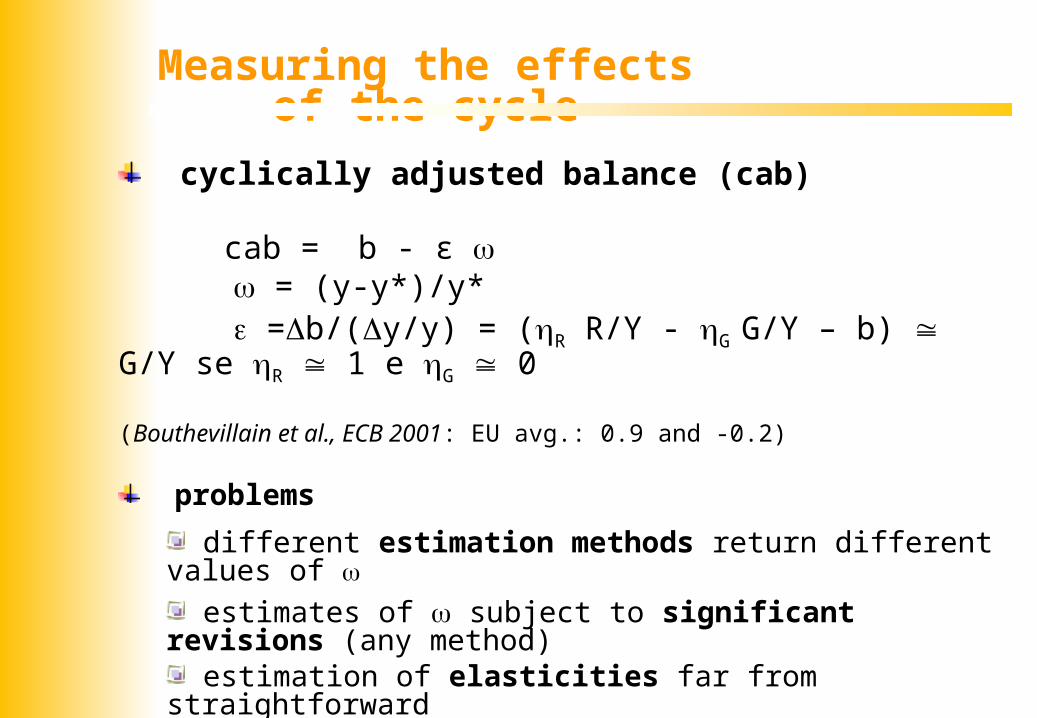

Measuring the effects of the cycle

cyclically adjusted balance (cab) cab = b - ε = (y-y*)/y* =b/(y/y) = (R R/Y - G G/Y – b) G/Y se R 1 e G 0

(Bouthevillain et al., ECB 2001: EU avg.: 0.9 and -0.2)

problems

different estimation methods return different values of

estimates of subject to significant revisions (any method) estimation of elasticities far from straightforward is the output gap enough? (composition of output; other variables)

JIQ

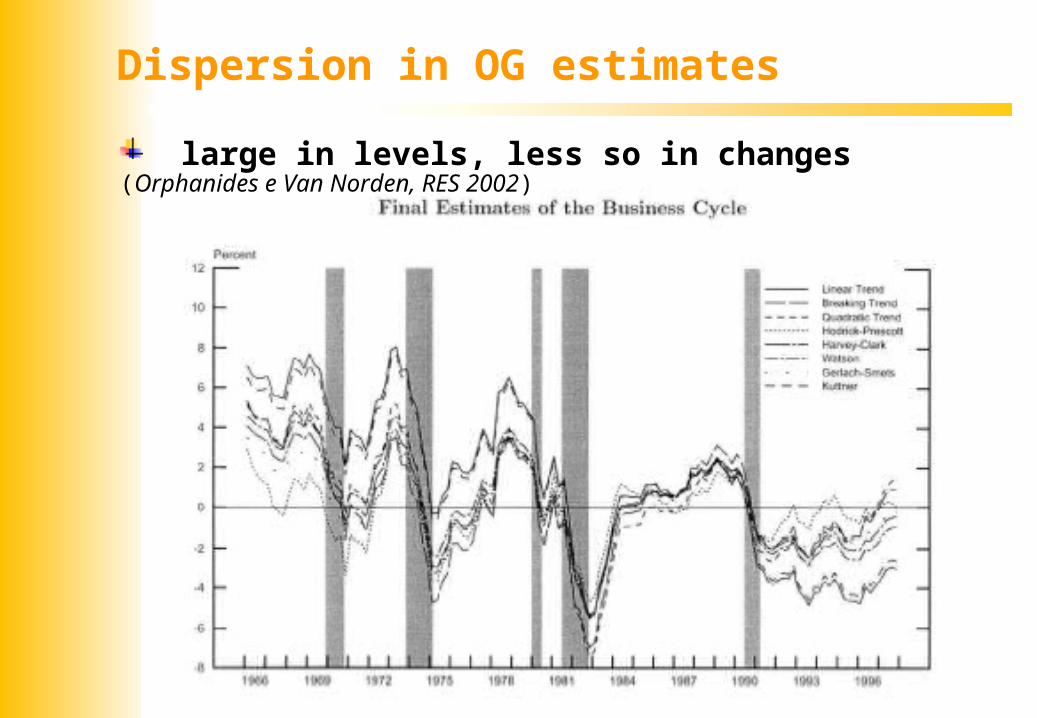

Dispersion in OG estimates

large in levels, less so in changes (Orphanides e Van Norden, RES 2002)

