Economia dell'Energia e dell'Ambiente.

46

[email protected] Dipartimento di Economia e Management, Università di Ferrara " Economia dell'Energia e dell'Ambiente.” a.a. 2019-20 Lezione 3 – appendice La rivoluzione dello Shale-Gas ed il crollo dei prezzi del Petrolio: effe9 economici, poli<ci e sociali

Transcript of Economia dell'Energia e dell'Ambiente.

Dipartimento di Economia e Management,

Università di Ferrara

" Economia dell'Energia e dell'Ambiente.” a.a. 2019-20

Lezione 3 – appendice

LarivoluzionedelloShale-GasedilcrollodeiprezzidelPetrolio:effe9economici,poli<ciesociali

ISPIEnergyWatch

ISPIEnergyWatchOsservatorioEnergiadell’Is2tutopergliStudidiPoli2caInternazionale,Milano

TheShaleRevolu6onandtheoilslump

Presenta6onbyMassimoNicolazziwithFilippoClô,AnnaRydenandMaFeoVerda

ISPIEnergyWatch

• Introduc6on

• FeaturesoftheShaleRevolu6on

• ThevolumesoftheRevolu6on

• Impactonthegasmarket

• Impactontheoilmarket

• Aboutcrudeoil.Ren6erStates,independentproducersandthepricedilemma

• Oversupply.ThepricedropanditsaLermath

TABLEOFCONTENTS

ISPIEnergyWatch

THEMEANINGOFUNCONVENTIONAL…

Unconven<onalincludes:

• CoalBedMethane

• OilShale

• TightOil/TightGas

• ShaleOil/ShaleGas

• ExtraHeavyOil/OilSands

Introduc6on

Unconven<onalalludestoamethodofproduc6on,nottothequalityofthehydrocarbonsactuallyproduced.

ISPIEnergyWatch

• ExtraHeavyOilandOilShalearebasicallyuntapped

• MaterialvolumesofCBMareproducedmostlyinAustralia,CanadaandtheUS

• Tarsandsaccountfor56%oftheCanadianoilproduc6on‒ approximately2Mbbl/d

• Tight/shalegasaccountsforover40%oftheUSNaturalGasproduc6on‒ approximately300Bcm/year

• Tight/shaleoilUSproduc6onhassurpassed3,5Mbbl/d

…ANDITSPRODUCTIONSIGNIFICANCE

Introduc6on

ISPIEnergyWatch

• Energyintensiveproduc6onmakesTarSandstheenvironmentallymostcontroversialunconven6onalproduc6on

• Methodsofproduc6oninclude:‒ Surfacemining(openpit)‒ CHOPS(ColdHeavyOilProduc6onwithSands)‒ CSS(CyclicSteamS6mula6on)‒ SAGD(SteamAssistedGravityDrainage)

• ThanksmainlytoTarSands,Canadaranksasthethirdcountryworldwideforprovedoilreserves(over174thousandmillionbarrels)

TARSANDS

Introduc6on

ISPIEnergyWatch

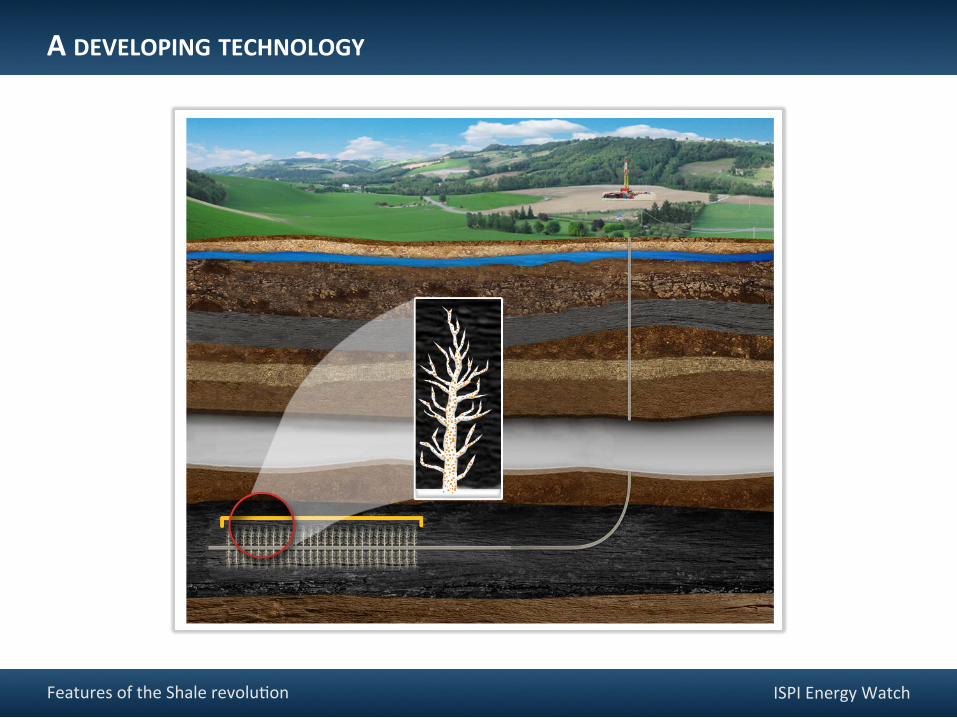

• Adevelopingtechnology

• Anewproduc6onmodel

• AnAmericanstory

FeaturesoftheShalerevolu6on

THESHALEREVOLUTION:COMMONFEATURES

ISPIEnergyWatch

• Nonewinven6on:‒ afrackingprocesswaspatentedin1949‒ con6nuousprocessupgrade

• Thebreakthroughwasop6misingandcombiningfrackingtechniquesandhorizontaldrilling

• Inparallel,newtechnologicaldevelopmentstoop6misedrillingcontrolhavecontributedtoasteepreduc6onofdrilling6me

FeaturesoftheShalerevolu6on

ADEVELOPINGTECHNOLOGY

ISPIEnergyWatchFeaturesoftheShalerevolu6on

ADEVELOPINGTECHNOLOGY

ISPIEnergyWatch

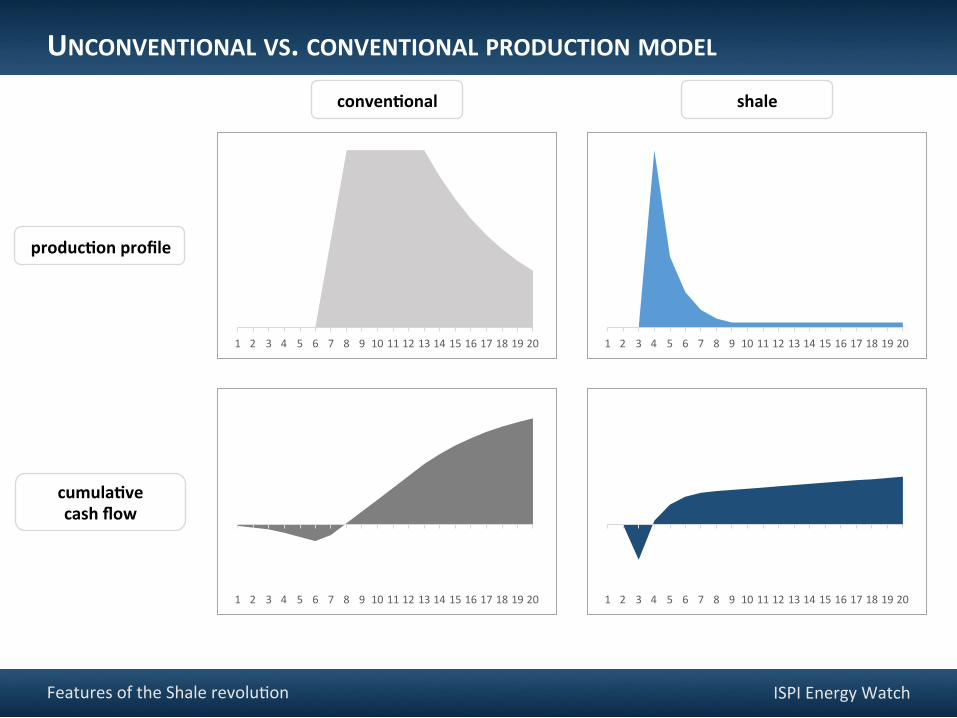

• Conven<onal(exceptforsmall/marginalfields):

‒ longterminvestmentperiod

‒ cashflowdeferredupto5/10yearsfrominvestmentincep6on

‒ stableproduc6onflowforthefirstyearswithoutfurthercapex

• Unconven<onal(shale):

‒ 6metomarket

‒ produc6onandcashflow2-3monthsfromtheinvestmentincep6on

‒ drama6cdecreaseinproduc6onflowaLerfirstyear:60%orevenmore

FeaturesoftheShalerevolu6on

THEPRODUCTIONMODEL:CONVENTIONALVS.UNCONVENTIONAL

ISPIEnergyWatch

produc<onprofile

FeaturesoftheShalerevolu6on

UNCONVENTIONALVS.CONVENTIONALPRODUCTIONMODEL

cumula<vecashflow

1 2 3 4 5 6 7 8 9 1011121314151617181920

conven<onal shale

1 2 3 4 5 6 7 8 9 1011121314151617181920

1 2 3 4 5 6 7 8 9 1011121314151617181920 1 2 3 4 5 6 7 8 9 1011121314151617181920

ISPIEnergyWatch

• Tomaintainorincreaseoverallyearlyshaleproduc6on,theproduc6oncurveofthewellsmandatesthatdrillingandinvestmentbecon<nuous