JIQ

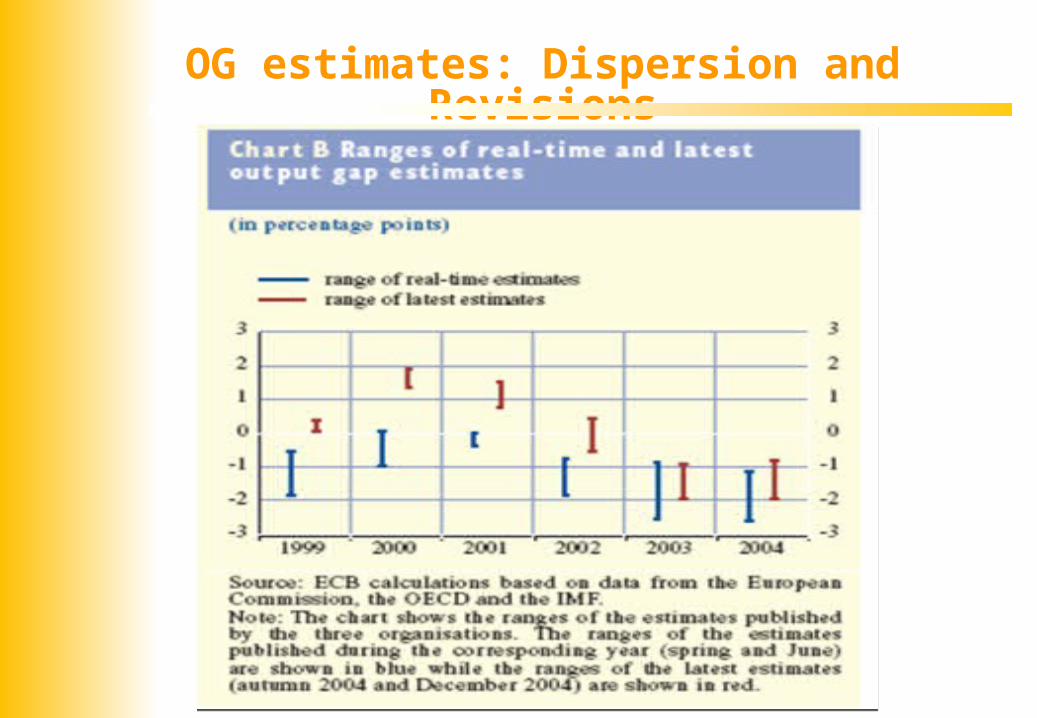

OG estimates: Dispersion and Revisions

JIQ

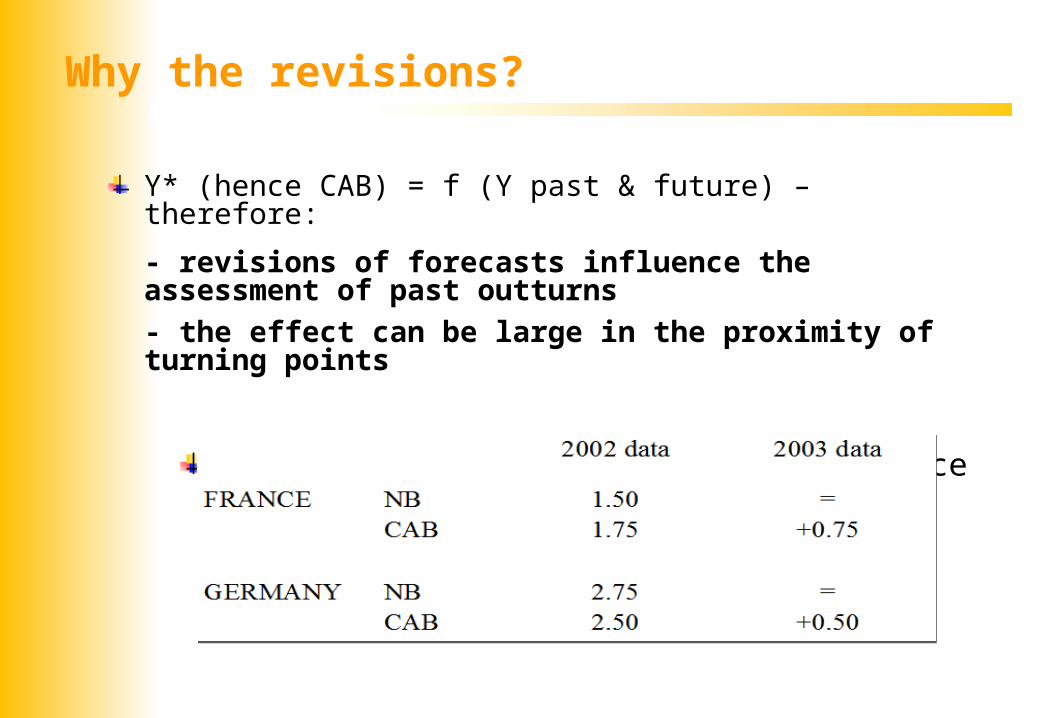

Y* (hence CAB) = f (Y past & future) – therefore:

- revisions of forecasts influence the assessment of past outturns

- the effect can be large in the proximity of turning points

Example: 2001 fiscal balances in France and Germany

Why the revisions?

JIQ

Elasticities

data intensive

institutional knowledge vs. econometrics (reforms)

identification of macroeconomic proxies for tax bases (e.g. profits)

JIQ

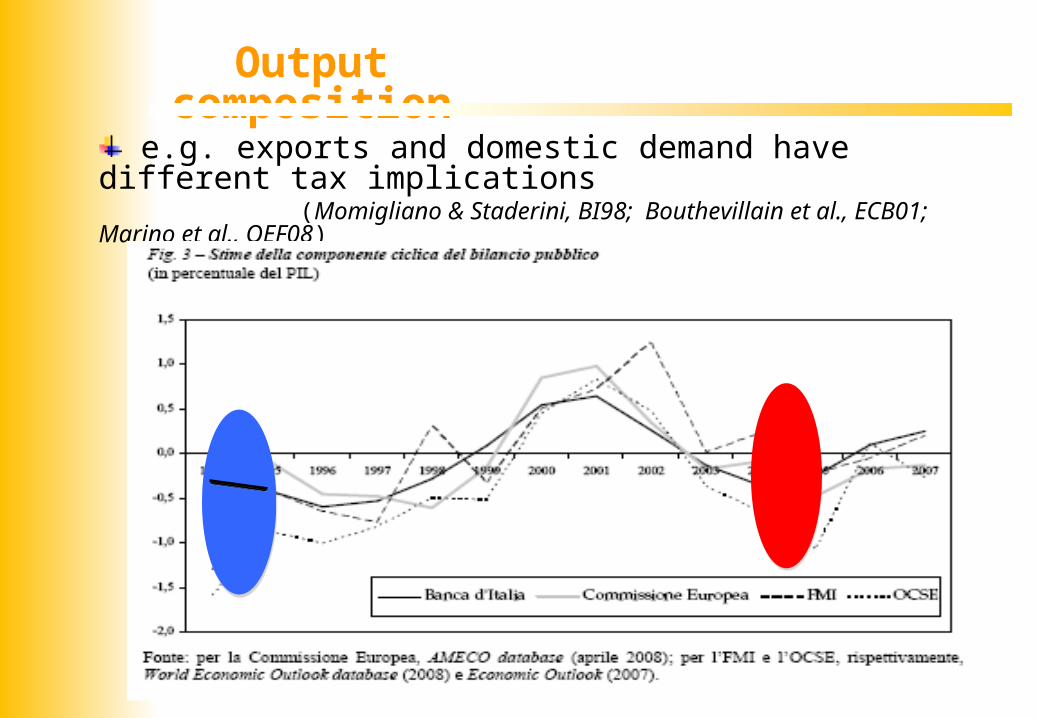

Output composition

e.g. exports and domestic demand have different tax implications (Momigliano & Staderini, BI98; Bouthevillain et al., ECB01; Marino et al., QEF08)

JIQ

A pragmatic approach

In sum: theory does not provide full guidance in defining both the long-term anchor and the medium term rule for a MTFF

Need a pragmatic approach: Define “prudent” debt levels

somewhat ad hoc (UK-EU) but not too different from proposals by theorists (Blanchard ES90, Buiter EP85…)

Derive corresponding “structural” deficit targets- based on long-term expenditure projections- use sensitivity analysis (sustainability reports – Norway; EPC ageing working group 2006)

Define medium-term / “over-the-cycle” targets with escape clauses in the face of unfavorable circumstances (Sweden; UK code of fiscal conduct; …)