• Investmentfinancingfordrillingopera6onsisoLenprovidedthroughthehedgingoffutureproduc6on

• Thecombina6onofdrillingintensityandfinancingrequirementsmakesshaleproduc<onvolumespricesensi<veintheshortterm

• Conven<onalproduc6onvolumesarepricesensi6veonlyinthemedium/longterm,i.e.thecurrentpricemayslowreservesreplacementinvestmentbuthasnoimmediateimpactontheproduc6oncapacity

FeaturesoftheShalerevolu6on

THEPRODUCTIONMODEL:DRILLINGINTENSITY

ISPIEnergyWatch

• TheOil&GasUSIndustryhasalonghistoryandcurrentlyemploysalmost600thousandworkers

• Unconven6onaldevelopmentisdrivenbyindependentproducers,notbymajors:theIndependentPetroleumAssocia6onofAmericahasapproximately8.000associates/members

• Legalframework:privatepropertyofnaturalresourcespromoteslocalpopula6onconsensus

• Drillingintensityrequiresanadequatedrillingstock:‒ in2014,thenumberofunconven6onalwellsdrilledintheUSwascloseto5.000

‒ USandCanadahostmorethan60%oftheglobaldrillingstock,andUSalone80%ofthehydraulicfracturingHPworldwide

FeaturesoftheShalerevolu6on

ANAMERICANSTORY

ISPIEnergyWatch

• Drillingintensitycannotcoexistwithpopula6ondensity• Theregulatoryframeworkshouldbereadjusted• Unlessandun6lop6misedprac6cesandadequatedrillingcostsarein

place,produc6oncostswillremainsignificantlyhigherthanintheStates‒ Todate,upto300%inPoland

• Shalegasandshaleoilresourcesarehowever“globallyabundant”(EIA,June2013)

• Russiaranksfirstforoil,ChinaforgasandArgen6naisamajorinboth.Whetheranyofthemwillbecapabletofullyimplementthemodelisaques6onforthebeginningofthenextdecade

FeaturesoftheShalerevolu6on

ANAMERICANSTORY.EXPORTINGTHEMODEL

Environmentalissuesmaybecomealimi6ngfactoralsoforUSexpansion

ISPIEnergyWatch

• TheShaleRevolu6onmaybeassumedtohavestartedin2005:• BushEnergyAct• Presidentfearsforana6on«addictedtooil»

• Fearofoilimportdependencehelpstheintroduc6onofsomeenvironmentalflexibility:

• certainac6vi6esrelatedtofrackingareexemptedfromfederalstandards(Cheney/Halliburtonloophole)

• Theincreaseinoilprice(2001-2008)helpsdevelopingandop6misingdrillingtechniques

• ALer10yearstheoutcomeisspectacular:• Gasproduc6onhasincreasedbyalmost200Bcm/y• Liquidsproduc6onhasincreasedbymorethan4Mbbl/d

ThevolumesoftheRevolu6on

VOLUMESOFTHEUNCONVENTIONALSOURCES

ISPIEnergyWatch

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

USOILCONSUMPTION,PRODUCTIONANDNETIMPORTS

2014figuresareprovisional–Source:elabora6ononBPeEIA

consump6onconsump6on

netimports

produc6on produc6on

USA USA+Canada

ThevolumesoftheRevolu6on

netimports

Mbbl/d Mbbl/d

ISPIEnergyWatch

USGASPRODUCTIONANDCONSUMPTION

2014figuresareprovisional–Source:elabora6ononBPandJODIgas

Bcm

ThevolumesoftheRevolu6on

0

100

200

300

400

500

600

700

800

900

1.000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

produc6onUSA consump6onUSAproduc6onUSA+Canada consump6onUSA+Canada

ISPIEnergyWatch

• “Theoilmarket,liketheocean,isagreatpool”(M.A.Adelmann)

• Thegasmarketremainsregional

• Sametechnology,differentmarkets

• Non-fungibility:‒ Oilconcentratesontransporta6on‒ Gasconcentratesonpower‒ Excep6on:petrochemicals

UNCONVENTIONALOIL/UNCONVENTIONALGAS:THESPLIT

ThevolumesoftheRevolu6on

ISPIEnergyWatch

GASPRICES2010-2015HENRYHUB,EUROPE,ASIA(JAPAN)

Source:EuropeanCommission

ThevolumesoftheRevolu6on

$/MMBtu

US(HHspot) US(Chicagocitygates) UK(NBPspot) Germany(border) Japan(LNGlanded)

2011 2012 2013 2014

ISPIEnergyWatchImpactonthegasmarket

THEGASMARKET:DOMESTICIMPACT

• Gaspowermarketsharefrom18to29%

• Upto3to1ra6opercalorificunityvs.oil(previously5to1withoilat100).Gas-to-oilpoten6allyfeasible

• Re-coupling.NaturalgasandLNGgrowingconsump6onastransporta6onfuelsresuming(marginal)compe66onwithoil

• Boos6ngenergyintensiveindustry

• Thepetrochemicalthreat:upto3to1costofproduc6ondifferen6albetweenEuropeanandUSproducedethylene.

ISPIEnergyWatch

GAS/OILCALORIFICPARITY

EnergyparityforWTI,Brent,andHenryHubnaturalgas–Source:elabora6ononEIA

-

5

10

15

20

25

Jan-00

May-00

Sep-00

Jan-01

May-01

Sep-01

Jan-02

May-02

Sep-02

Jan-03

May-03

Sep-03

Jan-04

May-04

Sep-04

Jan-05

May-05

Sep-05

Jan-06

May-06

Sep-06

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

Sep-09

Jan-10

May-10

Sep-10

Jan-11

May-11

Sep-11

Jan-12

May-12

Sep-12

Jan-13

May-13

Sep-13

Jan-14

May-14

Sep-14

Brent(oil) WTI(oil) HenryHub(gas)$/MMBtu

Impactonthegasmarket

ISPIEnergyWatch

• NorthAmericaproduc6onsurplusandexportinfrastructurewillhavematerialimpactonlytowardsendofdecade

• Marketsharecouldreachbetween10and20%oftheLNGmarket:‒ 4-8%ofinterna6onallytradednaturalgas

• Drama6cimpactongaspricesunlikelyduetomarketshareandtransporta6oncosts

• Marketliquiditywillbeposi6velyaffected

• Exportdirec6onwillbedecidedbyregionalpricedifferen6als

THEGASMARKET:INTERNATIONALIMPACT

Impactonthegasmarket

ISPIEnergyWatch

US+CANADAESTIMATEDGASPRODUCTIONSURPLUSFORECAST

2

76 93

0

200

400

600

800

1.000

1.200

2013 2020 2025

surplus produc6on consump6on

Source:elabora6ononIEA

Bcm

Impactonthegasmarket

ISPIEnergyWatch

LIQUEFACTIONCHAINDIAGRAMANDCOSTS

Source:EIA(2004)

Impactonthegasmarket

ISPIEnergyWatch

• Na6onaleffects:tradebalancesavingsrangingin6mefrom100toover200thousandmilliondollars

• Originofimportsredefinedonthebasisoftherefiningsysteminplace

• Sweetcrudeimportsfullysubs6tutedbyna6onalshaleproduc6on

• Nomaterialimpactonna6onalprices

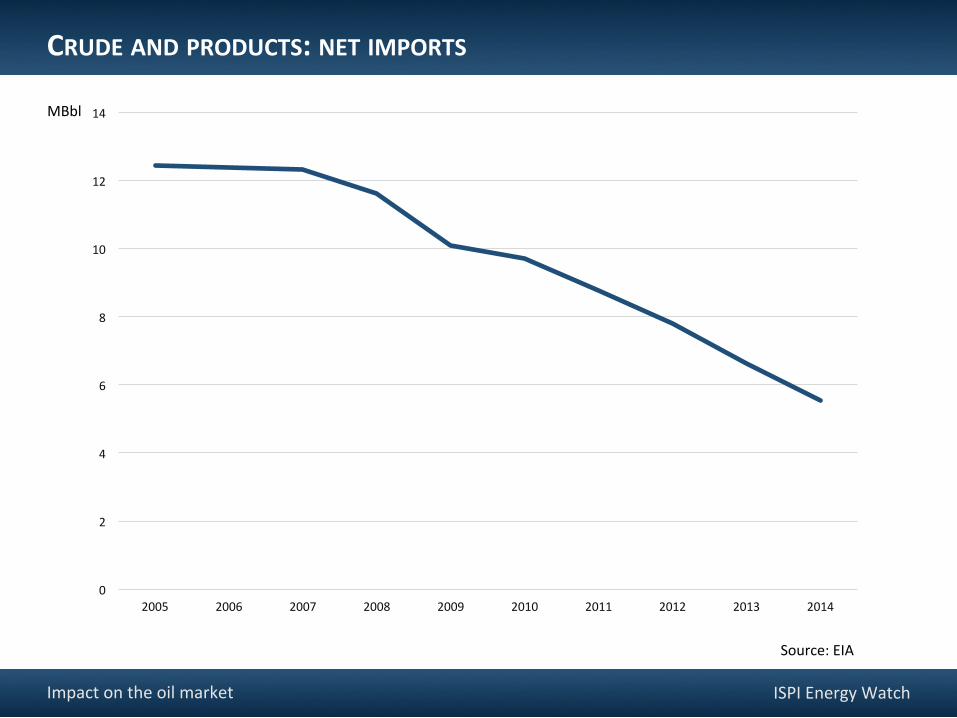

Impactontheoilmarket

THEOILMARKET:DOMESTICIMPACT

ISPIEnergyWatch

• Morethan6Mbbl/ddisappearingfromthe“conven6onalmarket”since2005

• Pricestabilizingeffectduringthe2011-2013disrup6ons(Arabspringetc)