JIQ

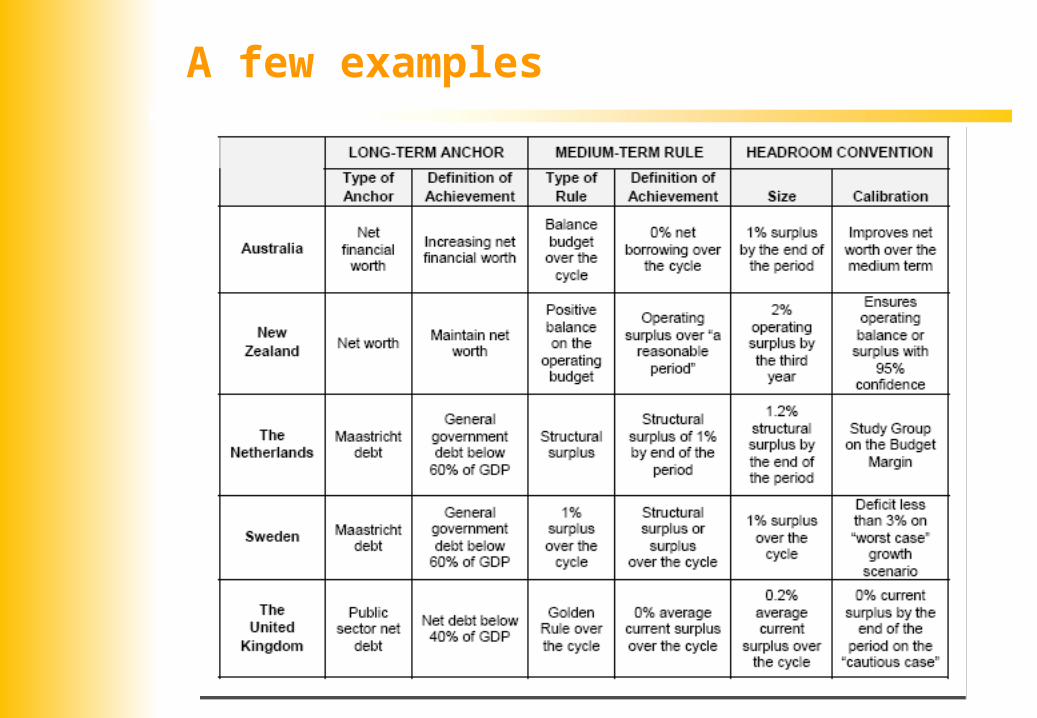

A few examples

JIQ

The design of fiscal rules

Rules = Rules = commitment-devicescommitment-devices and and signaling toolssignaling tools (they increase the costs of deviating from the target for policymakers and (they increase the costs of deviating from the target for policymakers and reduce public’s uncertainty about policymakers’ commitment)reduce public’s uncertainty about policymakers’ commitment)

Constrain the bias but Constrain the bias but mindful not tomindful not to::

√ introduceintroduce excess rigidity excess rigidity and prevent adequate responses and prevent adequate responses (e.g. let automatic stabilizers play in bad times – balanced budget rule?)(e.g. let automatic stabilizers play in bad times – balanced budget rule?) ,,

√ force inadequate responsesforce inadequate responses (e.g. a fiscal contraction in response to a temporary spike in interest rate, (e.g. a fiscal contraction in response to a temporary spike in interest rate, or depreciation of the exchange rate),or depreciation of the exchange rate),

√ Let the Let the bias unchecked in specific circumstancesbias unchecked in specific circumstances (e.g. allow for procyclical expansions – medium-term/over-the-cycle (e.g. allow for procyclical expansions – medium-term/over-the-cycle

formulations like the (old?) SGP and UK code of fiscal conduct)formulations like the (old?) SGP and UK code of fiscal conduct)

JIQ

√ some rules are not targeted to fiscal discipline (golden rule sustainability)

√ window dressing (inconsistent deficit/debt indicators – SGP)

√ some rules cannot stand alone (e.g. expenditure rules)

Other issues of “design”

JIQ

Expenditure rules PROS:

provide a stronger link between the long-term anchor and the multi-annual budget exercise

tackle the bias at source (expenditure)

let (revenue) automatic stabilizers play

BUT

cannot leave the revenue side unchecked (tax expenditure)

MORE COMPLEX THAN IT SEEMS

what about automatic stabilizers on the expenditure side?

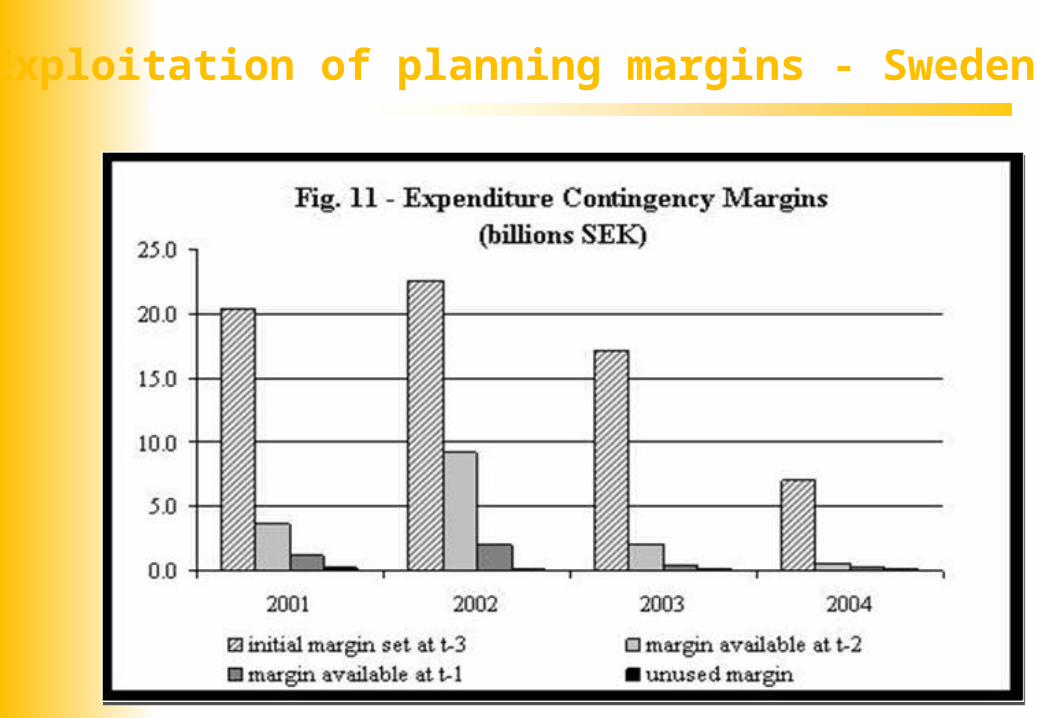

possible exploitation of planning margins?

JIQ

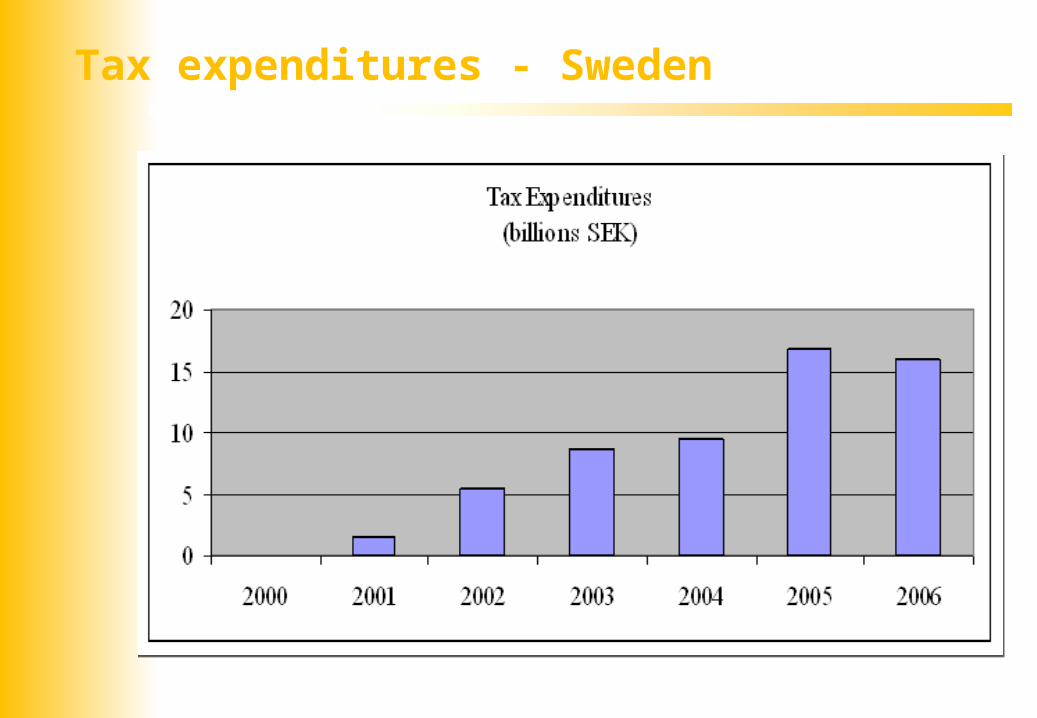

Tax expenditures - Sweden

JIQ

Exploitation of planning margins - Sweden

JIQ

III. Some Remarks about Italy

JIQ

SGP: debt-to-GDP ratio = 60% but when?(“satisfactory pace” never defined)

Often D/Y<100% targeted in official documents BUT on what basis?