• ThereaLeroneofthemainfactorsofthecurrentslump

• USalreadyanetexporterofoilproducts(over1,5Mbbl/d)

• ExportsofcrudewillnotbesubjecttotheUSbecoming«independent»fromimportsbutwillhappenasaconsequenceoftheunfitnessoftheUSrefiningsystemforthehandlingofhugevolumesofLTO(«LightTightOil»)

THEOILMARKET:INTERNATIONALIMPACT

Impactontheoilmarket

ISPIEnergyWatch

CRUDEANDPRODUCTS:NETIMPORTS

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MBbl

Impactontheoilmarket

Source:EIA

ISPIEnergyWatch

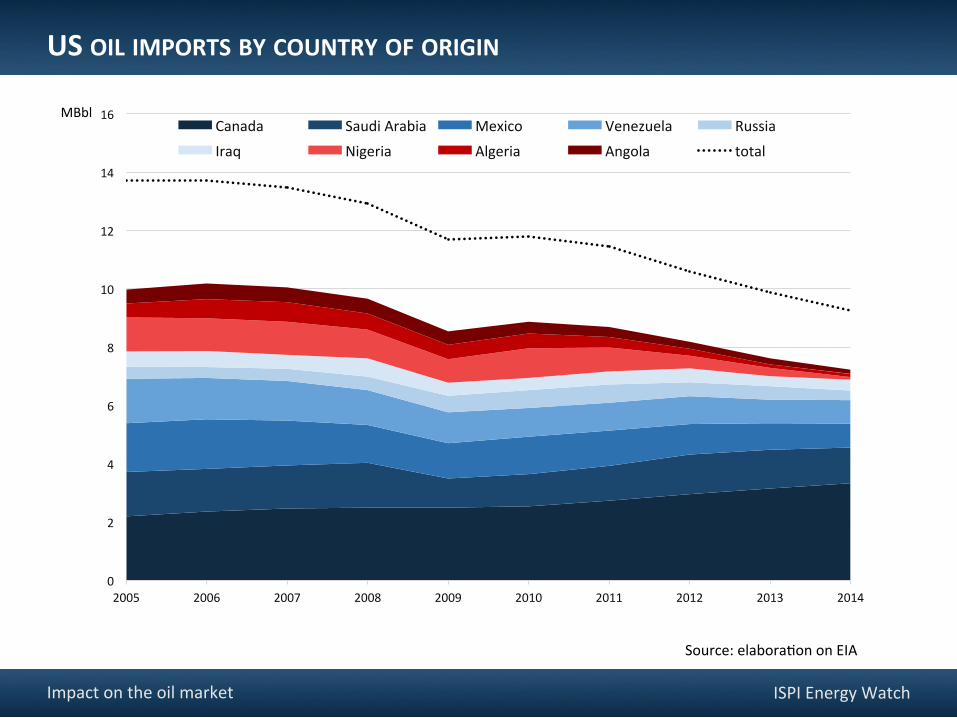

USOILIMPORTSBYCOUNTRYOFORIGIN

MBbl

Source:elabora6ononEIA

0

2

4

6

8

10

12

14

16

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Canada SaudiArabia Mexico Venezuela RussiaIraq Nigeria Algeria Angola total

Impactontheoilmarket

ISPIEnergyWatch

• Produc6oncostsofconven6onaloilremainlowwhencomparedtounconven6onal

• Mostconven6onalproducersrelyheavilyonoilrevenuesfortheirstatebudget,andthereforeneedtobargainasocialbreakevenpricetomaintaininternalstability

• Fallingpricesareathreattotherulingclassandcarryapoten6alfordisrup6onandsocialunrest

• Ina53,8$/bblaverage2015pricescenario,theproducerslossofincomewouldamountoverallto622thousandmilliondollars(asmodelledbyBancaIntesa)

Thepricedilemma

THEPRICEDILEMMA:THERENTIERSTATE

ISPIEnergyWatchThepricedilemma

THERENTIERSTATESBYRENTDEPENDENCE

Source:WorldBank(2012)

Totalnaturalresourcesrents(%ofGDP)

Worldaverage

0

10

20

30

40

50

60

ISPIEnergyWatchThepricedilemma

SOCIALBREAKEVENOILPRICE:COSTOFSTABILITY

Source:elabora6ononIMFandDeutscheBank

currentprices

0

20

40

60

80

100

120

140

160

180

Budgetbreakevenoilprice,for2015$/Bbl

ISPIEnergyWatch

Averageproduc6oncostsarees6matesofabsolutevalues.buttheorderofmagnitudeshouldbetakenasreliable

Thepricedilemma

ECONOMICBREAKEVENOILPRICE:COSTOFPRODUCTION

0

10

20

30

40

50

60

70

USshale Russia SaudiArabia

ISPIEnergyWatch

• Developmentoffrackingtechnologyhasmade6ghtoileconomicundercertainpriceassump6ons‒ S6llfarfromcostcompe66vewithmostoftheconven6onaloil

• ThedrillingintensitymodelreactsswiLlytomarketchanges‒ Investmentcurtailmentshaveanalmostimmediateeffecton

produc6oncapacity

• Produc6oncostsvarybetweenwells‒ Overallthemeaneconomicbreakevenshouldbeinthelow60$/bblrange

Thepricedilemma

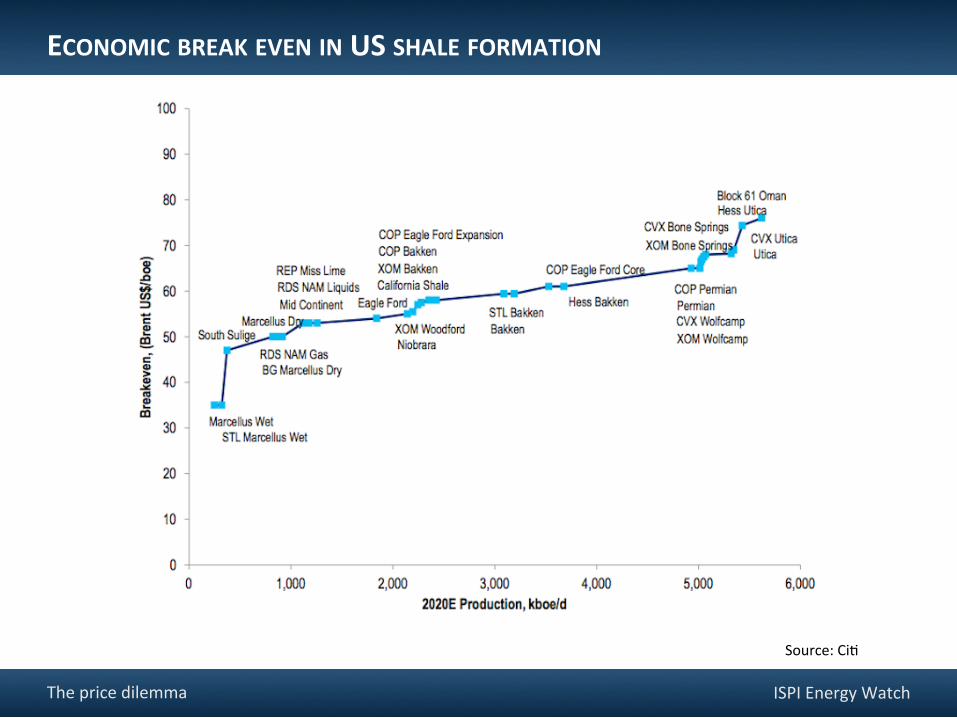

THEPRICEDILEMMA:THEINDEPENDENTPRODUCER

ISPIEnergyWatchThepricedilemma

ECONOMICBREAKEVENINUSSHALEFORMATION

Source:Ci6

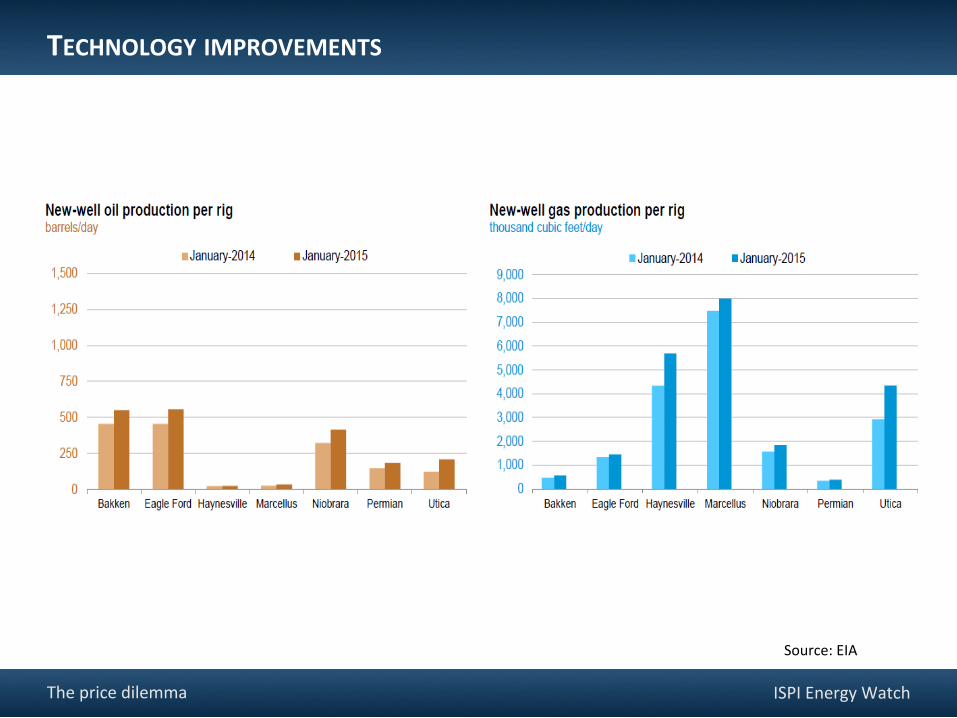

ISPIEnergyWatchThepricedilemma

TECHNOLOGYIMPROVEMENTS

Source:EIA

ISPIEnergyWatch

• UScontribu6on.The2014increaseinUSoilproduc6onalonehassurpassedtheincreaseinglobaldemand(1,16Mbbl/dvs.0,7Mbbl/d)

• Currentforecasts(e.g.PetroleumIntelligenceWeekly)assumethesupplysurplusfor2015tobeinexcessof2Mbbl/d

• Thesurpluswillfillstoragecapacity,totheextentavailable‒ Chinaiscurrentlyimpor6ngmorethan7Mbbl/d,ofwhicharound0,5couldbeforstorage

OversupplyandtheaLermathofthepriceslump

OVERSUPPLY

ISPIEnergyWatch

• Oversupplywillnotbemet,atleastintheshortperiod,byacorrespondingdemandgrowth

• Reducingtheoffermaytakethreedifferentforms

‒ Voluntary,viareduc6onofthecurrentconven6onalflow(OPEC)

‒ Social,viadisrup6onasaconsequenceofsocialunrestwithinaproducer

‒ Economic,viaslowdownandreduc6onoftheUSproduc6on

OversupplyandtheaLermathofthepriceslump

OVERSUPPLY:OUTOFTHESLUMP

ISPIEnergyWatch

• DifficulttoimaginewithoutSaudiinvolvement

• Withoutswingproducer,allotherproducersareforcedtokeepproduc6onatmaximumlevels