No sustainability report – setting medium-term deficit target?(long-term projections only for the EPC AWG)

The long-term anchor and the fiscal stance

JIQ

EU: structural adjustment by ½ percent per year towards structural balance + free play of automatic stabilizers

Truly endorsed?

No explicit convention about headroom within the target

The medium-term rule

JIQ

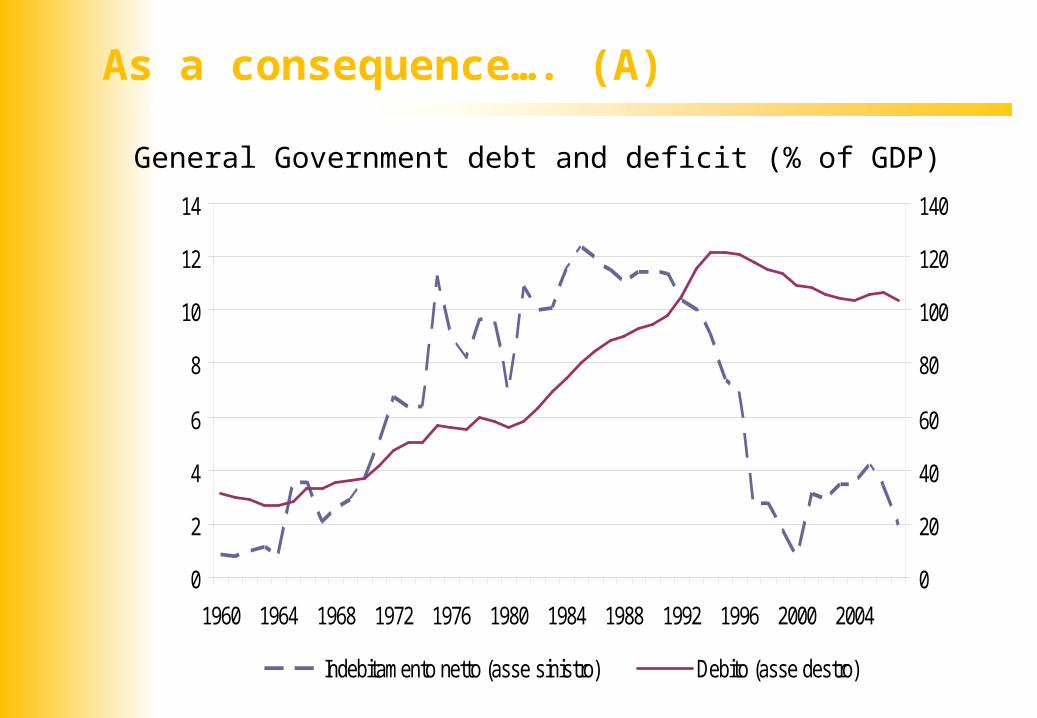

General Government debt and deficit (% of GDP)

As a consequence…. (A)

0

2

4

6

8

10

12

14

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 20040

20

40

60

80

100

120

140

Indebitamento netto (as s e s inis tro) Debito (as s e des tro)

JIQ

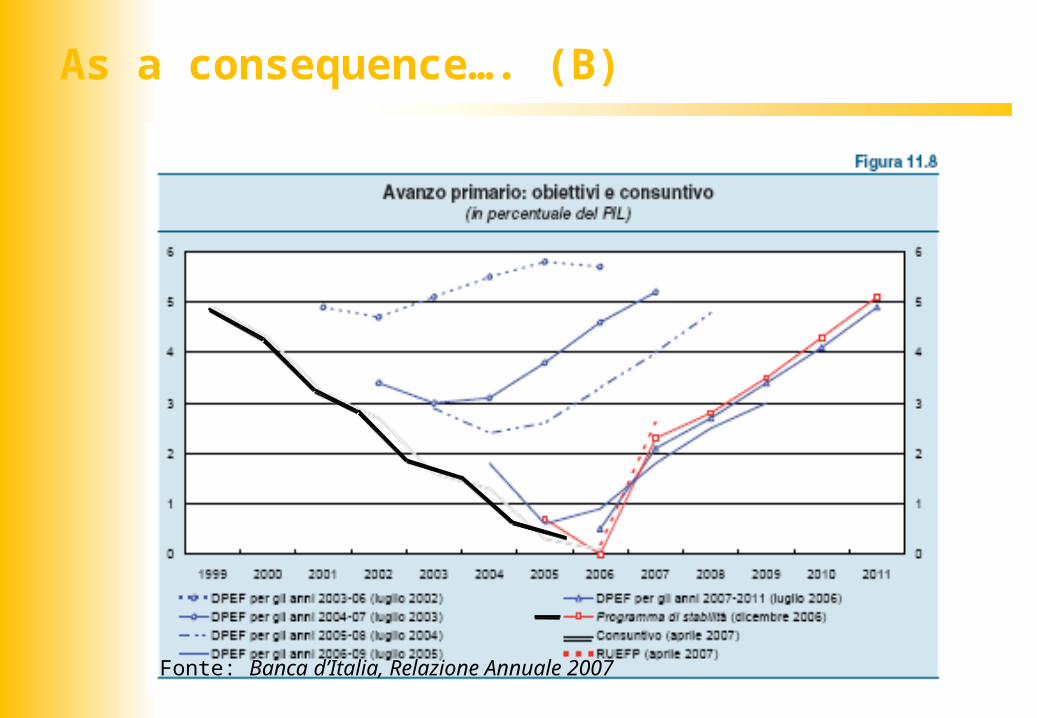

As a consequence…. (B)

Fonte: Banca d’Italia, Relazione Annuale 2007

JIQ

No “true” multi-year budget(3 years but t+1 and t+2 are forecasts, not binding plans)

No top-down budgeting(no expenditure ceilings)

Rather lax execution (no explicit contingency reserve but weak link between authorizations from the state budget and accounts relevant to the fiscal targets)(possibility to use “windfall revenues” to increase expenditure)

Multi-year budget, top-down preparation, tight execution

JIQ

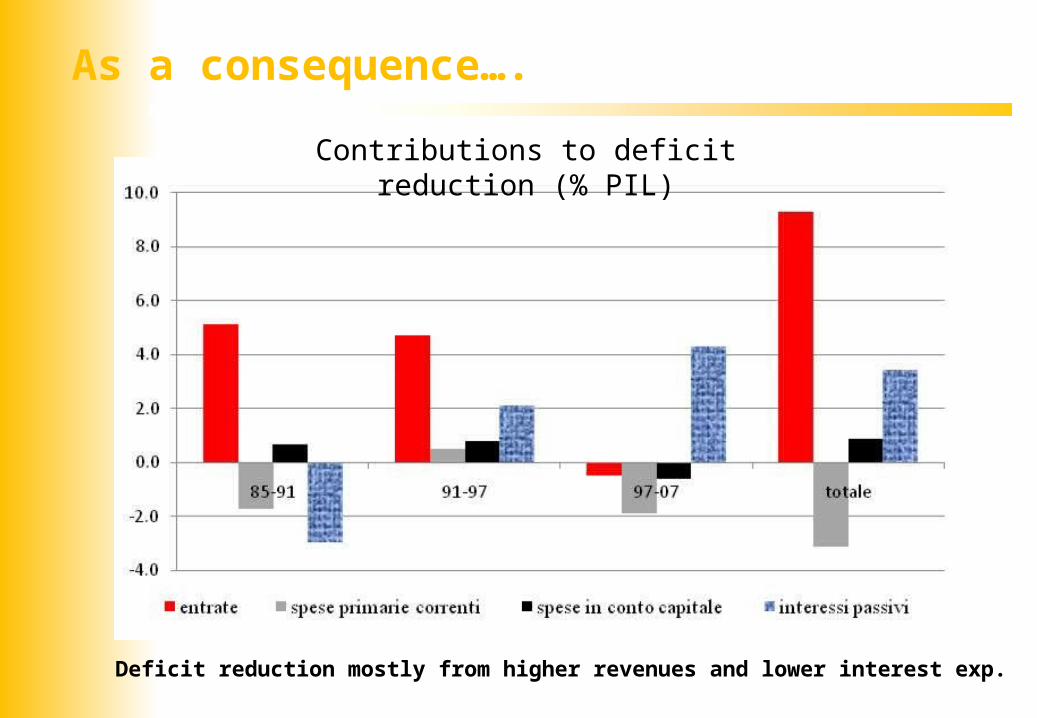

As a consequence….