‒ Theirbehaviourdoesnotimpactprices,theyareleLtochoosebetweenlowrevenues,ornorevenues

OversupplyandtheaLermathofthepriceslump

DECREASINGSUPPLY:VOLUNTARY

ISPIEnergyWatch

• Nega6veeffectsoflowpricesonna6onalbudgetslimitedonyearlybasisin2014‒ 99,54$/bblin2014vs108,64$/bblin2013

‒ For2015EIApredictsanaverageof68,08$/bbl

• Possibilityofsocialunrestanddisrup6onofproduc6oninsomeofthemostrent-addictedproducerstates

• Impactofdisrup6onsisdebatable

‒ Pastdisrup6ons,e.g.Libya,havebeenfullyamor6sedbytheavailabilityofexcesscapacity

‒ Thepresentoversupplyimpliesthatanyindividualproducer,exceptforthebigthree,isvirtuallyredundantonthemarket

OversupplyandtheaLermathofthepriceslump

DECREASINGSUPPLY:SOCIAL

ISPIEnergyWatch

• No6ght/shaledrillingforoneyearwouldreduceshaleproduc6onby60-65%andreduceoverallUSoilproduc6onbyalmost2Mbbl/d

• Averagebreakevenpricesaremisleadingwhenappliedbybasininsteadofbywell:inmatureprojectswithfullypaidinfrastructurehalfcyclebreakevencostsmayseFlebetween37and45$/bbl

• Technologicaldevelopmentappliedtoa6metomarkettechniquemays6llhaveasignificantshorttermimpactonthebreakevenbenchmark(10%ormore)

• Unlessthepricestabilizesunder60$/bbl,aslowdownoftheforecastedgrowthlooksmorelikelythanasharpdeclineincurrentproduc6on

OversupplyandtheaLermathofthepriceslump

DECREASINGSUPPLY:ECONOMIC

ISPIEnergyWatch

• Mostconven6onalproduc6oncomesfromoldfieldswithlowinvestment/produc6oncosts

• Thecreamingcurvemakesreservereplacementmoretechnicallychallengingandraisesthebenchmarkforbreakeven

• Mostkeyprojectspresentlyinthepipelinehavees6matedbreakevensignificantlyhigherthanshaleproduc6on

• GoldmanSachses6matesthata70$/bblpricewoulddelayorcancel930thousandmilliondollarsworthofupstreamplannedinvestment,represen6ngapoten6alproduc6onof2,3Mbbl/din2020and7,5inin2025