Deficit reduction mostly from higher revenues and lower interest exp.

Contributions to deficit reduction (% PIL)

JIQ

Insufficient information on fiscal projections on a current programs basis & on costing of new legislation

Difficult to assess outturn

No formal assignment of independent assessment (plus nothing much happens if targets are not met)

Budget and legislation by line-items not programs

Not surprisingly the 2007/2008 spending review found abundant evidence of inefficiency in the use of public money(CTSP08)

Prudent forecasts - Accountability

JIQ

0

20

40

60

80

100

120

140

160

180

200

La-Ab-Sa

Si-Cal Cam-Mo

Ve-TAA-

Fr

Pu-Ba ER-Ma To-Um Lo-Li Pi-VdA

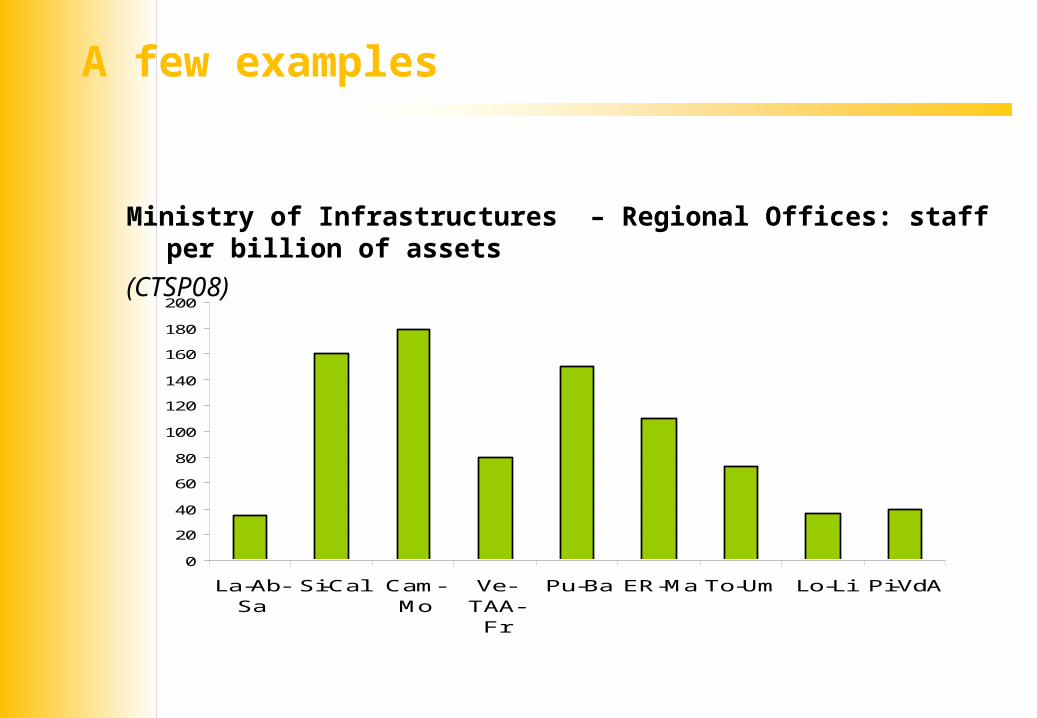

A few examples

Ministry of Infrastructures – Regional Offices: staff per billion of assets

(CTSP08)

JIQ

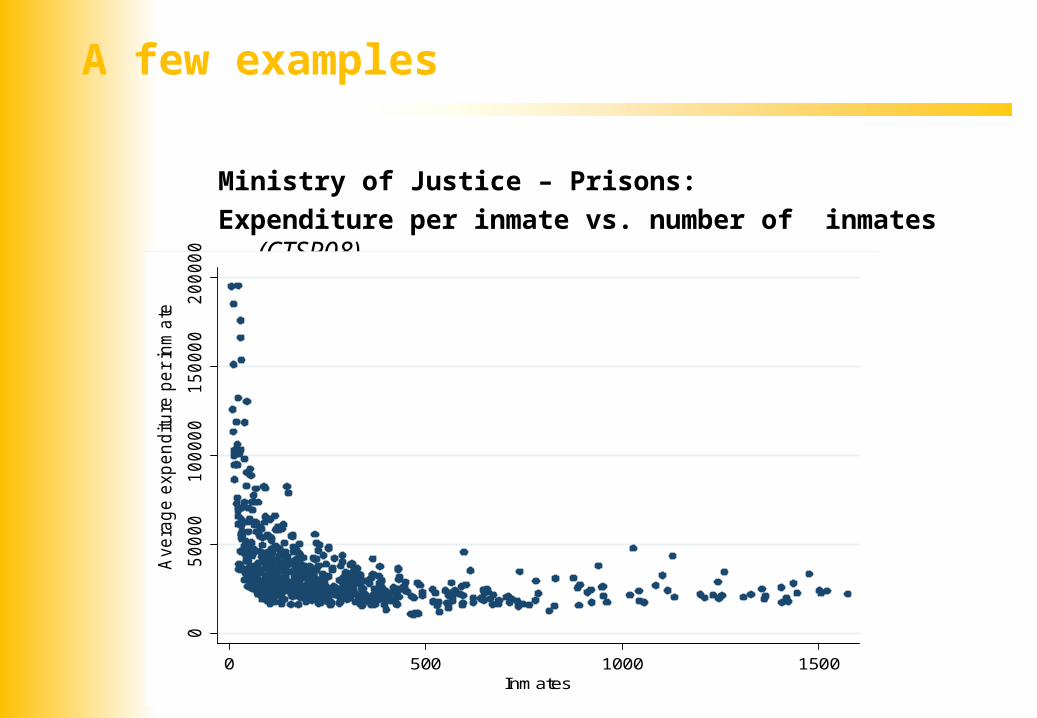

Ministry of Justice – Prisons:

Expenditure per inmate vs. number of inmates (CTSP08)0

500

00

100

00

01

50

00

02

00

00

0

Ave

rag

e e

xp

en

ditu

re p

er

inm

ate

0 500 1000 1500

Inmates

A few examples

JIQ

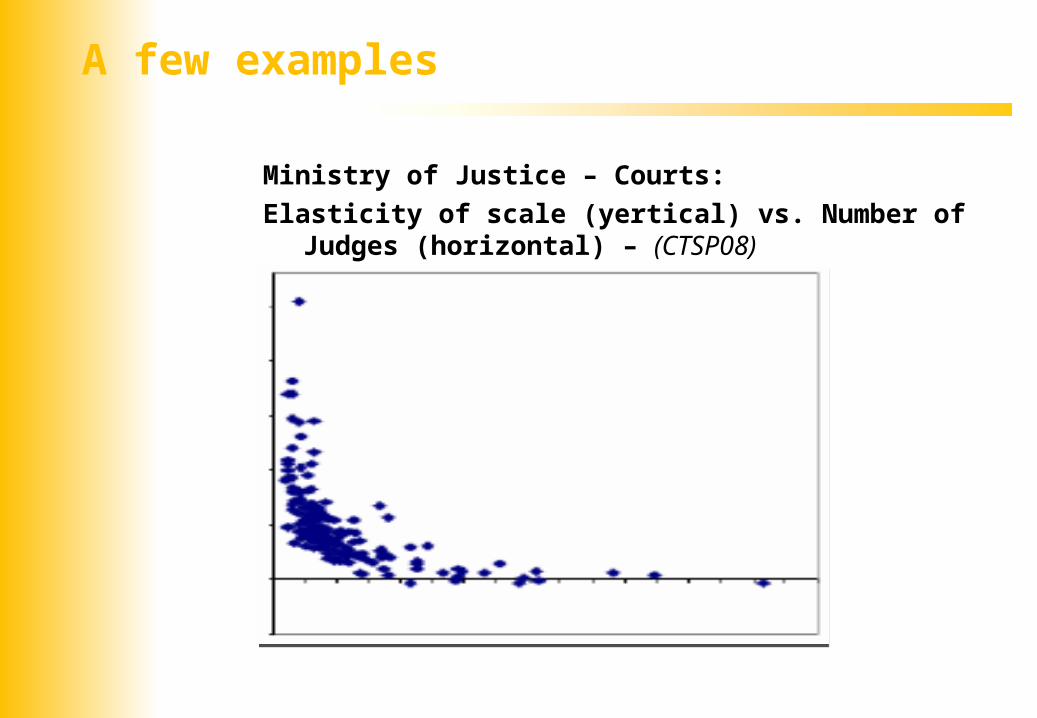

Ministry of Justice – Courts:

Elasticity of scale (yertical) vs. Number of Judges (horizontal) – (CTSP08)

A few examples

JIQ

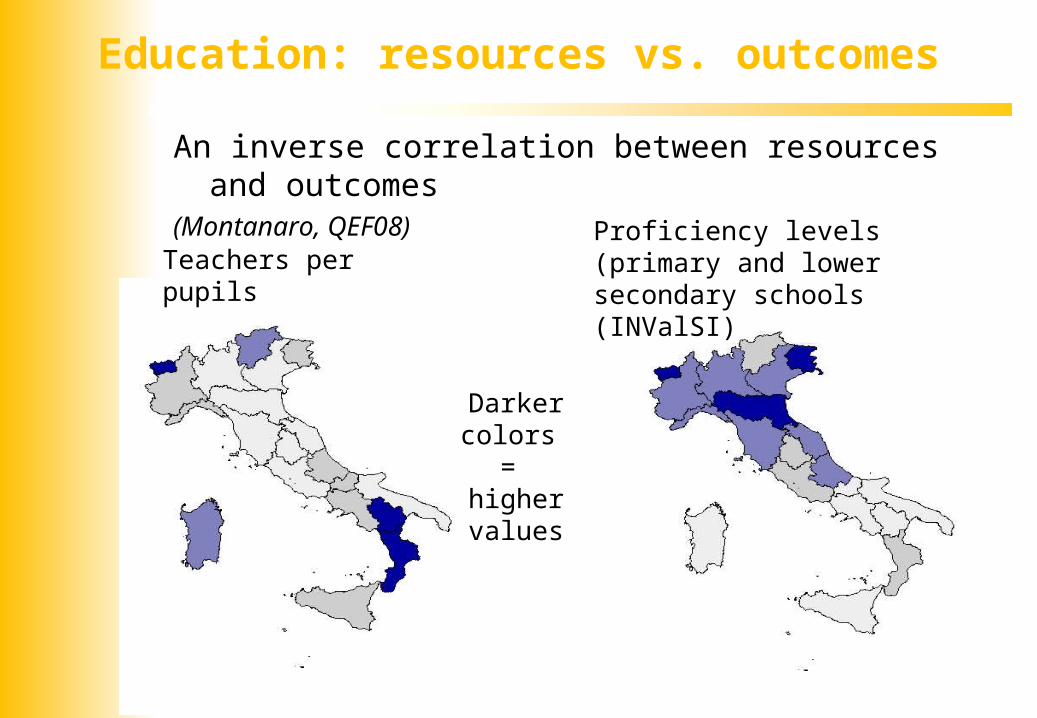

Education: resources vs. outcomes

Darker colors =

higher values

Teachers per pupils

An inverse correlation between resources and outcomes(Montanaro, QEF08)

Proficiency levels (primary and lower secondary schools (INValSI)

JIQ

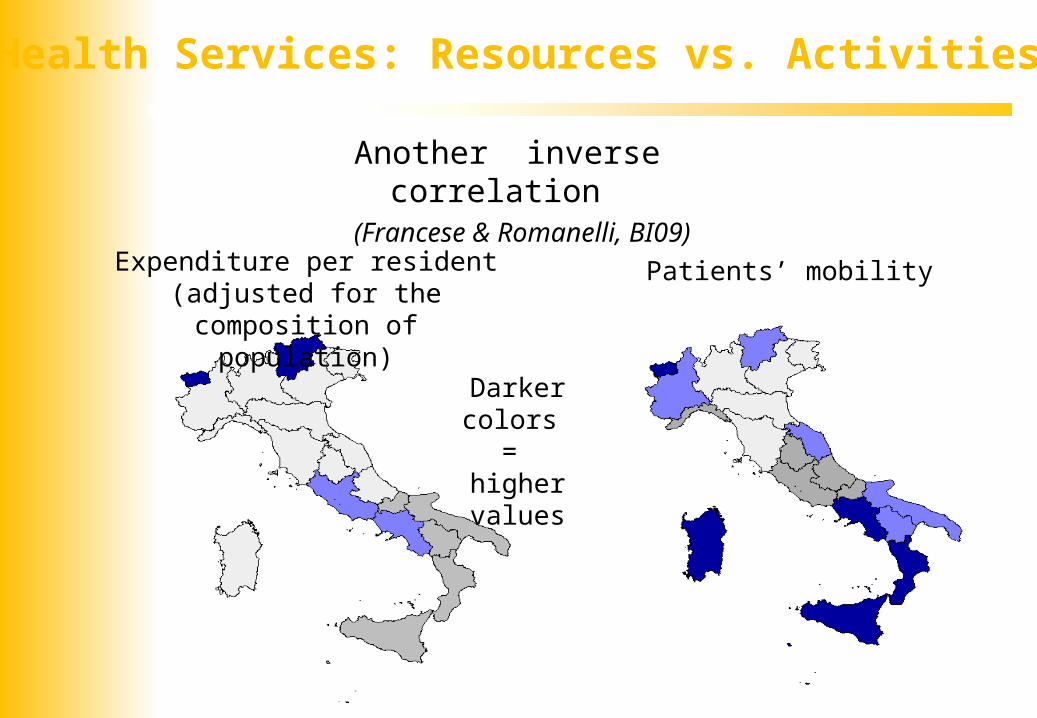

Health Services: Resources vs. Activities

Expenditure per resident (adjusted for the composition of population)

Patients’ mobility

Another inverse correlation(Francese & Romanelli, BI09)

Darker colors =

higher values

JIQ

IV. Summary and Conclusions

JIQ

1. There are significant incentives to fiscal indiscipline (both theory and evidence)

2. This entails both macro-risks and micro inefficiency

3. MTFFs can help re-engineering incentives and control risks:

they are not a magic wand but one is better-off having them

(issues in design & enforcement)