• Theoilpriceslumpmayimpairmediumtermreplacementandmateriallyswingthependulumtowardsundersupply

OversupplyandtheaLermathofthepriceslump

DECREASINGSUPPLY:NEWCONVENTIONALOIL

ISPIEnergyWatch

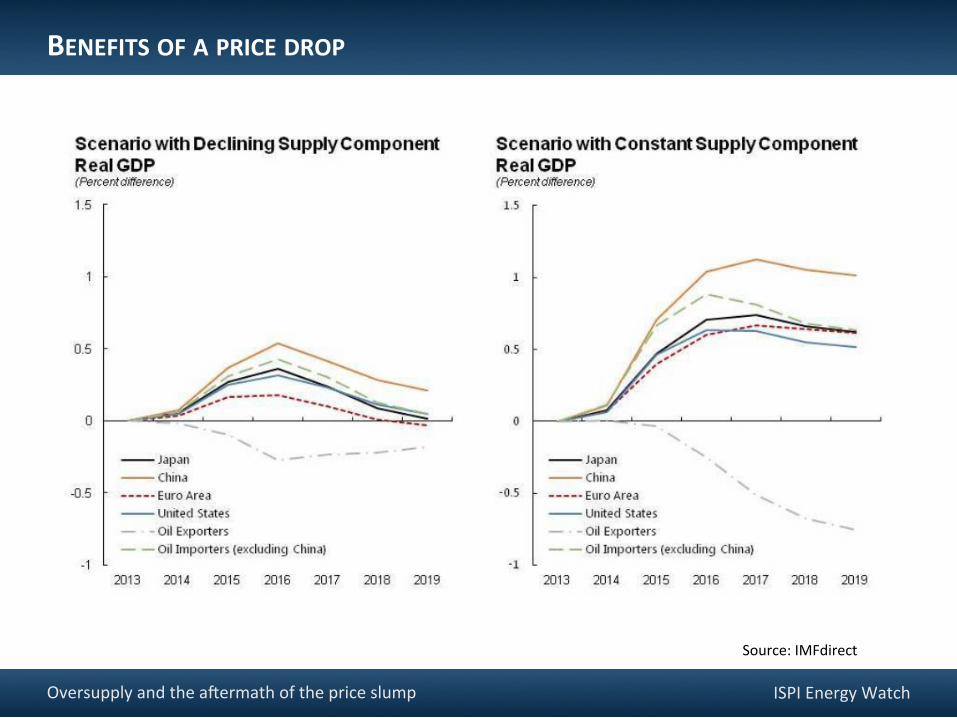

• Mostcurrentscenariosassumeaposi6veimpactofthepricedroponimpor6ngcountriesGDPandtradebalance

• Theextentoftheimpactremainscontroversial

• Thedifferentimpactonindividualcountrieswouldbemainlydrivenbytwofactors:

▫ Energyintensity

▫ Energytaxa6on

OversupplyandtheaLermathofthepriceslump

BENEFITSOFAPRICEDROP

ISPIEnergyWatchOversupplyandtheaLermathofthepriceslump

BENEFITSOFAPRICEDROP

Source:IMFdirect

ISPIEnergyWatch

• TheShaleRevolu6onhascontributedimpetustothepricedrop,andthepricedropwilllikelyslowtheShaleRevolu6on

• Theslowdowninthelongtermwillnotimplyloss,butjustdeferralofproduc6on

• Duetoshorttermpricesensi6vityandavailabledrillingstock,produc6onincreaseshouldregainspeedassoonasfavourablepricesignalshitthemarket

• Theprocessmayhoweverbedelayedandrequirehigher(riskrewarding)pricesshouldthecombina6onofthehedgingprac6ceandofthepresentpricedropresultinaseriouscrisisonthederiva6ves(junkbonds)market

Finalremarks

FINALREMARKS(1):SHALEREVOLUTIONANDPRICEDROP

ISPIEnergyWatch

• Shorttermbenefitstotheeconomiccycle(butpoten6alboosterofEuropeandefla6on)

• Inthemedium-longterm:• Riskofsocialinstabilityaffec6ngalsoneighbouringcountries• Slowdownofreservereplacementinvestmentsandpoten6alforpricevola6lity

• Poten6altemporaryslowdownofgreenpoliciesandincreaseofcarbonenergyconsump6on(beforethepricedrop,IEAforecastwasthatin2040carbonenergysourcessharewoulds6llbenolessthan74%)

Finalremarks

FINALREMARKS(2):PROSANDCONSOFTHEPRICEDROP

Needforpoliciescapableoflimi6ngthedownsizeofcheapoil.Would,amongstothers,acarbontaxhelp?

ISPIEnergyWatch

H.L.Mencken

For every complex problem there is an answer

that is clear, simple, and wrong.

H.L. Mencken