4. Italy: EU fiscal rules provide a frame but content needs to be

defined at the national level

JIQ

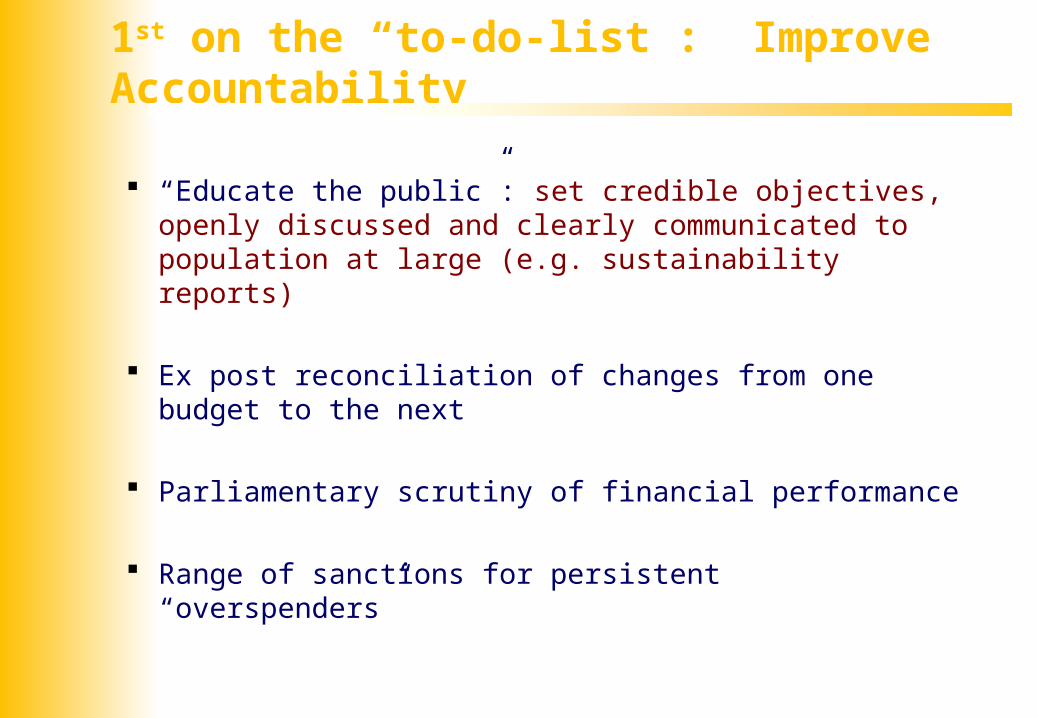

1st on the “to-do-list”: Improve Accountability

“Educate the public”: set credible objectives, openly discussed and clearly communicated to population at large (e.g. sustainability reports)

Ex post reconciliation of changes from one budget to the next

Parliamentary scrutiny of financial performance

Range of sanctions for persistent “overspenders”

JIQ

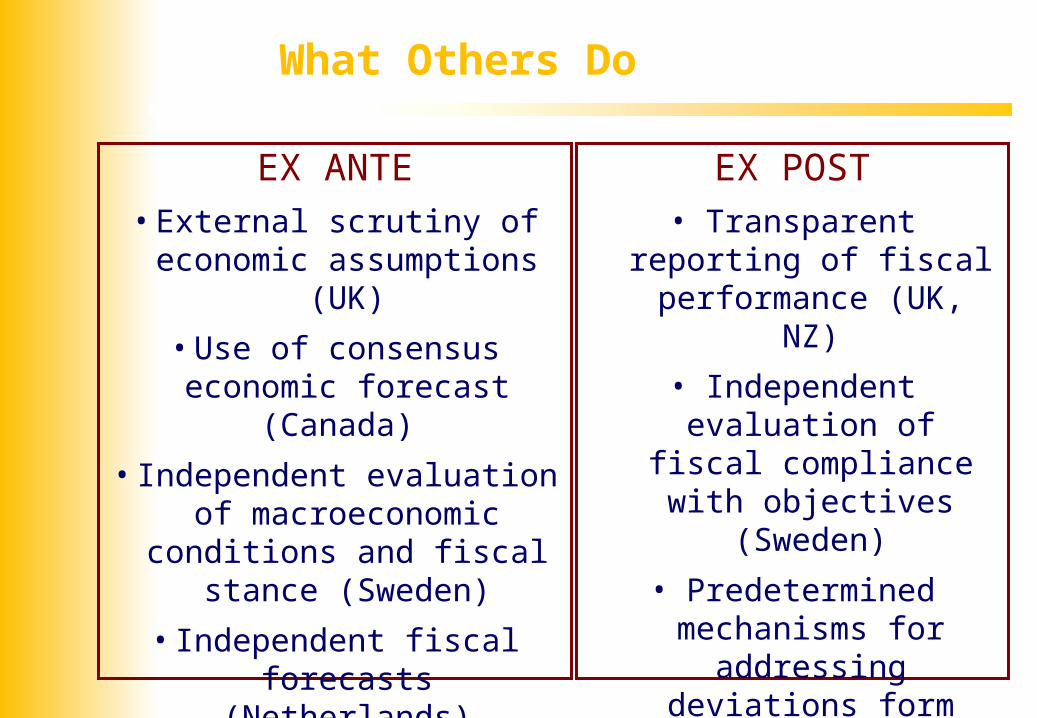

What Others Do

EX ANTE• External scrutiny of economic

assumptions (UK)

• Use of consensus economic forecast (Canada)

• Independent evaluation of macroeconomic conditions and

fiscal stance (Sweden)

• Independent fiscal forecasts (Netherlands)

EX POST• Transparent reporting of fiscal performance (UK, NZ)

• Independent evaluation of fiscal compliance with objectives (Sweden)

• Predetermined mechanisms for addressing deviations

form forecasts (Switzerland)

JIQ48

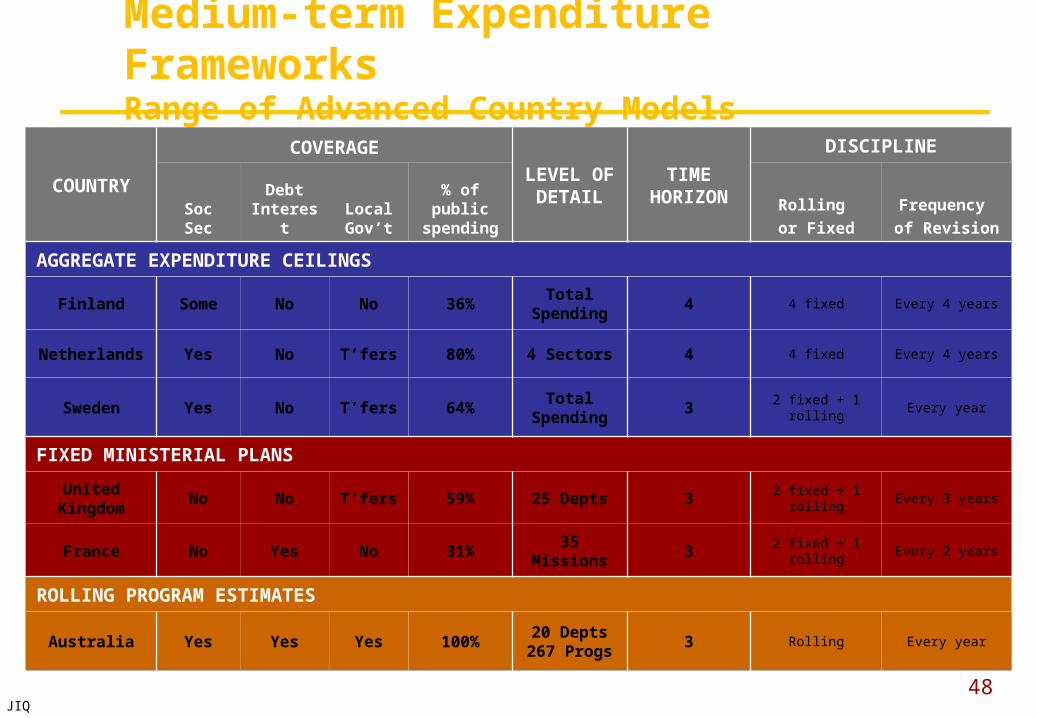

Medium-term Expenditure FrameworksRange of Advanced Country Models

COUNTRY

COVERAGE

LEVEL OF DETAIL

TIME HORIZON

DISCIPLINE

Soc SecDebt

InterestLocal Gov’t

% of public

spending

Rolling

or Fixed

Frequency

of Revision

AGGREGATE EXPENDITURE CEILINGS

Finland Some No No 36%Total

Spending4 4 fixed Every 4 years

Netherlands Yes No T’fers 80% 4 Sectors 4 4 fixed Every 4 years

Sweden Yes No T’fers 64%Total

Spending3 2 fixed + 1 rolling Every year

FIXED MINISTERIAL PLANS

United Kingdom

No No T’fers 59% 25 Depts 3 2 fixed + 1 rolling Every 3 years

France No Yes No 31% 35 Missions 3 2 fixed + 1 rolling Every 2 years

ROLLING PROGRAM ESTIMATES

Australia Yes Yes Yes 100%20 Depts

267 Progs3 Rolling Every year

JIQ

49

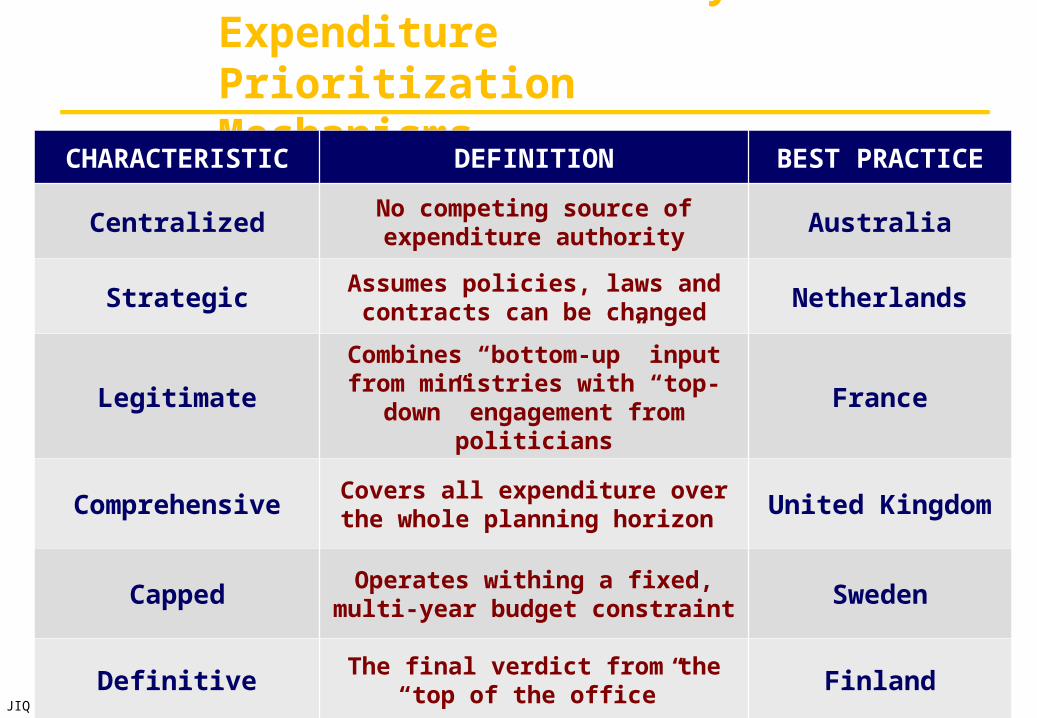

Effective Multi-year Expenditure Prioritization Mechanisms

CHARACTERISTIC DEFINITION BEST PRACTICE

CentralizedNo competing source of

expenditure authority Australia

StrategicAssumes policies, laws and contracts can be changed Netherlands

LegitimateCombines “bottom-up” input from

ministries with “top-down” engagement from politicians

France

ComprehensiveCovers all expenditure over the

whole planning horizon United Kingdom

CappedOperates withing a fixed, multi-year

budget constraint Sweden

DefinitiveThe final verdict from the “top of

the office” Finland

JIQ

50

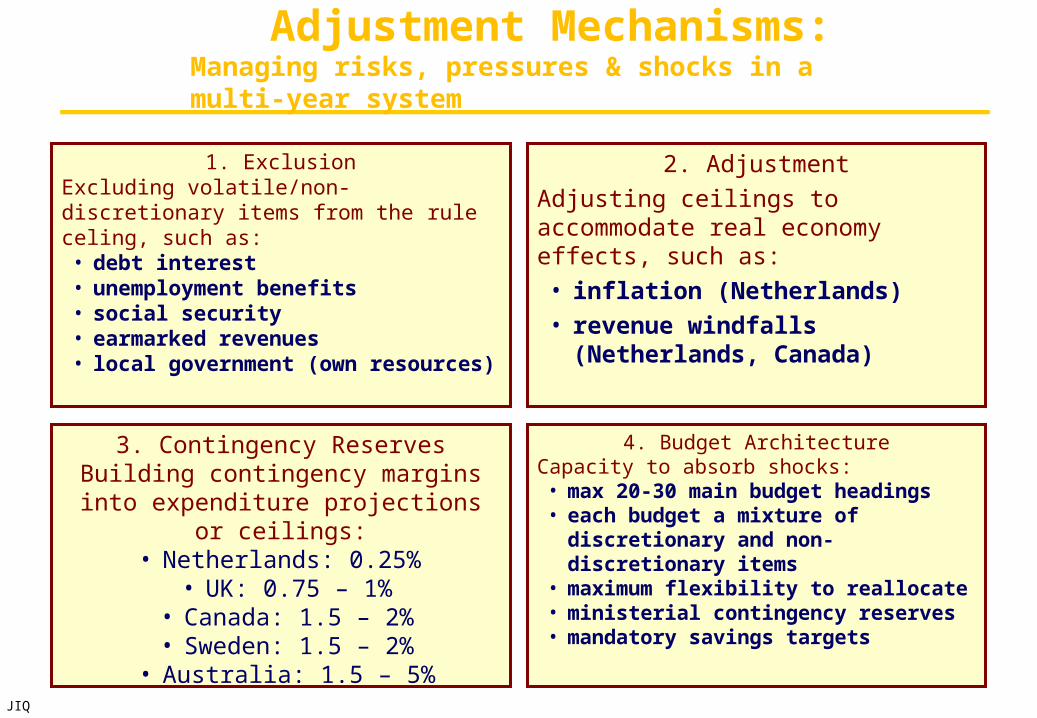

Adjustment Mechanisms:Managing risks, pressures & shocks in a multi-year system

1. ExclusionExcluding volatile/non-discretionary items from the rule celing, such as:

• debt interest • unemployment benefits• social security• earmarked revenues• local government (own resources)

2. Adjustment

Adjusting ceilings to accommodate real economy effects, such as:

• inflation (Netherlands)

• revenue windfalls (Netherlands, Canada)

4. Budget ArchitectureCapacity to absorb shocks:

• max 20-30 main budget headings• each budget a mixture of discretionary

and non-discretionary items• maximum flexibility to reallocate• ministerial contingency reserves• mandatory savings targets

3. Contingency ReservesBuilding contingency margins into expenditure projections or ceilings:

• Netherlands: 0.25% • UK: 0.75 – 1%

• Canada: 1.5 – 2%• Sweden: 1.5 – 2%

• Australia: 1.5 – 5%

JIQ

Once again on public scrutiny

“good finance cannot be attained without intelligent care on the part of the citizens ... due equilibrium between income and outlay will only be found where responsibility is enforced by the public opinion of an active and enlightened community”

Charles Bastable (1927)

![Fiscal Marotta [modalità compatibilità] - Unimoremorespace.unimore.it/.../uploads/sites/12/2014/09/Fiscal_Marotta.pdf · che abbiano accettato il Fiscal compact (nella UE tutti](https://static.fdocumenti.com/doc/165x107/5e505050d7f84203414a333a/fiscal-marotta-modalit-compatibilit-che-abbiano-accettato-il-fiscal-compact.jpg)